- Industrial Machinery

- Turbine Motor Market

Turbine Motor Market Size, Share, and Growth Forecast, 2025 - 2032

Turbine Motor Market by Motor Type (Gas Turbine Motors, Steam Turbine Motors, Hydraulic Turbine Motors, Wind Turbine Motors), Capacity (Small: Less than 10 MW, Medium: 10-100 MW, Large: Greater than 100 MW), End-use (Energy & Utilities, Aerospace, Manufacturing, Transportation, Mining & Metals), and Regional Analysis for 2025 - 2032

Turbine Motor Market Size and Trend Analysis

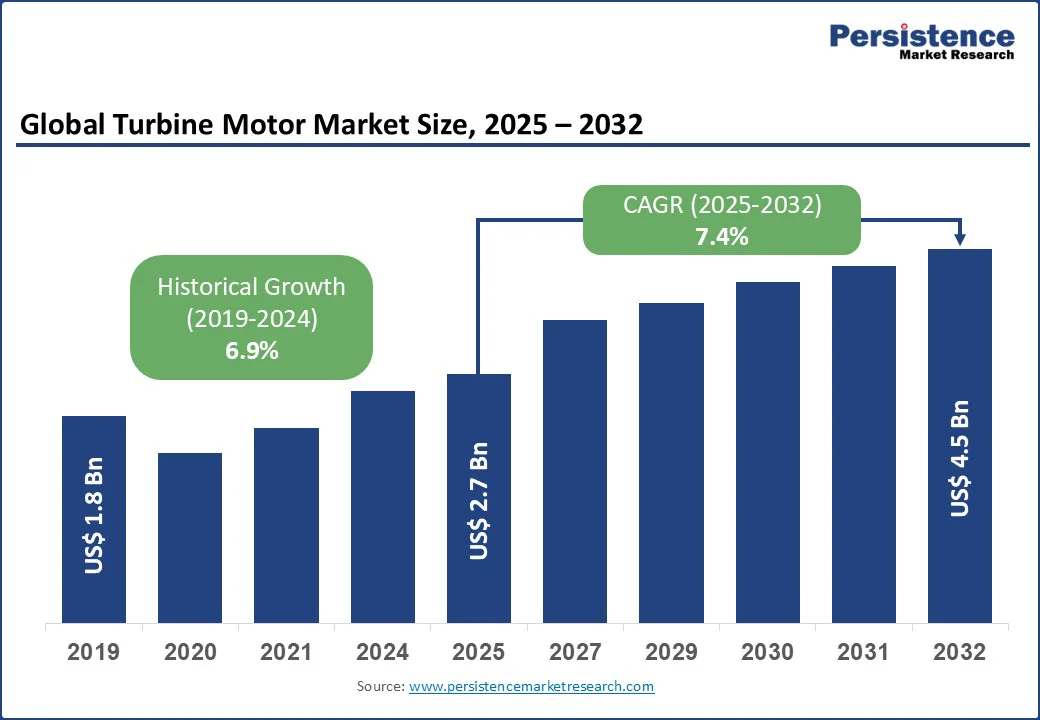

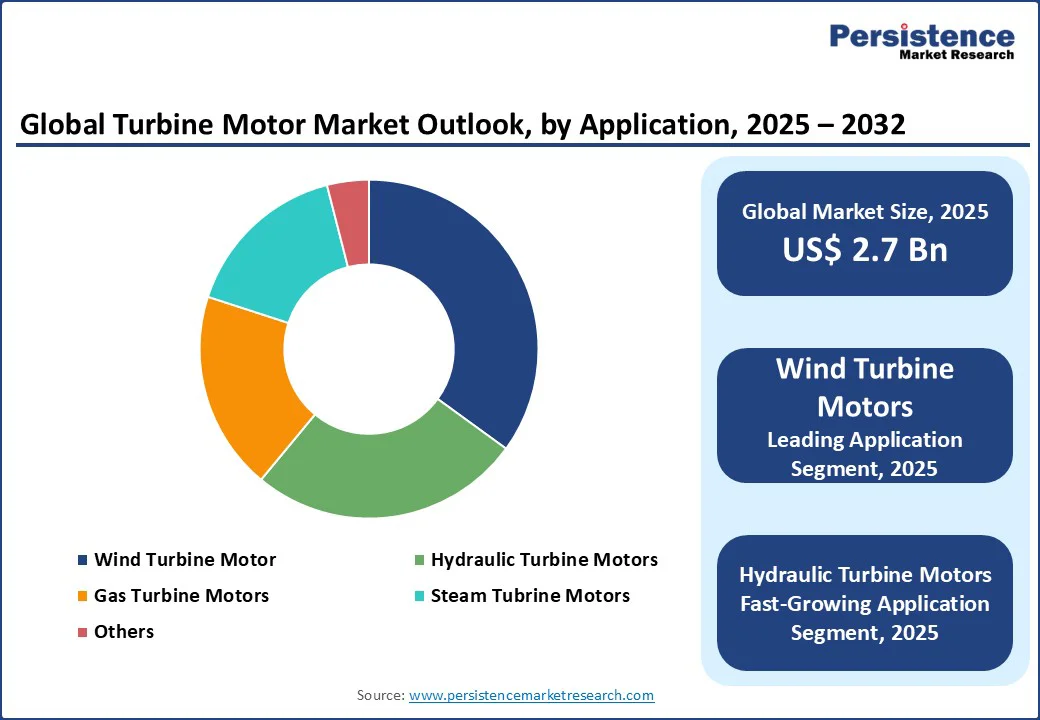

The global turbine motor market size is likely to be valued at US$2.7 Bn in 2025 and is expected to reach US$4.5 Bn by 2032, growing at a CAGR of 7.4% during the forecast period from 2025 to 2032.

The growth is driven by the rising adoption of renewable energy sources, especially wind and hydropower, supported by government initiatives and environmental policies worldwide.

Key Industry Highlights

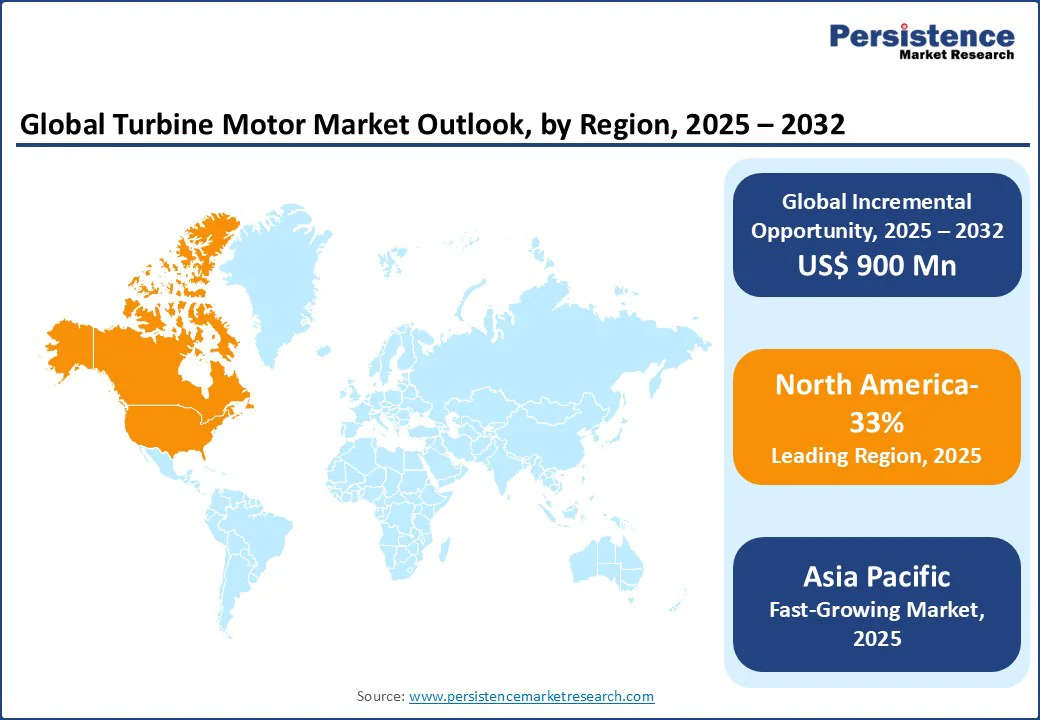

- Leading Region: North America accounts for 33% of the global turbine motor market in 2025, supported by strong demand from the aerospace industry and large-scale renewable energy projects.

- Fastest-Growing Region: Asia Pacific leads in growth, driven by rapid industrialization and expanding renewable energy investments in China and India.

- Dominant Motor Type: Wind turbine motors hold a 35% share in 2025, reflecting the global shift toward renewable energy generation.

- Leading Capacity: Large turbines above 100 MW capture 45% market share, playing a key role in utility-scale power generation.

- Leading End-Use: Energy and utilities dominate with a 50% share, supported by the accelerating adoption of clean energy infrastructure worldwide.

- Key Developments: In 2024, Andritz completed the modernization of 96.4 MW units at Nigeria’s Jebba hydropower plant, while global turbine manufacturers shifted focus to standardized designs to reduce costs and improve delivery.

|

Global Market Attribute |

Key Insights |

|

Turbine Motor Market Size (2025E) |

US$2.7 Bn |

|

Market Value Forecast (2032F) |

US$4.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.9% |

Increasing investments in clean energy infrastructure, coupled with technological advancements in turbine efficiency and digital monitoring, are boosting reliability and reducing operational costs. Expanding power demand in both developed and emerging economies further accelerates installations, positioning turbine motors as a key enabler of sustainable energy transitions and long-term global energy security.

Market Dynamics

Driver: Rising Demand for Renewable Energy and Technological Advancements

The turbine motor market is witnessing robust growth, driven by the rising global demand for renewable energy. For instance, the Ministry of New & Renewable Energy in India reports that the country has achieved nearly 70-80% domestic manufacturing of wind turbine generators, with an annual production capacity of around 18,000 MW. This government-backed indigenisation strengthens local supply chains and creates significant opportunities for turbine motor manufacturers to support the expansion of renewable energy projects worldwide.

At the same time, technological advancements in turbine motors are accelerating market growth by improving efficiency, reliability, and scalability. Innovations in turbine design, digital monitoring, and energy optimization are making turbine motors more cost-effective and better suited for large-scale deployment. These developments ensure that turbine motors remain central to the clean energy transition, reinforcing their adoption across global renewable energy infrastructure.

Restraint: High Initial Costs and Supply Chain Challenges

The expansion of the turbine motor market faces a major restraint due to the high initial costs involved in manufacturing, installation, and maintenance. Advanced turbine motors require significant capital investment in precision engineering, composite materials, and digital control systems.

According to the International Renewable Energy Agency (IRENA), onshore wind power projects typically require upfront investments between USD 1.3 million and 2.2 million per MW. In contrast, offshore wind projects often exceed USD 3 million per MW. Such substantial expenditure poses a barrier, particularly in developing economies where funding mechanisms and subsidies are less accessible, thereby slowing large-scale adoption despite growing renewable energy goals.

Adding to the challenge are supply chain disruptions that directly impact turbine motor production and deployment. Global shortages of steel and rare-earth materials, coupled with rising transportation costs and logistics delays, have inflated project budgets. The International Energy Agency notes that these supply chain pressures have driven renewable project costs upward by 15-20% in recent years, limiting profitability and delaying installations.

Opportunity: Expansion of Offshore Wind and Emerging Markets

The turbine motor market is poised to benefit significantly from the expansion of offshore wind projects, which are gaining momentum due to strong government support and increasing investments in clean energy. Offshore wind farms offer higher capacity factors compared to onshore, providing more consistent power output and creating strong demand for advanced turbine motors capable of operating in challenging marine environments.

The International Energy Agency projects that global offshore wind capacity could reach 500 GW by 2040, making it a central pillar of the renewable energy transition. This rapid expansion creates a lucrative opportunity for turbine motor manufacturers to develop specialized, high-performance solutions tailored for offshore applications.

At the same time, emerging markets in the Asia Pacific, Latin America, and Africa are accelerating their renewable energy initiatives, presenting vast untapped potential for turbine motor adoption. With countries such as Vietnam, Brazil, and South Africa rolling out ambitious wind power targets, demand for reliable turbine motors is set to surge. These regions offer cost-competitive labor, supportive policies, and rising energy needs, positioning them as growth hotspots for global manufacturers.

Category-wise Insights

Motor Type Insights

The turbine motor market in 2025 is led by wind turbine motors, which account for 35% of the total share. Their dominance is attributed to the accelerating global transition toward renewable energy and the rising adoption of large-scale wind power projects. According to the Global Wind Energy Council, wind turbine installations have increased by nearly 20% since 2020, highlighting the steady momentum in this segment as countries expand their clean energy capacity.

Meanwhile, hydraulic turbine motors are emerging as the fastest-expanding type, supported by growing investments in small and medium hydropower projects across Asia and Africa. In 2024, hydraulic turbine sales rose by 18%, reflecting their efficiency and adaptability in regions with abundant water resources and increasing electricity demand.

Capacity Insights

In 2025, large turbines above 100 MW dominate, holding a 45% share. These turbines play a pivotal role in utility-scale power generation, especially within the energy and utilities sector. Their demand is driven by the rising need for high-capacity solutions in both wind and hydroelectric projects, which are central to meeting national renewable energy targets and ensuring grid stability.

On the other hand, medium turbines ranging from 10 to 100 MW represent the fastest-expanding category. Their adaptability for industrial use and small-scale renewable projects makes them highly attractive in developing markets. Sales of medium turbines grew by 15% in 2024, with particularly strong uptake in the Asia Pacific region, where governments are actively supporting mid-scale renewable energy development.

End-use Insights

In 2025, the energy and utilities sector dominates with a 50% share, supported by large-scale investments in renewable energy infrastructure. This segment remains the backbone of demand, driven by the expansion of wind and hydropower projects worldwide. In 2024, turbine installations for these projects increased by 20%, underscoring the vital role of energy and utilities in the adoption of advanced turbine motors.

The aerospace sector has emerged as the fastest-growing end-use segment, fueled by rising demand for gas turbine motors in both commercial and defense aviation. Industry data indicates that turbine motor demand in aerospace rose by 22% in 2024, reflecting the global rebound in air travel and continued investments in next-generation aircraft technologies.

Regional Insights

North America Turbine Motor Market Trends

In 2025, North America accounts for 33% of the turbine motor market, led by the United States and Canada. The U.S. drives most of the demand, supported by major investments in wind energy and aerospace, with the Department of Energy noting more than 45 GW of new wind capacity added since 2020.

Canada’s market strength comes from hydropower, where hydraulic turbine installations increased by 15% in 2024. The region’s growth is further encouraged by strict environmental regulations and supportive policies, including the U.S. Production Tax Credit, which has boosted renewable energy adoption by 18% since 2022. Together, these factors ensure North America remains a key hub for turbine motor demand across energy, utilities, and industrial applications.

Europe Turbine Motor Market Trends

In 2025, Europe holds a significant share of the turbine motor market, supported by long-established wind and hydropower infrastructure. Countries such as Germany, Denmark, and Spain continue to lead in wind energy deployment, while France and the Nordic nations strengthen demand through large-scale hydropower projects.

The European Union’s commitment to achieving carbon neutrality by 2050, combined with policies under the Green Deal and Renewable Energy Directive, has accelerated the adoption of advanced turbine technologies. In 2024, wind capacity additions across Europe increased by 14%, while hydropower upgrades also contributed to steady growth. These initiatives highlight Europe’s strong position as a mature yet expanding market for turbine motors in both renewable energy and industrial applications.

Asia Pacific Turbine Motor Market Trends

In 2025, the Asia Pacific region is the fastest-growing region in the turbine motor market, driven by rising energy demand and large-scale renewable projects. China and India lead the region with major wind and hydropower expansions, supported by strong government targets and manufacturing capacity.

According to regional energy agencies, wind installations in the Asia Pacific region grew by over 20% between 2020 and 2024, while hydropower projects in countries such as Vietnam and Indonesia have steadily boosted demand for hydraulic turbines. Rapid industrialisation and urbanisation further fuel the need for reliable power generation, making turbine motors critical to meeting future energy requirements. With sustained investments and supportive policies.

Competitive Landscape

The global turbine motor market is moderately consolidated, with a few major companies accounting for a large share of global revenue. Competition is driven by innovation in high-capacity wind and hydropower turbines, efficiency improvements, and sustainable manufacturing practices.

In 2024, the top five participants collectively held nearly 65% market share, supported by strong R&D investments and regional expansion strategies. Smaller firms are increasingly targeting niche applications and emerging markets, intensifying competition while widening product offerings across the sector.

Key Developments

- November 2024: A leading European energy firm narrowed fourth-quarter operating losses and lifted its mid-term outlook, supported by strong power equipment demand and recovery in the wind turbine segment.

- 2024: Andritz completed the modernization of multiple 96.4 MW units at Nigeria’s Jebba hydropower plant, boosting efficiency, reliability, and extending service life.

- May 2024: Global wind turbine manufacturers shifted strategy from scaling up turbine size to standardizing proven models, aiming to cut costs, improve logistics, and accelerate delivery.

Companies Covered in Turbine Motor Market

- Andritz AG (Austria)

- General Electric (U.S.)

- Mitsubishi Hitachi Power Systems (U.S.)

- Siemens Gamesa (Spain)

- Toshiba Hydroelectric Power (Japan)

- Vestas Wind Systems (Denmark)

- Canyon Industries (U.S.)

- Voith GmbH & Co. Kgaa (Germany)

- Kirloskar Brothers Ltd. (India)

- Arani Power (India)

- Turbocam (U.S.)

- Gilbert Gilkes & Gordon Ltd. (U.K.)

- Others

Frequently Asked Questions

The turbine motor market is projected to reach US$2.7 Bn in 2025, driven by renewable energy demand and technological advancements.

Key drivers include the shift to renewable energy, government incentives, and rising energy demands from urbanization.

The turbine motor market will grow from US$2.7 Bn in 2025 to US$4.5 Bn by 2032, with a CAGR of 7.4%.

Opportunities include offshore wind expansion, emerging market growth, and modular turbine innovations.

Leading players include Andritz AG, General Electric, Mitsubishi Hitachi Power Systems, Siemens Gamesa, and Vestas Wind Systems.