- Metalworking & Fabrication

- High Speed Steel (HSS) Metal Cutting Tools Market

High Speed Steel (HSS) Metal Cutting Tools Market Size, Share, and Growth Forecast, 2025 - 2032

High Speed Steel (HSS) Metal Cutting Tools Market by Product Type (Drills, End Mills, Taps, Reamers, Broaches, and Others), Applications (Milling, Turning, Drilling, Tapping, and Others), End-use (Automotive, Aerospace, Medical, Industrial Manufacturing, Construction, and Others), and Regional Analysis for 2025 - 2032

High Speed Steel (HSS) Metal Cutting Tools Market Size and Trends Analysis

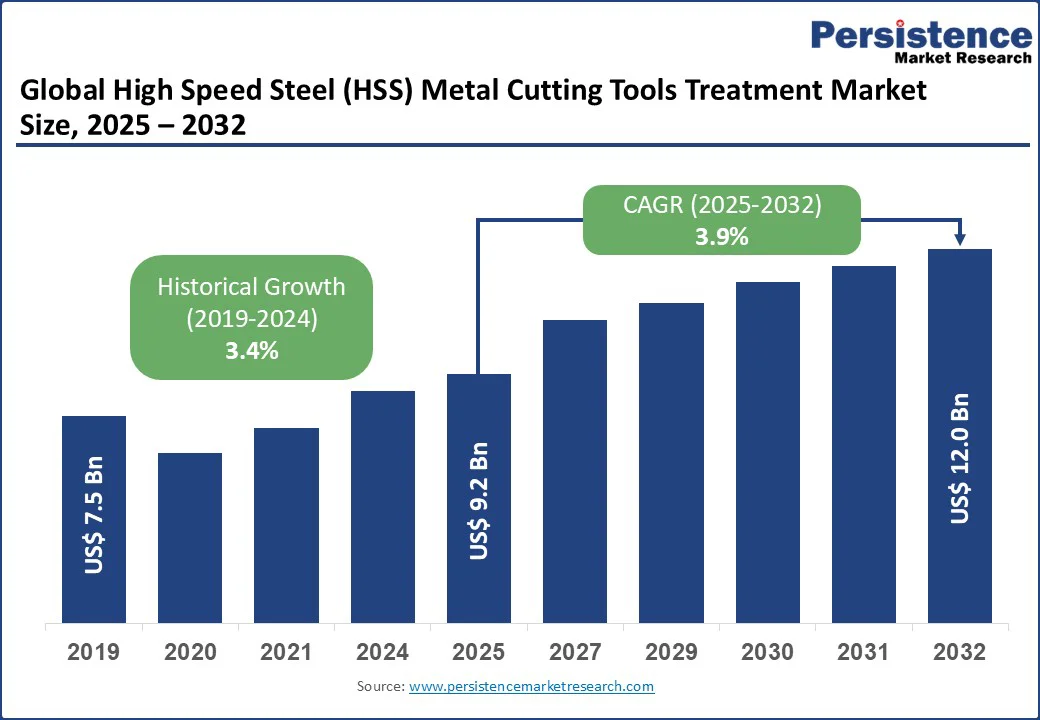

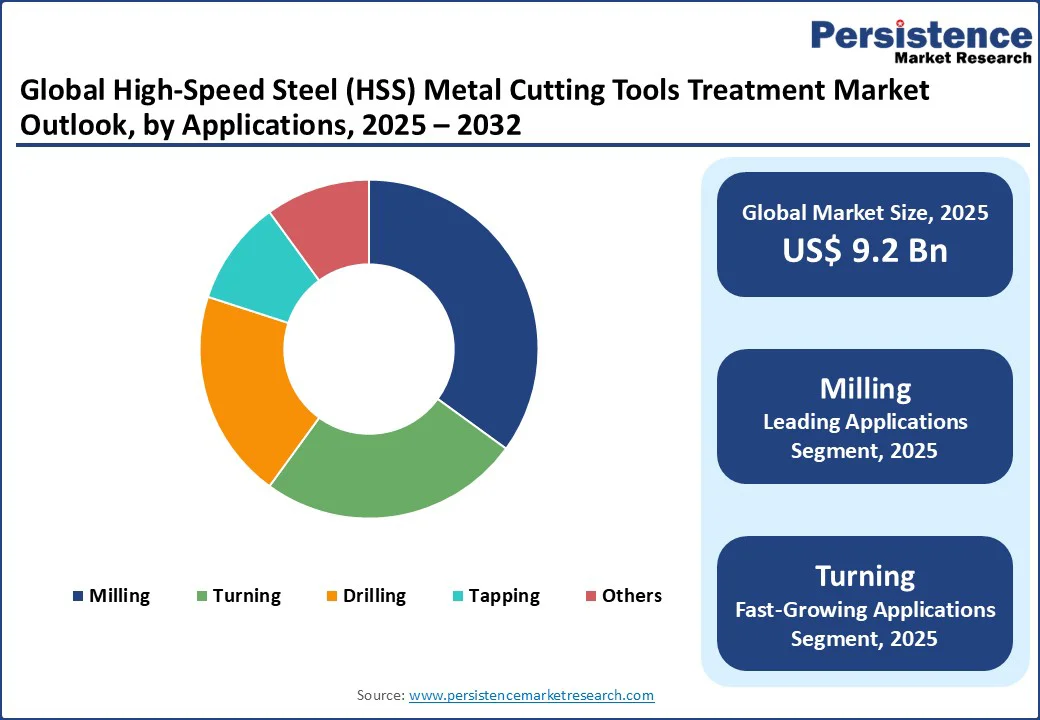

The global high speed steel (HSS) metal cutting tools market size is likely to be valued at US$ 9.2 Bn in 2025 and expected to reach US$ 12.0 Bn by 2032, growing a CAGR of 3.9% during the forecast period 2025 to 2032 and is driven by the increasing demand for precision machining in automotive, aerospace, and industrial manufacturing sectors, where HSS tools offer a balance of cost-effectiveness, durability, and performance.

Key Industry Highlights:

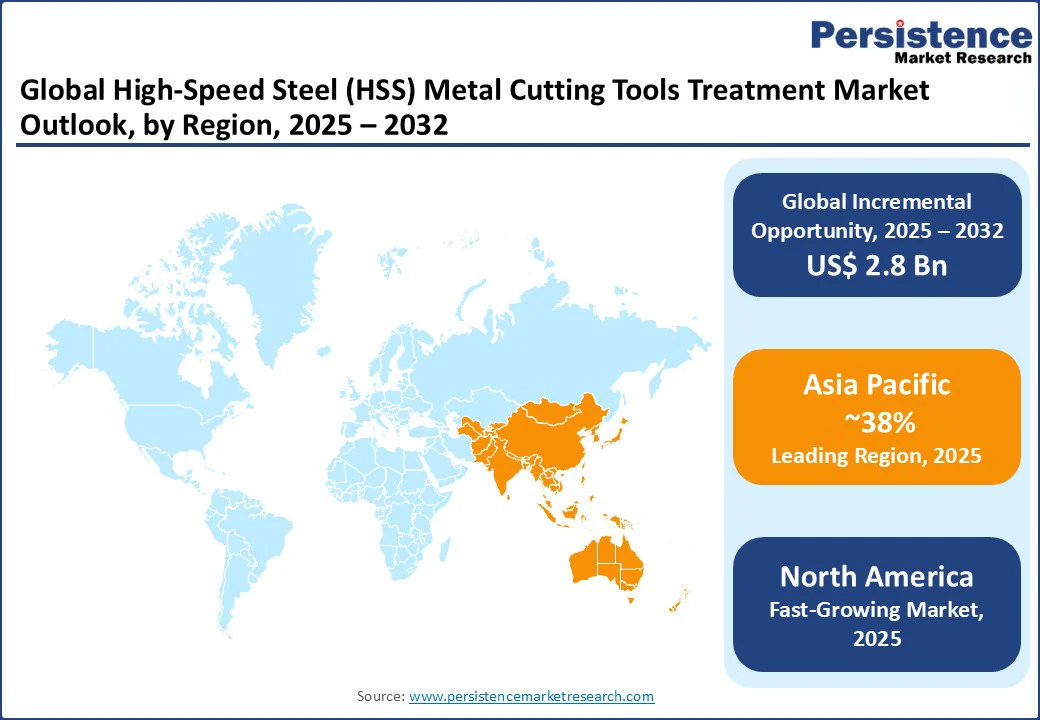

- Leading Region: Asia Pacific is expected to account for a 38% share in 2025, driven by automotive and manufacturing growth in China and India.

- Fastest-growing Region: North America is the fastest-growing region, driven by advancements in the aerospace and medical sectors.

- Dominant Product Type: Drills, commanding 35% market share, due to their versatility in drilling applications.

- Leading Application: Milling is the leading application, accounting for 40% of market revenue, driven by precision machining needs.

- Fastest-growing End-use: Aerospace is the fastest-growing end-use, due to demand for lightweight components.

- Market Opportunity: Advanced coatings and sustainable HSS formulations for eco-friendly manufacturing.

| Key Insights | Details |

|---|---|

|

High Speed Steel (HSS) Metal Cutting Tools Market Size (2025E) |

US$9.2 Bn |

|

Market Value Forecast (2032F) |

US$12.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.4% |

Market Dynamics

Drivers - Growth in Automotive and Aerospace Industries

The automotive and aerospace sectors are primary drivers of the High-Speed Steel (HSS) Metal Cutting Tools market, as these industries require high-precision tools for machining complex components. The global automotive production reached 92 million vehicles in 2025, with a 5% increase from the previous year, driving demand for HSS drills and end mills in engine and transmission manufacturing. In aerospace, the production of aircraft components, such as turbine blades and landing gear, relies on HSS tools for their ability to cut high-strength alloys such as titanium and Inconel at high speeds without losing edge sharpness.

HSS tools, with their superior heat resistance and wear properties, enable efficient production of lightweight parts for electric vehicles (EVs) and fuel-efficient aircraft, reducing manufacturing costs by up to 20% compared to carbide alternatives in certain applications. The shift toward EVs, with global sales reaching 14 Mn units in 2025, further boosts demand for HSS taps and reamers in battery housing and chassis fabrication, making these industries key growth engines for the market.

Restraints - Competition from Advanced Materials

The High-Speed Steel (HSS) Metal Cutting Tools market faces intense competition from carbide, ceramic, and diamond tools, which offer superior wear resistance and cutting speeds. Carbide tools, holding 40% of the global cutting tools market in 2025, can operate at 2-3 times the speed of HSS, reducing machining time in high-volume production. In aerospace and medical end-uses, where precision and heat resistance are critical, carbide dominates, limiting HSS penetration to 25% of the market. The higher initial cost of HSS tools, coupled with shorter tool life (30-50 hours vs. 200 hours for carbide), deters adoption in automated CNC environments, where tool change frequency increases downtime costs by 15-20%.

Opportunities - Development of Coated and Hybrid HSS Tools

Innovations in coatings such as TiAlN and DLC (diamond-like carbon) extend HSS tool life by 50-100%, creating opportunities in high-precision applications. Hybrid HSS-carbide tools combine HSS affordability with carbide durability, appealing to SMEs in automotive and construction. The global demand for coated tools with HSS variants is capturing a 30% share in milling and drilling. In the medical sector, coated HSS tools, especially reamers, are gaining traction due to their biocompatibility and precision machining capabilities. These tools are vital in orthopedic and dental implant manufacturing, where accuracy, smooth finishes, and safety are paramount. The adoption of coated HSS reamers is driven by rising implant demand and the expansion of advanced surgical procedures worldwide.

Category-wise Analysis

Product Type Insights

Drills dominate the High-Speed Steel (HSS) Metal Cutting Tools market, expected to account for approximately 35% share in 2025. Drills are essential for creating precise holes in metal components, making them indispensable in automotive and aerospace end-uses. HSS drills, with their high hardness and heat resistance, perform well in high-speed operations, with twist drills being the most popular variant. Leading manufacturers such as Kennametal and Sandvik Coromant leverage HSS drills for their cost-effectiveness and versatility in materials such as steel and aluminum.

End mills are the fastest-growing product type, driven by the rise of CNC machining and complex part fabrication. End mills, used for milling applications, benefit from HSS's toughness in slotting and profiling. Innovations in variable helix designs improve chip evacuation, enhancing performance in industrial manufacturing.

Applications Insights

Milling leads the applications segment, accounting for a 40% share in 2025. Milling operations, involving the removal of material using rotary cutters, are critical in aerospace for shaping turbine blades and in automotive for engine blocks. HSS end mills and face mills excel in milling due to their ability to maintain edge sharpness at moderate speeds, making them suitable for high-volume production.

Turning is the fastest-growing application, driven by the demand for lathe tools in the construction and medical sectors. Turning applications use HSS inserts for external and internal machining, with advancements in coatings extending tool life by 30%.

End-use Insights

Automotive dominates the end-use segment, accounting for 30% of market revenue in 2025. The automotive industry relies on HSS tools for machining chassis, gears, and EV components, with global vehicle production reaching 92 million units in 2025.

Aerospace is the fastest-growing end-use, driven by the need for precision tools in aircraft manufacturing. HSS reamers and taps ensure tight tolerances for landing gear and airframes, supported by rising air travel demand.

Regional Insights

North America High Speed Steel (HSS) Metal Cutting Tools Market Trends

North America is likely to hold a 25% share in 2025, driven by its advanced manufacturing ecosystem and strong aerospace and medical sectors. The U.S. leads, with the automotive industry using HSS drills and taps for EV production, supported by US$ 52 Bn in infrastructure funding under the Bipartisan Infrastructure Law. The aerospace sector, contributing US$ 500 Bn to the economy, relies on HSS end mills for precision machining of airframe components, with Boeing’s 737 MAX production driving demand.

Canada’s manufacturing sector, particularly in Ontario, uses HSS tools for automotive and machinery applications, with 20% of tools featuring advanced coatings. The medical industry demands HSS reamers for surgical implants, aligning with the region’s focus on precision and biocompatibility. Market Trends in North America emphasize sustainable manufacturing, with 30% of manufacturers adopting eco-friendly HSS tools to meet ESG goals.

Europe High Speed Steel (HSS) Metal Cutting Tools Market Trends

Europe is likely to holds a 30% share in 2025, led by Germany, France, and the U.K. Germany’s automotive industry, producing 4 Mn vehicles annually, drives HSS tool demand for engine and transmission machining, with €100 Bn in green manufacturing investments under the EU’s Green Deal. HSS drills and taps, used by companies such as Volkswagen and BMW, ensure precision in high-volume production, with coated tools reducing machining costs by 15%.

France’s aerospace sector, with €80 Bn in revenue, relies on HSS end mills for machining airframe components, supported by Airbus’s production goals of 900 aircraft annually by 2030. The industrial manufacturing sector uses HSS broaches for gear production, with 30% of machinery incorporating HSS tools. Market Trends in Europe emphasize eco-friendly coatings, with 50% of tools featuring CrN or DLC to meet sustainability mandates.

Asia Pacific High Speed Steel (HSS) Metal Cutting Tools Market Trends

Asia Pacific is poised to dominate with a 38% share in 2025, valued at US$ 3.5 Bn, driven by rapid industrialization in China, India, and Japan. China’s manufacturing sector, contributing 30% to global output, uses HSS taps and drills for machinery and automotive production, supported by US$ 50 Bn in Made in China 2025 funding. The automotive industry, producing 27 Mn vehicles in 2025, drives demand for HSS tools in engine and EV component machining.

India’s manufacturing growth, at 7% annually, fuels HSS adoption in construction and industrial manufacturing, with US$ 50 Bn in PLI scheme investments boosting machinery production. Japan’s aerospace and medical sectors use HSS reamers for precision machining, with ¥1 Tn in R&D funding supporting tool innovation. High Speed Steel (HSS) Metal Cutting Tools Market driven by SME adoption and infrastructure projects. The region’s focus on affordable, coated HSS tools aligns with cost-sensitive markets, with 60% of SMEs using HSS for drilling and milling.

Competitive Landscape

The global high-speed steel (HSS) cutting tools market is highly competitive, by a mix of global leaders, specialized toolmakers, and regional players. Major companies such as Sandvik Coromant, Kennametal, and Seco Tools maintain strong positions through continuous innovation in coatings, digital integration, and precision machining solutions. Others, such as Dormer Pramet, Emuge, and GWS Tool Group, focus on niche markets and customized offerings, while integrated manufacturers, such as Sumitomo Electric Industries, TimkenSteel, and Erasteel, leverage their material science expertise to develop advanced steel grades and durable tooling solutions.

Competition is driven by advancements in coatings and hybrid material technologies that enhance tool performance, as well as by the growing importance of digital lifecycle services such as tool tracking and predictive maintenance. Many players are also expanding production capabilities in Asia to cater to rising demand and reduce supply chain constraints.

Key Developments

- In 2023, Dormer Pramet has announced the expansion of its Synchro Tap line, delivering even greater productivity for manufacturers. The latest update introduces internal coolant options across all tap types, including spiral flute, spiral point, straight flute, and form taps, enabling improved chip evacuation, reduced heat generation, and longer tool life.

- In 2025, Tiangong International Company Limited announced the acquisition of Quintus Technologies, to expand production capacity through expanding its production facility in the Jiangsu province.

Companies Covered in High Speed Steel (HSS) Metal Cutting Tools Market

- Dormer Pramet

- Emuge

- Erasteel

- GWS Tool Group

- Hannibal Carbide Tool

- Kennametal

- Niagara Cutter

- RTS Cutting Tools

- Sandvik Coromant

- Seco Tools

- Sumitomo Electric Industries

- TimkenSteel

- Toolmex Industrial Solutions

Frequently Asked Questions

The global High-Speed Steel (HSS) Metal Cutting Tools Market Size is projected to reach US$ 9.2 billion in 2025.

Growth in the automotive and aerospace industries, advancements in manufacturing technologies, and demand for cost-effective tools drive the market.

The HSS metal cutting tools market is expected to grow at a CAGR of 3.9% from 2025 to 2032.

Development of coated and hybrid HSS tools and expansion in emerging markets offer significant opportunities.

Key players include Dormer Pramet, Emuge, Erasteel, Kennametal, Sandvik Coromant, and Seco Tools.