- Metalworking & Fabrication

- Plasma Cutting Equipment Market

Plasma Cutting Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Plasma Cutting Equipment Market by Equipment Type (Manual and Mechanized), Application (Industrial Manufacturing, Automotive, Construction, Salvage and Scrapping Operation, Shipbuilding and Others), by Thickness Capacity (Below 5mm, 5mm -15mm, 15mm-50mm and Above 50mm)) and Regional Analysis for 2026 - 2033

Plasma Cutting Equipment Market Size and Trends Analysis

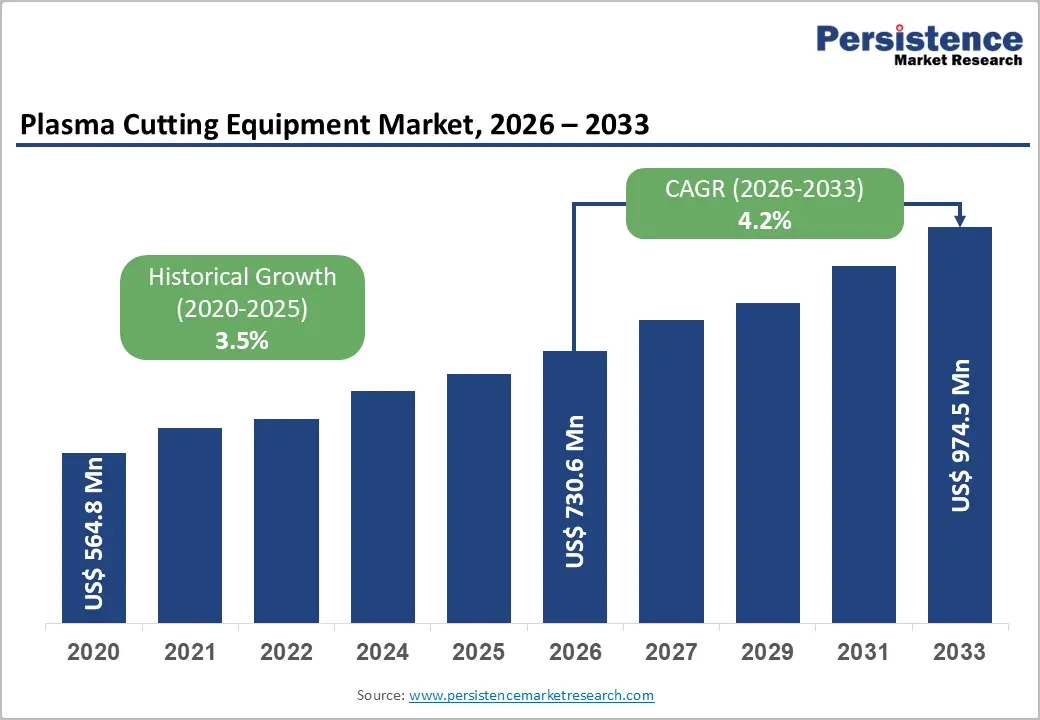

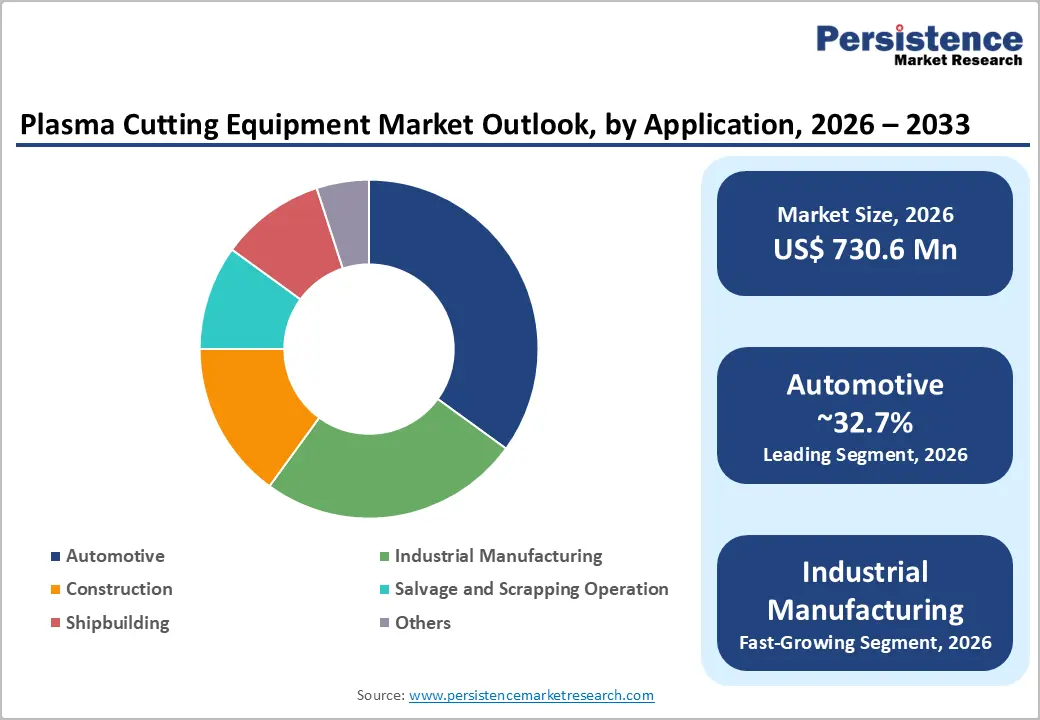

The global plasma cutting equipment market was valued at US$ 730.6 Mn in 2026 and is projected to reach US$ 974.5 Mn by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

Growth is driven by accelerating adoption of mechanized and CNC-controlled plasma systems in automotive and industrial manufacturing, increasing demand for high-precision cutting in shipbuilding and construction, and rising preference for plasma cutting over traditional oxy-fuel methods due to superior speed and edge quality.

Key Industry Highlights:

- Equipment type segmentation: Mechanized systems dominate at 65.4% share (~US$ 531.2 million 2026), while manual plasma cutters are fastest-growing at 5.8% CAGR, supported by emerging market accessibility and site-based fabrication.

- Application dynamics: Automotive represents 32.7% share (~US$ 266 million 2026) with steady 3.8% CAGR, while industrial manufacturing is fastest growing at 6.5% CAGR, driven by heavy equipment and emerging market expansion.

- Thickness capacity shift: 5mm-15mm range leads at 39.5% share, while 15mm-50mm range is fastest-growing at 5.2% CAGR, reflecting shipbuilding and structural fabrication expansion.

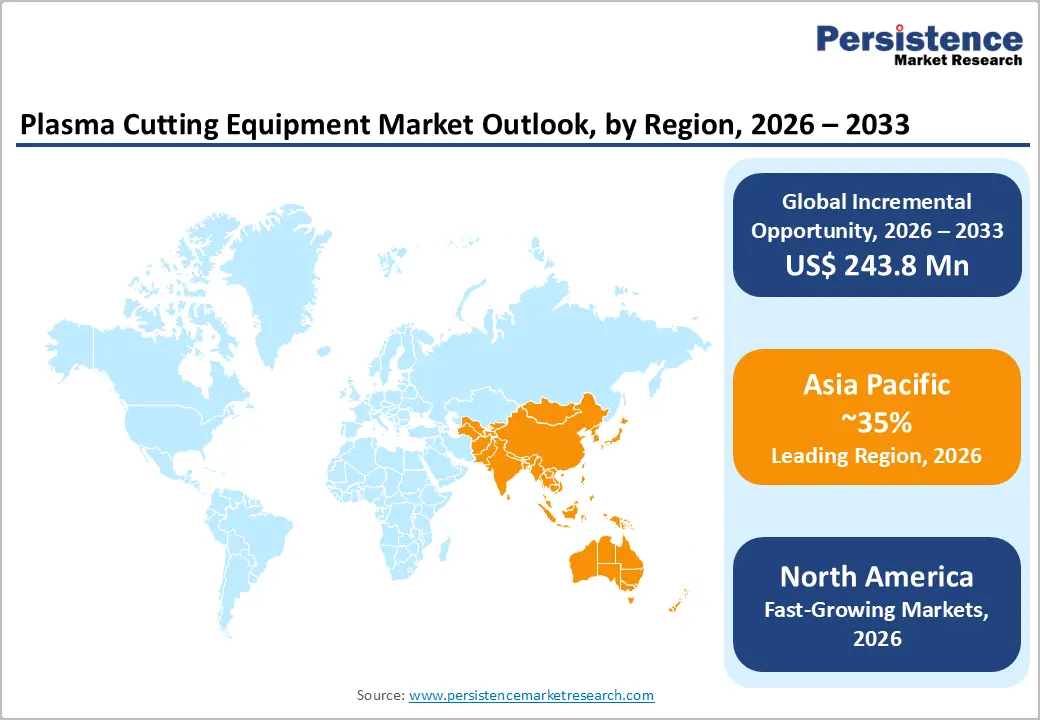

- Regional performance: Asia-Pacific dominates at 35% global share (~US$ 350-380 million 2026) with 5.5% CAGR; Europe shows steady growth (3.5% CAGR); North America exhibits mature market characteristics (3.2% CAGR).

- Strategic trends: Consumables differentiation and recurring revenue models emerging (Cutmaster Black, extended warranties); multi-technology consolidation (Hypertherm rebranding, Lincoln Electric integration); emerging market localization and channel partnerships (Fab-Cut, regional OEM relationships).

| Global Market Attributes | Key Insights |

|---|---|

| Plasma Cutting Equipment Market Size (2026E) | US$ 730.6 Mn |

| Market Value Forecast (2033F) | US$ 974.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2024) | 3.5% |

Market Dynamics

Growth Drivers

Industry 4.0 Integration and Automation-Driven Precision Manufacturing

Modern manufacturing environments increasingly demand real-time process control, precision repeatability, and automated quality verification2033capabilities embedded in advanced CNC plasma cutting systems with integrated torch height control (THC), automatic parameter adjustment, and AI-driven optimization. Plasma cutting machines equipped with multi-axis CNC controllers, CAD/CAM software integration, and automatic nesting algorithms achieve 15-25% material waste reduction, 20-40% cycle time improvements, and superior edge quality compared to manual operations. Industry 4.0 adoption is driving demand for connected plasma systems with IoT sensors, real-time diagnostics, and predictive maintenance algorithms enabling downtime reduction of 30-50%. The global manufacturing sector's investment in digital transformation and automation is estimated to drive incremental plasma cutting equipment demand of US$ 150 million annually across the forecast period.

Automotive and Aerospace Production Scaling with Precision Requirements

The automotive industry continues expanding production capacity globally, particularly for lightweight, high-strength materials (aluminum, stainless steel, advanced high-strength steels) requiring precision plasma cutting for chassis components, exhaust systems, body reinforcements, and structural elements. Automotive represents 32.7% of plasma equipment market share (~US$ 266 million 2026), with consistent growth from new model launches, platform electrification, and lightweight design initiatives. Aerospace and defense sectors2033experiencing 7-10% annual production growth2033require high-precision plasma cutting for fuselage components, fastener hole punching, and structural frame fabrication, commanding premium system pricing and sustained demand for advanced mechanized equipment.

Market Restraints

Capital Investment Requirements and Total Cost of Ownership Barriers

Advanced CNC mechanized plasma systems represent significant capital investments, with entry-level gantry systems starting at US$ 50,000-100,000 and high-precision, multi-torch systems exceeding US$ 500,000-2 million, including installation, tooling, software, operator training, and integration costs adding 25-40% to equipment purchase price. For small- and medium-sized enterprises (SMEs) in developing economies, this investment barrier defers purchases or forces continued reliance on lower-cost manual or semi-automatic equipment, constraining overall market growth. Financing and leasing options remain limited in emerging markets, further restricting access and penetration in high-growth regions like India and Southeast Asia.

Competition from Alternative Cutting Technologies and Price Deflation

Laser cutting technology, while more costly upfront, offers superior edge quality and reduced material waste in specific applications (thin-gauge materials <5mm, precision components), creating competitive headwinds for plasma equipment in premium segments. Additionally, oxy-fuel cutting remains entrenched in cost-sensitive applications and developing markets due to significantly lower equipment cost and established operator familiarity, constraining plasma equipment market growth in price-conscious segments. Equipment price deflation (estimated at 2% annually for standard mechanized systems) pressures manufacturer margins and limits growth for suppliers lacking differentiation through advanced technology, specialization, or service integration.

Market Opportunities

Industrial Manufacturing Sector Expansion and Advanced Fabrication Specialization

Industrial manufacturing2033spanning heavy equipment (excavators, cranes, hydraulic systems), agricultural equipment, construction machinery, and mining equipment2033represents the fastest-growing application segment at estimated 6.5% CAGR. Mechanized plasma cutting systems enable efficient production of complex structural components, hydraulic mounts, buckets, and boom structures, supporting high-volume, repetitive fabrication at competitive costs. This segment is estimated at US$ 110 million (2026), projected to grow toward US$ 180 million by 2033, representing a US$ 70 million incremental market opportunity for suppliers offering specialized heavy-duty cutting solutions with advanced automation and process optimization.

High-Definition (HD) Plasma Technology for Precision Thin-Stainless Cutting

High-definition plasma cutting technology 2033 featuring advanced torch designs, optimized gas dynamics, and precision power supply control 2033 enables superior edge quality and dimensional accuracy comparable to laser cutting for thin stainless steel and specialty materials. HD plasma systems command 15% price premiums relative to conventional systems and are growing at 8% CAGR, driven by aerospace, food processing, and medical device manufacturing demanding high-quality edges without post-cutting finishing. This specialized segment represents a US$ 60 million market opportunity growing at double the baseline market rate, offering high-margin growth for suppliers offering HD plasma platforms and specialized torches/consumables.

Segmentation Analysis

Equipment Type Analysis

Mechanized plasma cutting systems2033including CNC gantry tables, robotic plasma systems, and automated cutting centers2033represent the largest segment at 65.4% market share (~US$ 531.2 million 2026), driven by widespread adoption in automotive, shipbuilding, construction, and industrial manufacturing where precision, repeatability, and high-volume production are critical. Mechanized systems offer superior speed (cutting speeds 5-10m/min), precision (±0.5mm-1.0mm tolerance), and operator safety relative to manual equipment.

Manual plasma cutting equipment is the fastest-growing segment at estimated 5.8% CAGR, with market value of approximately US$ 281 million (2026) projected to grow toward US$ 430 million by 2033. Manual systems remain attractive for site-based construction fabrication, field repairs, salvage operations, and small-shop fabrication where equipment portability, ease-of-use, and lower capex are prioritized over maximum precision. Growth is driven by infrastructure construction expansion in emerging markets, accessibility in developing countries, and utility in salvage/scrapping operations.

Application Analysis

Automotive manufacturing represents the largest application segment at 32.7% market share (~US$ 266 million 2026), driven by chassis and structural component fabrication, exhaust system cutting, and body panel production. Automotive plasma equipment demand is projected to grow at approximately 3.8-4.5% CAGR, constrained by mature market saturation in developed countries but supported by new model launches, lightweight material adoption, and emerging market vehicle production.

Industrial manufacturing (heavy equipment, agricultural machinery, hydraulic systems, construction equipment) is the fastest-growing segment at estimated 6.5% CAGR, with market value of approximately US$ 110-140 million (2026) projected to grow toward US$ 180-230 million by 2033. Growth drivers include global heavy equipment production expansion, emerging market construction booms, and increasing adoption of mechanized cutting for efficiency and precision improvements.

Thickness Capacity Analysis

The 5mm-15mm thickness capacity range represents the largest segment at 39.5% share (~US$ 320.8 million 2026), reflecting widespread applicability across automotive, light fabrication, sheet metal work, and general industrial cutting where most components fall within this thickness range. This segment is expected to grow at approximately 3.5% CAGR, supporting steady revenue generation from mature, high-volume applications.

The 15mm-50mm thickness range is the fastest-growing segment at estimated 5.2% CAGR, driven by heavy industrial, shipbuilding, and structural fabrication applications requiring thick-plate cutting capability for hull plates, structural beams, platform components, and heavy machinery frames. Market value is approximately US$ 250-280 million (2026), projected to grow toward US$ 380 million by 2033, reflecting above-market growth in mechanized, high-capacity systems.

Regional Market Insights

North America

North America represents an estimated US$ 180 million market (2026) with projected growth to US$ 240 million by 2033, reflecting 2.9% CAGR2033below global baseline, reflecting market maturity. The U.S. dominates regional demand with approximately US$ 138.9 million market (2026), driven by strong automotive, aerospace, shipbuilding, and construction sectors.

The regulatory environment emphasizes OSHA workplace safety standards, EPA environmental compliance for consumables/gases, and material traceability requirements. These standards support steady equipment replacement and upgrading cycles among established manufacturers.

U.S. manufacturing exhibits strategic focus on automation, Industry 4.0 adoption, and supply chain localization (reshoring initiatives), creating demand for advanced CNC mechanized systems supporting precision manufacturing and efficiency targets. The competitive landscape features global leaders (Hypertherm, ESAB, Lincoln Electric, Messer Cutting Systems) with strong U.S. presence and regional specialists focusing on niche applications or customization.

Europe

Europe represents an estimated US$ 200 million market (2026) with projected growth to US$ 275 million by 2033, reflecting 4.5% CAGR. Germany, France, U.K., and Spain lead European demand, driven by strong automotive, manufacturing, and shipbuilding presence, combined with stringent environmental and safety regulations.

The regulatory environment emphasizes EU machinery directives (2006/42/EC), environmental standards (emissions, waste management), and worker safety (Machinery Directive). These standards drive investment in advanced equipment with enhanced safety features, environmental monitoring, and consumables management.

Germany's manufacturing sector 2033 accounting for 20% of EU industrial production2033maintains significant demand for mechanized plasma equipment serving automotive, machinery, and construction industries. European shipbuilding (Danish, Dutch, Italian yards) requires large-scale, high-precision mechanized systems, creating embedded demand for advanced plasma cutting platforms.

Asia-Pacific

Asia-Pacific represents an estimated US$ 350 million market (2026) with projected growth to US$ 540 million by 2033, reflecting 5.5% CAGR2033highest among global regions. The region is the largest market by absolute size (~35% of global market 2026), anchored by China's dominance, Japan's technological leadership, and emerging manufacturing in India and ASEAN.

China dominates regional demand with approximately US$ 115 million market (2026) and 6.8% projected CAGR, driven by world's largest automotive production (~28 million vehicles annually), heavy equipment manufacturing, shipbuilding dominance, and construction expansion. China is increasingly transitioning from manual/semi-automatic equipment toward advanced mechanized CNC systems, supporting above-market growth in high-precision segments.

Plasma Cutting Equipment Market Competitive Landscape

The plasma cutting equipment market is moderately fragmented, with global leaders (Hypertherm, ESAB/Thermal Dynamics, Lincoln Electric, Messer Cutting Systems, Victor Technologies) commanding approximately 40% of global revenues. The market supports meaningful participation from regional specialists, OEM suppliers, and equipment integrators focusing on specific applications, geographic markets, or niche technologies.

Barriers to entry include substantial R&D investment (US$ 2-10 million annually for competitive product development), manufacturing expertise in precision equipment, OEM relationships, and aftermarket support infrastructure. However, these barriers are not prohibitively high for regional manufacturers or system integrators offering cost-optimized solutions or application-specific configurations.

Key Industry Developments

- In March 2025, Linde Engineering and Voestalpine AG announced a partnership that will jointly develop a welding wire technique for ammonia tank welding. This aims to minimize the complexities of ammonia tank storage construction by the selection of proper welding consumables together with an increased degree of automation in the welding process.

- In March 2025, Miller, a leading welding brand, announced the release of Copilot Builder, the newest addition to its Collaborative Robots product portfolio. The robot is developed to address unique welding challenges with flexibility, delivering a versatile product solution that is reconfigurable, portable, and ready to tackle diverse welding needs.

Companies Covered in Plasma Cutting Equipment Market

- AMADA Co., Ltd

- Bystronic Laser AG

- Carlson Engineering & Manufacturing, Inc.

- Coherent Corp.

- DAIHEN Corporation

- ESAB Corporation

- Hypertherm

- Illinois Tool Works Inc.

- Kemppi Oy

- Koike Aronson, Inc.

- Others Key Players

Frequently Asked Questions

The Plasma Cutting Equipment market is estimated to be valued at US$ 730.6 Mn in 2026.

The key demand driver for the Plasma Cutting Equipment market is the growing need for fast, precise, and cost-efficient metal cutting across industrial manufacturing and fabrication sectors.

In 2026, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Plasma Cutting Equipment market.

Among the Application, Automotive hold the highest preference, capturing beyond 32.7% of the market revenue share in 2026, surpassing other Application.

The key players in Plasma Cutting Equipment are AMADA Co., Ltd, Bystronic Laser AG, Coherent Corp. and DAIHEN Corporation.