- Home Care & Utilities

- Commercial Flooring Market

Commercial Flooring Market Size, Share, and Growth Forecast, 2025 - 2032

Commercial Flooring Market By Product Type (Soft Coverings, Resilient Flooring, Others), Application (Commercial Buildings, Healthcare, Others), and Regional Analysis for 2025 – 2032

Commercial Flooring Market Size and Trends Analysis

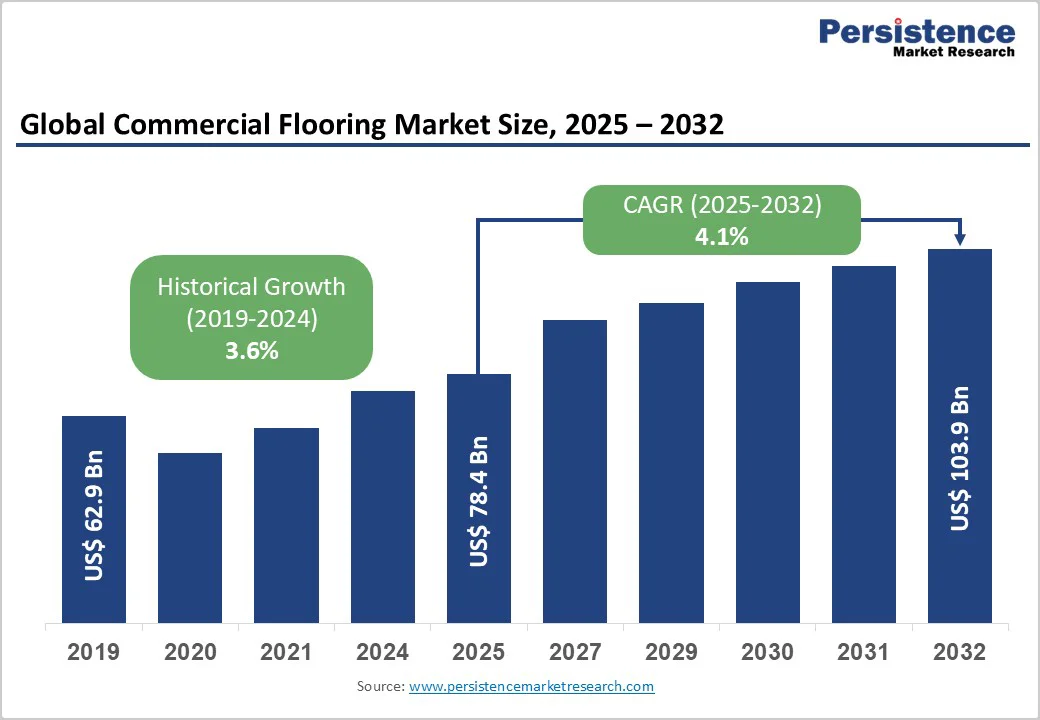

The global commercial flooring market size is likely to be valued at US$78.4 Billion in 2025, estimated to reach US$103.9 Billion by 2032, growing at a CAGR of 4.1% during the forecast period from 2025 to 2032, driven by increasing commercial construction, rising demand for durable and sustainable flooring solutions, and growing investments in office, retail, and healthcare infrastructure. The market is further propelled by innovations in resilient and eco-friendly flooring materials, catering to preferences for green building certifications and aesthetic appeal. The growing acceptance of industrial flooring as a critical element in enhancing workplace productivity and brand image is a key growth factor.

Key Industry Highlights:

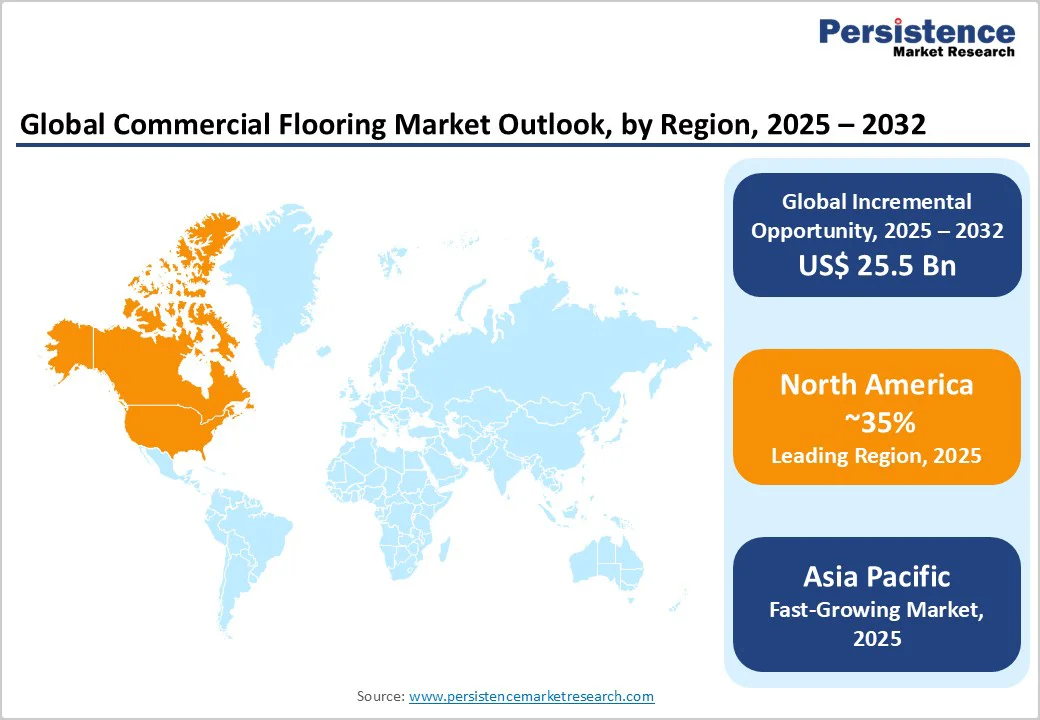

- Leading Region: North America, commanding a 35% market share in 2025, driven by advanced commercial real estate and renovation projects in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapid urbanization and retail expansion in China and India.

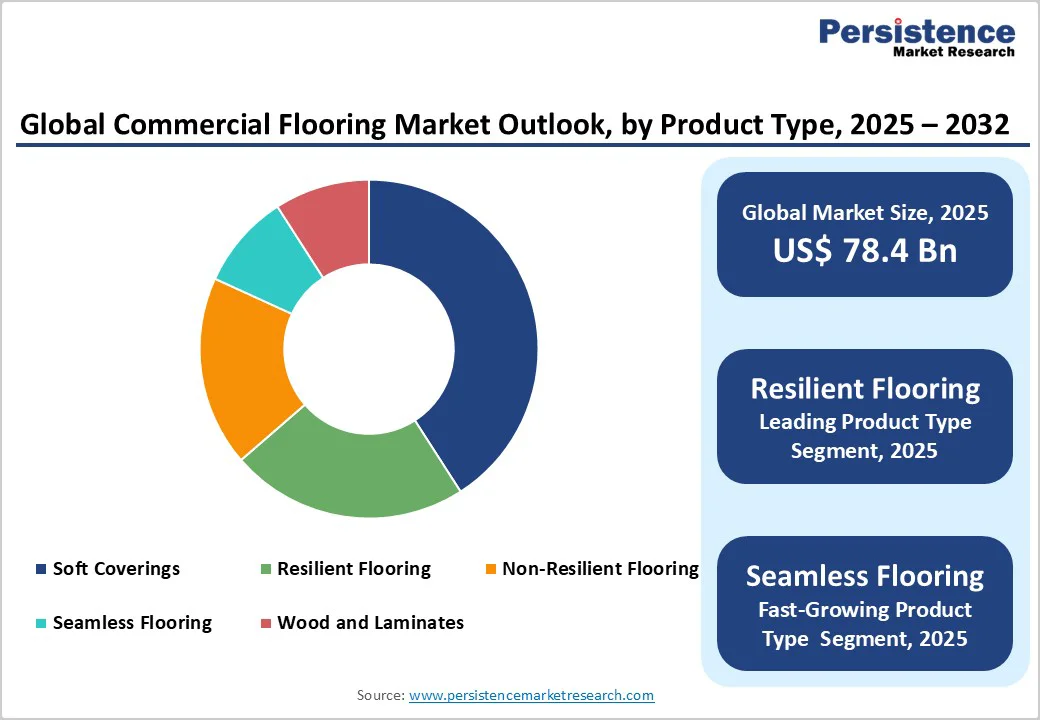

- Dominant Product Type: Resilient Flooring, holding approximately 40% of the market share, due to its durability and cost-effectiveness.

- Leading Application: Commercial Buildings, accounting for over 30% of market revenue, driven by office space developments.

- Key Market Driver: Innovations such as modular flooring systems, digital printing, and advanced surface coatings are enhancing product durability, design flexibility, and installation efficiency.

- Growth Opportunity: Expansion in sustainable and modular flooring for green building projects.

| Key Insights | Details |

|---|---|

| Commercial Flooring Market Size (2025E) | US$78.4 Bn |

| Market Value Forecast (2032F) | US$103.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Commercial Construction and Demand for Sustainable Flooring

The increasing volume of commercial construction and demand for sustainable, high-performance flooring are primary drivers of the commercial flooring market. Expanding infrastructure investments in offices, retail outlets, healthcare facilities, and educational institutions are fueling the need for durable, cost-effective, and aesthetically appealing flooring materials. Developers and architects increasingly prefer high-performance options such as vinyl, linoleum, laminate, and polished concrete that combine functionality with long-term value. Simultaneously, the global shift toward sustainability is transforming material preferences.

End users and regulators are prioritizing eco-friendly, low-emission, and recyclable flooring products that align with green building certifications such as LEED, BREEAM, and WELL. This has led manufacturers to innovate with bio-based polymers, recycled content, and low-VOC adhesives to minimize environmental impact. Furthermore, corporate sustainability goals and rising consumer awareness are pushing demand for carbon-neutral flooring solutions. The synergy between commercial construction growth and sustainability initiatives is fostering widespread adoption of advanced modular and eco-friendly flooring systems, positioning the market for steady expansion across both developed and emerging economies in the coming years.

High Installation Costs and Supply Chain Disruptions

High installation costs and supply chain volatility pose significant restraints on market growth. High installation costs and supply chain disruptions pose significant challenges to the growth of the global commercial flooring market. The installation of advanced flooring materials such as luxury vinyl tiles, epoxy coatings, and seamless systems often requires skilled labour, specialized equipment, and precise surface preparation factors that increase overall project costs. Labour shortages and rising wage rates in developed markets further add to these expenses, especially for large-scale commercial projects.

The global supply chain has faced considerable disruptions in recent years due to geopolitical tensions, trade restrictions, and logistics bottlenecks. Shortages of key raw materials such as PVC, adhesives, and resins have led to price volatility and delayed project timelines. Manufacturers are also burdened by increased transportation and energy costs, which affect production efficiency and product availability. These challenges are particularly critical in cost-sensitive markets, where budget constraints can limit the adoption of premium flooring solutions.

Growth in Modular and Eco-Friendly Flooring Solutions

Advancements in modular and sustainable commercial flooring present significant growth opportunities. Modular flooring options, such as carpet tiles, luxury vinyl tiles (LVT), and interlocking systems, are gaining popularity due to their ease of installation, replacement, and customization. These systems enable quick renovations with minimal disruption, making them ideal for offices, retail stores, and educational institutions.

Increasing environmental awareness and regulatory pressures are driving the shift toward eco-friendly materials such as recycled vinyl, linoleum, cork, and bio-based polymers. Manufacturers are focusing on developing products with low volatile organic compound (VOC) emissions, improved recyclability, and longer life cycles to meet global green building standards such as LEED and BREEAM. The combination of aesthetic appeal, functionality, and sustainability is attracting architects and designers seeking to balance performance with environmental responsibility.

Category-wise Analysis

Product Type Insights

Resilient Flooring dominates the market, accounting for 40% of the share in 2025, owing to its exceptional versatility, water resistance, and low maintenance requirements. Widely used in high-traffic areas such as offices, hospitals, and retail spaces, it offers durability, comfort underfoot, and design flexibility, making it a preferred choice for modern commercial and institutional applications.

Seamless Flooring is the fastest-growing segment, driven by increasing demand for hygienic, durable, and visually appealing solutions in healthcare and retail environments. Its smooth, joint-free surface prevents dirt accumulation, ensuring easy cleaning and maintenance. Growing preference for sleek aesthetics and customizable designs enhances its adoption across modern commercial and institutional spaces worldwide.

Application Insights

Commercial Buildings lead with 30% share, driven by ongoing corporate office expansions, workspace refurbishments, and sustainability-driven design upgrades. The demand for durable, noise-reducing, and visually appealing flooring materials is rising as companies focus on creating modern, comfortable, and productivity-enhancing environments in line with evolving workplace and design standards.

Retail is the fastest-growing, fueled by rapid store modernization and the growing emphasis on brand-focused interior aesthetics. Retailers are investing in durable, stylish, and easy-to-maintain flooring materials to enhance customer experience, reflect brand identity, and support high foot traffic, particularly across malls, boutiques, and large retail chains.

Regional Insights

North America Commercial Flooring Market Trends

North America accounts for 35% in 2025, driven by U.S. commercial real estate investments and demand for resilient flooring. The U.S. leads the regional market, supported by robust construction activities in office spaces, healthcare facilities, educational institutions, and hospitality projects. Increasing preference for vinyl, laminate, and hybrid flooring products offering durability, easy maintenance, and design versatility is fueling market growth. The rising focus on sustainability has encouraged the adoption of recyclable and low-VOC flooring solutions that comply with green building standards such as LEED.

The region also benefits from advanced installation technologies and a strong distribution network across retail and e-commerce channels. The U.K. market, though part of Europe, reflects similar trends, with a notable shift toward eco-friendly contract flooring during post-Brexit economic recovery. Increased refurbishments in offices, retail stores, and public infrastructure are boosting demand for modern, modular flooring systems that combine aesthetic appeal, durability, and compliance with sustainability goals.

Europe Commercial Flooring Market Trends

Europe holds about 30% market share, led by Germany and France where strong sustainability mandates and advanced construction standards drive product demand. The region’s growth is primarily influenced by the European Union’s strict environmental regulations, which promote the adoption of recyclable, low-emission, and energy-efficient flooring materials. Manufacturers are increasingly focusing on eco-friendly solutions such as bio-based vinyl, linoleum, and modular carpet tiles to align with the EU Green Deal and circular economy goals.

Germany dominates the regional market with extensive use of high-durability flooring in healthcare, education, and industrial facilities, emphasizing hygiene, safety, and acoustic comfort. France contributes significantly through robust commercial renovation activities and the integration of design-driven, sustainable materials in offices and retail spaces. The region’s well-established infrastructure, combined with high awareness of green certifications such as BREEAM and LEED, supports continued growth.

Asia Pacific Commercial Flooring Market Trends

Asia Pacific commands around 25% share and is the fastest-growing region, driven by rapid urbanization, infrastructure investments, and a thriving construction sector. China remains the dominant market, propelled by extensive commercial and industrial infrastructure projects, including offices, malls, healthcare centers, and transport hubs. The country’s focus on smart city development and sustainable construction materials further fuels demand for high-performance and eco-friendly flooring solutions.

In India, the rapid expansion of the retail and hospitality sectors, along with growing investments in commercial real estate, has created a robust market for durable, low-maintenance flooring options such as vinyl, laminate, and ceramic tiles. Rising disposable incomes and increasing awareness of aesthetics and functionality in interior spaces also contribute to regional growth. Moreover, foreign direct investments in construction and manufacturing are accelerating product availability and distribution networks.

Competitive Landscape

The global commercial flooring market is moderately consolidated, characterized by the presence of key players emphasizing sustainability, design flexibility, and strategic collaborations. Leading manufacturers are increasingly focusing on developing eco-friendly flooring solutions made from recycled materials, low-VOC adhesives, and bio-based polymers to meet stringent environmental standards and green building certifications such as LEED and BREEAM.

The demand for modular and customizable flooring systems, including carpet tiles, vinyl planks, and hybrid solutions, is rising due to their ease of installation, replacement, and aesthetic versatility. To strengthen market reach, companies are forming partnerships with architects, interior designers, and contractors to deliver integrated flooring solutions that meet the evolving needs of modern commercial spaces such as offices, healthcare facilities, and educational institutions. Digital tools such as 3D visualization and Building Information Modeling (BIM) are being adopted to improve project planning and customer experience.

Key Industry Developments

- In 2025, Forbo Flooring Systems, the commercial flooring division of Forbo Holding AG, has announced an expansion of its seamless flooring portfolio specifically tailored for healthcare environments in Europe. The enhanced offering addresses the rising demand for hygiene-focused, low-disruption flooring installations in hospitals, clinics, and other medical facilities.

- In 2020, Interface, Inc. a global leader in commercial flooring solutions, has unveiled its new Embodied Beauty™ collection, bringing to market the industry’s first cradle-to-gate carbon-negative carpet tile styles.

Companies Covered in Commercial Flooring Market

- Armstrong Flooring, Inc.

- Congoleum

- Flowcrete (RPM)

- Forbo International SA

- Gerflor

- Interface, Inc.

- IVC Group

- James Halstead Plc.

- Mannington Mills, Inc.

- NOX Corp.

- Tkflor

- Nora

Frequently Asked Questions

The global commercial flooring market is projected to reach US$78.4 Billion in 2025, driven by commercial construction growth.

The market is driven by growing emphasis on eco-friendly, recyclable, and low-VOC flooring supports green building certifications such as LEED and BREEAM.

The market is poised to witness a CAGR of 4.1% from 2025 to 2032, supported by eco-friendly innovations.

Expansion in green-certified industrial flooring offers opportunities for sustainable office and retail projects.

Armstrong Flooring, Interface, Inc., Forbo International, Gerflor, and Mannington Mills lead through innovative contract flooring solutions.