- Industrial Goods & Service

- Electric Hedge Trimmer Market

Electric Hedge Trimmer Market Size, Share, and Growth Forecast, 2026 - 2033

Electric Hedge Trimmer Market by Blade Type (Single Blade, Dual Blade, Rotary Blade, Laser Cut Blade, Diamond Ground Blade), Size of Hedge (Small Hedge, Medium Hedge, Large Hedge), and Regional Analysis for 2026 - 2033

Electric Hedge Trimmer Market Size and Trends Analysis

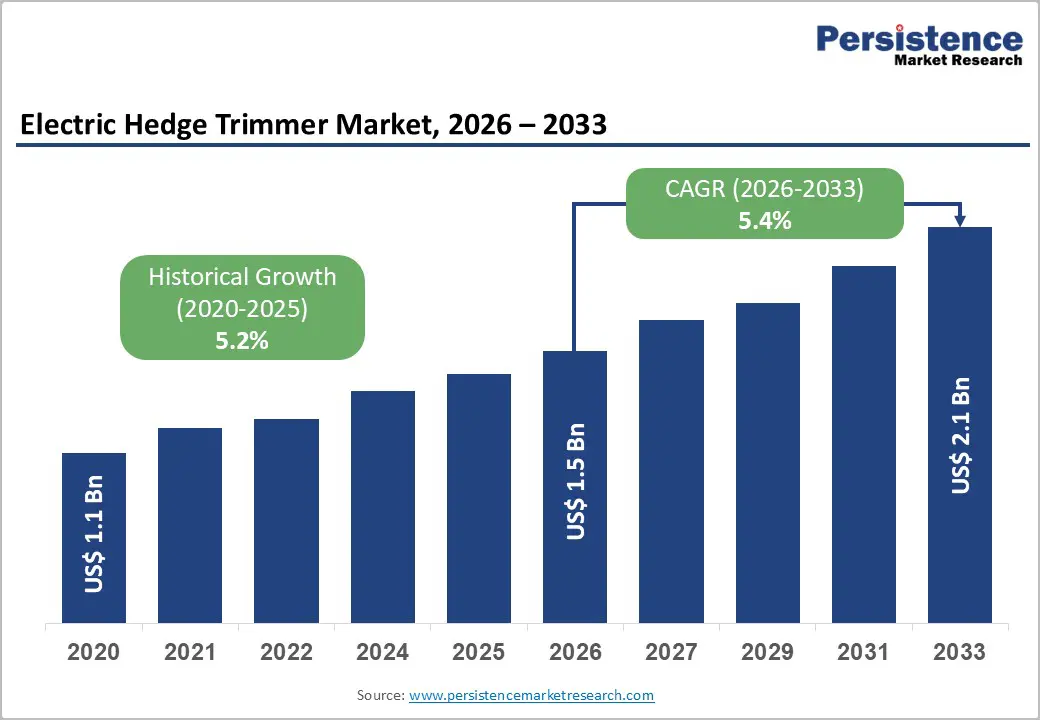

The global electric hedge trimmer market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$2.1 billion by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033, driven by increasing consumer preference for electric over gasoline-powered tools due to reduced emissions, lower maintenance requirements, improved safety, and quieter operation.

Rapid advancements in lithium-ion battery technology, offering enhanced runtime, faster charging cycles, lightweight configurations, and improved energy density, are significantly strengthening the value proposition of cordless models, which are gaining substantial traction over corded variants. Rising urbanization, expansion of residential housing projects, and increased investment in parks, recreational spaces, and smart city landscaping initiatives are reinforcing demand. Post-pandemic lifestyle shifts have also contributed to higher participation in home gardening and DIY lawn care activities, sustaining equipment replacement cycles and new product adoption.

Key Industry Highlights:

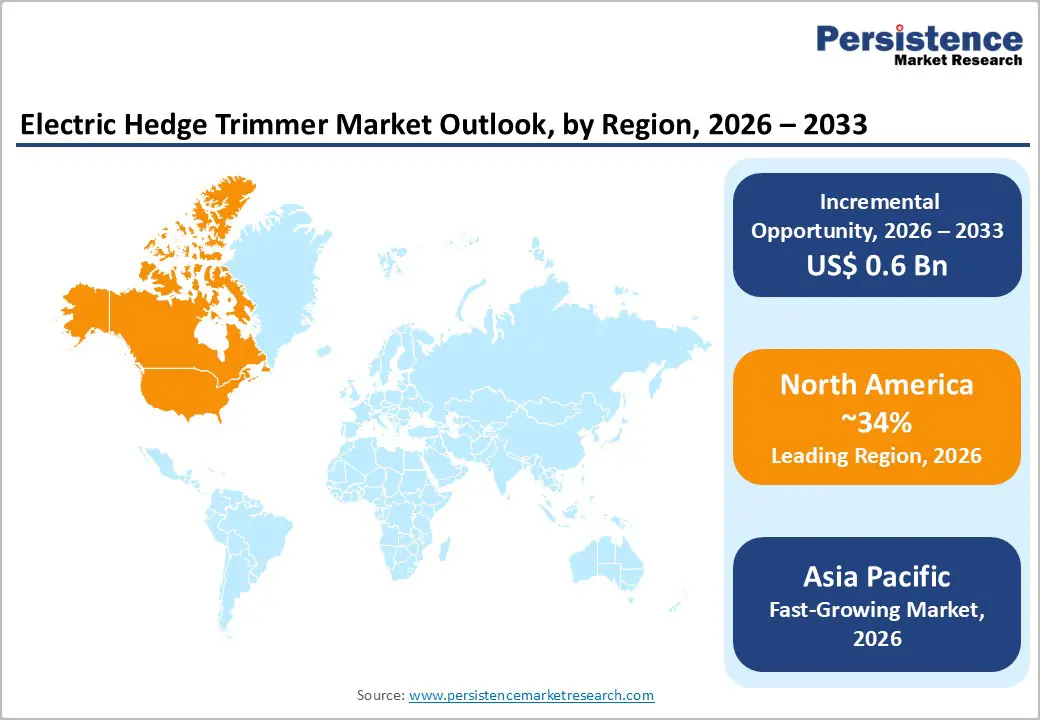

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 34% in 2026, driven by strong residential landscaping demand, regulatory support for low-emission equipment, and high adoption of advanced cordless hedge trimmers.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the electric hedge trimmer market in 2026, supported by strong manufacturing capacity, rapid urbanization, expanding residential gardening culture, and growing adoption of cost-competitive cordless models.

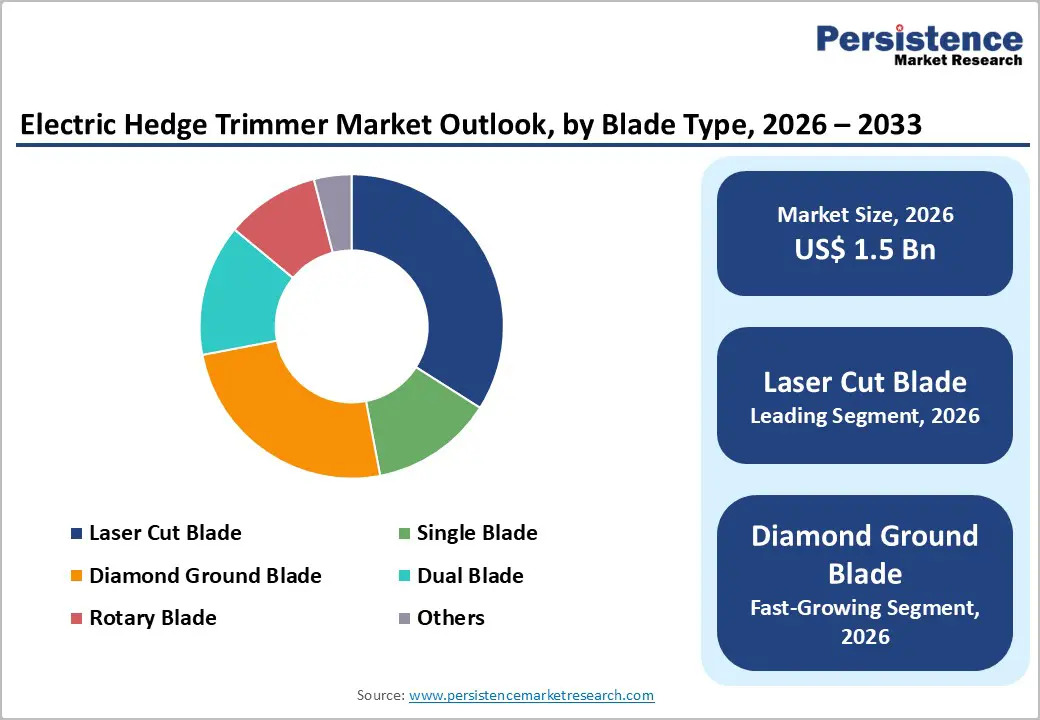

- Leading Blade Type: Laser cut blades are projected to represent the leading blade type in 2026, accounting for 55% of the revenue share, driven by superior cutting precision, enhanced durability, and strong preference in both residential and professional landscaping applications.

- Leading Size of Hedge: The medium hedge segment is anticipated to be the leading size of hedge, accounting for over 48% of the revenue share in 2026, supported by widespread residential landscaping needs and compatibility with standard cordless and electric hedge trimmer models.

| Key Insights | Details |

|---|---|

|

Electric Hedge Trimmer Market Size (2026E) |

US$1.5 Bn |

|

Market Value Forecast (2033F) |

US$2.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rise in Urban Gardening and DIY Culture

Urban gardening and DIY landscaping culture have significantly increased demand for electric hedge trimmers across residential markets. Increasing urbanization, smaller private gardens, balcony plantations, and compact green spaces have encouraged homeowners to invest in easy-to-use, lightweight gardening tools. Post-pandemic lifestyle shifts strengthened interest in home improvement and outdoor aesthetics, accelerating tool adoption. Electric hedge trimmers particularly benefit from this shift due to their low noise, minimal maintenance, and user-friendly operation. Growing awareness about sustainable living and self-maintained landscapes continues to reinforce steady product replacement cycles and first-time buyer expansion.

The DIY trend is especially prominent among younger homeowners and suburban households seeking cost savings from self-maintenance instead of professional landscaping services. Retail expansion through e-commerce platforms has improved product accessibility, reviews, and price transparency, encouraging impulse and seasonal purchases. Cordless models appeal strongly to DIY users due to convenience and mobility without fuel handling concerns. Social media gardening communities and home improvement content stimulate product awareness and engagement. As decorative hedging and lawn aesthetics become lifestyle preferences rather than occasional activities, the electric hedge trimmer market continues to benefit from sustained consumer participation in gardening culture.

Regulatory Push for Zero-Emission Tools

Stringent environmental regulations targeting carbon emissions and noise pollution are accelerating the shift from gasoline-powered hedge trimmers to electric alternatives. Governments across developed regions are implementing restrictions on small internal combustion engines, particularly in urban areas. These regulatory frameworks encourage the adoption of zero direct-emission outdoor tools, supporting electric hedge trimmer demand. Noise control ordinances in residential zones strengthen preference for quieter electric variants. Sustainability goals aligned with climate action policies are reshaping procurement standards for municipalities and commercial landscaping operators, driving steady replacement of conventional equipment with battery-powered solutions.

Incentive programs and rebate initiatives in certain regions promote electric landscaping equipment adoption. Public sector landscaping contracts increasingly prioritize environmentally compliant machinery, encouraging commercial fleets to transition toward cordless platforms. Manufacturers are responding by expanding lithium-ion battery ecosystems and brushless motor integration to meet performance expectations. Corporate sustainability commitments among landscaping service providers also reinforce electrification strategies. As regulatory frameworks become stricter and enforcement intensifies, the competitive advantage of electric hedge trimmers strengthens, positioning them as long-term replacements rather than supplementary tools in professional and residential markets.

Barrier Analysis - Battery Runtime and Performance Limitations in Demanding Applications

Despite technological progress, battery runtime remains a constraint in heavy-duty or large-scale landscaping applications. Professional users managing dense hedges or extended operational hours may experience limitations related to charging cycles and power consistency. While lithium-ion batteries offer improved energy density, runtime may still fall short compared to continuous fuel-powered equipment in high-demand conditions. This challenge impacts adoption in industrial landscaping and municipal maintenance, where uninterrupted performance is essential. Concerns about battery degradation over time and replacement costs also influence purchasing decisions among cost-sensitive buyers.

Extreme weather conditions can affect battery efficiency and tool performance, particularly in very hot or cold environments. Commercial operators often require multiple battery packs to maintain workflow continuity, increasing upfront investment. Although rapid-charging solutions mitigate downtime, infrastructure availability may vary across regions. Performance perception among traditional users accustomed to gasoline power can slow transition rates. While innovation continues to narrow the gap, runtime reliability in demanding professional applications remains a moderating factor influencing full-scale electrification within certain high-intensity landscaping segments.

Seasonal Demand Fluctuations and Inventory Management Challenges

The electric hedge trimmer market experiences pronounced seasonal demand patterns, with peak sales concentrated during spring and summer months. This cyclical purchasing behavior creates forecasting complexities for manufacturers and retailers. Off-season slowdowns can lead to excess inventory, promotional discounting, and margin pressure. Regional climate variations amplify unpredictability in demand cycles. Retailers must carefully balance stock availability with storage costs, especially for battery-powered models that involve bundled components. Such fluctuations can impact supply chain efficiency and production planning consistency.

Manufacturers also face challenges in aligning procurement of components such as batteries, motors, and blade systems with variable demand cycles. Overproduction risks inventory buildup, while underproduction may result in lost sales during peak seasons. E-commerce channels partially smooth demand variability, but physical retail remains influenced by climate-driven buying patterns. Professional landscaping demand varies based on municipal budget allocations and contract timing. These seasonal dynamics require strategic inventory optimization, flexible manufacturing capacity, and advanced demand forecasting to minimize operational inefficiencies across the value chain.

Opportunity Analysis - Technological Convergence with Smart Features and Interchangeable Batteries

Manufacturers are increasingly incorporating smart features such as battery health monitoring, load sensing, overload protection, and connectivity with mobile applications. Interchangeable battery platforms compatible across multiple outdoor tools enhance ecosystem value and encourage brand loyalty. Consumers benefit from reduced long-term ownership costs by sharing battery systems across lawn equipment. This convergence strengthens differentiation in competitive markets and promotes repeat purchases within integrated product portfolios.

Professional users particularly value battery platform compatibility, which enables fleet standardization and operational efficiency. Smart diagnostics and performance tracking support predictive maintenance and improved productivity management. Integration with smart home ecosystems enhances appeal among tech-oriented consumers. As brushless motor efficiency improves and battery charging speeds accelerate, product reliability and user convenience continue to expand. These advancements create opportunities for premium product positioning, higher-margin offerings, and stronger penetration within both residential and commercial landscaping segments worldwide.

Product Innovation in Lightweight, Ergonomic, and Low-Noise Designs

Product innovation focused on lightweight construction and ergonomic handling is unlocking new customer segments, including elderly users and urban residents with limited storage space. Advances in composite materials and compact motor design reduce overall tool weight while maintaining cutting efficiency. Improved grip designs, vibration reduction mechanisms, and balanced weight distribution enhance user comfort during extended operation. These features contribute to increased adoption among DIY consumers seeking ease of use and reduced physical strain.

Low-noise operation remains a competitive advantage in densely populated residential areas where sound regulations restrict equipment usage. Innovations in blade engineering, motor insulation, and housing design minimize acoustic output. Compact cordless models designed for small hedges and balcony gardens are gaining popularity in urban apartments. Continuous refinement in design aesthetics also strengthens consumer appeal. As user-centric innovation continues to evolve, manufacturers can capture incremental demand by aligning product development with comfort, convenience, and sustainability expectations in modern landscaping practices.

Category-wise Analysis

Blade Type Insights

Laser cut blade are expected to lead the electric hedge trimmer market, accounting for approximately 55% of revenue in 2026, driven by their superior cutting precision, smoother finish, and ability to handle medium-density hedges with minimal vibration. These blades are manufactured using advanced laser technology, ensuring uniform tooth spacing and sharper edges that improve operational efficiency. Dual-blade reciprocating mechanisms enhance performance, making them highly preferred in both residential and light-commercial landscaping applications. For example, the laser-cut blade systems used in premium cordless hedge trimmers offered by Makita are widely recognized for clean cutting performance and durability in suburban landscaping environments.

Diamond ground blades are likely to represent the fastest-growing segment in 2026, supported by their exceptional edge retention, durability, and reduced maintenance requirements. These blades undergo precision grinding processes that create extremely sharp and hardened cutting surfaces, extending operational lifespan compared to standard blades. Professional landscapers increasingly prefer diamond-ground systems because they minimize sharpening frequency and downtime, improving overall productivity. Rising labor costs and demand for high-performance tools support this growth trend. For example, the adoption of diamond-ground blade technology in professional-grade hedge trimmers from Husqvarna is where durability and long-term reliability are key value propositions for commercial fleet operators.

Size of Hedge Insights

The medium hedge segment is projected to lead the market, capturing around 48% of the revenue share in 2026, supported by its alignment with typical residential and suburban landscaping requirements. Most urban and suburban properties feature hedges of moderate height and density, requiring balanced power and blade length configurations. Electric hedge trimmers designed for medium hedges offer optimal runtime, manageable weight, and efficient cutting capability, making them versatile for both homeowners and light-commercial users. Their compatibility with standard cordless platforms enhances accessibility and replacement demand. For example, medium-hedge-focused cordless trimmers marketed by STIHL cater extensively to suburban garden maintenance and small landscaping contracts.

Small hedge is likely to be the fastest-growing size of hedge in 2026, driven by increasing urban apartment living, balcony gardening, and compact outdoor spaces. Lightweight cordless hedge trimmers designed for smaller hedges offer convenience, easy storage, and reduced physical strain, making them attractive to DIY users and elderly homeowners. Growth is influenced by post-pandemic gardening enthusiasm and aesthetic improvements in limited spaces. Compact design innovation and lower noise levels strengthen adoption in densely populated areas. For example, compact hedge trimmer models introduced by RYOBI are specifically engineered for small-scale residential trimming and urban gardening applications.

Regional Insights

North America Electric Hedge Trimmer Market Trends

North America is anticipated to be the leading region, accounting for a market share of 34% in 2026, driven by rising environmental awareness, regulatory pressures, and evolving consumer preferences. Urban and suburban homeowners increasingly seek low-noise, low-emission tools that align with stringent municipal regulations and state-level restrictions on gasoline-powered equipment. Retailers and distributors report growing sales of cordless electric models, particularly those featuring brushless motor technology, longer battery life, and enhanced ergonomics. The integration of advanced lithium-ion battery platforms across multiple outdoor power tools has strengthened brand loyalty and reduced total ownership costs for consumers.

Commercial landscaping services are also embracing electric hedge trimmers as part of broader sustainable operations strategies. Professional users are transitioning to cordless fleets to reduce fuel expenditures, maintenance downtime, and noise complaints in urban environments. Innovation in connected and sensor-enabled capabilities, including battery health diagnostics and real-time performance monitoring, is strengthening the appeal of premium models within the professional segment. A notable example is EGO Power+, whose modular battery ecosystem and high-performance hedge trimmers have achieved strong adoption among landscaping professionals across North America.

Europe Electric Hedge Trimmer Market Trends

Europe is likely to be a significant market for electric hedge trimmers in 2026 due to regulatory norms and modern landscaping preferences that align with electric tool adoption. Across major Western European countries, strict emissions and noise regulations are prompting homeowners and professional landscapers to replace gasoline models with electric alternatives. Government incentives and environmental policies focused on reducing urban air and sound pollution reinforce this shift. Growing interest in suburban and small-space gardening has driven demand for lightweight, cordless hedge trimmer models that deliver convenience without compromising performance.

Professional landscaping services across Europe are also integrating electric hedge trimmers into their equipment fleets, as these tools offer reduced maintenance requirements, lower operational expenditure, and enhanced compliance with local environmental standards. For example, Bosch’s electric hedge trimmer offerings in Europe emphasize balanced power, long-lasting lithium-ion battery platforms, and user-friendly features that resonate with both DIY gardeners and commercial landscaping crews. Collaborations between European manufacturers and regional distributors are enhancing product availability and after-sales services, while landscaping trade events spotlight emerging cordless technologies and battery ecosystems.

Asia Pacific Electric Hedge Trimmer Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by rising disposable incomes and expanding residential landscaping activities are driving broader tool adoption. Countries such as China, Japan, India, and ASEAN members are witnessing growing interest in outdoor power equipment that combines efficiency with environmental sustainability. Rapid infrastructure development and green-city initiatives are encouraging homeowners and landscapers to adopt electric hedge trimmers, particularly cordless models that deliver mobility and reduced operational noise. E-commerce growth is a strong facilitator in this region, making a diverse range of electric hedge trimmers accessible to both urban and semi-urban consumers.

Professional landscaping services and commercial property managers are also integrating electric hedge trimmers into standard equipment fleets to align with sustainability goals and to reduce dependence on fuel-powered machines. For example, Zhejiang Zomax Garden Machinery, whose electric hedge trimmer offerings in China and neighboring markets emphasize cost efficiency, competitive performance, and localized service support. These products appeal to both individual consumers and commercial users seeking value-oriented yet reliable solutions. Regional manufacturers are increasingly leveraging cost-competitive supply chains and localized production advantages to drive product availability and affordability.

Competitive Landscape

The global electric hedge trimmer market exhibits a moderately fragmented structure, driven by the presence of numerous regional and international manufacturers offering a range of corded and cordless models tailored to residential, commercial, and professional landscaping segments. Competition spans established power tool brands and specialized outdoor equipment makers, focusing on innovation, performance, and sustainability. Innovation in battery technology, ergonomic design, and integrated safety features is a key differentiator in product portfolios.

Key market leaders such as Husqvarna, STIHL, Bosch, Makita, EGO Power+, and RYOBI compete through strong R&D investments, continuous expansion of cordless battery ecosystems, and diversified product portfolios tailored to varying power requirements and user preferences. Their competitive strategies also include targeted marketing initiatives, strategic regional distribution partnerships, and technology collaborations designed to enhance product performance and elevate customer experience.

Key Industry Developments:

- In February 2026, STIHL unveiled its most powerful battery-powered long-reach hedge trimmers, the HLA 150 B and HLA 140 K-B/B models, designed for demanding landscaping tasks, featuring adjustable telescopic shafts, double-edged blades for efficient cutting at various heights, and advanced battery-powered motors that deliver quiet, robust performance while enhancing operator flexibility and productivity in professional maintenance applications.

- In February 2025, Milwaukee launched the new M18 FUEL™ 60 cm and 75 cm electric hedge trimmers designed for landscape professionals, featuring robust dual-sharpened blades with a 32 mm tooth gap and POWERSTATE™ brushless motors for powerful cutting performance and precise control, enhancing productivity and clean cutting in demanding trimming applications.

Companies Covered in Electric Hedge Trimmer Market

- American Honda Motor

- Husqvarna

- STIHL

- Blount International

- GreenWorks Tools

- MTD

- Stanley Black and Decker

- Flymo

- ECHO

- Robert Bosch

- The Toro Company

- Ernak

- Makita

- RYOBI

- Zhejiang Zomax Garden Machinery

Frequently Asked Questions

The global electric hedge trimmer market is projected to reach US$1.5 billion in 2026.

The electric hedge trimmer market is driven by rising demand for low-emission, low-noise landscaping tools supported by urban gardening trends and advancements in lithium-ion battery technology.

The electric hedge trimmer market is expected to grow at a CAGR of 5.4% from 2026 to 2033.

Key market opportunities lie in expanding cordless battery platforms, smart-feature integration, and growing demand for lightweight, ergonomic, and eco-friendly landscaping equipment across residential and professional segments.

American Honda Motor, Husqvarna, STIHL, Blount International, GreenWorks Tools, and Stanley Black & Decker are the leading players.