- Medical Devices

- Digital Biomarkers Market

Digital Biomarkers Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Digital Biomarkers Market by Product Type (Wearable, Mobile Based Applications, Sensors, Others), Clinical Practice (Diagnostic Digital Biomarkers, Monitoring Digital Biomarkers, Predictive and Prognostic Digital Biomarkers, Others), Therapeutic Area (Cardiovascular and Metabolic Disorders (CVMD), Neurodegenerative Disorders, Diabetes, Respiratory Disorders, Sleep and Movement Disorders, Others), End-user (Healthcare Consumers, Healthcare Providers, Others), and Regional Analysis from 2026 to 2033

Digital Biomarkers Market Share and Trends Analysis

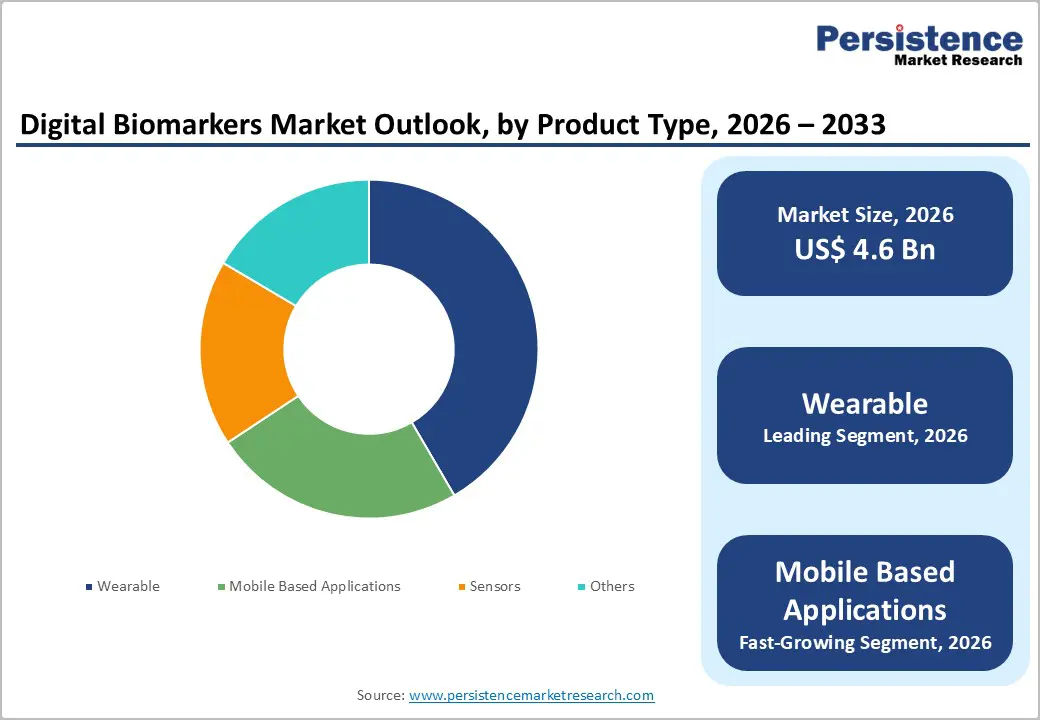

The global digital biomarkers market is estimated to grow from US$ 4.6 billion in 2026 to US$ 18.7 billion by 2033. The market is projected to record a CAGR of 22.1% during the forecast period from 2026 to 2033.

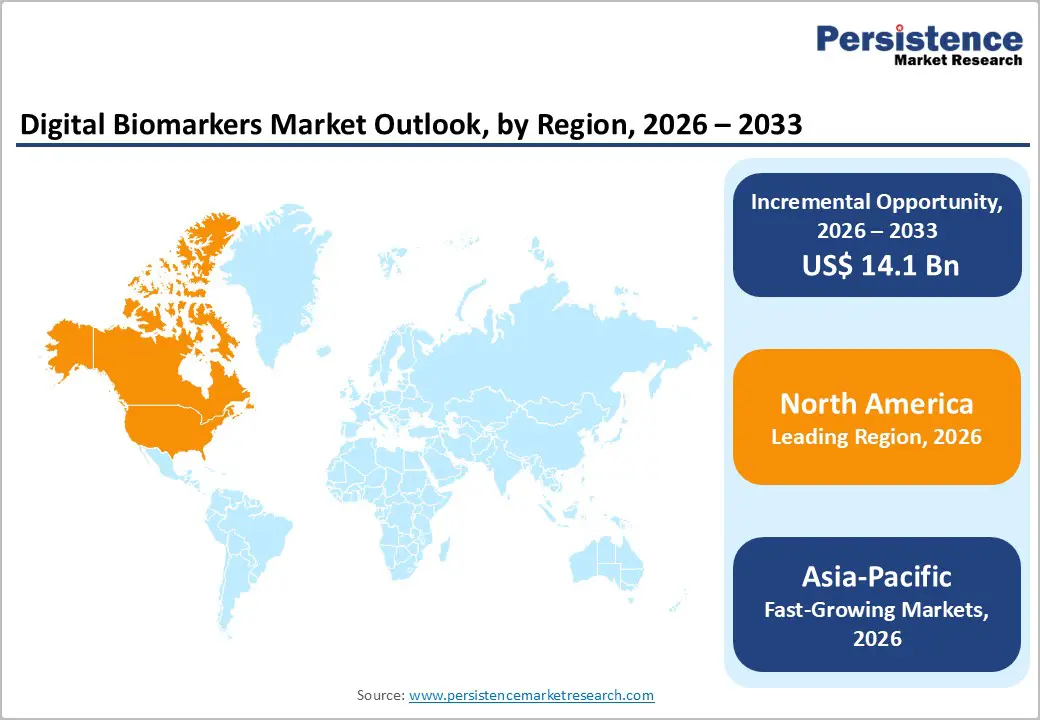

The global digital biomarkers market is growing rapidly due to aging population, rising chronic disease prevalence, and increasing demand for remote patient monitoring. North America dominates, supported by advanced healthcare infrastructure and FDA regulatory leadership. Asia-Pacific is the fastest-growing region, driven by expanding smartphone penetration, supportive government digitization policies, local device manufacturing, and rising investments in AI-powered healthcare technologies.

Key Industry Highlights:

- Dominant Segment: Diagnostic digital biomarkers holds 52.3% share in 2025, driven by their critical role in early disease detection, arrhythmia screening, and cognitive assessments, along with point-of-care accuracy and compatibility with wearables and mobile platforms.

- Dominant Region: North America leads in 2025 with 45.5% share, supported by FDA regulatory frameworks, Medicare reimbursement policies, and strong adoption of remote patient monitoring in clinical trials. Asia-Pacific is the fastest-growing region, fueled by smartphone penetration, government AI mandates, rising chronic disease burden, and increasing investment in digital health infrastructure.

- Market Drivers: Market growth is driven by rising chronic disease prevalence, increasing adoption of wearables and mobile health apps, aging populations, growth in decentralized clinical trials, and technological advancements in AI/ML algorithms for continuous health monitoring.

- Market Opportunity: Key opportunities include expansion of voice and vocal biomarkers, growth in mental health and neurodegenerative monitoring, rising demand in emerging markets, integration with telemedicine platforms, and development of FDA-cleared, consumer-grade devices improving early intervention and personalized medicine.

| Key Insights | Details |

|---|---|

| Global Digital Biomarkers Market Size (2026E) | US$ 4.6 Bn |

| Market Value Forecast (2033F) | US$ 18.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 22.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 20.5% |

Market Dynamics

Driver: Increasing Adoption of Wearables and Mobile Health Technologies

The digital biomarkers market is experiencing unprecedented growth driven by the rapid adoption of wearable devices and mobile health applications among consumers worldwide. According to the National Institutes of Health's Health Information National Trends Survey, wearable device usage among U.S. adults increased from 28-30% in 2019 to 36.36% in 2022, with 44% of Americans owning wearable health tracking devices by 2023. This surge reflects a fundamental shift in consumer health engagement, with over 80% of wearable device users willing to share information with their doctors to support health monitoring. The global wearable shipments have surpassed 543 million units in 2024, representing a 6.1% increase from the previous year, with projections indicating smartwatch users alone will reach 740 million globally by 2029.

The integration of wearables into healthcare ecosystems is transforming patient care delivery and clinical research methodologies. Research published in PMC journals demonstrates that individuals using wearable devices are approximately 32% more likely to adopt telehealth services compared to non-users, facilitating remote patient monitoring and decentralized clinical trials. The FDA has recognized this transformation by establishing the Digital Health Center of Excellence and approving over 215 sensor-based digital health technologies, including continuous glucose monitors like Dexcom G7 and cardiac monitoring devices such as Apple Watch's AFib detection feature.

Restraint: Lack of Standardized Data Collection and Analysis Protocols

The absence of standardized protocols for data collection and analysis represents a critical barrier hindering the clinical adoption and regulatory approval of digital biomarkers. Research published in PMC journals highlights that clinical test data originates from multiple sources without standardized collection and storage protocols, creating systematic biases across institutions due to variations in testing equipment parameters and operational standards. This heterogeneity severely limits the ability to combine data from multiple studies or replicate findings across different populations, fundamentally undermining the validity and reliability of digital biomarker research. The Digital Biomarker Discovery Pipeline study emphasizes that proprietary algorithms from wearable manufacturers do not provide information on their verification and validation processes, making it difficult to confirm the validity of aggregate metrics.

The standardization challenge extends beyond technical specifications to encompass regulatory compliance and clinical implementation pathways. According to research on vocal biomarkers, many datasets are privatized and available datasets are not large enough to develop meaningful biomarkers, reflecting a structural issue where stakeholders lack strong incentives to make their data or methodologies transparent. The lack of common data formats, calibration procedures, and quality control metrics applicable across different research environments has historically prevented the establishment of universal standards essential for regulatory approval. Studies indicate that without standardized metadata annotation practices, data integration across different biobanks becomes inherently challenging, with inconsistent terminology and annotation protocols leading to incomplete metadata that hinders accurate interpretation and analysis.

Opportunity: Development of Standardization Frameworks and Regulatory Pathways

The establishment of comprehensive standardization frameworks presents a transformative opportunity to unlock the digital biomarkers market's full potential. The FDA's recent guidance on Digital Health Technologies for Remote Data Acquisition in clinical investigations, issued in December 2023, provides crucial regulatory clarity that enables developers to design fit-for-purpose validation protocols and bring-your-own-device approaches. Collaborative initiatives such as the Quantitative Imaging Biomarkers Alliance and European Imaging Biomarkers Alliance are actively working to identify barriers and develop solutions for standardizing numerical descriptors and analysis procedures, while the Image Biomarker Standardization Initiative has already defined 174 radiomic features with standardized nomenclature and processing schemes.

The convergence of standardization efforts with artificial intelligence and federated learning technologies creates unprecedented opportunities for collaborative research while maintaining data sovereignty and patient privacy. Investment in digital biomarker platforms has accelerated dramatically, with notable funding including Koneksa Health's USD 45 million Series C raise in 2022, BioSensics receiving a USD 2 million NIH contract in May 2024, and DANNCE.AI securing USD 2.6 million in pre-seed investment in November 2024. Government initiatives further support this ecosystem, with the U.S. Precision Medicine Initiative allocating USD 5.6 million in June 2024 specifically for rare disease biomarker research. The development of master protocols, open-source software platforms like the Digital Biomarker Discovery Pipeline, and standardized frameworks such as the V3 verification-validation-clinical validation model are democratizing access to digital biomarker development, enabling multidisciplinary collaboration between computational experts and clinical domain specialists to accelerate innovation and regulatory approval pathways.

Category-wise Analysis

By Product Type Insights

Wearable Devices are leading with 41.6% share in 2025, because they provide continuous, real-time physiological and behavioral data that traditional episodic clinical tests cannot match. Wearables capture heart rate, activity levels, sleep quality, and other parameters continuously, enabling richer, longitudinal datasets essential for early detection and personalized health insights. Their widespread consumer adoption and integration into everyday life also lower barriers to large-scale data collection, enhancing research and clinical utility. Real-world evidence shows that wearables are the primary data source in over 70% of digital biomarker studies that systematically review device usage in clinical contexts.

By Application Insights

Diagnostic digital biomarkers lead the clinical practice segment because they provide the most immediate clinical value: identifying or confirming the presence of disease. Market analyses show diagnostic digital biomarkers captured the largest share of clinical practice use about 52.3% of the global digital biomarkers market in 2025, higher than monitoring or predictive categories. Their dominance stems from widespread clinical adoption of digital tools that detect disease signatures earlier or more precisely than conventional approaches, such as smartphone-derived gait or speech data for neurological disorders, or retina imaging algorithms for diabetic eye disease. Moreover, regulatory clearances (e.g., CE marks on wearable diagnostic tools) and integration into clinical workflows have accelerated their uptake, reinforcing diagnostic digital biomarkers as primary contributors to clinical decision-making.

Regional Insights

North America Digital Biomarkers Market Trends

North America leads the global digital biomarkers market primarily because of its mature digital healthcare ecosystem and high technology adoption. The United States has a strong healthcare IT infrastructure, widespread use of wearables and mobile health technologies, and a large volume of clinical research incorporating digital endpoints. For instance, the U.S. hosts over 11,000 clinical trials, many of which leverage digital health data for chronic disease outcomes, according to the International Clinical Trials Registry Platform, which increases demand for digital biomarkers. Moreover, chronic diseases such as coronary artery disease affect millions of adults in the U.S., creating a substantial need for continuous monitoring and personalized care tools that digital biomarkers provide.

Europe Digital Biomarkers Market Trends

Europe is a key regional market for digital biomarkers, driven by strong public health infrastructure and policies promoting healthcare digitization. European countries, especially Germany, the United Kingdom, and the Nordics, are actively integrating digital health technologies into clinical care and research, supported by EU-wide initiatives on digital health data interoperability. The World Health Organization notes that digital health adoption is increasing across the WHO European Region, transforming how conditions such as cancer, diabetes, and mental health are diagnosed and managed. Europe’s focus on data privacy and harmonized regulation (e.g., GDPR) also fosters the development of digital biomarker platforms that respect patient rights while enabling clinical innovation, making it a strategically important, stable market.

Asia-Pacific Digital Biomarkers Market Trends

The Asia Pacific region is the fastest-growing market for digital biomarkers, with forecasts suggesting double-digit CAGR growth driven by expanding digital health adoption, a large patient population, and rising healthcare investments. Countries such as China, Japan, India, and South Korea are increasing the deployment of mobile-based health monitoring, wearable sensors, and remote patient management solutions as part of broader digital health strategies. Rapid smartphone penetration and government efforts, such as national digital health missions, support the uptake of digital technologies. In addition, the burden of chronic diseases in the Asia Pacific is rising sharply; the WHO reports that non-communicable diseases account for a large share of mortality worldwide, a trend reflected in Asia’s ageing and urbanizing populations. These factors combine to make Asia Pacific a dynamic region with the highest projected growth rates in digital biomarker adoption.

Competitive Landscape

The digital biomarkers market is moderately fragmented, with competition among specialized digital health firms, wearable technology companies, and pharmaceutical collaborators. Key players focus on sensor accuracy, AI-driven analytics, clinical validation, and regulatory compliance. Strategic partnerships, pilot studies, and integration into clinical trials differentiate competitors and drive market positioning.

Key Industry Developments:

- In January 2026, Altoida and Mindspan announced a research collaboration to use AI- and augmented reality-powered digital cognitive assessments to personalize cognitive care. The partnership aimed to combine Altoida’s validated digital biomarkers with Mindspan’s clinical expertise to enable earlier detection of cognitive decline, improve diagnostic precision, and tailor interventions for patients with neurological and cognitive disorders.

- In January 2025, ActiGraph accelerated clinical trial modernization by completing the acquisition of Biofourmis’ Life Sciences business. The acquisition expanded ActiGraph’s digital measurement and analytics capabilities, strengthened its decentralized clinical trial offerings, and enhanced the use of wearable-derived digital biomarkers to improve patient monitoring, data quality, and trial efficiency.

Companies Covered in Digital Biomarkers Market

- ActiGraph LLC

- AliveCor Inc.

- Koneksa Health

- Altoida Inc.

- Biogen

- Empatica Inc.

- Vivo Sense

- IXICO plc

- Aural Analytic

- Huma

- Sonde Health, Inc.

- Akili Interactive Labs, Inc.

- Cambridge Cognition Ltd.

- Dassault Systemes (Medidata)

- Shimmer

- Feel Therapeutics

- Clario

- Imagene AI

- Brainomix

- Kinsa Inc.

- Pfizer Hellas S.A.

- Human API

- Evidation Health, Inc.

- Verily

- electronRx

- Others

Frequently Asked Questions

The global digital biomarkers market is projected to be valued at US$ 4.6 Bn in 2026.

Rising chronic diseases, wearable adoption, AI analytics, remote patient monitoring demand, and regulatory support drive market growth.

The global digital biomarkers market is poised to witness a CAGR of 22.1% between 2026 and 2033.

Expansion in decentralized trials, personalized medicine, AI-driven diagnostics, emerging markets, and integration with electronic health records.

ActiGraph LLC, AliveCor Inc., Koneksa Health, Altoida Inc., Biogen, Empatica Inc.