- Metalworking & Fabrication

- Coil-fed Punching and Cutting Machine Market

Coil-fed Punching and Cutting Machine Market Trends, Size, Share, and Growth Forecast, 2026 - 2033

Coil-fed Punching and Cutting Machine Market by Product type (Coil-fed Punching Machines, Coil-fed Cutting Machines and Combined Machines), Drive Type (Hydraulic and Servo Electric), Vehicle Type (Automotive, Railways, Aerospace & Defense, Electronics, Consumer Goods, HVAC and Others (Building Industry, Metal Ceilings, & Agricultural)), and Regional Analysis for 2026 - 2033

Coil-fed Punching and Cutting Machine Market Size and Trends Analysis

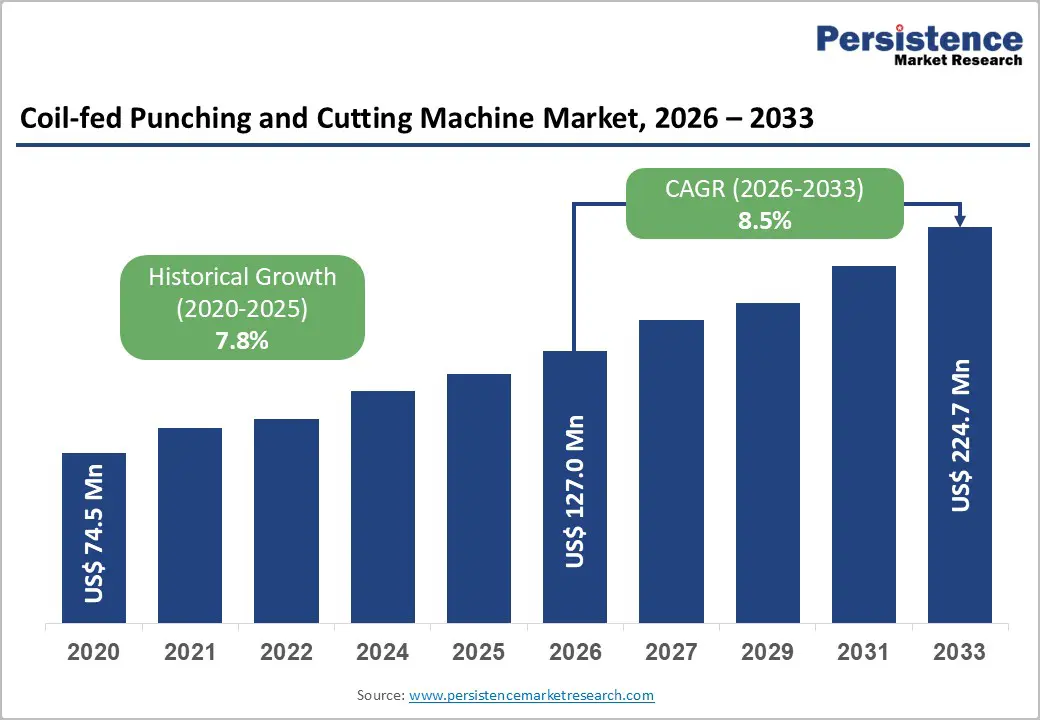

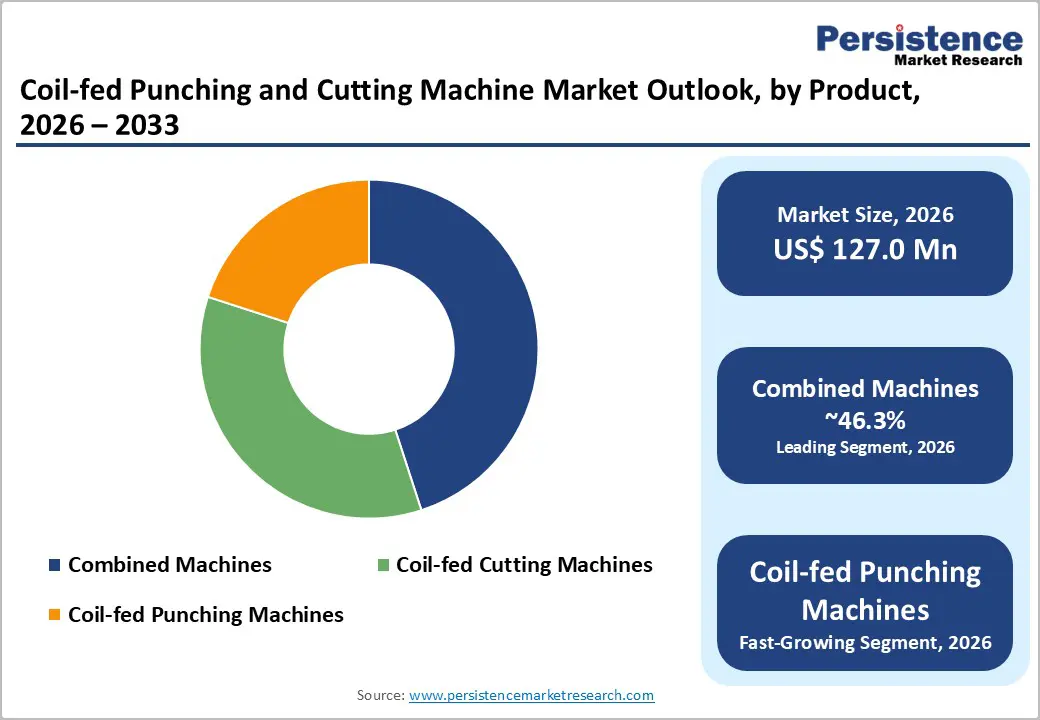

The global coil-fed punching and cutting machines market was valued at US$ 127.0 million in 2026 and is projected to reach US$ 224.7 million by 2033, growing at a CAGR of 8.5% between 2026 and 2033.

Growth is underpinned by increased adoption of automation in automotive and aerospace manufacturing, rising demand for precision metal components from advanced materials, and the integration of servo-electric and Industry 4.0 technologies.

Key Industry Highlights:

- Drive type segmentation: Hydraulic systems dominate at 65% share, while servo-electric is the fastest-growing segment at a 13% CAGR, driven by energy-efficiency, precision, and sustainability demands that outpace baseline market growth.

- Product mix: Combined punching-cutting machines lead at 46.3% share, while coil-fed cutting machines are the fastest-growing product at 9% CAGR, driven by advanced laser/plasma/precision shearing technologies.

- Application dynamics: Aerospace & Defense represents the largest segment at 25% share, while Railways are the fastest-growing application at 10% CAGR, supported by global high-speed rail expansion and transit modernization.

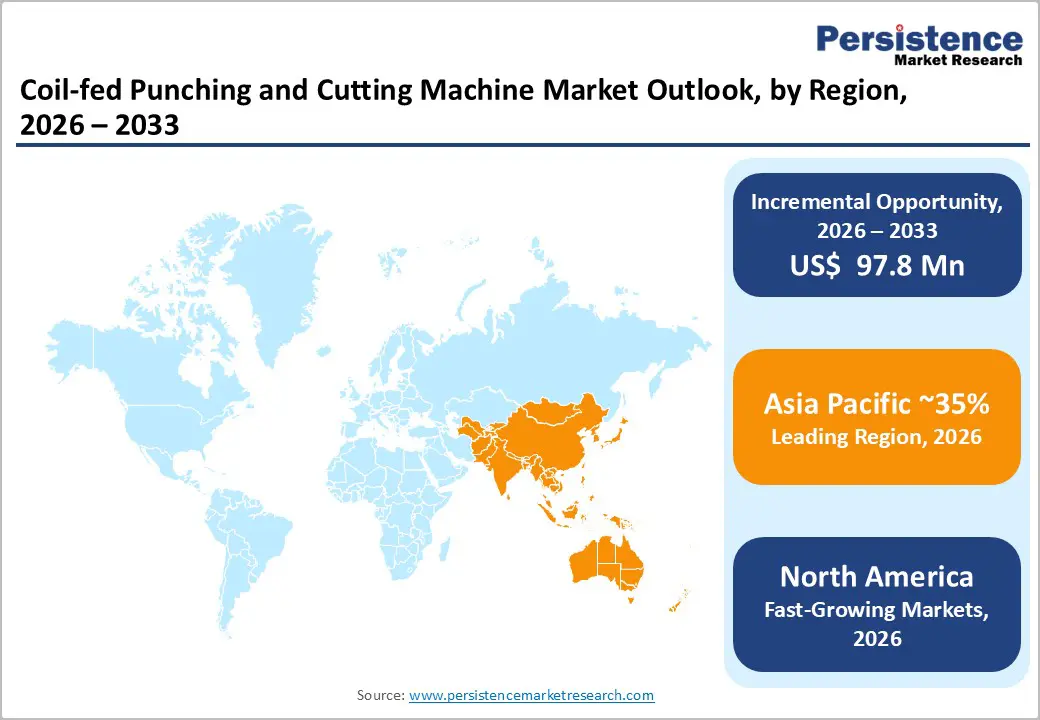

- Regional performance: Asia Pacific is the largest and fastest-growing region with 8.5% CAGR, North America exhibits mature market characteristics (5.6% CAGR); Europe maintains moderate growth.

- Consolidation and strategic moves: Manufacturing consolidation (Ward Manufacturing-LINE Group, PrecisionX-National Manufacturing) and technology launches (TRUMPF, Amada servo-electric platforms) reflect industry consolidation and premium technology differentiation strategies

| Key Insights | Details |

|---|---|

| Coil-fed Punching and Cutting Machine Market Size (2026E) | US$ 127.0 Mn |

| Market Value Forecast (2033F) | US$ 224.7Mn |

| Projected Growth (CAGR 2026 to 2033) | 8.5% |

| Historical Market Growth (CAGR 2020 to 2024) | 7.8% |

Market Dynamics

Drivers - Automation and Industry 4.0 Integration in Manufacturing

Modern manufacturing environments increasingly demand real-time monitoring, predictive maintenance, and remote operations capabilities embedded in advanced coil-fed machine systems. Integration of IoT sensors, AI-driven diagnostics, and CAD/CAM dental systems enables manufacturers to achieve precision improvements of 20%, reduce cycle times by 25%, and minimize unscheduled downtime by 46%. Companies like Prima Power report machines with up to 300 kN force capacity, 1,000 hits-per-minute (hpm) speed, and 75% energy savings compared to prior-generation hydraulic systems.

The automotive sector alone is expected to grow at 6.1% in Germany (2024) and 11.6% year-on-year in China, creating substantial demand for precision stamping and forming equipment integrated with digital control systems. As regulatory requirements for quality traceability and supply chain transparency intensify, manufacturers prioritize systems offering documented precision, real-time data logging, and full operational visibility.

Rising Demand for Lightweight and Advanced Materials

Automotive electrification, aerospace expansion, and medical device manufacturing all drive demand for lightweight composites, aluminum alloys, titanium, and advanced high-strength steels (AHSS). These materials require specialized punching and cutting capabilities to achieve precision without material degradation or excessive tool wear. The global aerospace market is projected to record a 7% CAGR between 2024 and 2025, with coil-fed equipment central to fuselage component fabrication, fastener hole punching, and structural frame assembly.

Similarly, the electric vehicle supply chain drives incremental demand for battery enclosure components, high-voltage connector housings, and thermal management system parts requiring tight tolerances and complex geometries achievable only through advanced coil-fed systems. Market analyses indicate that adoption of lightweight materials increases per-unit machine content by 20%, as manufacturers invest in enhanced tooling, precision fixtures, and advanced actuation systems.

Restraints - High Capital Investment and Extended ROI Timelines

Coil-fed punching and cutting systems are significant capital expenditures, with entry-level machines starting at US$100,000-200,000 and advanced systems exceeding US$500,000-1.5 million, including installation, tooling, and training. For small- and medium-sized enterprises (SMEs) with limited capex budgets, this investment barrier defers purchases and extends procurement cycles. Additionally, manufacturers must invest in precision tooling, sensor calibration, and operator certification, adding 20-35% to the total cost of ownership beyond equipment purchase price. In price-sensitive markets (India, Southeast Asia, parts of Latin America), funding constraints force manufacturers to retain legacy hydraulic systems longer, slowing market penetration even in regions experiencing rapid industrial growth.

Volatile Raw Material Costs and Supply Chain Constraints

Coil-fed machine manufacturers depend on precision-machined components, hydraulic/servo-electric actuators, control electronics, and specialty alloys sourced from global suppliers, all of which are subject to commodity price volatility and geopolitical disruption. Elevated steel and aluminum prices in 2024 - 2025 increased machine manufacturing costs by 8-12%, with suppliers passing costs to end customers or absorbing margin compression. Additionally, semiconductor supply constraints for control systems and sensor components create extended lead times (18-24 months for fully integrated smart machines), limiting manufacturers' ability to respond to demand surges. These supply-side pressures constrain growth, particularly for smaller machine builders lacking supply chain redundancy or hedging strategies.

Opportunity - Aerospace and Defense Sector Expansion

Aerospace and defense represent the largest end-use application segment, accounting for 25% of market share, driven by the recovery in aircraft production, military modernization, and the expansion of defense contracting. Boeing, Airbus, and regional aircraft manufacturers are increasing production rates and upgrading precision fabrication infrastructure. The global aerospace market projected at 7% CAGR (2024 - 2025) creates a US$ 35-50 million addressable opportunity for advanced coil-fed systems tailored to titanium and composite component fabrication.

Additionally, defense contractors expanding next-generation platform capabilities (5th-gen fighters, missile systems, autonomous platforms) require specialized punching and cutting equipment meeting stringent precision, repeatability, and traceability standards. Suppliers offering aerospace-qualified machines, AS9100-compliant documentation, and integration with defense supply chain systems can command premium positioning and recurring revenue from platform production and sustainment contracts.

Smart Manufacturing and Remote Monitoring Services

Emerging business models emphasize equipment-as-a-service (EaaS), predictive maintenance contracts, and performance-based pricing rather than simple equipment sales. Manufacturers can differentiate by embedding IoT sensors, cloud-based monitoring platforms, and AI-driven predictive maintenance algorithms into machine systems, generating recurring software and service revenue. This model offers customers reduced capex burden, outcome-based pricing aligned with production output, and access to real-time analytics and optimization recommendations.

The global market opportunity for smart manufacturing services tied to coil-fed equipment is estimated at US$ 15 million by 2033, growing at 20% CAGR-substantially above equipment sales growth and offering margin-accretive revenue streams for technology-forward suppliers.

Category-wise Analysis

Drive Type Insights

Hydraulic drive systems dominate the market with roughly 65% share, driven by their strong force output, long-proven reliability, and cost-effectiveness for standard manufacturing needs. These machines are preferred for high-force operations above 200 kN, high-volume production runs, and applications where moderate precision of ±0.1-0.2 mm is sufficient. Hydraulic systems also remain widespread in emerging markets such as China, India, and Southeast Asia, were lower capital costs and compatibility with existing factory infrastructure support continued adoption.

Servo-electric systems are the fastest-growing segment, projected to grow at a 12% CAGR. They offer higher energy efficiency, superior accuracy of ±0.01-0.05 mm, reduced maintenance, and quieter operation. As energy prices rise and sustainability goals intensify, manufacturers in advanced markets increasingly favor servo-electric technology despite its higher upfront cost.

Product Type Insights

Combined punching and cutting machines lead the coil-fed equipment market with a 46.3% share, driven by their ability to integrate multiple operations in a single pass, reduce scrap by 15-25%, and cut changeover time by 30-45%. These systems are ideal for high-mix, small-batch production and currently represent a market value of US$ 53 million in 2026, or about 42% of the total coil-fed market.

Meanwhile, coil-fed cutting machines are the fastest-growing category, supported by advancements in laser, plasma, waterjet, and precision shearing technologies. Offering ±0.5 mm tolerance and improved edge quality, they meet rising demands in electronics, aerospace, and appliance manufacturing. This segment, valued at US$ 35-42 million in 2026, is projected to reach US$ 70 million by 2033 at a 9% CAGR.

Application Insights

Aerospace and defense is the largest end-use segment, accounting for 25% of the market due to rising aircraft production, military modernization, and expanding defense manufacturing. These sectors require extremely high precision (±0.05 mm), AS9100-compliant traceability, and specialized handling of materials such as titanium and composites. The segment is valued at about US$ 32 million in 2026, making it the strongest application area.

Railways represent the fastest-growing segment, with a projected 10% CAGR driven by high-speed rail projects, urban transit expansion, and fleet upgrades across Europe, Asia, and parts of North America. Railway manufacturing demands high-volume precision production of structural components such as bogies, couplers, and enclosures. Valued at US$20 million in 2026, the railway segment is expected to reach US$38 million by 2033.

Regional Market Insights

North America Coil-fed Punching and Cutting Machine Market Trends

North America represents an estimated US$ 47 million market (2026) with projected growth to US$ 70 million by 2033, reflecting 4.6% CAGR slower than global baseline, reflecting market maturity but steady underlying demand from automotive, aerospace, and electronics manufacturing. The U.S. market specifically is valued at approximately US$ 23.9 million (2024), with modest growth expectations.

The regulatory environment emphasizes workplace safety (OSHA standards), environmental compliance (EPA emissions and waste disposal rules), and manufacturing quality (ISO 9001, AS9100 for aerospace). These standards create baseline demand for precision equipment with documented traceability and safety certifications, supporting steady replacement and upgrading cycles among established manufacturers. The competitive landscape features global suppliers (TRUMPF, Amada, Prima Power) alongside regional specialists and system integrators focusing on niche applications and customization.

Europe Coil-fed Punching and Cutting Machine Market Trends

Europe represents an estimated US$ 38 million market (2026) with growth to US$ 65 million by 2033, reflecting moderate 4.5% CAGR and mature market characteristics. Germany leads European markets with largest absolute demand, driven by dominant automotive and machinery manufacturing presence, while the U.K., France, and Spain contribute meaningfully to overall European consumption. Technology leadership in Europe emphasizes energy efficiency, precision, and sustainability. German machinery builders (TRUMPF, Amada Germany operations) and European specialists dominate the innovation landscape.

Investment trends reflect consolidation among SME machinery builders and the acquisition of specialty tooling/technology companies by larger industrial groups. The European market's mature character, strong regulatory framework, and technological sophistication create opportunities for premium-positioned equipment, specialized applications (medical, railway, aerospace), and value-added services rather than commodity coil-fed systems.

Asia Pacific Coil-fed Punching and Cutting Machine Market Trends

Asia Pacific represents the largest and fastest-growing regional market, estimated at US$ 60 million (2026) with projected growth to US$ 130 million by 2033, reflecting 6.5% CAGR. China dominates regional demand with approximately US$ 11.7 million market (2024) and projected 8.7% CAGR to 2034, translating to approximately US$ 27 million market value by 2034. China's position as a global manufacturing hub across automotive, electronics, consumer goods, and railways drives massive coil-fed machine adoption and increasingly positions China as a significant exporter competing globally on price and volume.

Japan maintains an approximately US$15 million market, characterized by high technical standards, premium servo-electric adoption, and specialization in precision automotive and electronics applications. India and ASEAN represent high-growth emerging opportunities with a 12% CAGR, driven by rapid industrialization, automotive manufacturing expansion, and growth in electronics assembly.

Competitive Landscape

The coil-fed punching and cutting machines market is moderately concentrated, with global suppliers (TRUMPF, Amada, Prima Power, Murata Manufacturing) commanding significant market share alongside regional specialists and emerging Chinese manufacturers.

Top five players are estimated to hold approximately 45% of global revenues, indicating meaningful fragmentation permitting competitive participation from specialized and regional players. Competition centers on technology differentiation (servo-electric vs hydraulic, precision capabilities, speed), geographic presence, aftermarket support, and application specialization.

Key Industry Developments:

- In January 2023, Dallan S.p.A. launches a new generation of high-speed coil fed punching machines with integrated laser cutting capabilities.

- In June 2023, A major automotive manufacturer in China announces a significant investment in automated coil fed punching lines to increase production capacity

Companies Covered in Coil-fed Punching and Cutting Machine Market

- TRUMPF GmbH & Co. KG

- Amada Co., Ltd.

- Prima Power

- LVD Company NV

- Salvagnini S.p.A.

- Murata Machinery, Ltd.

- Dallan S.p.A.

- DANOBAT GROUP

- HACO Group

- Produtech s.r.l.

- Pivatic Oy

- Others Key Players

Frequently Asked Questions

The Coil-fed Punching and Cutting Machine market is estimated to be valued at US$ 127.0 Mn in 2026.

The primary demand driver for the Coil-Fed Punching and Cutting Machine market is the growing need for high-productivity, continuous metal-processing solutions across automotive, HVAC, construction, and appliance manufacturing.

In 2026, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Coil-fed Punching and Cutting Machine market.

Among the Product Type, Combined Machines holds the highest preference, capturing beyond 46.3% of the market revenue share in 2026, surpassing other Product Type.

The key players in Coil-fed Punching and Cutting Machine are TRUMPF GmbH & Co. KG, Amada Co., Ltd., Prima Power, LVD Company NV, and Salvagnini S.p.A..