- Specialty & Fine Chemicals

- Floor Screed Market

Floor Screed Market Size, Share, and Growth Forecast, 2026 - 2033

Floor Screed Market by Material Type (Cementitious Screed, Sulfate-free Screeds, Resin Screeds, Calcium Sulfate Screeds), Screed Type (Bonded, Unbonded, Floating, Flowing, Heated), End-Use (Residential, Industrial, Commercial, Infrastructure), and Regional Analysis for 2026 - 2033

Floor Screed Market Share and Trends Analysis

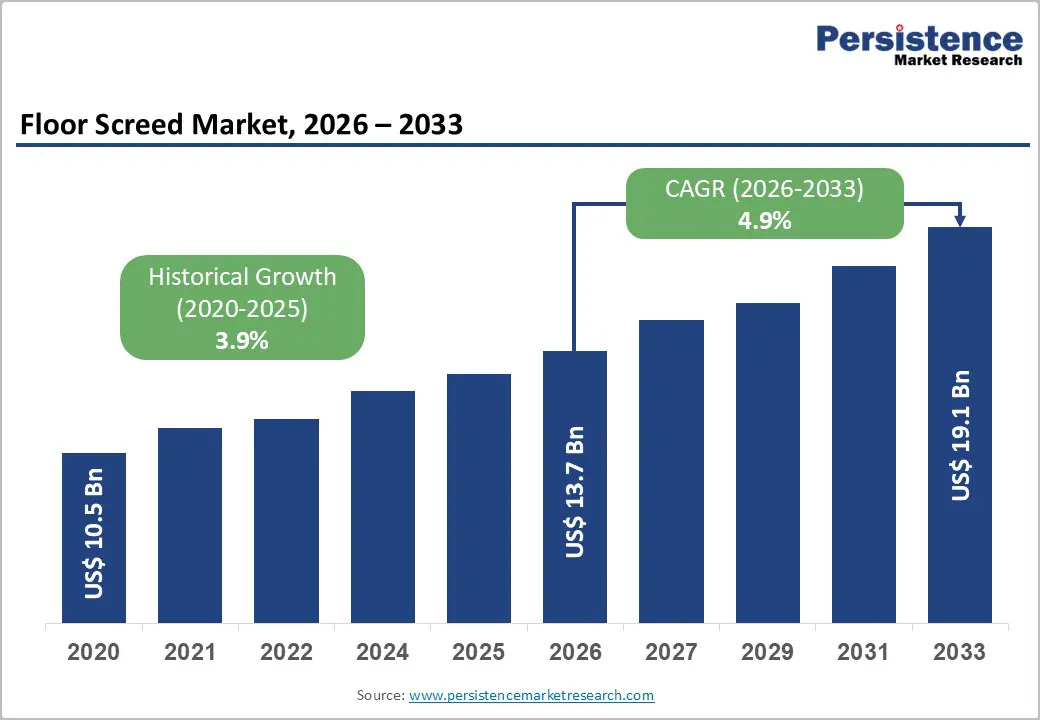

The global floor screed market size is likely to be valued at US$ 13.7 billion in 2026, and is projected to reach US$ 19.1 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026−2033.

The growth trajectory reflects structural expansion in global construction activity, rising urban population density, and the modernization of commercial and infrastructure assets. Rapid urbanization, as documented by the United Nations, increases demand for durable flooring systems across residential and commercial developments. Government-led infrastructure initiatives, including programs administered by the U.S. Department of Transportation (DOT) and the European Commission (EC), stimulate new construction and refurbishment cycles requiring advanced screed formulations.

Technological integration within construction practices, including automated mixing systems, flowing screed solutions, and compatibility with underfloor heating networks, enhances installation efficiency and lifecycle durability. Regulatory emphasis on sustainable construction materials encourages adoption of low-emission, sulfate-free, and resin-modified screeds aligned with environmental frameworks issued by the European Chemicals Agency (ECHA).

Key Industry Highlights

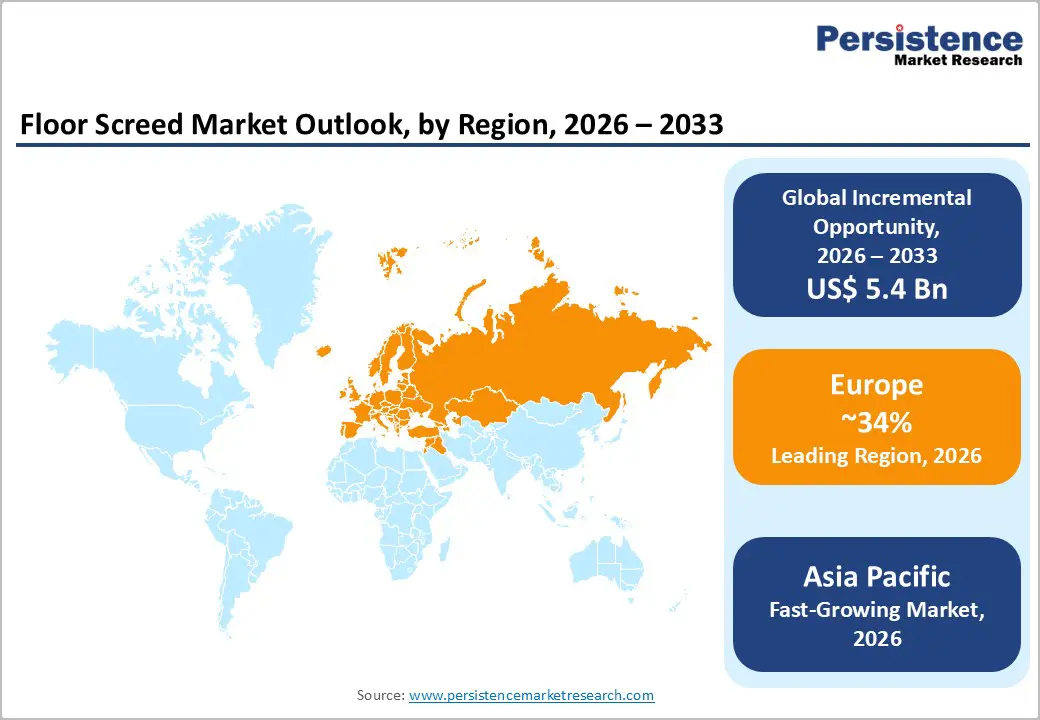

- Dominant Region: Europe is set to dominate the market share with nearly 34% in 2026, driven by advanced standards, strict codes, and high-performance screed demand.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by urbanization and rising screed demand.

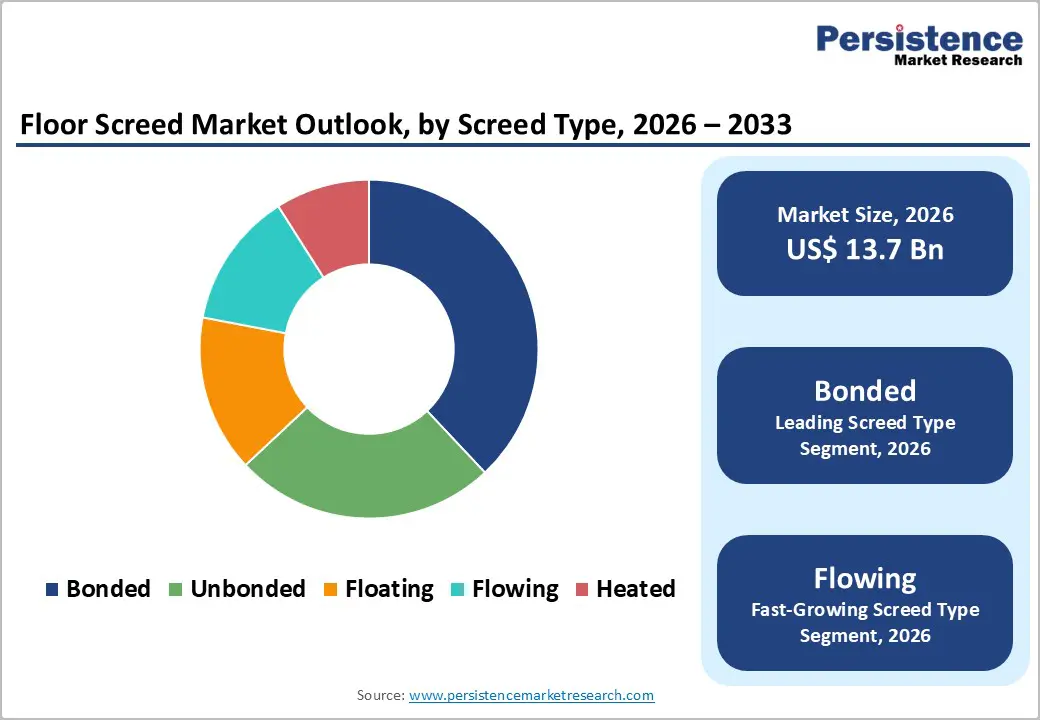

- Leading Screed Type: Bonded screed is poised to lead with around 38% share in 2026, favored for its strong adhesion, durability, and suitability for refurbishment and high-traffic projects.

- Fastest-growing Screed Type: Flowing screed is projected to grow the fastest between 2026 and 2033, driven by automation, self-leveling, and efficiency gains in heated flooring and fast-track projects.

- January 2026: Cemfloor expanded its liquid screed range with Fastrack and Durafibre for faster drying and higher strength.

| Key Insights | Details |

|---|---|

|

Floor Screed Market Size (2026E) |

US$ 13.7 Bn |

|

Market Value Forecast (2033F) |

US$ 19.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rapid Growth in Construction Activity

Strong expansion in building projects drives demand for floor screed since it plays a foundational role in preparing subfloors for final surface finishes in both commercial and residential properties. Increased permits for new construction and upgrades to existing structures create larger volumes of concrete subfloors that require levelling and strength control, which contractors address through screed application. Growing infrastructure work, such as transit hubs, healthcare facilities, and education campuses, emphasizes precision flooring systems that withstand higher loads and traffic, directing procurement toward quality screed solutions during the early stages of project planning. In environments where finish materials such as tile or engineered flooring must perform without uneven wear, specification of an appropriate screed supports schedule adherence and compliance with building codes.

According to the United States Census Bureau, total construction spending reached a seasonally adjusted annual rate of US$ 2,175.2 billion in October 2025, reflecting sustained expansion in public and private building activity that relies on structured floor preparation processes. Elevated capital allocation to residential, commercial, and institutional assets drives broader demand for compliant flooring systems across new development and renovation pipelines. Coordination between structural concrete placement and finishing trades underscores the operational importance of screed in delivering flat, load-bearing substrates that align with engineering and architectural specifications.

Integration with Underfloor Heating Systems

Embedding underfloor heating systems into floor structures increases demand for screed since it serves as a thermal mass and conductive layer that efficiently transfers heat from heating elements to the occupied space. The U.S. Department of Energy (DOE) notes that radiant floor systems deliver heat directly through the floor surface, leveraging radiant heat transfer to provide comfort more efficiently than many conventional systems, thereby reducing duct or distribution losses. A well-designed screed encapsulates hydronic or electric heating elements and ensures uniform heat distribution across the floor, thereby significantly reducing energy consumption and operational costs.

Government incentives and building codes that support energy-efficient home improvements further drive the adoption of radiant heating solutions. The U.S. Internal Revenue Service (IRS) updated its Energy Efficient Home Improvement Credit in 2025, outlining requirements for qualifying energy-saving upgrades and encouraging investments in efficient heating technologies, including radiant systems embedded within floor structures. Such policy frameworks stimulate builders and homeowners to integrate underfloor heating paired with screed layers during construction or renovation, as part of broader strategies to meet thermal comfort, energy cost reduction, and sustainability targets.

Competition from Alternative Flooring Solutions

Alternative flooring systems are increasingly displacing traditional base preparation methods in many construction and renovation projects due to their ease of installation, lower-skilled labor requirements, and broad functional appeal. Solutions such as luxury vinyl tile (LVT), engineered wood, ceramic tile, and resilient flooring systems often integrate directly onto existing substrates with minimal preparatory work, bypassing the need for extensive leveling or curing that conventional layer-by-layer surface preparation demands. This installation efficiency significantly shortens project timelines and reduces total installed cost, appealing to developers and homeowners facing tight schedules and budget constraints.

The structural simplicity and modular design of many alternative floor coverings also align with evolving building standards and homeowner preferences for durability and low ongoing maintenance, further diminishing reliance on thicker, process-intensive floor substrate preparations. Contemporary materials often incorporate performance attributes such as waterproofing, impact resistance, and aesthetic versatility that reduce the perceived marginal benefit of traditional leveling techniques. In markets prioritizing retrofit work over new construction, these attributes become especially relevant when existing substrates are serviceable but uneven, enabling installers to deliver high-quality finished surfaces without extensive preliminary surface enhancements.

Installation Complexity and Moisture Risks

Proper floor surface preparation requires rigorous moisture assessment and management before installing final flooring materials. Construction standards such as the U.S. Environmental Protection Agency (EPA)’s Moisture Control Guidance for Building Design, Construction and Maintenance emphasize that moisture can move into and within a building through air movement, diffusion and heat transfer, and that failing to control this movement undermines structural durability and indoor environmental quality. Skilled teams must measure relative humidity and moisture emissions to ensure the substrate is dry enough to meet manufacturer requirements for subsequent layers.

Moisture from ground infiltration or trapped construction water poses a threat to the long-term performance of flooring finishes and interior environments. Industry benchmarks show that a standard cementitious floor layer can require approximately four months of drying under controlled conditions before it reaches an acceptable relative humidity level for final finishes. Project sequences that fail to accommodate this timeframe risk adhesive failures, delamination, warped surfaces or mold growth, all of which drive corrective costs and schedule overruns.

Integration with Energy-Efficient and Smart Building Systems

Alignment of floor screed solutions with energy-efficient and smart building frameworks represents a structural shift in construction priorities toward performance-driven design. Modern commercial and residential developments increasingly incorporate underfloor heating, embedded sensors, and centralized building management systems that rely on stable thermal mass and consistent conductivity within the flooring layer. High-performance screed formulations support low-temperature radiant systems by enabling uniform heat distribution, faster thermal response, and reduced energy intensity per square foot. Smart building platforms integrate occupancy sensors, programmable thermostats, and automated climate controls that require compatible subfloor systems capable of maintaining dimensional stability under variable thermal cycles.

Regulatory emphasis on energy conservation, decarbonization targets, and green building certifications strengthens demand for materials that contribute measurable efficiency gains. Developers prioritize specifications that enhance Energy Performance Certificates, Leadership in Energy and Environmental Design (LEED), and other sustainability benchmarks tied to asset valuation and financing access. Screed systems engineered for moisture control, crack resistance, and thermal optimization align with digital monitoring tools used in smart infrastructure, supporting predictive maintenance and lifecycle performance tracking. Growth in connected buildings, electrification of heating systems, and data-driven facility management further expands application scope across offices, healthcare facilities, logistics hubs, and multifamily housing.

Eco-friendly and Low-Emission Screed Formulations

Government policy and regulation are increasingly shaping building material selection by requiring transparency and a reduction in life-cycle emissions. The European Union (EU)’s Energy Performance of Buildings Directive (EPBD) mandates that the life-cycle global warming potential (GWP) of new buildings must be calculated and disclosed on energy performance certificates, effectively pushing developers and product manufacturers to prioritize low-emission, low-embodied-carbon materials in construction projects. This regulatory framework creates a measurable demand signal for products with reduced greenhouse gas intensities throughout manufacture, transport, installation, and disposal, supporting wider adoption of sustainable material solutions.

Market demand is further reinforced by national sustainability initiatives and public procurement policies that tie funding and project eligibility to climate criteria. In the United States, the Federal Buy Clean Initiative directs federal funding toward projects that use substantially lower embodied-carbon materials, such as lower-emission concrete and steel, thereby expanding the economic case for suppliers to reformulate products and scale greener alternatives. This policy-driven environment of emissions accounting and procurement incentives reduces barriers to advanced formulations and encourages innovation in materials science, aligning product development with climate goals and shifting industry standards toward sustainability.

Category-wise Analysis

Screed Type Insights

Bonded screed is likely to be the leading segment with a projected 38% market share in 2026, due to strong structural adhesion to concrete substrates and suitability for refurbishment projects. Contractors rely on bonded systems for thin-layer applications in renovation cycles across Europe and North America. The reliable bond ensures long-term durability and minimizes risks of delamination, which is critical in high-traffic areas and multi-story buildings. Established installation standards allow workers to follow consistent protocols, reducing variability in mechanical performance. Predictable compressive and flexural strength make bonded screed preferred for projects requiring precise load-bearing capacity, while compatibility with different finishing materials further reinforces sustained adoption across residential, commercial, and industrial construction projects.

Flowing screed is expected to grow the fastest between 2026 and 2033, driven by automation in application processes and compatibility with heated flooring systems. Pump-applied solutions reduce labor intensity and improve surface regularity. Commercial developers adopt flowing systems to meet tight project timelines and quality benchmarks. Consistent thickness and self-leveling properties enhance the efficiency of subsequent flooring installations, such as tiles, wood, or resilient materials. Integration with digital moisture-measurement tools and rapid-drying additives enables projects to accelerate handover schedules without compromising performance.

End-User Insights

The residential segment is expected to hold a dominant position, accounting for an anticipated 44% of the floor screed market revenue share in 2026, driven by large-scale housing developments, renovation cycles, and rising adoption of underfloor heating systems. Urban expansion and multi-unit residential projects generate recurring demand for bonded and floating screed systems. Contractors leverage standardized techniques to maintain consistency across numerous units, ensuring durability and surface quality. Homeowners increasingly prefer solutions that enable energy-efficient heating integration and fast-drying properties. Cost efficiency, the availability of local materials, and familiarity with installation methods reinforce the widespread use of screed in residential construction, including both new builds and retrofit projects.

The infrastructure segment is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by government investment in transportation hubs, logistics corridors, and public facilities. Infrastructure assets require durable, load-bearing substrates with extended lifecycle performance. Large-scale projects prioritize mechanical strength, abrasion resistance, and chemical stability to withstand high traffic loads. Capital allocation through national infrastructure frameworks increases specification of high-strength and resin-modified screeds suitable for heavy-duty environments. Consistent quality, regulatory compliance, and long-term maintenance efficiency make these solutions essential for airports, rail stations, warehouses, and public buildings requiring reliable, long-lasting flooring systems.

Regional Insights

North America Floor Screed Market Trends

The market in North America is positioned for steady growth in floor screed adoption, aided by mature construction industries, high-value residential projects, and extensive commercial development. Multi-unit residential buildings, office complexes, and retail spaces drive demand for bonded and flowing screed systems that ensure structural integrity, surface precision, and long-term durability. The adoption of underfloor heating in high-end residential and commercial projects increases demand for screeds compatible with energy-efficient systems. Skilled contractors and established installation standards enable consistent performance across refurbishment and new-build projects. Public facility upgrades, including educational campuses and healthcare infrastructure, emphasize abrasion resistance, chemical stability, and predictable mechanical strength, further reinforcing adoption. Advanced formulations, such as resin-modified and rapid-drying screeds, offer flexibility for thin-layer applications and fast project turnaround, meeting stringent construction timelines and quality requirements.

Technological integration and sustainable material selection further drive market development. Pump-applied and self-leveling systems reduce labor intensity and improve surface uniformity, while digital moisture measurement tools enhance installation accuracy. Manufacturers focus on eco-friendly solutions with a low carbon footprint to align with energy-efficiency regulations and sustainability incentives, thereby promoting wider acceptance in public and private projects. Renovation cycles of aging building stock and high population density in urban corridors create recurring demand for reliable floor preparation solutions. Availability of local raw materials, mature distribution networks, and contractor proficiency ensure efficient project execution and cost optimization.

Europe Floor Screed Market Trends

Europe is expected to dominate with an estimated 34% of the floor screed market share in 2026, reflecting strong regulatory frameworks, advanced construction standards, and widespread adoption of high-performance flooring systems. High-rise developments and multi-unit residential projects drive consistent demand for bonded and flowing screed systems that emphasize structural integrity, durability, and surface precision. Stringent building codes focused on thermal insulation, energy efficiency, and lifecycle performance encourage the use of screeds compatible with underfloor heating and low-emission materials. Preference for premium formulations that provide resistance to wear, chemical exposure, and long-term dimensional changes further strengthens adoption, particularly in commercial and public infrastructure projects where performance reliability is critical.

Demand is reinforced by extensive refurbishment and retrofit activity across aging building stock. Thin-layer applications, rapid-drying products, and resin-modified screeds provide efficient solutions for renovation projects with time constraints or structural limitations. Automation in pumping and digital moisture measurement systems enhances consistency and reduces labor intensity, improving project efficiency. Developers and contractors favor standardized installation protocols and predictable mechanical strength to minimize risk in high-value projects. Well-established supply chains, easy access to raw materials, and mature distribution networks enable faster project mobilization and optimized cost management.

Asia Pacific Floor Screed Market Trends

Asia Pacific is forecast to be the fastest-growing floor screed market between 2026 and 2033, driven by rapid urbanization, expanding industrial zones, and large-scale housing programs in countries such as India, China, and Indonesia, which generate recurring demand for durable, efficient floor preparation systems. Multi-unit residential developments, commercial complexes, and logistics facilities increasingly adopt automated pumping solutions and self-leveling screeds to meet tight project schedules while maintaining uniform surface quality. Investment in energy-efficient buildings drives the selection of screeds compatible with underfloor heating and sustainable materials. Infrastructure projects, including airports, rail stations, and smart city initiatives, specify high-strength, resin-modified formulations designed for long-term load-bearing performance, abrasion resistance, and chemical stability.

High population density and rapid economic growth in these countries accelerate demand for both new construction and renovation projects. Digital moisture testing, rapid-drying additives, and automated leveling tools enable precise and time-efficient installation in urban high-rise and industrial developments. Locally produced, cost-effective materials support competitive pricing without compromising quality, facilitating adoption across residential, commercial, and infrastructure segments. Governments promote sustainable and energy-efficient building practices through incentives and regulatory frameworks, further boosting demand. Frequent refurbishment cycles in high-density housing and public buildings generate consistent consumption of bonded and flowing screeds.

Competitive Landscape

The global floor screed market structure reflects moderate concentration with global construction chemical companies controlling significant share, while regional producers address localized demand. Leading players such as Sika, Saint-Gobain, MAPEI, Cemex, Holcim, BASF, Fosroc, and Ardex Group leverage diversified product portfolios to maintain revenue dominance across residential, commercial, and infrastructure segments. Emphasis on high-performance screeds, including bonded, flowing, and resin-modified formulations, allows these companies to cater to evolving construction requirements. Strategic investments in research and development enable continuous formulation innovation, enhancing mechanical strength, rapid-drying properties, and compatibility with underfloor heating systems. Localized manufacturing facilities and distribution networks allow quick delivery and technical support, ensuring adherence to project timelines and regional regulatory standards.

Competitive strategies focus on innovation, distribution reach, and contractor engagement. Companies differentiate through high-value product features, sustainable formulations, and advanced application technologies, enabling penetration into high-density urban projects and large-scale infrastructure initiatives. Contractual alliances with construction firms, design consultants, and public authorities strengthen market presence and secure long-term procurement agreements. Regional producers complement this landscape by addressing specific cost-sensitive and smaller-scale projects, ensuring localized demand is met efficiently. Digital tools, technical support services, and knowledge-sharing initiatives enhance brand reputation and customer loyalty, creating barriers to entry for smaller competitors.

Key Industry Developments

- In November 2025, LKAB Minerals launched Gypsol Zero Laitance (ZL), a low-carbon, laitance-free liquid floor screed that accelerates installation and supports sustainable building standards such as the Future Homes Standard and BREEAM by significantly cutting embodied carbon and labor needs.

- In September 2025, Somero® introduced the SRS-4 Laser Screed® in India, a compact laser-guided screed machine designed to significantly improve accuracy, efficiency, and cost-effectiveness for large-scale concrete finishing projects.

- In April 2025, Tremco announced re-engineered TremSmooth screeds, including the SX300 TremSmooth HP and SX302 TremSmooth MT, offering faster walk-on times, improved flow and enhanced application properties to deliver higher-quality flooring finishes more efficiently for contractors and distributors.

Companies Covered in Floor Screed Market

- Sika AG

- Saint-Gobain

- MAPEI

- Cemex

- Holcim

- BASF

- Fosroc, Inc.

- Ardex Group

- UltraTech Cement Ltd.

- Flowcrete Group Ltd.

Frequently Asked Questions

The global floor screed market is projected to reach US$ 13.7 billion in 2026.

Rising construction activity, urbanization, underfloor heating adoption, and demand for durable, efficient flooring solutions are driving the market.

The market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Strong demand for low‑carbon, fast‑drying, self‑leveling, and technologically advanced screeds is opening new opportunities for market players.

Some of the key market players include Sika AG, Saint-Gobain, MAPEI, Cemex, Holcim, BASF, Fosroc, Inc., and Ardex Group.