- Beauty & Personal Care

- Facial Epilator Market

Facial Epilator Market Size, Share, and Growth Forecast, 2026 - 2033

Facial Epilator Market by Product Types (Dry skin epilators, Dual (Wet/Dry epilators), Foam epilators, and Wet skin epilators), By Formats (Cordless, Rechargeable, and Corded), by Distribution Channel (Online Stores, Hypermarket/Supermarket, Convenience Store, Specialty Store, Others) and Regional Analysis for 2026 - 2033

Facial Epilator Market Size and Trends Analysis

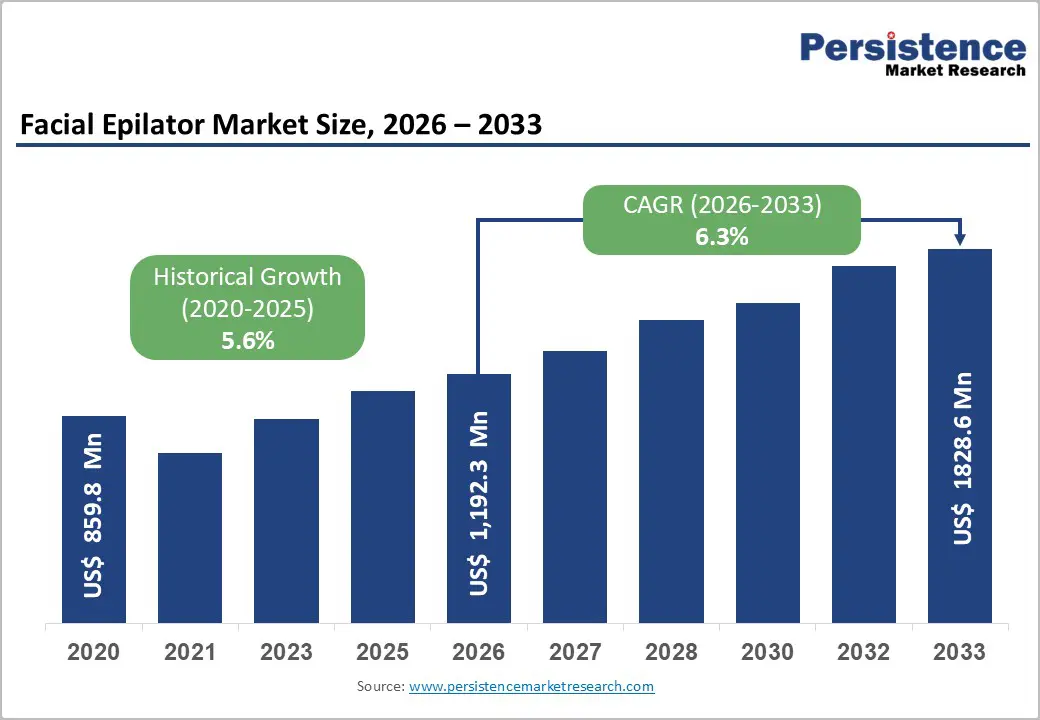

The global facial epilator market size is likely to be valued at approximately US$ 1.19 billion in 2026 and is projected to reach around US$ 1.83 billion by 2033, expanding at a CAGR of 6.3% during the forecast period. Facial epilators are handheld devices that typically use rotating tweezers and advanced mechanisms to ensure precision, convenience, and improved skin comfort. Growing consumer demand for at-home grooming solutions has significantly boosted worldwide demand for facial epilators.

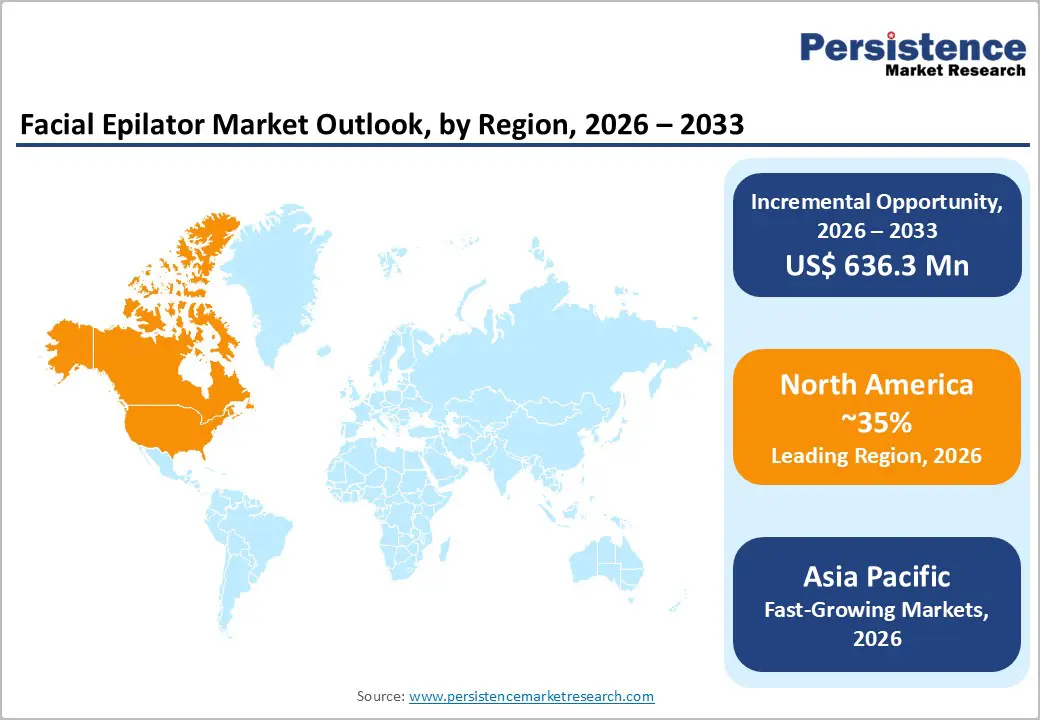

Market growth is primarily driven by rising awareness, changing beauty standards, and higher disposable income. Continuous product innovation, including cordless models, wet-and-dry functionality, hypoallergenic heads, and ergonomic designs, enhances user experience and supports adoption. The rapid expansion of e-commerce platforms further strengthens market penetration. Regionally, North America leads in revenue share due to strong consumer purchasing power, while Asia Pacific is the fastest-growing region, supported by urbanization and rising middle-class spending on personal care products.

Key Industry-Highlights:

- At-Home Grooming Shift: Rising DIY beauty routines and lasting post-pandemic salon substitution strengthen demand for convenient, long-lasting facial epilation devices across urban working women demographics globally.

- Pain Sensitivity Barrier: Skin irritation concerns and pain perception limit adoption, while alternatives like depilatory creams emphasize painless positioning, requiring brands to ensure clinical validation and safety assurances.

- Dry Epilators Lead: Dry epilators hold above 45% revenue share by 2026, driven by affordability, simple designs, wide availability, and strong penetration in price-sensitive offline markets.

- Wet Dry Premiumization: Dual wet/dry models grow fastest at 7.2% CAGR, supported by waterproof features, shower usability, improved comfort perception, and higher-margin upgrade pathways.

- Cordless Dominance Trend: Cordless formats are projected to exceed 60% revenue share by 2026, reflecting consumer preference for portability, flexibility, and enhanced convenience in bathroom and travel settings.

- Rechargeable Growth Surge: Rechargeable sub-segment expands at nearly 7.0% CAGR, driven by lithium-ion adoption, sustainability concerns, USB-C charging, and alignment with premium device ecosystems.

- Online Sales Leadership: Online channels surpass 45% revenue share by 2026, fueled by marketplaces, D2C platforms, influencer education, peer reviews, and cross-border beauty device discovery.

- North America Leadership: North America contributes above 35% global revenue in 2026, supported by high per-capita beauty spend, strong retail ecosystems, and premium cordless adoption.

- Asia Pacific Acceleration: Asia Pacific records fastest growth at 7.4% CAGR, driven by urbanization, social media beauty norms, manufacturing advantages, and expanding middle-class disposable incomes.

| Key Insights | Details |

|---|---|

|

Facial Epilator Market Size (2026E) |

US$ 1,192.3 Mn |

|

Market Value Forecast (2033F) |

US$ 1,828.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Dynamics

Drivers - Rising at-home grooming and self-care expenditure

Industry data show the global facial epilator market reached about US$ 445–470 Mn in 2023–2024, with forecasts of roughly US$ 648–684 Mn by 2030 at a 5.5–6.3% CAGR, confirming steady medium-term expansion. This reflects broader consumer shifts to at-home beauty routines and DIY grooming, reinforced by pandemic-era salon closures and lasting preference for convenient, repeatable treatments at home. As beauty device penetration increases, facial epilators gain share from shaving, threading, and depilatory creams by offering longer-lasting results and more precision on small facial areas. For manufacturers and retailers, this underpins a predictable volume base and supports premiumization and subscription-style replenishment models.

Demographic shifts and social media–driven beauty norms

Analysts highlight rising awareness of facial grooming among women, especially in working-age cohorts, as a core demand driver. North America and Europe lead current device penetration due to high per-capita beauty spend and established beauty device ecosystems. At the same time, Asia Pacific is seeing rapid uptake of beauty devices driven by urbanization, increasing female workforce participation, and social media beauty trends, particularly in China, Japan, South Korea, and India. As grooming standards and digital beauty content proliferate, facial epilators benefit from greater category education and word-of-mouth, supporting sustained volume growth and new-user recruitment.

Restraint - Skin sensitivity, pain perception, and safety concerns

Despite improvements, epilation remains associated with pain and potential irritation, which limits adoption among pain-averse and sensitive-skin users. Although many devices promote hypoallergenic materials and gentler operation, regulators and dermatological guidance continue to highlight the risks of inappropriate use, especially in delicate facial areas. Competing solutions such as depilatory creams and facial wax strips (e.g., Veet) emphasize painless or low-pain positioning and moisturization benefits, providing alternatives for consumers who avoid mechanical hair removal. For brands, this creates a persistent need for clinical validation, clear usage instructions, and post-purchase support to mitigate churn and negative word-of-mouth

Opportunity - Innovative Product Architectures Targeting Sensitive Skin and New User Segments

Manufacturers are already augmenting facial epilators with features such as flexible heads, multi-speed modes, facial-specific caps, and cleansing/massage attachments, as seen in Braun’s flexible-head epilators and Remington’s all-in-one facial kits. Philips’ facial hair remover series emphasizes hypoallergenic surfaces, gentle cutting technology, and self-sharpening blades, directly addressing pain and irritation concerns. Extending this innovation to dermatologist-tested sensitive-skin lines, male facial grooming, teenage starters, and inclusive skin-tone positioning offers scope for higher price-points and new segments.

Category-wise Analysis

Product Types Insights

Dry epilators anchor revenues while dual wet/dry drives premium growth

Scenario assumptions indicate dry skin epilators account for above 45% of market revenue in 2026, reflecting their lower price points, simpler designs, and wide availability across brands and retailers. This dominance aligns with industry segmentation, where dry epilators and basic models make up the largest installed base worldwide. They serve as accessible entry products, particularly in price-sensitive markets and offline channels, underpinning unit volumes and enabling brand trial before consumers upgrade to more advanced formats.

At the same time, dual (wet/dry) epilators are the fastest-growing product type. This aligns with trends toward waterproof and shower-friendly devices that promise reduced pain perception and greater convenience. Foam and wet-skin epilators remain in smaller niches but benefit from bundling with skincare routines and spa-like positioning. Strategically, vendors can manage a portfolio ladder: dry epilators as volume drivers, and dual wet/dry models as margin-rich upgrades with richer feature sets.

Formats Insights

Cordless platforms dominate usage as rechargeable architectures accelerate value capture

Cordless facial epilators are expected to command over 60% of revenues by 2026 under this scenario, reflecting strong consumer preference for freedom of movement and ease of use in the bathroom or on the go. Device comparisons consistently highlight cordless and battery-operated epilators from Braun, Philips, Panasonic, and Remington as leading recommendations for flexibility and convenience. Corded devices continue to appeal to budget-conscious buyers and those favoring stable power, but their share is gradually eroding as battery performance and charging speeds improve.

Rechargeable formats are projected as the fastest-growing sub-segment with about 7.0% CAGR, supported by sustainability concerns around disposable batteries and the shift to USB-C or inductive charging. Many flagship models already use rechargeable lithium-ion batteries with wet/dry compatibility and multi-speed settings. For brands, standardizing platforms on rechargeable cordless architectures simplifies R&D and supply chains, enables common accessories, and supports premium price tiers and warranty-based differentiation.

Distribution Channel Insights

Online channels lead sales while modern trade underpins incremental category reach

Industry research underscores the rapid growth of online channels in beauty devices, with e-commerce enabling cross-border sales, peer reviews, and influencer-driven discovery, especially for niche categories such as facial epilators. In the scenario, online stores are expected to exceed 45% share of global facial epilator revenues by 2026, reflecting strong representation on marketplaces and brand D2C sites. Brands such as Philips and Finishing Touch Flawless follow digital content, product videos, and customer reviews to demystify usage and build trust.

Hypermarkets and supermarkets are positioned as the fastest-growing offline channel, with an assumed CAGR of about 7.5%, as retailers broaden shelf space for beauty electrics and run price promotions to drive trial. Specialty stores and convenience outlets remain important for experiential discovery and impulse purchases in urban locations. For manufacturers, an omnichannel approach—balancing strong online visibility with curated offline placements—optimizes reach, pricing power, and brand equity.

Regional Insights and Trends

North America Facial Epilator Market Trends

North America is one of the largest regional markets for facial epilators and beauty devices, supported by high per-capita beauty expenditure and strong penetration of at-home grooming tools. Under this scenario, North America accounts for more than 35% of global facial epilator revenues in 2026, consistent with this leadership position. The United States dominates regional demand, with Canada providing additional volume in premium segments.

Growth in North America is underpinned by the rapid adoption of cordless and wet/dry epilators, dense e-commerce infrastructure, and strong retailer assortments in drugstores, mass merchants, and specialty chains. Regulatory oversight is also tightening: the U.S. FDA’s Modernization of Cosmetics Regulation Act (MoCRA) expands GMP, safety substantiation, and adverse-event reporting requirements for cosmetic products, indirectly raising expectations for devices marketed in close association with skincare regimes. The competitive landscape is relatively consolidated, with P&G’s Braun, Philips, Spectrum Brands’ Remington, Panasonic, Conair, and Wahl as key players. Investment opportunities center on premiumization, D2C ecosystem building, and dermatologist-endorsed sensitive-skin ranges, particularly targeting affluent and trend-sensitive consumers

Asia Pacific Emerges as High-Velocity Growth Engine for Category Expansion

Asia Pacific is widely recognized as the fastest-growing region for facial epilators and related beauty devices, driven by demographic scale and rapidly evolving beauty behaviors. Industry sources highlight China, Japan, South Korea, and India as key demand centers, with rising disposable incomes, social-media-driven beauty norms, and expanding modern retail channels fostering uptake of at-home grooming tools. Scenario assumptions place the Asia Pacific as the fastest-growing region with around 7.4% CAGR, materially above global averages.

Manufacturing advantages are another structural tailwind: major OEM and ODM hubs across China and Southeast Asia underpin competitive production costs and facilitate rapid product iteration for local preferences. Regulatory regimes vary, but many markets follow or adapt EU and US standards for electrical safety and cosmetic compatibility, creating both compliance complexity and opportunities to differentiate through certified safety and dermatologist partnerships. Competitive landscapes are becoming more fragmented as local brands and cross-border e-commerce entrants challenge global incumbents with regionally tailored aesthetics and pricing. Investment themes include localized marketing, K-beauty-style product design, and exclusive collaborations with regional influencers and platforms.

Competitive Landscape

The Facial Epilator Market demonstrates a moderately consolidated competitive landscape, where a limited number of multinational brands command a substantial market share, complemented by a wide base of regional and niche manufacturers. Prominent players include Braun (under Procter & Gamble), Philips, Remington (a Spectrum Brands company), Panasonic, Emjoi, Epilady, Tria Beauty, Conair, and Wahl. These companies benefit from diversified personal care portfolios, extensive global distribution networks, strong brand recognition, and continuous investments in research and development.

Simultaneously, emerging and innovation-driven brands such as Finishing Touch Flawless, along with several direct-to-consumer (D2C) entrants, are broadening the market’s reach. They are leveraging digital-first strategies, influencer marketing, and visually appealing product designs to attract younger consumers and tap into evolving beauty and grooming preferences.

Key Industry Developments

- In October 2025, Panasonic launched the Eyebrow & Face Epilator ES-EF10: A compact, pen-style facial epilator featuring four tweezers and an integrated LED precision light, designed to gently remove fine hairs without pinching, ensuring smooth brows and long-lasting facial skin results. Commercial rollout began in H2 2025, including Nordic markets.

- In September 2025, Pluxy launches Epil Pro 3.0: Positioned as a 2024 hair-removal innovation, this facial-focused epilator features 17 mm discs, Glide Technology, and silver-ion antimicrobial protection. It removes hair four times shorter than waxing while keeping skin smooth for up to four weeks, particularly suited for sensitive skin users, supported by strong global D2C and TikTok-linked campaigns.

Companies Covered in Facial Epilator Market

- Braun

- Philips

- Tria Beauty

- Emjoi

- Epilady

- Panasonic

- Remington

- Conair

- Wahl

- Andis

- Olay

- Silk'n

- Other Market Players

Frequently Asked Questions

The Facial Epilator market is estimated to be valued at US$ 1192.3 Mn in 2026.

The key demand driver for the Facial Epilator market is the rising consumer preference for convenient, at-home grooming solutions. Increasing awareness of personal appearance, evolving beauty standards, and busy lifestyles have led consumers to seek efficient, time-saving, and long-lasting facial hair removal options.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Facial Epilator market.

Among product types, dry skin epilators have the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other product types.

Braun, Philips, Tria Beauty, Emjoi, Epilady, Panasonic, and Remington a few leading players in the Facial Epilator market.