- Specialty & Fine Chemicals

- Floor Paints Market

Floor Paints Market Size, Share, and Growth Forecast, 2025 - 2032

Floor Paints Market By Product Type (Epoxy, Polyurethane, Others), End-user (Industrial, Commercial, Residential), Substrate, and Regional Analysis for 2025 - 2032

Floor Paints Market Size and Trends Analysis

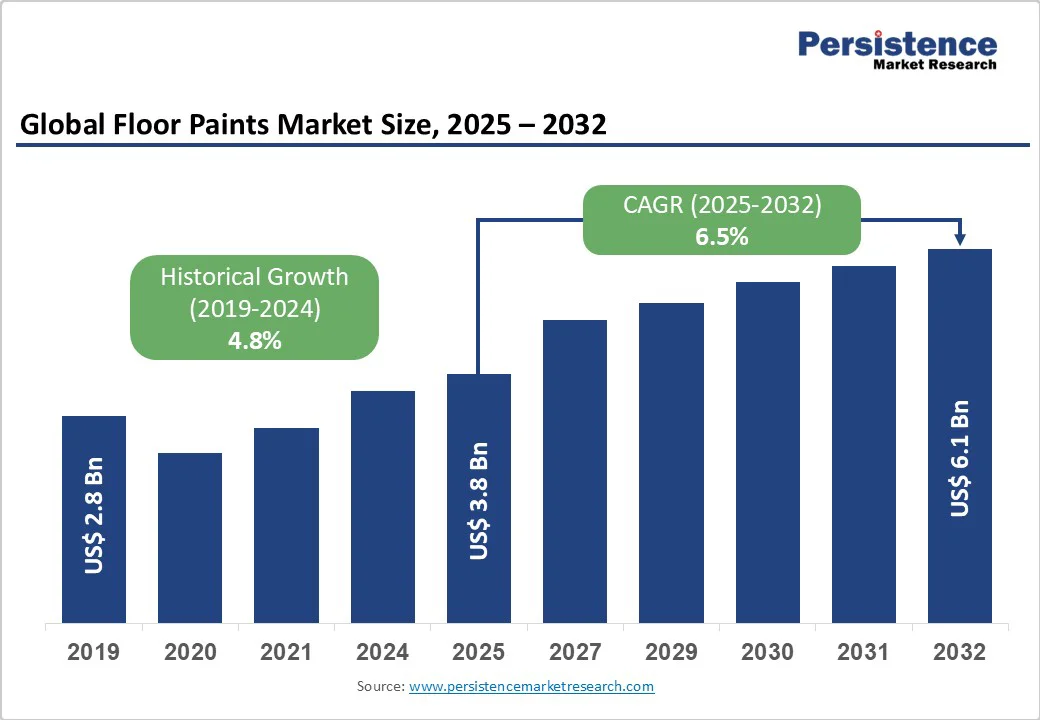

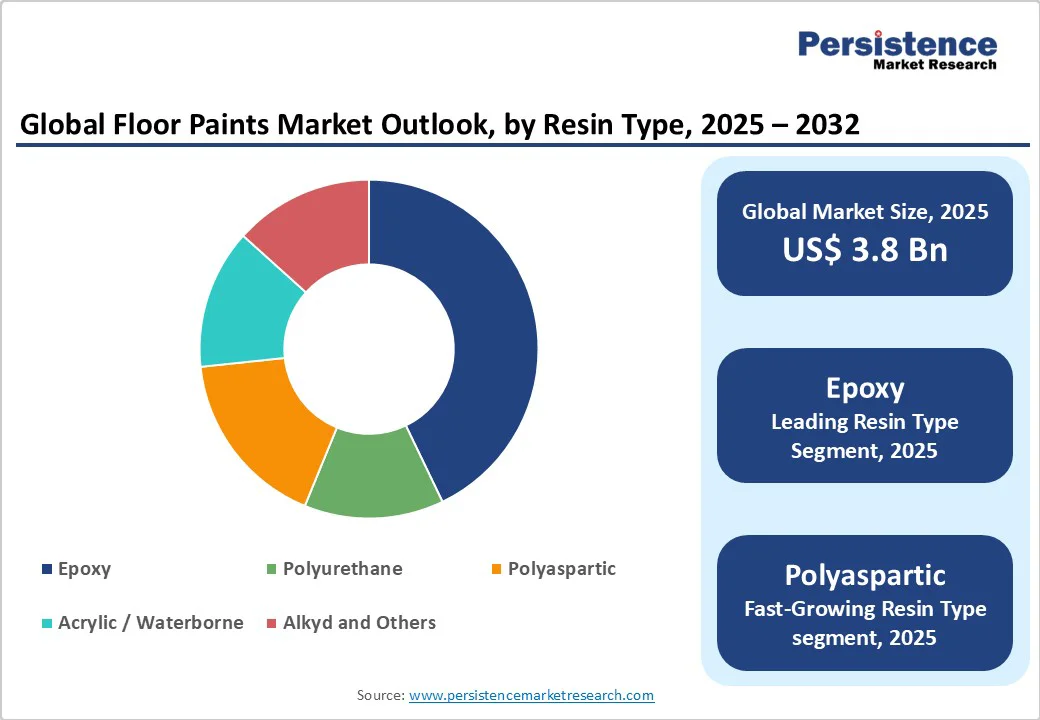

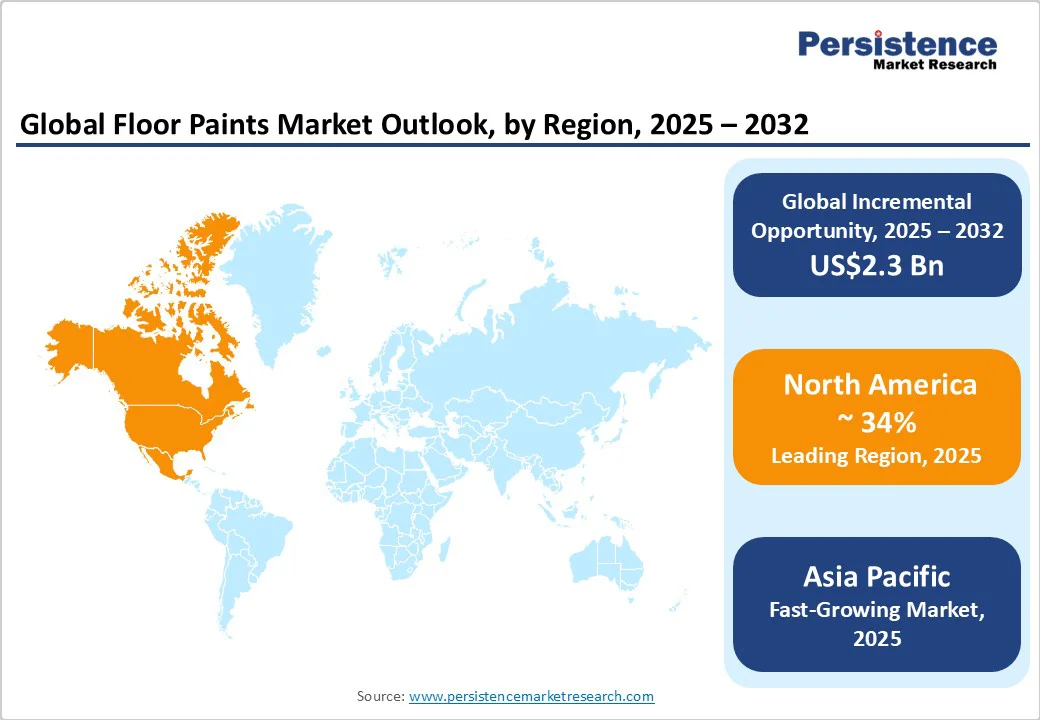

The global floor paints market size is likely to be valued at US$3.8?Billion in 2025, and is expected to reach US$6.1 Billion by 2032, growing at a CAGR of 6.5% during the forecast period 2025 to 2032, driven by global construction expansion, industrial infrastructure investments, and the increasing demand for high-performance protective coatings. Floor paints, particularly epoxy and polyurethane, are increasingly used in industrial, commercial, and residential spaces for their durability, chemical resistance, and visual appeal. Growing sustainability concerns and stricter environmental regulations are boosting demand for low-VOC and waterborne formulations.

Key Industry Highlights

- Leading Region: North America holds the largest market share, accounting for approximately 34% of global revenues in 2025, driven by industrial upgrades, logistics expansion, and advanced formulation adoption.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, fueled by rapid urbanization, industrialization, and infrastructure development in China, India, and ASEAN countries.

- Investment Plans: Major players are expanding regional manufacturing and R&D capacities. For instance, Asian Paints and Nippon Paint have established new blending and production facilities in India, Vietnam, and China to meet rising demand and reduce logistics costs.

- Dominant Resin Type: Epoxy coatings dominate the market, holding an estimated 45.3% of total revenue, due to their superior chemical resistance, adhesion, and suitability for industrial and heavy-duty applications.

- Leading Application: Industrial applications lead the market, accounting for around 50.1% of the global revenue, supported by manufacturing plants, automotive facilities, pharmaceutical sites, and cold storage warehouses that require high-performance, durable flooring systems.

| Key Insights | Details |

|---|---|

|

Floor Paints Market Size (2025E) |

US$3.8 Bn |

|

Market Value Forecast (2032F) |

US$6.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Global Construction and Industrial Investment Growth

The steady expansion of construction and industrial activities worldwide forms the core demand engine for floor paints. Ongoing urbanization, infrastructure upgrades, and industrialization are creating a vast pipeline of commercial and manufacturing facilities that require durable floor protection systems. Global construction output is projected to rise considerably through 2030, supported by industrial and logistics investments in North America, Europe, and Asia Pacific. Rising facility standards for epoxy and polyurethane coatings drive steady floor paint demand, boosting annual volumes and industrial-grade value share.

Shift Toward Performance-Based Resin Systems

Technological advancement in floor paint chemistries, particularly epoxy, polyurethane, and polyaspartic systems, is transforming the industry. These resins offer superior abrasion resistance, faster curing times, and high UV stability. Epoxy remains the most widely used product category due to its affordability and performance balance, while polyaspartic coatings are gaining attention for their rapid cure properties and decorative potential. Industries such as automotive, food processing, and healthcare increasingly require advanced coatings that ensure hygiene, safety, and reduced downtime. This shift toward performance-based systems not only enhances the product mix but also elevates the market’s overall revenue potential as customers opt for premium formulations.

Barrier Analysis - Raw Material Price Volatility

The floor paints market faces cyclical cost pressure due to its dependence on petrochemical feedstocks such as epoxy resins, isocyanates, and solvents. Volatility in crude oil prices and disruptions in global supply chains significantly affect manufacturing margins and pricing stability. These fluctuations can discourage procurement or lead to substitution with lower-cost systems. The volatility risk particularly affects smaller manufacturers, who often lack strong backward integration or long-term supply contracts, limiting their ability to absorb cost spikes.

Stringent Environmental Regulations

Environmental restrictions on volatile organic compounds (VOCs) and hazardous chemicals are tightening across major regions. Regulations in the U.S., European Union, and Japan have accelerated the shift toward waterborne and low-VOC formulations. However, reformulation efforts often demand substantial R&D spending and technical validation, raising production costs and prolonging product development cycles. Smaller regional manufacturers struggle to meet these compliance demands, limiting their competitiveness and slowing market entry of new solvent-free solutions.

Opportunity Analysis - Rising Refurbishment and Retrofit Projects

Renovation and maintenance cycles in commercial and residential buildings present a consistent revenue opportunity. Older facilities, especially in North America and Europe, are undergoing flooring replacements to meet modern aesthetic and hygiene standards. Refurbishment accounts for a growing share of floor coating demand, estimated at nearly one-third of annual consumption in developed economies. Manufacturers that offer quick-dry, low-odor, and long-life coating systems stand to gain, as project owners prioritize minimal downtime and reduced maintenance costs.

Expansion of Industrial and Logistics Facilities

Rapid global expansion in logistics, cold storage, and EV manufacturing has created large-scale demand for durable, high-load floor coatings. These applications require specialized formulations that resist abrasion, chemicals, and thermal shocks. The growing number of automated warehouses and clean-manufacturing environments favors advanced epoxy and polyurethane systems. The industrial floor segment’s potential value addition is estimated to increase by several hundred million dollars annually by the end of this decade, driven by warehouse automation and EV battery manufacturing projects.

Category-wise Analysis

Resin Type Insights

Epoxy systems dominate the market, accounting for 45.3% of the share of total revenue due to their exceptional chemical and mechanical resilience. These coatings are extensively used in industrial and commercial settings, including automotive manufacturing plants, pharmaceutical facilities, food and beverage production lines, and high-traffic warehouses. Epoxy’s ability to adhere strongly to concrete substrates makes it ideal for heavy-duty applications where resistance to abrasion, chemical spills, and impact is critical. Additionally, epoxy coatings are widely used in decorative applications such as polished concrete floors in offices, showrooms, and hospitals. The combination of durability, cost efficiency, and proven long-term performance, supported by established supply networks and technical expertise, ensures epoxy maintains its leading market position.

Polyaspartic systems are expanding faster than the overall market CAGR, driven by growing demand for premium, high-performance floor solutions. Polyaspartic coatings, with their rapid curing times, are preferred in commercial spaces and logistics centers where minimizing downtime is essential. For example, warehouses undergoing frequent turnover or maintenance cannot afford long curing periods; polyaspartic solutions allow same-day installation. Their aesthetic versatility, offering glossy, matte, or metallic finishes, further expands their adoption in decorative commercial floors and public infrastructure, supporting accelerated growth.

Application Insights

Industrial facilities constitute the largest end-use category for floor paints, representing 50.1% of global market revenue. Key sectors include automotive manufacturing plants, food processing units, pharmaceutical laboratories, chemical production sites, and cold storage facilities. These environments demand floor coatings with high chemical resistance, durability, slip-resistance, and hygiene compliance. For example, pharmaceutical plants require epoxy or polyurethane floors that can withstand frequent cleaning with harsh disinfectants, while automotive factories use epoxy coatings resistant to oil, solvents, and heavy machinery impact. Large-scale industrial floors also necessitate multi-layer systems, including primers, base coats, and topcoats, which increases the overall market value per project. The consistent need for maintenance, refurbishment, and compliance with industrial safety standards ensures ongoing demand and revenue dominance in this segment.

Commercial applications, including retail stores, shopping malls, warehouses, airports, data centers, and office buildings, represent the fastest-growing floor paints segment. The rise of e-commerce and the rapid expansion of logistics and fulfillment centers have driven significant demand for durable, visually appealing, and fast-curing floor coatings. For instance, large-scale warehouses for companies such as Amazon and FedEx require polyaspartic coatings to allow same-day curing and immediate operations. Decorative epoxy floors are increasingly used in retail spaces, hotels, and restaurants to combine aesthetics with high wear resistance. Airports and public transit facilities often deploy polyurethane or hybrid systems to endure heavy foot traffic and maintain hygienic standards. The commercial segment’s combination of high specification requirements, rapid turnover, and emphasis on aesthetics ensures its accelerated growth rate compared to the industrial and residential segments.

Regional Insights

North America Floor Paints Market Trends - Logistics Growth, Fast-Curing Systems, and Technical Innovation

North America accounts for a significant market share, driven by a mature construction industry, stringent safety regulations, and high renovation activity. The United States is the largest contributor, supported by ongoing industrial upgrades, expanding logistics hubs, and residential remodeling projects. For example, recent expansions of e-commerce distribution centers by companies such as Amazon and Walmart have spurred demand for rapid-curing epoxy and polyaspartic floor systems that minimize operational downtime.

The market benefits from advanced formulation technology, including antimicrobial epoxy floors for healthcare facilities and low-odor, fast-dry coatings for commercial spaces. Public sector modernization, such as renovations at major airports, hospitals, and government buildings, continues to support floor coating adoption. Key players, including Sherwin-Williams, PPG Industries, and RPM International, leverage integrated distribution networks, certified applicator partnerships, and localized technical support to maintain market dominance.

In 2024, Sherwin-Williams launched a new polyaspartic floor system in North America designed for high-traffic logistics and industrial facilities, reducing curing times by up to 50%. PPG Industries expanded its production capacity for low-VOC industrial floor coatings in the U.S., addressing increasing demand from environmentally conscious commercial projects. Such initiatives reinforce North America’s continued value growth and innovation leadership.

Europe Floor Paints Market Trends - Regulatory Compliance, Refurbishment Demand, and Eco-Friendly Coatings

Europe is characterized by strict regulatory standards, mature building codes, and a strong sustainability focus. Germany, the United Kingdom, France, and Spain represent the largest markets in the region. Germany leads in industrial and manufacturing floor coatings, serving sectors such as automotive production and chemical plants, while the U.K. shows significant growth in commercial refurbishment, including office complexes and retail centers.

The European Green Deal and VOC reduction policies have accelerated the adoption of waterborne and solvent-free coatings, creating opportunities for innovation in environmentally friendly formulations. Manufacturers such as AkzoNobel, BASF, and Hempel focus on enhancing durability, aesthetics, and lifecycle cost-efficiency. The mature nature of the market means that growth is largely driven by refurbishment, replacement cycles, and niche high-performance applications rather than new construction.

In 2023, BASF introduced a new epoxy-polyurethane hybrid coating tailored for food and beverage facilities in Europe, meeting stricter hygiene and chemical resistance standards. AkzoNobel partnered with specialized applicators in Germany and France to provide turnkey solutions for industrial and commercial flooring, ensuring compliance with VOC limits while reducing project timelines. These moves demonstrate the market’s focus on sustainability, regulatory compliance, and technical innovation.

Asia Pacific Floor Paints Market Trends - Industrial Boom, Fast Application, and Regional Manufacturing Expansion

Asia Pacific is the fastest-growing region, driven by rapid urbanization, industrialization, and infrastructure expansion. China, India, Japan, and ASEAN countries are key contributors, with the construction of logistics parks, smart manufacturing facilities, and residential developments fueling demand for durable, high-performance coatings. For instance, China’s expansion of cold storage facilities for e-commerce and India’s growing pharmaceutical manufacturing sector have increased demand for epoxy and polyurethane systems capable of handling heavy loads and chemical exposure.

The region benefits from cost competitiveness, improving technical standards, and rising awareness of workplace safety and hygiene. Local manufacturers such as Asian Paints and Berger Paints are expanding production facilities, while international players such as Nippon Paint and Jotun are investing in regional blending plants and training centers to capture long-term growth.

In 2024, Asian Paints launched a range of fast-curing polyaspartic coatings for warehouses in India, enabling same-day application and reducing operational downtime. Nippon Paint established a new production facility in Vietnam to cater to ASEAN industrial and commercial floor coating demand. Jotun expanded its decorative floor coating portfolio in China to serve premium retail and hospitality segments. These initiatives highlight the region’s rapid adoption of technologically advanced coatings and the growing importance of regional manufacturing and logistics capabilities.

Competitive Landscape

The global floor paints market is moderately consolidated, with a few multinational corporations accounting for a major share of total revenue. Companies such as Sherwin-Williams, PPG Industries, AkzoNobel, BASF, and Nippon Paint dominate the high-performance coatings segment. Regional producers compete through customized formulations, local distribution networks, and applicator partnerships. The market’s top players benefit from integrated value chains, strong brand recognition, and technical support services.

The presence of numerous local formulators ensures healthy price competition and innovation across niche applications. Leading players focus on product innovation, geographic expansion, and sustainability-driven differentiation. Partnerships with applicators, training programs, and turnkey installation services have become critical for securing large institutional contracts.

Key Industry Developments

- In March 2025, Sherwin-Williams launched its Pro Industrial Fast-Cure Epoxy Flooring system in the U.S., designed for high-traffic industrial facilities and warehouses, reducing curing time by 50% and minimizing operational downtime.

- In April 2025, PPG Industries introduced the Durapoxy Low-VOC Industrial Floor Coating in North America, targeting environmentally regulated commercial and manufacturing applications with enhanced chemical resistance and rapid curing properties.

- In May 2025, AkzoNobel released the Intercrete 4801 Polyurethane Floor System in Germany, optimized for chemical plants and food processing facilities, combining durability, slip resistance, and VOC compliance.

Companies Covered in Floor Paints Market

- Sherwin-Williams

- PPG Industries

- AkzoNobel

- BASF

- Nippon Paint

- Asian Paints

- Kansai Paint

- RPM International

- Axalta Coating Systems

- Hempel

- Jotun

- Berger Paints

- Beckers Group

- Valspar

- Tikkurila

- Benjamin Moore

- Kelly-Moore Paints

- Mapei

- Sika AG

- Masco Corporation

Frequently Asked Questions

The floor paints market size in 2025 is US$3.8 Billion.

The floor paints market is projected to reach US$6.1 Billion by 2032.

Key trends include the increasing adoption of low-VOC and waterborne coatings, rapid growth in industrial and commercial applications, rising demand for epoxy, polyurethane, and polyaspartic systems, and expansion in refurbishment and retrofit projects. Sustainability and regulatory compliance are driving product innovation.

Epoxy coatings lead the market, accounting for the largest revenue share due to their chemical resistance, durability, and widespread use in industrial and commercial applications.

The market is projected to grow at a CAGR of 6.5% between 2025 and 2032.

Major players with strong portfolios include Sherwin-Williams, PPG Industries, AkzoNobel, BASF, and Asian Paints.