- Advanced Materials

- Flooring Market

Flooring Market Size, Share, Trends, Growth, Regional Forecasts 2026 to 2033

Flooring Market by Product Type (Resilient Flooring (Vinyl Tiles, Linoleum, Rubber, Others); Non-resilient Flooring (Ceramic Tiles, Wood, Laminate, Others) and Carpets & Rugs), End-user (Residential, Commercial), by Regional Analysis, 2026 - 2033

Flooring Market Share and Trends Analysis

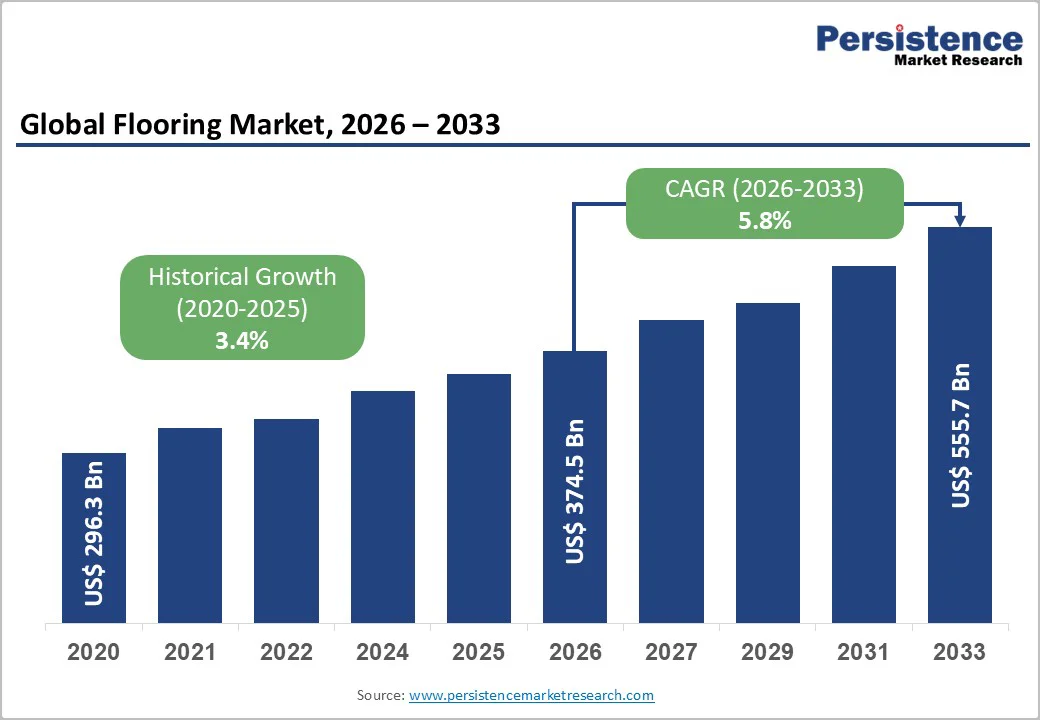

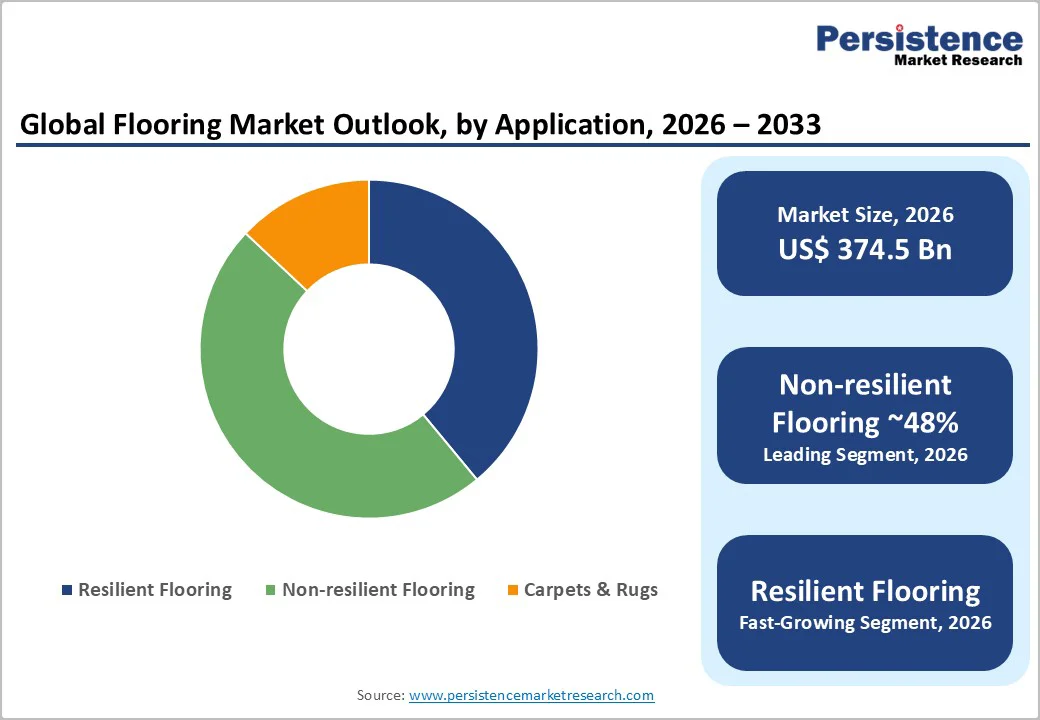

The global flooring market size is likely to value at US$374.5 billion in 2026 and is projected to reach US$555.7 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

This expansion reflects sustained demand across residential and commercial construction sectors, driven by rapid urbanization, rising disposable incomes, and increasing renovation activities. The market's growth trajectory is supported by technological advancements in resilient flooring materials, particularly Luxury Vinyl Tile (LVT) and Stone Plastic Composite (SPC) products, which offer enhanced durability and aesthetic versatility.

Key Industry Takeaways:

- Segment Leadership: Non-resilient flooring commands over 48% market share in 2026, while resilient categories such as LVT, SCP demonstrate the fastest growth at 8% CAGR through 2033.

- End-User Dominance: Residential segment accounts for over 55% market share in 2026, though commercial applications represent the fastest-growing opportunity segment.

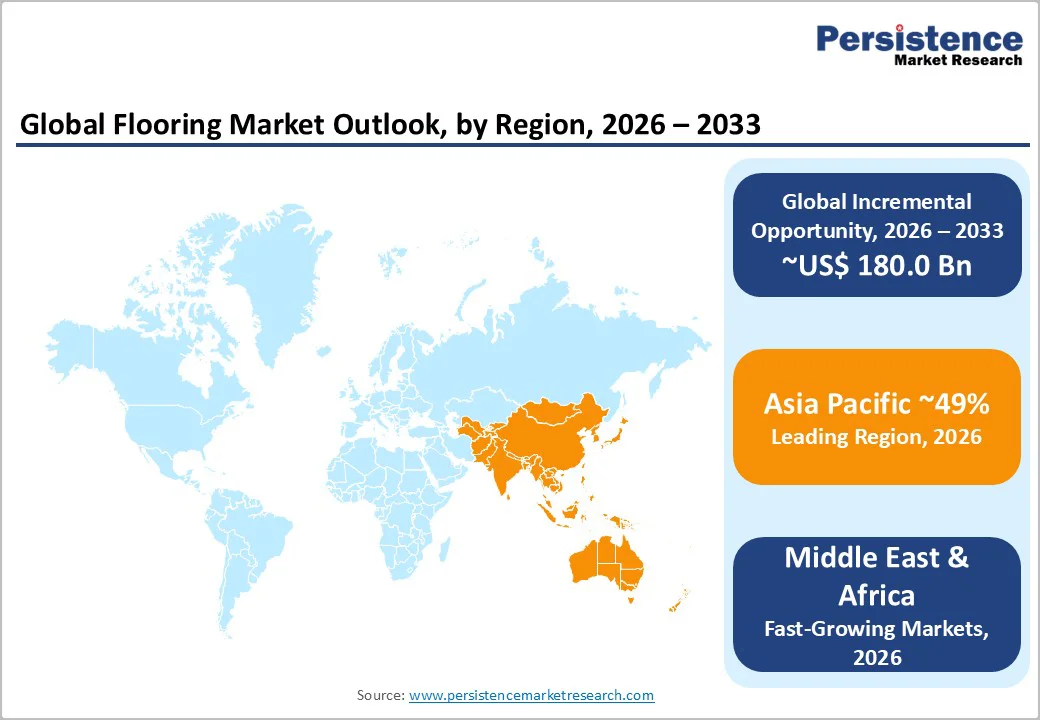

- Regional Growth: Asia Pacific leads with 50% global market share in 2026; India emerges as the fast-growing country at over 7.5% CAGR, exceeding US$20 billion by 2033.

- Innovation Impact: Luxury Vinyl Tile captures over 40% share in the vinyl resilient flooring revenue, with waterproof and sustainable product launches driving premium segment growth.

- Leadership Consolidation: Mohawk Industries consolidates market leadership with strategic acquisitions adding ~$600 million annual sales (2022 - 2023), including Brazil's Elizabeth and Mexico's Vitromex, while introducing PVC-free sustainable products; Shaw Industries expands LVT/SPC capacity with US$90 million investment, doubling Ringgold facility production by 2026.

- Supply Chain Resilience: Raw material price volatility and logistics disruptions remain critical challenges, prompting leading manufacturers to invest in domestic production capacity and resilient supply chain models.

| Key Insights | Details |

|---|---|

| Flooring Market Size (2026E) | US$374.5 Bn |

| Market Value Forecast (2033F) | US$555.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.4% |

Market Dynamics and Growth Factors

Driver - Rapid Urbanization and Residential Construction Growth

Rapid urbanization globally, particularly in Asia Pacific, Latin America, and emerging African markets, is driving substantial demand for residential, commercial, and industrial flooring materials. The United Nations estimates that urban populations will comprise 68% of the global population by 2050, from approximately 56% in 2025, creating persistent demand for housing infrastructure and commercial developments.

Government-backed housing initiatives, notably India's "Housing for All" program and China's ongoing urbanization projects, are systematically expanding construction activity. Global investment in construction infrastructure reached unprecedented levels in 2024 - 2025, with commercial real estate absorbing significant capital across office, healthcare, and retail sectors. This construction boom directly translates to sustained flooring demand across all material categories.

Residential Remodeling and Renovation Market Expansion

The residential segment dominates the flooring market with over 55% market share in 2026, driven by homeowner investment in property upgrades and aesthetic improvements. Rising disposable incomes in developed markets and the expanding middle class in emerging economies have increased consumer spending on home enhancement projects.

The U.S. residential remodeling market, which represents a critical bellwether, demonstrated resilience through 2024 - 2025 despite economic headwinds, with consumers prioritizing floor replacements and renovations. The preference for premium flooring solutions, including luxury vinyl tiles (LVT) and engineered wood products, reflects consumer willingness to invest in higher-quality, longer-lasting materials that enhance property value.

Technology-Driven Product Innovation and Design Advancement

Technological breakthroughs in flooring manufacturing, including digital printing, embossing-in-register technology, rigid core composite development, and AI-optimized production processes, have fundamentally expanded product differentiation and accessibility. Manufacturers now achieve hyper-realistic wood and stone textures on synthetic materials, creating "luxury on a budget" value propositions that appeal to cost-conscious consumers.

Digital printing capabilities have reduced manufacturing waste by enabling on-demand customization, while rigid stone plastic composite (SPC) and wood plastic composite (WPC) technologies provide superior dimensional stability and durability. These innovations have positioned resilient flooring, particularly LVT, as the fastest-growing category, expanding from traditional niche applications into mainstream residential and commercial markets.

This shift is driven by LVT/SPC’s ability to realistically mimic wood and stone at a lower installed cost, combined with high wear resistance and ease of installation. Rapid acceptance in both residential renovation and commercial spaces (offices, retail, hospitality, healthcare) is accelerating category mix upgrades, lifting overall market value even in relatively mature volume environments.

Restraints - Raw Material Volatility, PVC Scrutiny, and Compliance Costs

Resilient flooring relies heavily on PVC, resins, and petrochemical derivatives. Market analyses highlight volatile raw material prices as a major restraint, as swings in vinyl chloride, plasticizers, and rubber directly pressure manufacturer margins and end-user pricing.

At the same time, tighter EU and national frameworks on VOC emissions and toxic substances require extensive testing and reformulation of flooring products, increasing compliance costs and extending time to market. Emerging trade actions and customs enforcement on certain SPC and vinyl imports have also created uncertainty in parts of the supply chain, raising working capital and inventory risk.

Cyclical Exposure to Housing, Interest Rates, and Renovation Cycles

Flooring demand is tightly linked to new housing starts and renovation cycles. In 2024, several leading producers reported volume declines in residential flooring, particularly in Europe and North America, citing elevated interest rates, inflation and weaker renovation activity.

Tarkett, for example, noted that high mortgage rates and inflation sharply reduced new construction and renovation projects in Europe, with residential volumes underperforming even as certain commercial segments (offices, health, education) remained more resilient. This cyclicality translates into earnings volatility for flooring manufacturers and can delay capital investment and innovation during downturns.

Market Opportunities

Low-carbon, Circular, and PVC-free Flooring Solutions

Global climate goals and corporate ESG commitments are creating a premium segment for low-carbon and circular flooring. WorldGBC estimates buildings are responsible for 39% of energy-related CO2 emissions, with 11% from materials and construction (embodied carbon). Leading flooring manufacturers are responding to this initiative. Interface launched the world’s first carbon-negative carpet tile and continues to push carbon-storing backings.

Tarkett reports a 23% reduction in scope 1-3 emissions vs. 2019 and uses ~19% recycled raw materials in volumes. Shaw has made about 90% of its products Cradle to Cradle Certified® and introduced PVC-free, closed-loop, recyclable resilient flooring (EcoWorx Resilient).

These moves signal a scalable opportunity in green building certifications (LEED, BREEAM, WELL) and public procurement, where sustainable flooring can command higher margins and win specifications.

Sustainability and Eco-Friendly Product Differentiation

The global eco-friendly flooring market is experiencing unprecedented growth with a projected CAGR of 7.85% through 2032, as consumers increasingly prioritize environmental impact and indoor air quality. Demand for products incorporating recycled materials, bamboo, cork, bio-based composites, and reclaimed wood continues to accelerate, particularly in developed markets where regulatory tailwinds support premium sustainable product pricing.

Manufacturers implementing circular economy models, including take-back programs, material passports, and design-for-disassembly approaches, achieve competitive differentiation while building consumer loyalty. Corporate sustainability commitments create enterprise flooring procurement opportunities with specifications favoring eco-certified products.

Category-wise Insights

Product Insights

Non-resilient flooring dominates the global market, accounting for over 48% of market share in 2026, with ceramic tiles leading the segment. Ceramic tiles captured 50% of the non-resilient market in 2026, driven by their durability, water resistance, and cost-effectiveness in high-moisture applications.

Wood and laminate flooring maintain strong positions in residential markets, particularly in North America and Europe, where aesthetic preferences favor natural material appearances. The segment benefits from established manufacturing infrastructure, widespread distribution networks, and consumer familiarity, though growth rates are moderate compared to emerging resilient categories.

In Asia Pacific, non-resilient flooring will still exceed 55% share in 2026, led by ceramic tiles for residential, retail, and institutional buildings, especially in China, India, Turkey, and Russia, where tiles remain the default option for cost, durability, and climate reasons. In price-sensitive markets such as India and Southeast Asia, ceramic tiles constitute the most preferred flooring type, reinforcing non-resilient’s role as the volume backbone of the global market.

Price volatility in timber and stone materials, along with installation complexity, presents ongoing challenges for non-resilient product adoption.

Fast-growing Segment: Resilient Flooring

Resilient flooring categories demonstrate exceptional growth momentum, with Luxury Vinyl Tile (LVT) and Stone Plastic Composite (SPC) driving category expansion. LVT alone accounts for over 40% of the vinyl resilient flooring revenue, offering waterproof features, acoustic insulation, and diverse design options that appeal to both residential and commercial buyers.

The segment's growth is fueled by technological advancements enabling realistic replication of natural materials at lower price points, combined with DIY-friendly installation systems that reduce labor costs.

Europe and Asia Pacific are also seeing strong LVT/SPC penetration, particularly in multi-family housing, hospitality, and retail, where quick turnaround and acoustic performance are valued. Beyond vinyl, rubber, and linoleum flooring are gaining in healthcare, education, and public buildings because of their low VOC emissions and recyclability, aligning with tightening green-building criteria.

End-user Insights

The residential end-use segment commands the largest market share, accounting for over 55% in 2026. This dominance reflects the scale of global housing construction and renovation activities, driven by population growth, urbanization, and rising living standards. Consumers are increasingly viewing flooring as a critical interior design element, investing in premium materials that enhance property values and overall lifestyle quality.

The segment is leading in the Asia Pacific, where rapid urbanization creates a continuous demand for new housing units, while mature markets such as North America and Europe generate substantial sales driven by renovation. Carpets and rugs capture approximately 40% of the residential market in 2026, though resilient flooring gains share through LVT and waterproof vinyl products.

- New Build vs. Renovation & Retrofit

- Globally, new construction still represents the bulk of installed floor area additions, especially in fast-urbanizing regions. UN data suggest that half of the buildings that will exist in 2050 have not yet been built, underscoring the importance of new-build standards for long-term flooring demand and specification.

- Large infrastructure and housing projects in China, India, and ASEAN countries, supported by national infrastructure programs, are key contributors to volume growth.

- Renovation, Retrofit, and Decarbonization Upgrades

- Renovation and retrofit are increasingly important as decarbonization of the existing building stock emerges as a policy priority.

- The Global Buildings Status Report notes that achieving net-zero by 2050 requires major improvements in both operational energy and embodied carbon, with building-sector efficiency investments exceeding US$285 billion in 2022, although still below required levels. Flooring upgrades, such as low-VOC, high-insulation underlays, and circular materials, form part of many renovation packages.

Commercial flooring applications represent the fastest-growing end-use segment, driven by expansion in office spaces, retail establishments, hospitality venues, and institutional facilities. The sector's growth correlates with infrastructure development, organized retail sector expansion, and increasing service industry investments.

Commercial buyers prioritize durability, maintenance efficiency, and safety compliance, creating strong demand for resilient flooring solutions such as LVT, rubber, and linoleum. Healthcare and education sectors exhibit particularly robust adoption rates, specifying flooring materials that meet stringent hygiene standards while providing slip resistance and acoustic performance.

The segment's growth outpaces residential markets in emerging economies, where commercial construction accelerates to support urbanization and economic development.

Regional Insights

North America Flooring Market Trends & Analysis

The North American flooring market is mature but value-accretive. The U.S. is the largest market in the region, accounting for over 90% of the region.

The U.S. flooring market is likely to exceed US$40 billion by 2033, growing at a 3.7% CAGR through 2033, underpinned by steady residential construction and renovation demand. The residential sector dominates U.S. demand and is likely to hold 60% market share in 2033, driven by high renovation rates and new housing construction.

Carpets and rugs account for approximately 40% of the market in 2026, maintaining traditional consumer preferences, while resilient flooring categories, particularly LVT, demonstrate faster growth trajectories. The region's advanced distribution infrastructure, strong e-commerce penetration, and established manufacturer presence support market stability, though growth rates are modest compared to emerging markets.

Regulatory Environment and Innovation Ecosystem

Stringent environmental regulations, including VOC emission standards and sustainable sourcing requirements, shape product development and manufacturing practices. The U.S. Green Building Council's LEED certification program drives demand for eco-friendly flooring, with the green building sector contributing substantially to GDP.

From a regulatory standpoint, the U.S. is increasingly aligning with low-VOC and indoor air-quality standards (e.g., Green Label Plus, GREENGUARD), encouraging adoption of low-emission carpets, hardwoods, and laminates. The region also benefits from a robust innovation ecosystem led by global players such as Mohawk Industries, Shaw Industries, Mannington Mills, AHF Products, and Interface, which invest heavily in design, digital printing, performance coatings, and recycling infrastructure.

Investment trends include PVC-ree resilient lines, carbon-negative carpet tiles, and expanded take-back programs, positioning North America as a test bed for advanced sustainable flooring technologies.

Europe Flooring Market Trends Analysis

Europe is the second-largest flooring market globally, with strong positions in ceramic tiles, laminates, engineered wood, linoleum, and high-performance vinyl. The region is expected to surpass US$70 billion in 2026, with Germany alone accounting for over 20% of regional flooring demand, followed by France and the U.K. Non-resilient flooring dominates with over 55% share, led by ceramic tiles and supported by laminate and wood.

European growth is modest in volume but supported by mix improvement and sustainability-driven renovation. The EU’s updated Construction Products Regulation and harmonized EN standards require more rigorous testing of flooring for fire performance, VOC emissions, and environmental declarations.

In parallel, Europe’s building-sector climate agenda recognizes buildings as responsible for around one-third of energy demand and CO2 emissions, prompting policies such as renovation wave initiatives and national energy-efficiency programs. These frameworks strongly favour low-carbon, low-VOC, and circular materials such as linoleum, cork, recyclable vinyl, and carpets with high recycled content.

Turkey and Russia are significant flooring consumers by volume, particularly in ceramic tiles, leveraging local raw materials and cost-competitive production. Overall, Europe’s competitive landscape is characterized by strong regional champions, sophisticated distribution networks, and high specification rates in architect-driven projects.

Major European flooring producers, including Tarkett (France), Forbo (Switzerland), Gerflor (France), and Beaulieu International Group (Belgium), have invested in recycling centers, take-back schemes (e.g., Tarkett’s ReStart®), and high levels of recycled content to align with EU circular-economy objectives.

Asia Pacific Flooring Market Trends

Asia Pacific is the leading region, accounting for about 50% of the global flooring market share in 2026. Regional flooring materials revenues are projected to increase from and create an incremental opportunity of US$100 billion between 2026 and 2033, making Asia Pacific both the largest and one of the fastest-growing markets.

China alone is expected to generate roughly US$116 billion in flooring value by 2026, with ceramic tiles as the primary product, reflecting its status as the world’s largest ceramic tile producer and consumer.

India is among the fast-growing flooring markets, with the sector projected to grow at over 7.5% annually between 2026 and 2033 and market size exceeding US$20 billion by 2033, again led by ceramic tiles.

ASEAN markets (Vietnam, Indonesia, Thailand, Philippines) add further momentum through housing, industrial parks, and infrastructure build-out. The region is highly price-sensitive, favoring ceramic tiles, basic vinyl and laminates, but also increasingly adopting resilient LVT and linoleum in urban middle-class housing and commercial projects.

Japan and parts of Australia are more mature markets, with stable replacement demand and higher specification of premium wood, high-design vinyl, and tatami-compatible solutions. Asia Pacific’s manufacturing base spans ceramics (China, India, Vietnam), vinyl and laminates (China, Korea, Taiwan), and integrated building materials firms (e.g., LX Hausys in Korea, SCG Ceramics in Thailand), strengthening the region’s export capabilities.

Investment opportunities center on upgrading to value-added products, raising environmental standards, and expanding distribution in Tier 2/3 cities, as urbanization continues and policy support for affordable housing and infrastructure remains strong.

Competitive Landscape

Manufacturers Focusing On Innovation, Sustainability, and The Circular Economy

The global flooring market is moderately fragmented, with a mix of global groups and numerous regional ceramic, wood, and vinyl specialists.

Mohawk Industries is widely recognized as the world’s largest flooring manufacturer by revenue, with vertically integrated operations across carpet, rugs, ceramic tile, laminate, wood, and LVT. Other large players, Shaw Industries, Tarkett, Forbo, Gerflor, Interface, Beaulieu International Group, Mannington Mills, RAK Ceramics, Kajaria Ceramics, AHF Products, and LX Hausys, hold strong positions in specific product and regional niches.

Market leaders focus on innovation, sustainability, and segmentation rather than pure price competition. Key themes include low-carbon and PVC-free product development, circularity (recycling and take-back), digital design capabilities, and modular systems.

Differentiation increasingly comes from environmental credentials, lifecycle cost propositions, and channel strength (specialist dealers, project sales, e-commerce), while emerging business models, such as flooring-as-a-service and leasing in commercial settings, gain traction in select segments.

Recent Developments

- In 2025, Tarkett S.A. established a groundbreaking industry standard by launching the world’s first carbon-negative linoleum flooring range, encompassing all stages of the life cycle. Tarkett Lino not only meets expectations but surpasses them, achieving carbon negativity throughout every phase, from the responsible sourcing of renewable raw materials to the end-of-life processes of deconstruction, recycling, and reuse.

- In 2025, Mohawk Group announced a significant advancement in sustainable flooring: EcoFlex Matrix ULC, a revolutionary modular carpet backing, establishing an industry-leading standard for low-carbon solutions, boasting an exceptionally low carbon footprint of just 3.92 kilograms of CO2 emitted per square meter.

- In 2025, RAK Ceramics introduced Re-Use, the groundbreaking porcelain tile collection crafted entirely from 100% pre-consumer recycled materials. This innovative product sets a new standard in the tile industry, delivering exceptional performance, timeless elegance, and a strong commitment to environmental integrity all in one leading-edge offering.

- In 2024, Shaw Industries announced plans to enhance its U.S. resilient flooring manufacturing capabilities at its Plant RP in Georgia. The company is investing a substantial US$90 million to more than double the facility’s production capacity for SPC and LVT resilient flooring by 2026. This strategic expansion positions Shaw at the forefront of the flooring industry.

Companies Covered in Flooring Market

- Mohawk Industries

- Shaw Industries Group, Inc.

- Tarkett S.A.

- Beaulieu International Group N.V.

- Forbo Holding AG

- Interface Inc.

- Gerflor SAS

- Grupo Lamosa

- RAK Ceramics P.J.S.C

- Mannington Mills Inc.

- Balta Industries N.V.

- Armstrong Flooring

- Pamesa Ceramica

Frequently Asked Questions

The global flooring market was valued at US$374.5 billion in 2026 and is projected to reach US$555.7 billion by 2033, at a 5.8% CAGR. Growth is driven by urbanization, construction spending, and rising renovation activity worldwide.

Resilient flooring, especially luxury vinyl tiles (LVT) and stone plastic composites (SPC), is the fastest-growing segment. The resilient flooring market is expected to grow from about US$36.2 billion in 2024 to US$64 billion by 2034, reflecting strong demand in residential and commercial projects.

Asia Pacific is the largest flooring market, accounting for roughly 50% of global share in 2026. Regional revenue is forecast to rise from about US$135.2 billion in 2024 to US$215.5 billion by 2032, led by China and fast-growing India.

The residential sector is the leading end-user, contributing over 55% of global flooring demand in 2026. New housing construction, affordable housing schemes and home renovations sustain this dominance, especially in Asia Pacific and North America.

Stricter building regulations and ESG targets are boosting demand for low-VOC, low-carbon, and recyclable flooring, including linoleum, cork and PVC-free resilient products. Green building certifications (e.g., LEED, BREEAM, Cradle to Cradle) are now key differentiators for flooring manufacturers.