- Metalworking & Fabrication

- Cutting Tool Inserts Market

Cutting Tool Inserts Market Size, Share, and Growth Forecast 2026 - 2033

Cutting Tool Inserts Market by Product Type (Turning Inserts, Milling Inserts, Drilling Inserts and Specialty Inserts), Material (Carbide Inserts, Ceramic Inserts, Cubic Boron Nitride Inserts and Polycrystalline Diamond Inserts), Application (Metal Machining, Woodworking, Composite Materials and Plastic Machining), End-User (Automotive, Aerospace, General Manufacturing, Construction and Mining) and Regional Analysis 2026 - 2033

Cutting Tool Inserts Market Share and Trends Analysis

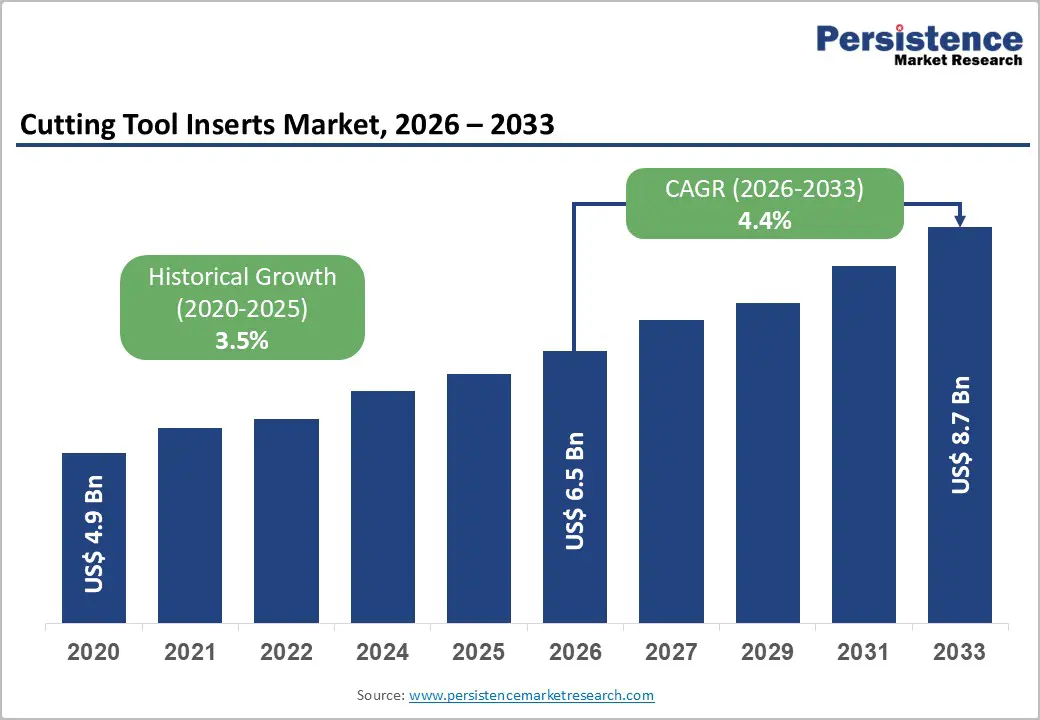

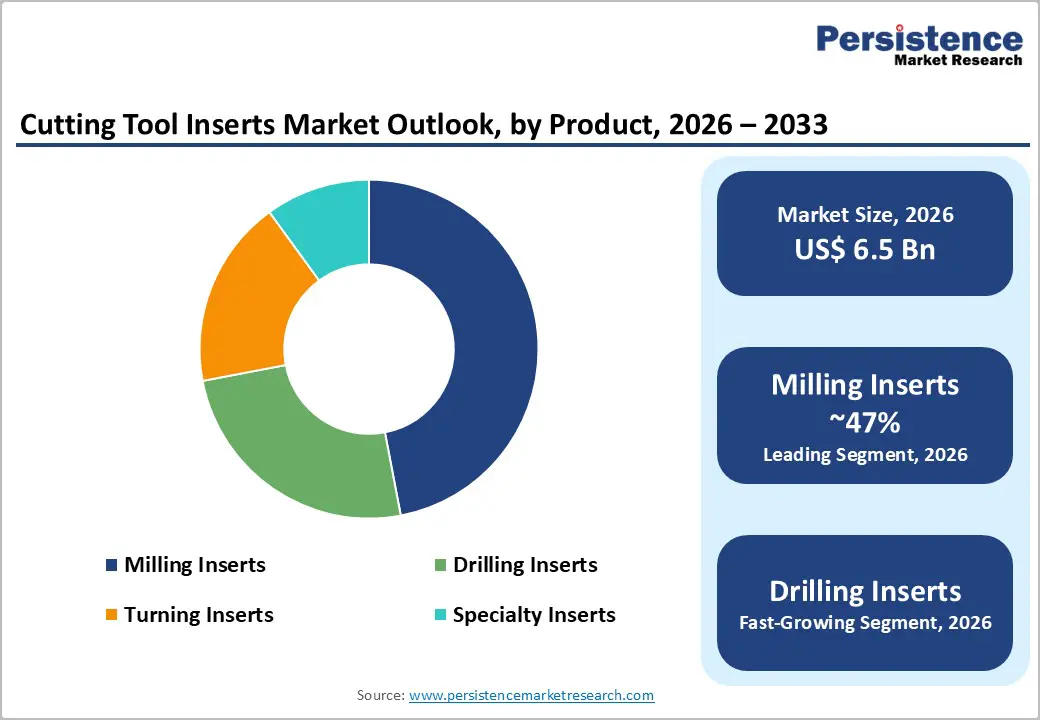

The global cutting tool Inserts market size is likely to be valued at US$ 6.5 billion in 2026 and is projected to reach US$ 8.7 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

This market expansion is fundamentally driven by accelerating demand for precision machining in the automotive and aerospace sectors, with manufacturers increasingly adopting advanced carbide and ceramic inserts and coated cutting tools to enhance operational efficiency and reduce tool-life costs. The proliferation of computer numerical control (CNC) machinery globally and rising investments in manufacturing automation across emerging economies, including China, India, and Vietnam, are creating sustained demand for specialized cutting solutions.

Key Industry Highlights:

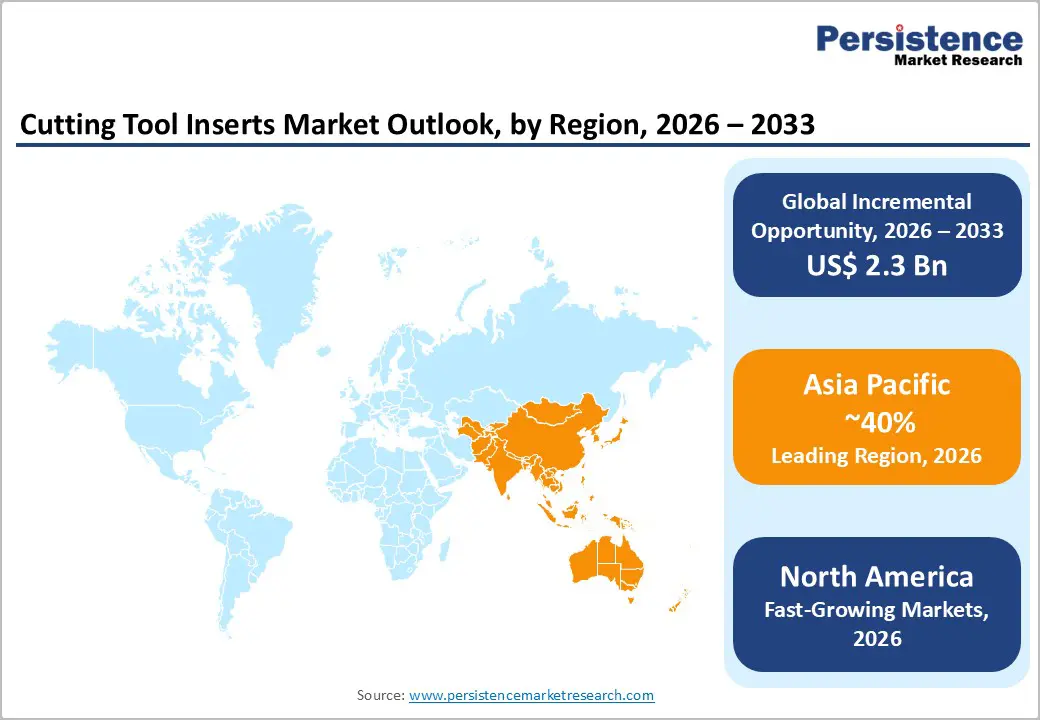

- Leading Region: Asia Pacific dominates the global market with 40% share driven by China's 29 million annual vehicle production, India's expanding automotive sector reaching 4.5 million units, and emerging manufacturing capabilities in Vietnam, Thailand, and Indonesia, supporting exceptional demand expansion through 2033

- Fastest-Growing Region: Fastest growing application segments include advanced automotive electric drivetrain component machining and aerospace composite material operations, expanding at 8% annually, driven by EV manufacturing acceleration and aircraft production rate increases

- Dominant Product Segment: Carbide inserts maintain 64% market dominance driven by versatility across diverse materials, cost-per-part justification through extended tool life, and continued adoption of advanced PVD and CVD coating systems, enhancing thermal stability and wear resistance

- Fastest-Growing Region: Coated cutting tool inserts demonstrate exceptional growth momentum with 25% extended tool life compared to uncoated alternatives, accelerated adoption driven by dry machining mandates and environmental sustainability objectives, reducing coolant consumption by up to 90%

- Opportunity: Strategic manufacturer consolidation and vertical integration initiatives, including SANDVIK's Buffalo Tungsten acquisition, exemplify market emphasis on supply chain resilience and raw material security amid volatile commodity pricing and geopolitical supply considerations.

| Key Insights | Details |

|---|---|

| Cutting Tool Inserts Market Size (2026A) | US$ 6.5 Bn |

| Projected Year Value (2033F) | US$ 8.7 Bn |

| Value CAGR (2026 - 2033) | 4.4% |

| Historical Market Growth Rate (CAGR 2019 to 2023) | 3.5% |

Market Dynamics

Drivers - Accelerating Precision Machining Demand in Automotive and Aerospace Industries Supporting Equipment Adoption

The automotive and aerospace sectors represent critical market drivers, collectively accounting for substantial cutting tool insert consumption driven by increasing manufacturing complexity and quality requirements. Global automotive production continues advancing toward electric vehicle (EV) manufacturing, necessitating specialized machining solutions for battery housings, lightweight aluminum components, and precision transmission systems. According to projections from the International Energy Agency (IEA), electric vehicle sales are expected to account for approximately 35% of total automotive production by 2033, prompting manufacturers to invest in advanced machining capabilities. Aerospace machining demand similarly increases as commercial aircraft production recovers from post-pandemic disruptions, with production rates at Boeing and Airbus rising substantially. These industries require cutting inserts engineered for machining heat-resistant superalloys, titanium alloys, and composite materials, establishing specialized demand segments commanding premium pricing justifications.

Advanced Coating Technologies and Material Science Innovation Enabling Superior Performance and Extended Tool Life Optimization

Technological advancement in coating technologies represents a transformative market opportunity, with manufacturers increasingly deploying Physical Vapor Deposition (PVD) and Chemical Vapor Deposition (CVD) coating systems, enhancing cutting insert performance and durability. Coated inserts demonstrate approximately 25-30% extended tool life compared to uncoated alternatives, translating to significant cost reduction per manufactured component and justifying premium product positioning. Advanced coating innovations, including multi-layer nano-coatings and ceramic-titanium composite coatings, enable cutting speed increases by 15-20% while improving thermal stability and wear resistance, particularly in high-speed machining applications. Industry leaders, including SANDVIK, Kennametal Inc., and Kyocera Corporation, continuously invest in research and development supporting innovation in coating architectures.

Restraints - Volatile Raw Material Pricing and Supply Chain Disruptions Constraining Manufacturing Economics

Cutting tool inserts manufacturing fundamentally depends on critical raw materials including tungsten carbide, cobalt, and nickel-based superalloys, with commodity price volatility creating substantial margin compression challenges for manufacturers. Tungsten carbide prices fluctuate substantially based on geopolitical dynamics and mine production capacity, with primary tungsten reserves concentrated in China, accounting for approximately 70% of global supply, creating concentrated sourcing risk. Cobalt procurement similarly encounters volatility driven by Democratic Republic of Congo supply disruptions and geopolitical considerations, with cobalt prices increasing by 30-40% during supply constraint periods. Manufacturing cost escalations directly cascade through industry value chains, constraining profitability, particularly for lower-margin commodity insert products. Supply chain disruptions stemming from logistics challenges and port congestion periodically restrict raw material availability, limiting production capacity and extending customer delivery timelines, potentially undermining market share positions for manufacturers encountering prolonged material sourcing constraints.

Intense Competitive Pricing Pressure and Market Consolidation Reduce Profitability Opportunities

The cutting tool inserts market exhibits highly competitive dynamics with established global manufacturers competing aggressively on pricing alongside emerging regional suppliers from China and India offering cost-competitive alternatives. Original equipment manufacturers (OEMs) and industrial distributors continuously negotiate price concessions, leveraging purchasing power and product specification flexibility, constraining pricing leverage for suppliers. Market consolidation trends including strategic mergers and acquisitions among mid-market competitors, create competitive pressures forcing smaller players toward niche specialization or exit. Overcapacity in certain insert product categories including standard carbide turning inserts and face milling inserts create deflationary pricing environments particularly in price-sensitive markets across Southeast Asia and South Asia, limiting profitability expansion opportunities and constraining research and development investment capacity for differentiation innovation.

Opportunity - Commercial Fleet Electrification and High-Volume Automotive Component Manufacturing: Establishing Exceptional Growth Opportunities

Commercial vehicle electrification, including heavy-duty trucks, buses, and commercial delivery vehicles, creates substantial opportunities for increased demand for cutting tool inserts as fleet operators implement zero-emission mandates and regulatory electrification targets. Battery manufacturing for commercial vehicles requires precision machining of aluminum battery housings, copper busbars, and thermal management components, establishing specialized insert demand segments with growth rates exceeding 15% annually. Precision casting and die-casting operations supporting electric drivetrain components including electric motor housings and transmission cases necessitate advanced cutting solutions. Additionally, lightweight material machining including magnesium alloys and advanced composites utilized in vehicle structural components creates emerging opportunities for specialized insert geometries and material compositions.

Additive Manufacturing Integration and Digital Manufacturing Technologies Enabling Software-Driven Cutting Tool Solutions

Advanced manufacturing technologies, including additive manufacturing (3D printing) and digital twin simulation, establish transformative opportunities for cutting tool insert manufacturers pursuing technology-enabled business model evolution. Hybrid manufacturing systems that combine additive and subtractive processes require inserts engineered for machining 3D-printed metal components and for post-processing operations, thereby establishing distinct demand segments. Industry 4.0 adoption and smart manufacturing initiatives drive demand for cutting tool inserts integrated with sensor technologies, enabling real-time tool wear monitoring and predictive maintenance analytics. Software platforms analyze tool performance data and enable optimization algorithms, identifying optimal cutting parameters, and justify premium pricing supporting margin expansion.

Category-wise Analysis

Product Type Insights

Milling Inserts represent the dominant product category commanding approximately 47% market share expansion driven by widespread adoption across automotive, aerospace, and general manufacturing applications requiring diverse geometric configurations and material compositions. Milling insert demand accelerates with increasing complexity in component designs necessitating shoulder milling, face milling, and high-feed milling operations achieving exceptional material removal rates while maintaining surface finish specifications. Advanced milling inserts geometries incorporating reinforced cutting edges and vibration-dampening features enable operation in low-rigidity machining environments common in job-shop and contract manufacturing facilities. Turning inserts account for approximately 32% of the market, with substantial volume deployment supporting lathe-based operations and CNC turning centers across industries.

Material Insights

Carbide inserts establish clear market dominance, commanding approximately 64% market share, reflecting superior performance characteristics, including exceptional hardness, thermal resistance, and extended tool life compared to alternative materials. Cemented carbide comprising tungsten carbide particles suspended in cobalt binder matrix provides versatility across diverse machining applications from cast iron to stainless steel operations. Carbide insert adoption continues accelerating driven by cost-per-part reduction justification as extended tool life and increased cutting speeds offset premium material costs. Ceramic inserts capture approximately 18% market share, demonstrating accelerating growth particularly in high-speed machining applications including finish milling and precision finishing operations. Silicon-nitride and aluminum-oxide ceramic compositions enable cutting speeds 50% higher than carbide alternatives while maintaining thermal stability at extreme temperatures exceeding 1000 degrees Celsius.

Application Insights

Metal machining dominates application segments, commanding approximately 71% market volume, reflecting ubiquitous cutting tool insert utilization across diverse industries requiring material removal and dimensional precision. Metal machining applications span ferrous materials including cast iron and steel, non-ferrous materials including aluminum and copper alloys, and exotic materials including titanium and nickel-based superalloys requiring specialized insert compositions and coating systems. Woodworking applications capture approximately 12% market share, with cutting inserts engineered for hardwood and engineered wood product machining incorporating geometries and edge preparations optimizing chip control and dimensional precision in wood production environments. Composite material machining represents approximately 11% market share and demonstrates exceptional growth momentum driven by aerospace industry adoption of carbon-fiber-reinforced polymers (CFRP) and glass-fiber-reinforced polymers (GFRP) in aircraft structures and wind energy applications.

End-user Insights

The automotive industry dominates end-user segments, commanding approximately 38% of cutting tool insert consumption, driven by exceptional production volume, manufacturing complexity, and quality requirements governing engine components, transmission systems, and structural elements. Automotive machining operations, including engine block machining, cylinder head finishing, crankshaft machining, and transmission component manufacturing, require sustained procurement of cutting tool inserts across diverse insert geometries and material compositions. Aerospace industry captures approximately 28% market share despite lower production volumes relative to automotive, reflecting premium pricing justification based on exceptional material requirements and quality mandates. Aerospace machining encompasses fuselage panel machining, wing component manufacturing, landing gear fabrication, and engine component production requiring inserts engineered for heat-resistant superalloys, titanium alloys, and composite materials.

Regional Insights

Asia Pacific Cutting Tool Inserts Market Share and Trends

Asia Pacific commands dominant global position accounting for approximately 40% of worldwide cutting tool inserts demand, driven by extraordinary manufacturing expansion, rising CNC machining adoption, and systematic government infrastructure investments supporting industrial capacity development. China maintains clear regional leadership as world's largest manufacturing economy with exceptional cutting tool insert consumption spanning automotive, aerospace, machinery, and electronics manufacturing sectors. Chinese automotive production exceeding 29 million units annually creates significant demand for cutting tool equipment, as manufacturers increasingly adopt advanced coatings and specialized geometries. India's manufacturing sector demonstrates accelerating expansion with automotive production reaching approximately 4.5 million vehicles annually, complemented by emerging aerospace and precision engineering capabilities supporting cutting tool insert demand growth at rates 6% annually.

North America Cutting Tool Inserts Market Share and Trends

North America represents approximately 28% of global market share, characterized by advanced manufacturing infrastructure, aerospace specialization, and an established automotive industrial base supporting sustained cutting tool insert demand. The United States aerospace sector dominance, driven by Boeing, Lockheed Martin, and Northrop Grumman defense and commercial aircraft programs, establishes exceptional demand for advanced carbide and ceramic inserts engineered for titanium and nickel alloy machining. Automotive manufacturing encompassing traditional internal combustion engine production and accelerating electric vehicle component manufacturing supports continued cutting tool equipment adoption. Mexican manufacturing expansion supporting North American automotive supply chains following nearshoring initiatives drives regional cutting tool insert demand growth, with manufacturers establishing production capabilities supporting major Detroit-based and Mexican-based automotive OEMs.

Europe Cutting Tool Inserts Market Share and Trends

Europe maintains approximately 25% global market share underpinned by precision engineering tradition, advanced manufacturing specialization, and strong aerospace and automotive industrial bases. Germany establishes regional manufacturing leadership position with exceptional precision machining capabilities supporting automotive powertrains, aerospace components, and machinery manufacturing. German manufacturers including EMUGE-FRANKEN, Gühring GmbH & Co. KG, and Ingersoll Cutting Tools maintain significant regional and global market positions through technology differentiation and specialized product development. Northern European countries including Sweden and Switzerland maintain stronghold positions in precision tool manufacturing and advanced coating technology development, supporting cutting-edge innovation in PVD and CVD coating systems. Eastern European manufacturing expansion, including Poland, the Czech Republic, and Slovakia, driven by lower labor costs and FDI inflows, establishes emerging demand growth opportunities.

Competitive Landscape

The cutting tool inserts market exhibits significant consolidation among global manufacturers including SANDVIK (Sweden), Kennametal Inc. (United States), Mitsubishi Materials Corporation (Japan), Kyocera Corporation (Japan), and ISCAR (Israel) collectively commanding dominant market positions through comprehensive product portfolios, established customer relationships, and continuous innovation emphasis. SANDVIK Coromant maintains clear market leadership position through exceptional turning insert, milling insert, and drilling insert product ranges, complemented by advanced coating technologies and digital manufacturing solutions supporting customer productivity enhancement.

Recent Strategic Developments and Market Trends

- In October 2024: SANDVIK Acquisition of Buffalo Tungsten Inc. SANDVIK announced strategic acquisition of Buffalo Tungsten Inc., a tungsten concentrate and powdered tungsten producer located in Montana, United States, strengthening upstream raw material supply security and establishing vertical integration supporting sustained competitive positioning in cemented carbide production.

- In September 2024, Kennametal Inc. Introduces KCP25C Steel Turning Grade with KENGold Coating Technology Kennametal Inc. launched KCP25C high-performance steel turning grade featuring proprietary KENGold coating technology enhancing wear identification visibility and enabling maximum cutting-edge utilization supporting customer productivity gains and tool life optimization.

Companies Covered in Cutting Tool Inserts Market

- EMUGE-FRANKEN

- Gühring GmbH & Co. KG

- Ingersoll Cutting Tools

- ISCAR

- Kennametal Inc.

- Kyocera Corporation

- Mitsubishi Materials Corporation

- Nachi-Fujikoshi Corp.

- SANDVIK

- Sandvik Coromant

- Seco Tools

- Other Market Players

Frequently Asked Questions

The global cutting tool inserts market was valued at US$ 6.5 billion in 2026 and is projected to reach US$ 8.7 billion by 2033, representing a 4.4% CAGR expansion through the forecast period.

Primary growth in drivers include accelerating precision machining demand from automotive and aerospace sectors, with global automotive production exceeding 81 million vehicles annually and commercial aircraft production recovering to pre-pandemic volumes. Advanced coating technology adoption including PVD and CVD coating systems extending tool life by 25-30% and enabling cutting speed increases by 15% justifies premium pricing and supports customer productivity enhancement.

Milling inserts dominate with approximately 47% market share expansion driven by widespread adoption across automotive, aerospace, and general manufacturing applications requiring diverse geometric configurations. Milling insert demand accelerates with complex component designs necessitating shoulder milling, face milling, and high-feed milling operations achieving exceptional material removal rates.

Asia Pacific maintains dominant position with approximately 40% global market share driven by China's manufacturing leadership with 29 million annual vehicle production and India's expanding automotive sector reaching 4.5 million vehicles annually.

Market leaders include SANDVIK Coromant, Kennametal Inc., CBN, and Mitsubishi Materials Corporation emphasizing ceramic insert innovation and superalloy machining solutions.