- Metalworking & Fabrication

- Laser Cutting Machine Market

Laser Cutting Machine Market Size, Share, and Growth Forecast, 2025 - 2032

Laser Cutting Machine Market by Technology (Solid State Lasers, Gas Lasers, Semiconductor Lasers, Others), Process Type (Fusion Cutting, Flame Cutting, Sublimation Cutting, Others), Application (Automotive, Consumer Electronics, Defense & Aerospace, Industrial, Others), and Regional Analysis for 2025 - 2032

Laser Cutting Machine Market and Trend Analysis

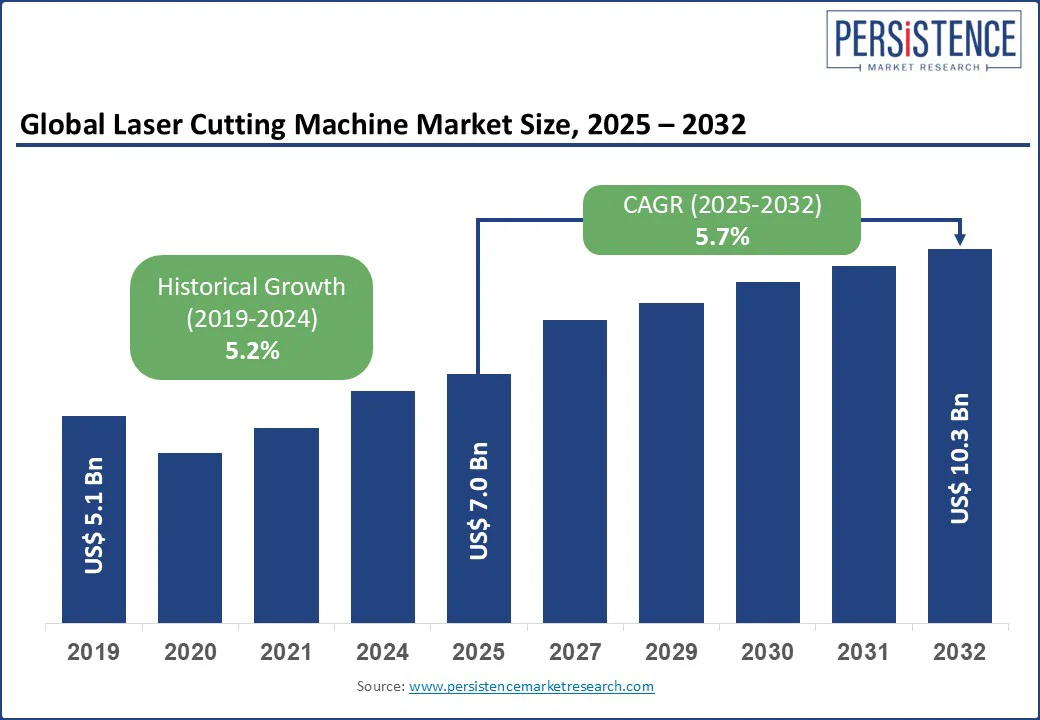

The global laser cutting machine market size is likely to be valued at US$7.0 Bn in 2025 and is estimated to reach US$10.3 Bn by 2032, growing at a CAGR of 5.7% during the forecast period from 2025 to 2032.

The rising adoption of fiber laser cutting machines, offering faster processing speeds, higher energy efficiency, and reduced maintenance compared to CO? and traditional systems, propels the need. Expanding applications in automotive, aerospace, and electronics manufacturing, along with the surge in EV battery production, are boosting demand. Furthermore, Industry 4.0 integration and automation in metal fabrication are accelerating investment, positioning fiber laser technology as the preferred choice across global industrial sectors

Key Industry Highlights:

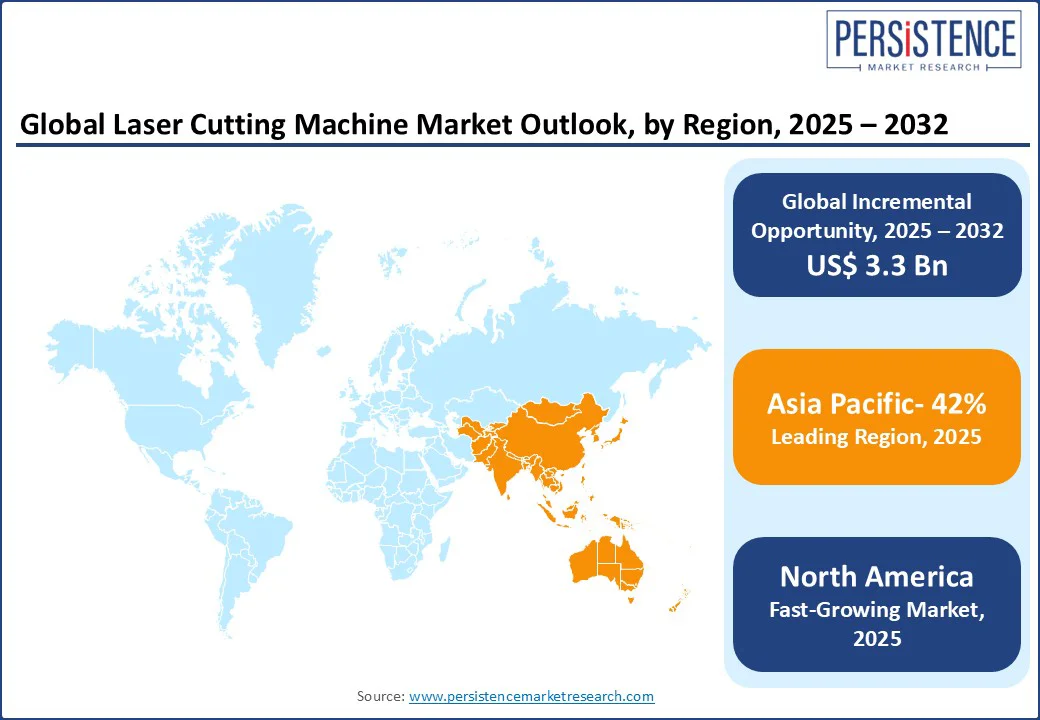

- Leading Region: Asia Pacific leads the global laser cutting machine market in 2025 with a 42% share, driven by manufacturing expansion in China, India, and growing industrial infrastructure.

- Fastest-Growing Region: North America is the fastest-growing market, driven by the adoption of advanced fiber and solid-state lasers, automation, precision manufacturing, and rising demand from the automotive, aerospace, and electronics sectors.

- Dominant Technology: Fiber lasers dominate with a 45% share, favored for energy-efficient, high-speed, and precise cutting across automotive, aerospace, electronics, and heavy metal fabrication applications.

- Leading Process: Flame cutting commands a 43.7% share, widely utilized in metal cutting applications requiring high efficiency, durability, and cost-effectiveness in construction, automotive, and shipbuilding industries.

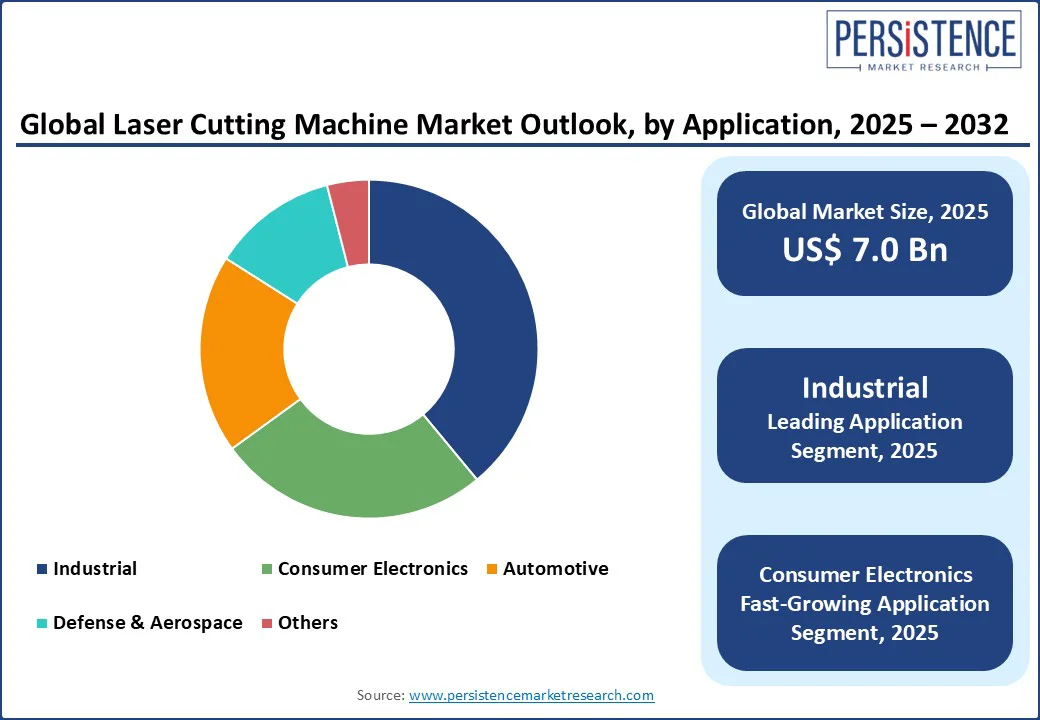

- Leading Application: Automotive leads with a 39% share, driven by electric vehicle production, precision component fabrication, and increasing demand for advanced metal and sheet cutting solutions.

- Key Developments: In 2023, Bystronic launched the ByCut Star 3015, while in 2024, Trumpf introduced AI-driven solutions, enhancing productivity and automation across metal fabrication operations.

|

Global Market Attribute |

Key Insights |

|

Laser Cutting Machine Market Size (2025E) |

US$7.0 Bn |

|

Market Value Forecast (2032F) |

US$10.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.2% |

Market Dynamics

Driver: Rising Demand for Precision Manufacturing in Automotive and Electronics

The rising demand for precision manufacturing is a key driver in the laser cutting machine market, particularly across the automotive sector. Automakers are increasingly integrating advanced electronic systems, including sensors, EV battery modules, and powertrain controls, which require high-accuracy and efficient production processes. According to the U.S. Department of Energy, electronics are expected to represent a significant share of vehicle costs in the coming years, making precision laser cutting and automated machining essential for scaling production. These technologies enable faster cutting speeds, reduced material waste, and superior quality—benefits that are critical for meeting global automotive manufacturing standards.

In electronics manufacturing, government initiatives are amplifying this trend. For instance, India’s Ministry of Electronics and Information Technology has launched large-scale Production-Linked Incentive (PLI) schemes to promote domestic electronic component production. Such programs are driving investment in precision machining, laser cutting systems, and smart manufacturing, reinforcing growth opportunities across both the automotive and electronics industries.

Restraint: High Initial and Operational Costs

A key restraint is the high initial investment required for advanced systems such as fiber lasers. While these machines deliver exceptional efficiency and precision, their capital costs remain significantly higher compared to conventional cutting equipment. Small and medium-sized manufacturers often find it difficult to allocate such large budgets, which limits adoption despite the long-term productivity gains. The requirement for additional infrastructure, including cooling units and safety systems, further increases the overall cost burden.

In addition to the steep purchase price, operational expenses present another challenge. Regular maintenance, replacement of parts, and the use of assist gases raise running costs. Moreover, employing skilled operators and technicians trained in handling advanced laser technologies adds to workforce expenditure. These combined financial factors slow down market penetration, particularly in cost-sensitive regions, restraining the widespread deployment of laser cutting machines across industries.

Opportunity: Advancements in Fiber Laser Technology and Emerging Markets

Advancements in fiber laser technology are creating significant growth opportunities in the laser cutting machine market. Modern fiber lasers deliver faster cutting speeds, higher energy efficiency, and reduced operating costs compared to traditional CO? systems. Innovations such as multi-kilowatt lasers, improved beam quality, and automated control systems are expanding in industries such as automotive, aerospace, and electronics. These advancements not only improve precision and throughput but also make fiber laser cutting a sustainable choice by reducing energy consumption and material waste, aligning with global trends toward smart manufacturing and Industry 4.0 integration.

Simultaneously, emerging markets are presenting lucrative avenues for expansion. Rapid industrialization in the Asia Pacific, Latin America, and parts of the Middle East is driving demand for advanced fabrication technologies. Government-backed manufacturing initiatives and infrastructure development projects are further encouraging investment in modern cutting solutions. As manufacturers in these regions seek efficient and cost-effective technologies, fiber laser cutting machines are increasingly positioned as a preferred solution for high-precision and scalable production.

Category-wise Analysis

Technology Insights

Solid-state lasers dominated in 2025, capturing about 45% share in 2025. Their leadership stems from superior energy efficiency, low maintenance requirements, and a strong capability to cut metals such as steel and aluminum with high precision. These qualities make them highly favored across industries such as automotive, aerospace, and heavy machinery, where durability and accuracy are critical. The increasing adoption of automation and Industry 4.0 technologies has further accelerated their usage, as manufacturers prioritize reliable and cost-effective solutions for high-volume production.

Gas lasers, on the other hand, are emerging as the fastest-growing technology segment. Known for their compact designs and cost-effectiveness, they are widely used in micro-cutting and precision applications within electronics manufacturing. Their growing role in semiconductor packaging, where nearly a quarter of processes adopted gas laser systems in 2024, highlights their importance in enabling miniaturization and supporting the rising demand for advanced electronic devices.

Process Type Insights

Flame cutting leads the laser cutting machine market in 2025, accounting for a 43.7% share. Its dominance is driven by the ability to handle thick materials such as carbon steel with high efficiency and relatively lower operational costs. Industries such as construction, shipbuilding, and automotive continue to rely on flame cutting for heavy-duty applications where durability and penetration depth are more critical than ultra-fine precision. This makes it a preferred choice for large-scale manufacturing environments seeking robust and cost-effective cutting solutions.

Fusion cutting, on the other hand, is expected to be the fastest-growing process segment in 2025. Known for delivering cleaner edges, enhanced accuracy, and reduced need for secondary finishing, it is increasingly adopted in aerospace, electronics, and medical device manufacturing. With industries prioritizing precision, reduced waste, and seamless integration with automation, fusion cutting is emerging as the process of choice to meet next-generation production demands

Application Insights

The industrial segment led in 2025, holding around 39% share. Its dominance is supported by strong demand from heavy machinery, automotive, shipbuilding, and construction, where high-precision cutting of metals such as steel and aluminum is essential. The push for automation, smart factories, and Industry 4.0 adoption has further reinforced the role of laser cutting machines in large-scale industrial applications, as manufacturers seek efficiency, durability, and cost optimization in high-volume production environments.

Consumer electronics is emerging as the fastest-growing end-use segment, driven by rapid miniaturization and the need for precise micro-cutting in devices such as smartphones, tablets, and wearables. Laser cutting enables high-accuracy processing of delicate components, including semiconductors and printed circuit boards, supporting the growing demand for compact and multifunctional devices. As governments and manufacturers invest heavily in electronics production capacity, laser cutting technology is increasingly becoming integral to next-generation electronics manufacturing.

Regional Insights

North America Laser Cutting Machine Market Trends

North America is expected to witness the fastest CAGR supported by strong adoption of fiber lasers and advanced cutting technologies across automotive, aerospace, and electronics manufacturing. The growing emphasis on precision manufacturing and automation, driven by Industry 4.0 initiatives, is accelerating equipment upgrades across the region. According to the U.S. Department of Energy and the National Institute of Standards and Technology, government-backed programs promoting energy-efficient and smart manufacturing are fueling demand for next-generation laser systems. Furthermore, rising investments in electric vehicle production and semiconductor fabrication in the U.S. and Canada are positioning North America as a high-growth hub for laser cutting technologies.

Europe Laser Cutting Machine Market Trends

Europe holds a significant share in 2025, supported by its strong industrial base and advanced manufacturing capabilities. The region’s well-established automotive, aerospace, and machinery sectors continue to drive steady demand for fiber and solid-state laser systems. European manufacturers are also at the forefront of adopting sustainable and energy-efficient technologies, aligning with the EU’s Green Deal and carbon reduction targets. Germany, Italy, and France remain key hubs for precision engineering and smart factory deployment, ensuring consistent uptake of laser cutting machines across industrial applications and reinforcing Europe’s leadership in high-value manufacturing.

Asia Pacific Laser Cutting Machine Market Trends

Asia Pacific dominated the laser cutting machine market in 2025, accounting for approximately 42% share, driven by rapid industrialization and a growing manufacturing infrastructure in countries such as China, India, and Japan. Strong demand from automotive, electronics, and metal fabrication industries, coupled with increasing adoption of fiber and solid-state laser technologies, has reinforced the region’s leadership. Government initiatives supporting smart manufacturing, automation, and local production capacity are further accelerating growth. Additionally, the expansion of electric vehicle production and semiconductor manufacturing in the region continues to drive investment in high-precision laser cutting systems, positioning Asia Pacific as the largest and most dynamic market globally.

Competitive Landscape

The global laser cutting machine market is highly competitive, driven by continuous technological innovation and the growing demand for high-precision and energy-efficient systems. Manufacturers are focusing on developing advanced fiber and solid-state lasers, integrating automation and smart factory solutions to enhance productivity. Regional expansion, strategic partnerships, and investments in R&D are intensifying competition. Additionally, rising adoption in automotive, aerospace, electronics, and emerging industrial sectors is prompting companies to differentiate through product efficiency, versatility, and cost-effectiveness, shaping a dynamic and evolving market landscape.

Key Developments:

- November 2023: Bystronic launched the ByCut Star 3015, enhancing cutting efficiency by 15%, offering faster processing and improved precision for metal fabrication applications.

- March 2024: Trumpf introduced the AI Runability Guide for the TruMatic 5000, boosting operational productivity by 10% through smarter automation and optimized cutting processes.

- December 2024: HSG Laser inaugurated a new facility in Jinan, aiming to produce 10,000 units annually, strengthening manufacturing capacity and supporting market expansion in Asia.

Companies Covered in Laser Cutting Machine Market

- Trumpf

- Bystronic

- Mazak

- Amada

- Coherent

- IPG Photonics

- Prima Power

- Mitsubishi Electric

- Han's Laser Technology

- Hypertherm

- Others

Frequently Asked Questions

The laser cutting machine market share is projected to reach US$7.0 Bn in 2025, driven by automotive and electronics demand.

Precision manufacturing needs in automotive, electronics, and aerospace, along with automation trends, fuel growth.

Market share is estimated to grow from US$7.0 Bn in 2025 to US$10.3 Bn by 2032, with a CAGR of 5.7%.

Fiber laser advancements and emerging market expansion in India and Brazil drives growth.

Leading players include Trumpf, Bystronic, Mazak, Amada, and IPG Photonics.