- Medical Devices

- Cutting Balloons Market

Cutting Balloons Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Market Study on Cutting Balloons: PMR Suggests Promising Prospects for the Market, Analysing the Innovations in Vascular Interventions, Rising Prevalence of Arterial Diseases and a Growing Demand for Minimally Invasive Treatment Options

Cutting Balloons Market Share and Trends Analysis

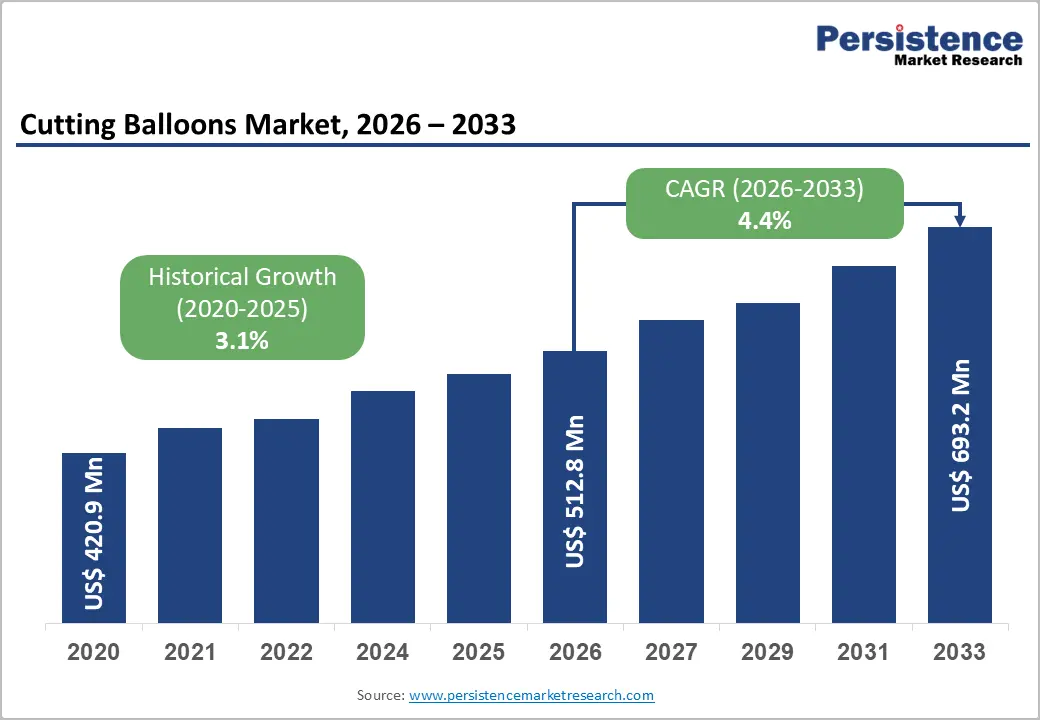

The global cutting balloons market size is likely to be valued at US$512.8 million in 2026 to US$693.2 million by 2033, growing at a CAGR of 4.4% during the forecast period from 2026 to 2033. With the rise in adoption of interventional cardiology, demand for precision-based tools for complex vascular lesions is rising.

Cutting balloons are designed with microsurgical blades that create controlled incisions in fibrotic or calcified plaques, enabling effective vessel dilation at lower inflation pressures. Their use is expanding in procedures such as coronary artery disease treatment, in-stent restenosis management, and peripheral vascular interventions. The growing prevalence of cardiovascular diseases, rising preference for minimally invasive procedures, and improved clinical outcomes compared to conventional angioplasty balloons are supporting market growth.

Key Industry Highlights:

- The rise in prevalence of coronary artery disease, peripheral artery disease, and calcified lesions globally is driving demand for cutting balloons as effective plaque-modifying tools in interventional cardiology procedures.

- The global shift toward minimally invasive cardiovascular interventions has increased demand for advanced balloon technologies that enhance procedural efficiency, accuracy, and patient recovery outcomes.

- Hospitals and cardiac catheterization laboratories remain primary users due to high procedure volumes, availability of skilled interventional cardiologists, and access to advanced imaging and support systems.

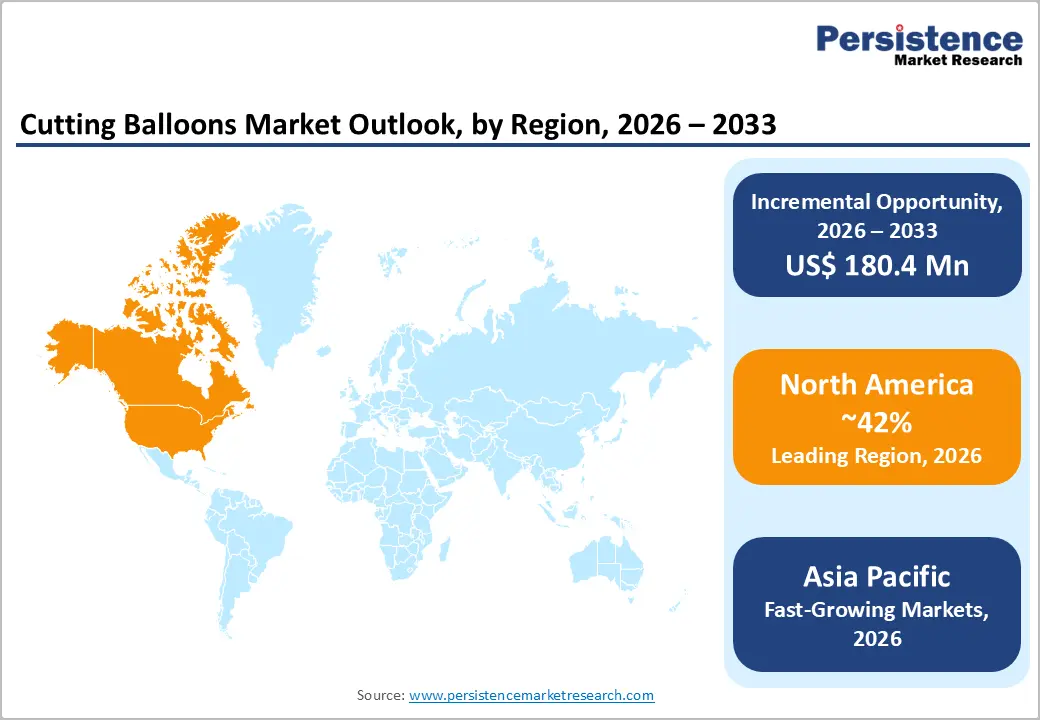

- Leading Region: North America leads due to a high prevalence of cardiovascular diseases, widespread adoption of advanced interventional cardiology procedures, and strong presence of well-equipped hospitals and cardiac catheterization laboratories.

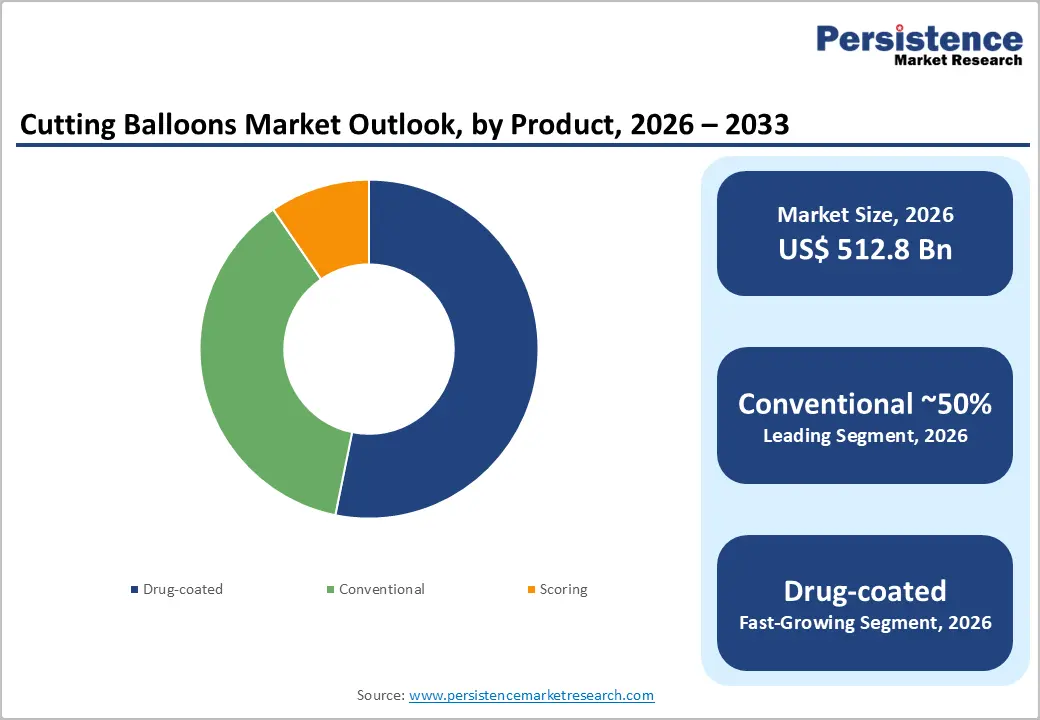

- Leading Product: Conventional cutting balloons are widely used due to their established clinical effectiveness, broad availability, and lower cost compared to drug-coated and scoring variants.

| Key Insights | Details |

|---|---|

|

Cutting Balloons Market Size (2026E) |

US$512.8 Mn |

|

Market Value Forecast (2033F) |

US$693.2 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.1% |

Market Dynamics

Driver - Higher Incidence of In-Stent Restenosis

The rising incidence of in-stent restenosis (ISR) has become a significant driver for the cutting balloons market, as clinicians increasingly seek precise and controlled lesion-preparation devices to manage this complex condition. In-stent restenosis occurs when excessive neointimal tissue growth leads to re-narrowing of the treated vessel after stent implantation, often compromising blood flow and increasing the risk of repeat interventions. Conventional balloon angioplasty may inadequately address the dense, fibrotic tissue associated with ISR, resulting in suboptimal vessel expansion and higher recurrence rates.

Cutting balloons offer a targeted solution by incorporating microsurgical blades that create controlled incisions in the restenotic tissue before dilation. This mechanism allows uniform plaque modification at lower inflation pressures, reducing vessel trauma, elastic recoil, and uncontrolled dissections. As a result, cutting balloons are increasingly preferred during ISR treatment to improve procedural predictability and optimize lumen gain prior to additional therapies such as drug-coated balloons or repeat stenting.

The growing volume of coronary stent implantations worldwide has naturally increased the pool of patients at risk for ISR, further elevating demand for effective lesion-preparation technologies. Additionally, advancements in cutting balloon design, flexibility, and trackability have improved their performance in challenging anatomies commonly seen in restenotic lesions. Overall, the need to enhance clinical outcomes, minimize repeat procedures, and manage complex post-stent complications positions cutting balloons as a critical tool in modern interventional cardiology practice.

Restraints - Risk of Vessel Injury

Risk of vessel injury remains a critical restraint in the cutting balloons market, primarily due to the mechanical nature of the device and its reliance on microsurgical blades to modify vascular plaque. Unlike conventional balloons that apply uniform radial pressure, cutting balloons create controlled incisions in the vessel wall to facilitate dilation. When used improperly—such as incorrect balloon sizing, excessive inflation pressure, or poor lesion selection—these blades can penetrate beyond the intended plaque layer, increasing the risk of vessel dissection or perforation. This risk is particularly pronounced in fragile, calcified, or small-diameter vessels, where arterial walls are thinner and less tolerant to mechanical stress.

In complex anatomies, such as tortuous or highly stenotic lesions, precise positioning becomes challenging, further elevating the chance of unintended vascular injury. Any complication involving vessel damage can lead to prolonged procedures, emergency stenting, or surgical intervention, increasing both clinical risk and procedural cost. As a result, many interventional cardiologists prefer alternative plaque-modification technologies that offer greater safety margins in delicate cases.

Additionally, concerns around vessel injury limit the broader use of cutting balloons in peripheral and small-vessel interventions, confining their application largely to selected coronary lesions. The perceived safety risk also influences hospital purchasing decisions, as institutions may restrict usage to highly experienced operators only. Until device designs further improve blade control, flexibility, and safety predictability, the potential for vessel injury remains a significant barrier to widespread adoption, particularly in less specialized healthcare settings.

Opportunity - Integration with Drug-Coated Technologies

Integration with drug-coated technologies represents a compelling growth opportunity within the Cutting Balloons market, as it addresses one of the most persistent challenges in interventional cardiology—long-term vessel patency. While cutting balloons are highly effective at mechanically modifying fibrotic and calcified plaques through controlled micro-incisions, restenosis can still occur due to smooth muscle cell proliferation and inflammatory responses following vessel injury. Integrating drug-delivery strategies with cutting balloon technology offers a synergistic approach by combining precise plaque disruption with localized pharmacological therapy.

By creating controlled incisions in the vessel wall, cutting balloons can enhance drug penetration when paired with antiproliferative agents, improving drug uptake compared to conventional balloon angioplasty. This integration can potentially reduce neointimal hyperplasia, minimize elastic recoil, and lower the need for repeat revascularization procedures. From a procedural standpoint, such hybrid devices may streamline workflows by reducing the number of devices required during interventions, improving efficiency in cardiac catheterization laboratories.

Clinically, drug-integrated cutting balloons could offer a valuable alternative for patients with complex lesions, small vessels, or in-stent restenosis where stent placement is less desirable. From a market perspective, this innovation allows manufacturers to differentiate products, command premium pricing, and align with value-based care models focused on durable outcomes rather than procedural volume. As clinical evidence and regulatory approvals expand, integration with drug-coated technologies is poised to redefine cutting balloon applications and significantly enhance long-term treatment effectiveness.

Category-wise Analysis

By Product Insights

In the Cutting Balloons market, conventional cutting balloons hold the highest market share due to their widespread clinical acceptance, proven efficacy, and cost-efficiency. These devices have been extensively used in interventional cardiology for plaque modification, particularly in fibrotic or calcified coronary lesions, as well as in managing in-stent restenosis. Their well-established safety profile and predictable performance make them the preferred choice among interventional cardiologists, especially in routine procedures where reliability and ease of use are critical.

Compared to drug-coated and scoring variants, conventional cutting balloons are more widely available and come at a lower cost, making them accessible to hospitals and cardiac catheterization laboratories globally. While drug-coated balloons offer the advantage of delivering antiproliferative agents to reduce restenosis, and scoring balloons provide enhanced precision in complex lesions, these segments are relatively newer, more specialized, and often command higher prices. Consequently, their adoption is limited to specific patient populations or challenging cases.

Overall, the combination of affordability, broad clinical applicability, established outcomes, and clinician familiarity ensures that conventional cutting balloons remain the dominant product segment, contributing the largest revenue share in the market while other innovative variants continue to grow steadily.

By End-user Insights

In the Cutting Balloons market, hospitals dominate the end-user segment due to their capacity to perform a high volume of complex interventional cardiology procedures. Hospitals, particularly tertiary care centers with fully equipped cardiac catheterization laboratories, manage both routine and high-risk patients requiring coronary and peripheral interventions. The availability of advanced imaging technologies, experienced interventional cardiologists, and comprehensive support infrastructure allows hospitals to adopt cutting balloons extensively for precise plaque modification, in-stent restenosis management, and complex lesion treatments.

Hospitals also benefit from robust budgets and reimbursement support, enabling procurement of high-cost devices like cutting balloons, which smaller cardiac centers or ambulatory surgical centers may find cost-prohibitive. Additionally, hospitals often serve as referral centers for complex cases, increasing procedural volumes and reinforcing their dominant market share.

While cardiac centers and ambulatory surgical centers are witnessing gradual adoption due to growing awareness and minimally invasive procedure trends, their limited procedural capacity, narrower service scope, and lower budgets restrict widespread usage. Overall, the combination of high procedure volume, infrastructure, trained personnel, and financial capability ensures hospitals remain the leading end-user segment, driving the majority of cutting balloon demand globally.

Regional Insights

North America Cutting Balloons Market Trends

North America is the leading region in the Cutting Balloons market, driven by advanced cardiovascular care infrastructure, high prevalence of coronary artery disease, and early adoption of innovative interventional technologies. In the U.S., cutting balloons are increasingly used in hospitals and cardiac catheterization laboratories for treating complex lesions, calcified plaques, and in-stent restenosis. Favorable reimbursement policies, widespread insurance coverage, and high awareness among cardiologists support adoption across both urban and regional healthcare facilities.

Technological advancements are shaping the market, with next-generation cutting balloons offering improved blade designs, enhanced flexibility, and compatibility with drug-coated applications, enabling precise plaque modification and better procedural outcomes. Hospitals leverage these devices to improve patient safety, reduce elastic recoil, and minimize repeat interventions. Additionally, the integration of cutting balloons with imaging guidance and workflow optimization platforms streamlines procedures and enhances clinical efficiency.

Rising minimally invasive procedures, increased procedural volumes, and a focus on value-based care further strengthen demand. The U.S. remains the largest contributor to regional growth, while Canada and Mexico also demonstrate gradual adoption, driven by expanding cardiovascular services. Overall, North America’s combination of infrastructure, clinical expertise, regulatory support, and technological innovation solidifies its position as the leading market globally.

Asia Pacific Cutting Balloons Market Trends

Asia Pacific is emerging as the fastest-growing market for cutting balloons, fueled by rising cardiovascular disease prevalence, expanding healthcare infrastructure, and increasing awareness of advanced interventional cardiology procedures. Countries such as China, India, Japan, and Australia are investing heavily in modern hospitals and cardiac catheterization laboratories, enabling the adoption of cutting balloons for treating complex coronary lesions, calcified plaques, and in-stent restenosis. Rapid urbanization, growing disposable incomes, and increased access to private healthcare are driving demand for minimally invasive procedures, making cutting balloons a preferred choice for precision angioplasty.

Technological innovations, including improved blade designs, low-profile balloons, and integration with drug-coated and imaging-guided systems, are enhancing procedural success and patient outcomes. Government initiatives and public health programs promoting cardiovascular disease management further support market expansion, particularly in India, Southeast Asia, and China. Additionally, partnerships between local distributors and global device manufacturers are increasing product availability and awareness.

Overall, the Asia Pacific presents significant growth opportunities as hospitals, cardiac centers, and emerging healthcare facilities adopt cutting balloons to improve patient care, procedural efficiency, and long-term clinical outcomes, positioning the region as a key emerging market globally.

Competitive Landscape

The Cutting Balloons market is highly competitive, driven by innovation, clinical effectiveness, and technological differentiation. Key players compete by offering advanced blade designs, flexible shafts, low-profile balloons, and integration with drug-coated or imaging-guided systems to improve procedural outcomes. Competition also focuses on expanding hospital and cardiac center adoption through physician training, reimbursement support, and workflow optimization. Emerging entrants emphasize cost-effective solutions, minimally invasive applications, and peripheral artery interventions.

Key Industry Developments:

- In March 2025, Abbott received CE Mark approval in Europe for the Volt™ PFA System to treat patients with atrial fibrillation (AFib). Following the earlier-than-expected CE Mark, Abbott began commercial PFA procedures in the EU with physicians who had already gained experience with the Volt PFA System through Abbott's PFA clinical studies.

- In August 2025, Boston Scientific initiated the AGENT DCB STANCE trial to assess the safety and effectiveness of the AGENT™ Drug-Coated Balloon (DCB) compared to the standard of care percutaneous coronary intervention (PCI) with drug-eluting stents (DES) and/or balloon angioplasty in patients with de novo (previously untreated) coronary lesions.

Companies Covered in Cutting Balloons Market

- Abbott

- Boston Scientific Corporation

- B. Braun Melsungen AG

- Cook Medical

- Cordis

- Medtronic

- MicroPort Scientific Corporation

- Opto Circuits (India) Ltd.

- Spectranetics (Philips Healthcare)

- Terumo Corporation

- TriReme Medical, LLC (QT Vascular Ltd.)

- Vascular Concepts Limited

- Others

Frequently Asked Questions

The global cutting balloons market is projected to be valued at US$512.8 Mn in 2026.

Cutting balloons allow controlled plaque incision at lower inflation pressures, reducing vessel trauma and improving procedural outcomes compared to conventional balloon angioplasty.

The global market is poised to witness a CAGR of 4.4% between 2026 and 2033.

Development of flexible, low-profile, and lesion-specific balloons increases procedural efficiency and patient safety.