- Home Appliances

- Floor Lamp Market

Floor Lamp Market Size, Share, and Growth Forecast 2026 - 2033

Floor Lamp Market by Light Source (LED Floor Lamps, Halogen Floor Lamps, Fluorescent/CFL Floor Lamps, Others), Material (Metal, Wood, Plastic, Glass, Textile), Price Range (Mass, Premium, Luxury), Application (Commercial, Household, Industrial), Distribution Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Floor Lamp Market Size and Trend Analysis

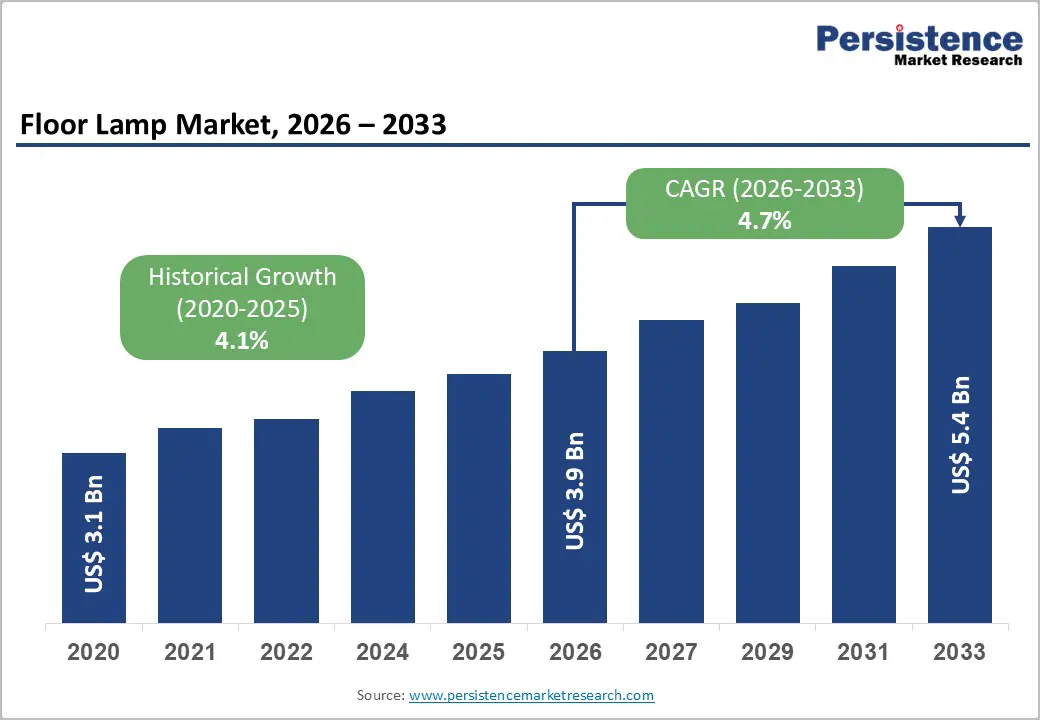

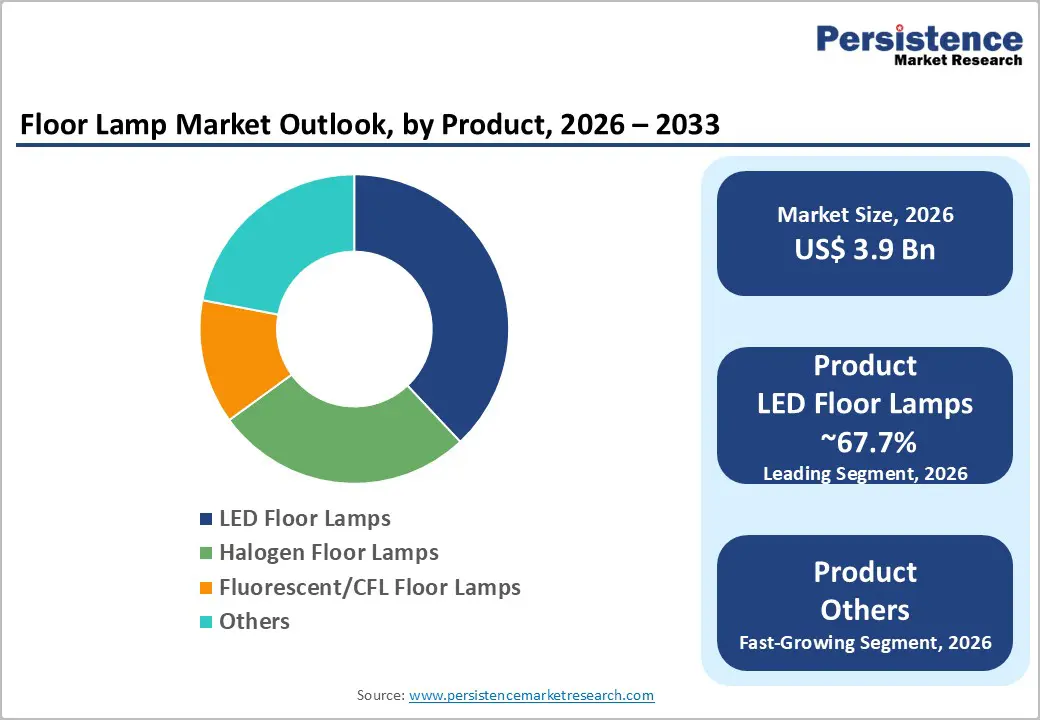

The global floor lamp market size is projected to be valued at approximately US$ 3.9 billion in 2026 and is expected to reach around US$ 5.4 billion by 2033, registering a CAGR of 4.7% during the forecast period from 2026 to 2033.

Market growth is supported by rising consumer preference for multifunctional lighting solutions that combine aesthetics with practicality, as well as the rapid adoption of energy-efficient LED technologies. Increasing investments in interior design, growing urbanization, and higher disposable incomes are further boosting demand. Additionally, the trend toward home personalization and advancements in smart lighting systems continue to strengthen adoption across residential, commercial, and industrial applications worldwide.

Key Industry Highlights:

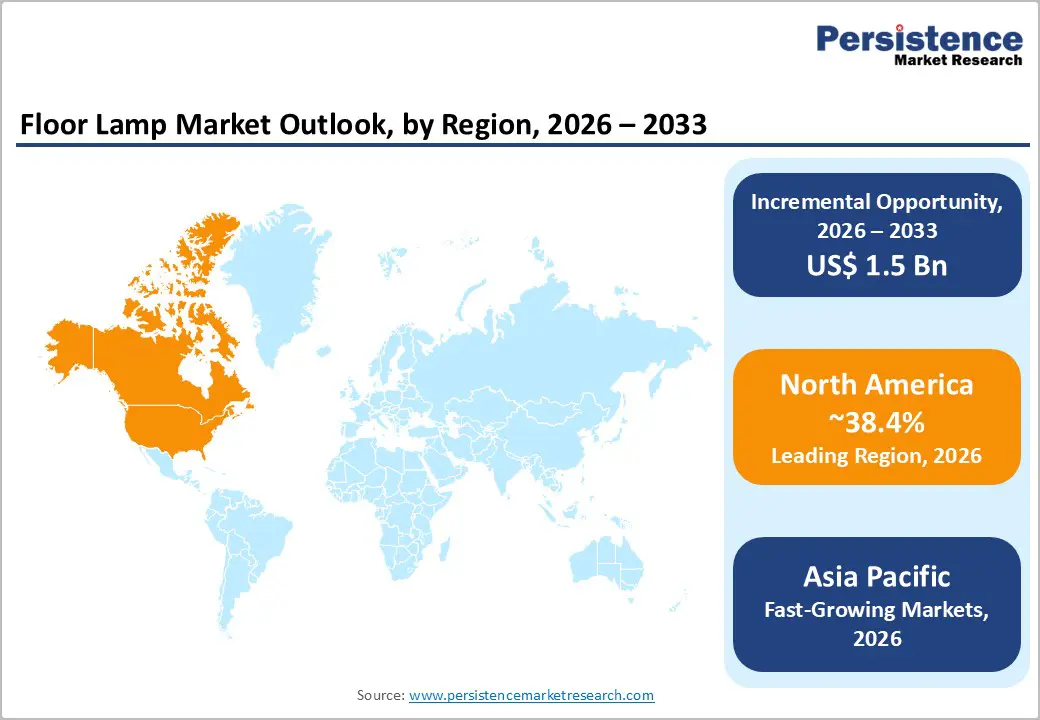

- Leading Region: North America leads with 38.4% share, driven by high disposable incomes, LED regulations, advanced retail, and strong premium floor lamp demand.

- Fastest-Growing Region: Asia Pacific accounts for 35.5% share, propelled by urbanization, rising middle-class spending, smart city initiatives, and design-focused home lighting demand.

- Dominant Segment: LED floor lamps hold 65.7% share, supported by regulatory phase-outs, energy efficiency, long lifespan, and smart home integration.

- Fastest-Growing Segment: Online distribution is expanding fastest due to e-commerce growth, convenience, wider selection, and direct-to-consumer strategies.

- Key Market Opportunity: Eco-friendly floor lamps are a high-growth segment, driven by sustainable consumer demand, circular economy policies, and a willingness to pay premiums.

| Key Insights | Details |

|---|---|

| Floor Lamp Market Size (2026E) | US$ 3.9 billion |

| Market Value Forecast (2033F) | US$ 5.4 billion |

| Projected Growth CAGR (2026 - 2033) | 4.7% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Accelerating Transition Toward Energy-Efficient LED Floor Lamp Technologies

The adoption of energy-efficient lighting solutions and the shift toward LED-based lighting is fueled by awareness of energy savings, cost efficiency, and sustainability. LEDs consume far less electricity than incandescent and fluorescent lamps while offering extended operational lifespans, reducing maintenance and replacement frequency. The residential, commercial, and hospitality sectors are embracing LED solutions owing to their reliability and long-term value.

Government regulations and incentive programs reinforce this transition by phasing out inefficient lighting technologies. When combined with advanced dimming controls and smart features, LED lighting optimizes energy usage and cost savings. This makes LEDs a future-ready choice, supporting both operational efficiency and environmental sustainability across multiple applications.

Rising Adoption of Smart Home Integration and IoT-Enabled Floor Lamps

The rapid expansion of smart home ecosystems is significantly influencing demand for IoT-enabled floor lamps, as consumers increasingly seek connected and intelligent lighting solutions. Features such as voice control, mobile app integration, programmable schedules, and customizable lighting settings align with modern preferences for convenience, personalization, and automation in everyday living environments.

Beyond residential use, this trend is extending into commercial and workspace settings where smart floor lamps support energy monitoring, occupancy-based lighting, and human-centric illumination. Businesses are adopting connected lighting systems to enhance operational efficiency, employee comfort, and productivity. As smart infrastructure adoption accelerates globally, technologically integrated floor lamps are becoming integral to intelligent lighting ecosystems.

Restraints - Price Sensitivity in Emerging Economies and Volatility in Raw Material Costs

Price sensitivity continues to restrain the adoption of floor lamps in emerging markets, where consumers prioritize affordability and basic functionality over premium design or smart features. Wide price gaps between entry-level and high-end floor lamps limit demand for technologically advanced products, particularly in residential segments. Rising inflationary pressures further constrain discretionary spending on non-essential home décor items, slowing growth in the premium segment.

Volatility in raw material prices, especially metals, electronic components, and semiconductors, creates cost uncertainty for manufacturers. Trade restrictions, tariffs on imported lighting components, and ongoing supply chain disruptions raise production expenses. These cost increases are often passed on to consumers, reducing competitiveness in price-sensitive regions and moderating overall market expansion.

Competitive Pressure from Low-Cost Alternatives and Market Fragmentation

The global floor lamp market is highly fragmented, with many regional and local manufacturers competing aggressively on price. Budget-friendly floor lamps produced by low-cost manufacturers often undercut established brands, placing sustained pressure on profit margins. As basic floor lamp designs face minimal technological barriers, new entrants frequently enter the market, intensifying price competition across mass-market segments.

This fragmented competitive landscape limits pricing power and reduces incentives to position as a premium. While consolidation opportunities exist due to the absence of dominant players, current fragmentation restricts investment in innovation, advanced materials, and smart lighting technologies, thereby constraining long-term value creation and market differentiation.

Opportunity - Explosive Growth in Home Décor Spending and Rising Interior Design Consciousness

Rising global spending on home décor and increasing interior design awareness are creating strong growth opportunities for floor lamp manufacturers. Consumers across income groups are actively investing in personalized living spaces, positioning floor lamps as both functional lighting solutions and decorative focal points. Contemporary interior trends emphasize layered lighting and coordinated aesthetics, driving demand for visually distinctive and design-forward floor lamp offerings across residential settings.

Digital tools such as interior design software, virtual staging platforms, and social media channels are further influencing purchasing behavior by showcasing innovative lighting applications. The ongoing work-from-home culture has transformed homes into multifunctional environments, increasing demand for versatile floor lamps that support task lighting, ambiance, and flexible space use.

Sustainability-Driven Innovation and Expansion of Eco-Conscious Consumer Segments

Growing environmental awareness is driving demand for sustainable floor lamps made from responsibly sourced and recycled materials. Eco-conscious consumers increasingly prefer products made with bamboo, FSC-certified wood, recycled plastics, and biodegradable components, enabling manufacturers to command premium prices. This shift is encouraging innovation in material sourcing and environmentally responsible manufacturing practices across the lighting industry.

Supportive government policies promoting circular economy principles and corporate sustainability commitments are accelerating investment in green product lines. Premium decorative floor lamps with strong sustainability narratives are gaining traction among affluent buyers. Combined with expanding e-commerce access to curated eco-friendly lighting options, this trend presents significant opportunities for differentiated and value-driven market entrants.

Category-wise Analysis

Light Source Insights

LED floor lamps dominate the light source category, accounting for approximately 65.7% of the overall market share. This leadership is supported by superior energy efficiency, extended lifespan, and seamless compatibility with smart home ecosystems. Declining LED component costs and regulatory phase-outs of incandescent and fluorescent lighting further accelerate adoption. Manufacturers increasingly compete through features such as adjustable color temperatures, brightness control, and integrated smart functionalities rather than core lighting performance.

Smart and tunable LED floor lamps represent the fastest-growing category as consumers seek customizable lighting experiences. Demand is rising for lamps that integrate with voice assistants, mobile applications, and automated home systems. This growth is driven by urban lifestyles, home personalization trends, and increasing preference for adaptive lighting solutions across residential and commercial environments.

Material Insights

Metal remains the leading material segment, holding approximately 45.5% market share due to its durability, structural strength, and compatibility with modern interior aesthetics. Metal floor lamps come in a range of finishes, including matte black, brushed steel, and antique bronze, making them suitable for residential and commercial use. Recyclability further enhances appeal amid rising consumer and manufacturer sustainability awareness.

Plastic-based floor lamps are emerging as the fastest-growing material category. Lightweight construction, design flexibility, and cost advantages drive adoption, particularly in urban households and rental spaces. Innovations using recycled plastics and sustainable polymers are expanding plastic’s appeal, enabling manufacturers to balance affordability with eco-conscious positioning in competitive markets.

Price Range Insights

Mass market floor lamps dominate pricing segmentation with approximately 55.6% market share, driven by strong demand for affordable and functional lighting solutions. Typically priced below US$50, these products emphasize accessibility, basic illumination, and wide availability across offline and online retail channels. This segment benefits from high-volume sales and broad adoption among cost-conscious residential consumers.

Luxury floor lamps represent the fastest-growing price category as affluent consumers increasingly invest in premium home décor. Demand is driven by exclusive designs, artisanal craftsmanship, bespoke customization, and designer collaborations. Growth is particularly strong in developed markets and emerging urban centers where consumers prioritize aesthetic distinction and brand value over price sensitivity.

Application Insights

Household applications lead the floor lamp market, accounting for approximately 60.6% of the market. Residential demand is driven by interior decoration trends, personal expression, and the need for layered lighting solutions. Living rooms, bedrooms, and study areas consistently demand floor lamps that balance visual appeal with ambient and task lighting.

Commercial applications represent the fastest-growing usage segment as businesses increasingly adopt decorative yet functional lighting. Offices, retail stores, hospitality venues, and restaurants utilize floor lamps to enhance ambiance, brand identity, and customer experience. Growing emphasis on workplace aesthetics, employee comfort, and flexible interior layouts continues to support rising adoption.

Distribution Channel Analysis

Offline channels dominate distribution with approximately 56.4% market share, supported by furniture stores, lighting specialty retailers, and home improvement outlets. Physical retail enables consumers to evaluate design quality, materials, and lighting performance firsthand. Professional guidance and experiential purchasing remain critical for higher-value and design-centric floor lamp purchases.

Online distribution is the fastest-growing channel, driven by convenience, wider product availability, and competitive pricing. E-commerce platforms and direct-to-consumer models provide access to customized, premium, and niche designs that are not available locally. Digital-native consumers increasingly prefer online channels for comparison, personalization options, and doorstep delivery.

Regional Insights

North America Floor Lamp Market Trends

North America remains the leading regional market, accounting for approximately 38.4% of global floor lamp demand, driven primarily by the United States. High disposable income levels support strong spending on premium home décor, positioning floor lamps as design-centric interior elements. Regulatory emphasis on energy efficiency, including state-level bans on inefficient lighting technologies, has accelerated LED adoption and standardized consumer preference toward advanced lighting solutions.

Commercial real estate growth and hospitality expansion across major U.S. cities continue to support demand for decorative and functional floor lamps. Advanced e-commerce infrastructure enables rapid expansion of direct-to-consumer channels. Design awareness among millennials and Gen Z consumers further fuels demand for statement floor lamps aligned with sustainability and personalized living trends.

Europe Floor Lamp Market Trends

Europe represents a mature and design-driven market, expanding at an estimated CAGR of around 4.9% over the forecast period. Germany, the United Kingdom, and France anchor regional demand, supported by stringent building energy efficiency regulations and strong adoption of LED technologies. EU-wide Ecodesign and Energy Labeling directives continue to drive innovation, quality standardization, and product differentiation across member states.

Environmental consciousness strongly influences purchasing behavior, sustaining demand for energy-efficient and sustainably sourced floor lamps. Germany emphasizes performance and compliance-driven solutions, while France and Southern Europe favor premium aesthetics and artisanal craftsmanship. The UK market shows renewed momentum, with wellness-oriented and human-centric lighting driving commercial and workplace applications.

Asia Pacific Floor Lamp Market Trends

Asia Pacific is the fastest-growing regional market, accounting for approximately 35.5% of global floor lamp demand, led by China, India, and Japan. China dominates regional consumption, supported by rapid urbanization, rising disposable incomes, and its dual role as a major lighting manufacturer and consumer market. Government-backed smart city initiatives further stimulate the adoption of advanced and connected lighting systems.

India’s market is expanding rapidly as urban housing development and middle-class spending on home décor increase. Consumers are transitioning toward design-focused and aesthetic lighting solutions. Japan remains a premium-driven market emphasizing energy efficiency, minimalist design, and smart home integration, supporting higher average selling prices and strong brand differentiation.

Competitive Landscape

The floor lamp market is highly fragmented, with the top three players collectively accounting for only about 10-12% of total demand. Low entry barriers for basic designs enable numerous regional and local manufacturers to compete aggressively on pricing and localized preferences. This fragmentation creates intense competition across mass and mid-range segments while leaving room for consolidation and brand differentiation through design, technology, and distribution strategies.

Competitive positioning is shaped by innovation in LED efficiency, smart lighting integration, and sustainability-focused materials. Companies increasingly emphasize connected features, customizable designs, and eco-conscious manufacturing. Cost-optimized production and direct-to-consumer digital channels allow emerging players to challenge established brands, particularly in price-sensitive segments.

Key Market Developments:

- In September 2025, Signify/Philips Lighting received 11 Red Dot Design Awards spanning its consumer and professional lighting product portfolio, reinforcing the company's position as a leader in innovative design and technological integration. The awards recognize excellence across floor lamp designs incorporating smart features, aesthetic innovation, and functional performance enhancements that advance market standards.

- In March 2025, the Z-Bar Titan Floor Lamp achieved international recognition for design excellence, featuring innovative USB-C charging (45-watt capacity), wireless Qi charging, and rotatable LED heads providing unprecedented functionality combining task lighting with consumer electronics integration. This award exemplifies market trends toward multifunctional floor lamps addressing contemporary consumer lifestyle needs.

- In February 2025, Cree LED launched advanced XLamp XP-L Photo Red S Line LEDs for specialized horticulture applications and introduced CV28D LEDs with FusionBeam Technology for display and sign applications, demonstrating continuous component-level innovation supporting broader floor lamp ecosystem advancement and manufacturer capabilities expansion.

Companies Covered in Floor Lamp Market

- IKEA Group

- Signify N.V.

- OSRAM GmbH

- Panasonic Corporation

- Acuity Brands, Inc.

- Zumtobel Group AG

- OPPLE Lighting Co., Ltd.

- Artemide S.p.A.

- FLOS S.p.A.

- Eglo Group

- Hubbell Lighting, Inc.

- Cree Lighting

- Louis Poulsen

- Foscarini

- Vibia

- Koncept Lighting

- GE Lighting

- Havells India Limited

- TCL Lighting

- NVC Lighting

Frequently Asked Questions

The global floor lamp market is projected to reach US$ 5.4 billion by 2033, up from US$ 3.9 billion in 2026 at a 4.7% CAGR, driven by LED adoption, smart homes, and home décor investments.

Growth is driven by LED adoption, government mandates, smart/IoT integration, rising incomes, urbanization, and eco-conscious consumer demand.

LED floor lamps lead with 65.7% market share due to efficiency, long lifespan, smart compatibility, and regulatory phase-outs.

North America holds 38.4% global share, supported by high incomes, advanced retail and e-commerce, and premium lighting demand.

Sustainable floor lamps using recycled, bamboo, FSC-certified, and biodegradable materials offer the highest growth potential.

Major market players include Signify N.V., OSRAM GmbH, Acuity Brands, Inc., IKEA Group, Panasonic Corporation, and Zumtobel Group AG.