- Specialty & Fine Chemicals

- Cutting Oils Market

Cutting Oils Market Size, Share, and Growth Forecast, 2026 - 2033

Cutting Oils Market by Product Type (Neat Cuttings Oils, Water-Soluble Cuttings Oils), Application (Machining, Grinding, Milling, Drilling), End-User (Automotive, Aerospace, Defense), and Regional Analysis for 2026 - 2033

Cutting Oils Market Share and Trends Analysis

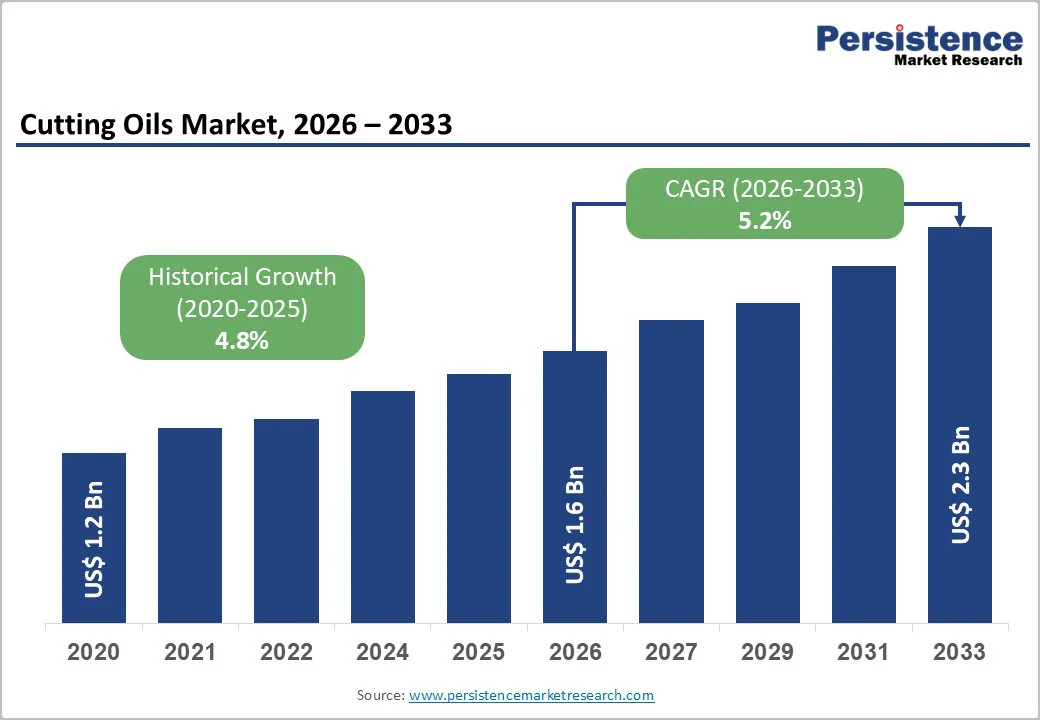

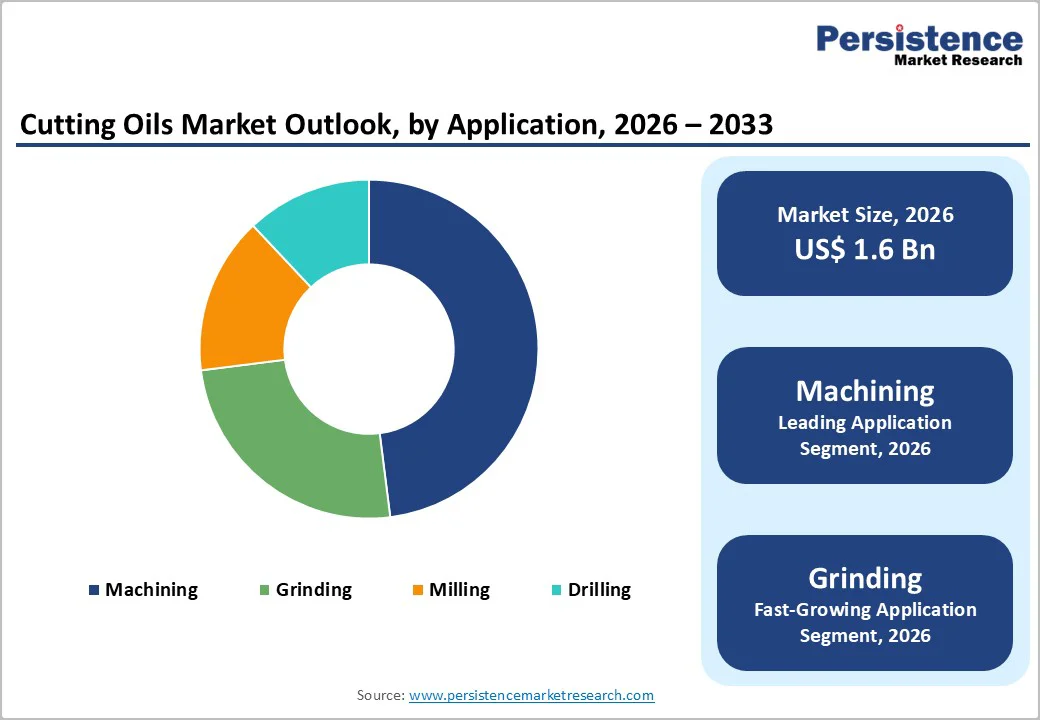

The global cutting oils market size is likely to be valued at US$ 1.6 billion in 2026, and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026−2033. Accelerating industrial manufacturing activities across automotive and aerospace sectors, where precision machining operations demand advanced metalworking fluids, is the primary growth determinant for the market.

Growing emphasis on extending tool life and improving surface finish quality in metal cutting operations continues to fuel adoption. Stricter workplace safety regulations and environmental compliance requirements are also prompting manufacturers to invest in bio-based and synthetic cutting oil formulations that deliver superior performance while minimizing health and environmental risks.

Key Industry Highlights

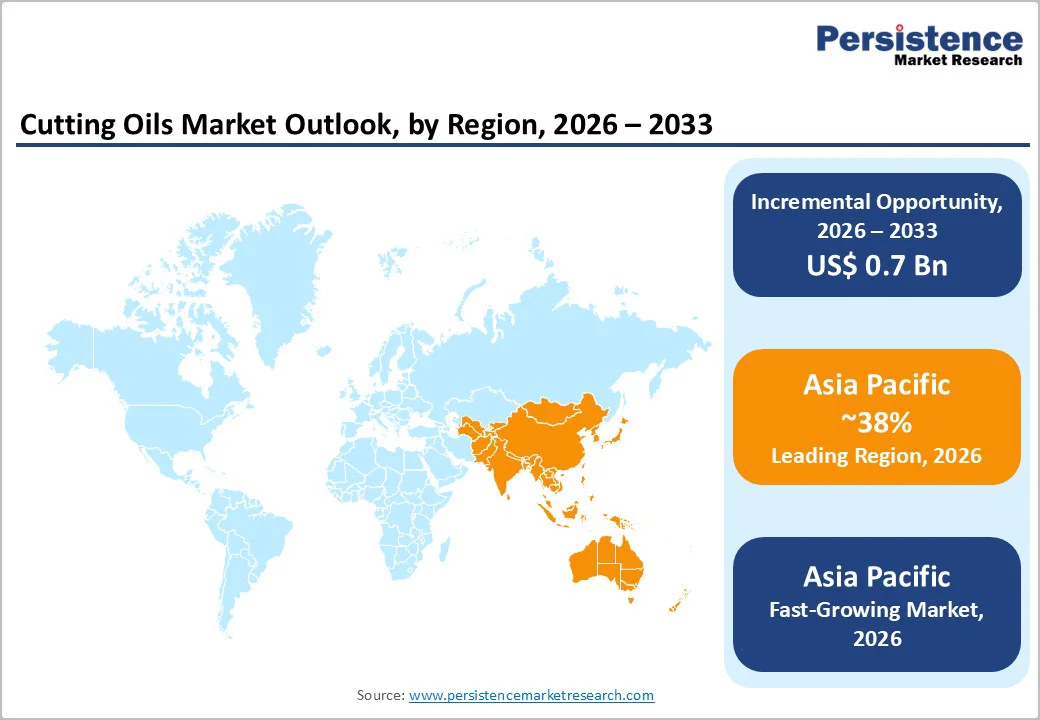

- Dominant Region: Asia Pacific is expected to command about 38% market share in 2026, supported by a robust manufacturing base spanning core sectors.

- Fastest-growing Market: The Asia Pacific market is anticipated to be the fastest-growing through 2033, on account of large-scale infrastructure investments.

- Leading & Fastest-growing Product Type: Neat cuttings oils are set to lead with about 58% in 2026, while water-soluble cuttings oils are likely to grow the fastest during the 2026-2033 forecast period.

- Application Dominance: Machining is slated to dominate with a projected 40% share in 2026, with grinding posting the highest 2026-2033 CAGR.

- Market Drivers: Expansion of global manufacturing infrastructure and widespread industrial automation are emerging as the central growth catalyzers for the market.

| Key Insights | Details |

|---|---|

|

Cutting Oils Market Size (2026E) |

US$ 1.6 Bn |

|

Market Value Forecast (2033F) |

US$ 2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Global Manufacturing Infrastructure and Industrial Automation

Global manufacturing expansion and industrial automation drive strong demand for advanced cutting oils. Automotive, aerospace, and heavy machinery sectors scale high-speed machining and computer numerical control (CNC) operations to boost output and precision. These environments demand fluids that deliver superior lubrication, cooling, and tool safeguarding under intense heat and pressure. Manufacturers evolve cutting oils into essential components for consistent production. Operators should select formulations that match specific machine loads and materials to cut tool wear by up to 30 percent and extend service intervals.

The automotive shift to electric vehicles (EVs) has redefined fluid needs with extensive use of aluminum alloys and composites. Producers require stable viscosities, foam resistance, and efficient chip evacuation for flawless surfaces. Aerospace applications demand even tighter tolerances and longer tool life. Tailored cutting oils minimize interruptions and enhance efficiency. End-users gain by partnering with suppliers who offer customized blends and performance testing, ensuring alignment with production goals and sustainability targets.

Health Concerns and Disposal Challenges Associated with Metalworking

Health concerns and end-of-life handling requirements can restrain adoption of cutting oils, even as formulations improve. In several machining cells, workers can encounter skin irritation, dermatitis, or breathing discomfort when oil mist accumulates in enclosed areas, and therefore, plants need disciplined occupational health and safety (OHS) controls that reduce contact and airborne concentrations. Practical steps include using local exhaust ventilation, enclosing high-splash operations, selecting low-mist products, and enforcing personal protective equipment (PPE) protocols, while also tracking fluid condition to limit harmful degradation by-products. These actions also help organizations contain compliance effort, lower incident risk, and avoid avoidable legal or insurance costs.

Environmental obligations add another layer of complexity because used metalworking fluids often contain metal fines, tramp oil, and process residues that require controlled collection and treatment before disposal. When companies treat this stream as a managed process rather than a maintenance afterthought, they can reduce cost volatility by standardizing segregation, filtration, and recycling pathways, and by documenting chain-of-custody with certified waste partners. This pressure also explains the growing interest in process changes such as dry machining and minimum quantity lubrication (MQL), which can cut fluid consumption and shrink waste volumes in suitable operations.

Rapid Industrialization and Infrastructure Development in Emerging Economies

Rapid urbanization in developing economies with massive infrastructure projects have catalyzed the cutting oils market expansion. National authorities across Asia Pacific and the Middle East are aggressively industrializing through dedicated special economic zones (SEZs). These clusters host diverse facilities such as heavy machinery or aerospace manufacturing plants which depend upon reliable fabrication processes. Strategic planners should view these emerging hubs as vital centers for high-volume intake.

Major economies, including China and India, are transitioning from basic assembly toward complex, high-value engineering. This evolution increases reliance on sophisticated metalworking fluids that deliver superior tool life alongside flawless surface finishes. Organizations must establish robust domestic supply chains for satisfying the deepening requirements of local enterprise ecosystems. Developing technical service capabilities early allows firms to secure loyal customers before the landscape becomes saturated. Investors who prioritize localized distribution using bespoke support will likely capture the greatest long-term rewards within shifting global business environments.

Category-wise Analysis

Product Insights

Neat cuttings oils are poised to lead with approximately 58% of the market revenue share in 2026. Neat cutting oils, also called straight oils, are undiluted oil-based products typically made from mineral or highly refined base oils blended with extreme-pressure (EP), anti-wear, and lubricity additives. They deliver maximum lubricity and strong boundary protection, making them ideal for heavy-duty operations like tapping, broaching, gear cutting, and machining difficult alloys where tool life and surface integrity are critical. Widely used in traditional job shops, general engineering, and automotive/heavy machinery segments optimized for straight-oil systems.

Water-soluble cuttings oils are likely to be the fastest-growing segment during the 2026-2033 forecast period, due to their support for higher cutting speeds, superior heat dissipation, cleaner equipment, and easier environmental management compared to straight oils. Tightening EHS regulations such as REACH in Europe and OSHA/EPA guidelines in North America, along with original equipment manufacturer (OEM) demands for reduced mist, lower volatile organic compounds (VOCs), and simpler waste handling, are driving adoption of semi-synthetic and synthetic variants, particularly in automotive, aerospace, and precision machining applications. Water-soluble cutting oils, also known as soluble oils, semi-synthetics, and synthetic water-miscible fluids, are concentrates mixed with water to create emulsions or clear solutions.

Application Insights

Machining is slated to dominate with a projected 40% of the cutting oils market revenue share in 2026. This application supports high-volume production of automotive components, shafts, housings, industrial parts, and structural elements using CNC lathes, multi-axis machines, and versatile machining centers. Neat oils excel here for their superior lubricity in moderate-to-severe conditions, while water-soluble emulsions provide essential cooling for sustained high feeds, speeds, and continuous operations. Machining's leadership stems from its ubiquity across automotive manufacturing, general engineering, machinery production, and job shops, where consistent tool life, reliable throughput, and cost-effective performance are prioritized over specialized finishing or precision requirements.

Grinding is expected to be the fastest-growing segment during 2026-2033 forecast period, driven by precision demands in aerospace turbine blades, automotive bearings, and medical implants. Water-soluble fluids dominate due to their superior cooling, which prevents thermal damage, inhibits wheel loading, and enables clean rinsing for micron-level finishes. Rising adoption of high-speed super-abrasive wheels (CBN, diamond) and automated grinding cells accelerates demand for low-foam, high-cleanliness formulations. Growth is fueled by aerospace expansion and quality standards (AS9100, ISO 13485) that mandate defect-free surfaces.

End-User Insights

Automotive is set to lead with an approximate 42% of the market revenue share in 2026. This dominance reflects the automotive industry's massive metalworking intensity, as typical passenger vehicle production requires machining of engine blocks, cylinder heads, transmission components, suspension parts, and drivetrain elements. Despite electric vehicle adoption trends reducing certain powertrain components, substantial machining requirements persist for electric motor housings, battery enclosures, chassis components, and structural elements. Major automotive manufacturers operate extensive machining facilities, with leading OEMs purchasing cutting oils in large volumes annually through centralized procurement programs.

Aerospace is anticipated to be the fastest-growing segment during the 2026-2033 forecast period. This exceptional growth is driven by expanding commercial aircraft production backlogs, with major manufacturers like Boeing and Airbus maintaining substantial order books that extend years into the future. Aerospace components require extensive machining of difficult-to-machine materials, including titanium alloys, Inconel superalloys, and aluminum-lithium alloys—all demanding specialized cutting oil formulations with extreme-pressure additives and superior thermal stability. Critical components such as turbine disks, structural forgings, and landing gear elements require precision machining with tightly controlled surface integrity.

Regional Insights

Asia Pacific Cutting Oils Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for cutting oils in 2026, accounting for approximately 38% of the cutting oils market share. The region is an important demand center for cutting oils, supported by a deep and diversified manufacturing base spanning the automotive, machinery, electronics, and industrial equipment sectors. China anchors regional consumption as the leading automotive producer and a dominant hub for engineered products, while Japan contributes substantial demand through its advanced automotive, precision machinery, and machine tool industries. India is emerging as the fastest-growing market in the region, underpinned by expanding vehicle production, government-led manufacturing initiatives, and rapidly developing aerospace capabilities. In parallel, key ASEAN economies such as Thailand, Indonesia, and Vietnam are scaling up industrial capacity and attracting sustained foreign direct investment in metalworking-intensive industries.

Regional growth is reinforced by the ongoing expansion of manufacturing capacity, large-scale infrastructure investment, and a shift toward higher value-added, export-oriented production. The automotive and aerospace sectors are particularly important, as domestic commercial aircraft programs and defence aviation buildouts require sophisticated metalworking fluid technologies. The adoption of advanced CNC machining, automated production lines, and precision engineering raises performance requirements for cutting oils, increasing demand for higher-specification formulations. Regulatory frameworks are also tightening, especially in China and Japan, which is driving greater emphasis on environmental compliance and worker safety. Competition involves both global manufacturers with localized plants and agile regional suppliers, while technology transfer and localization efforts are strengthening domestic formulation capabilities and allowing regional players to gain market share through competitive pricing and responsive technical support.

Europe Cutting Oils Market Trends

Europe serves as a key demand center for cutting oils, underpinned by its leadership in automotive manufacturing, machine tool production, and precision engineering across multiple industrial sectors. Germany dominates regional consumption through its automotive industry, which produces premium vehicles and components that require high-performance fluids, while the United Kingdom contributes significantly via aerospace manufacturing, particularly commercial aircraft wing production and engine machining. France supports demand through its diversified base in automotive, aerospace, and defense applications, complemented by Spain’s growing automotive production footprint. This balanced industrial structure sustains consistent demand for advanced cutting oils tailored to strict quality and performance standards.

Regional expansion is driven by the strength of the aerospace sector, where major aircraft programs require qualified fluids that meet rigorous performance specifications, alongside excellence in machine tool manufacturing that generates both captive and end-user demand. Precision engineering priorities and stringent manufacturing quality standards support premium positioning for synthetic and bio-based formulations. The transition to electric vehicles has mixed implications, as reduced traditional powertrain machining is offset by growing requirements for electric motors, battery enclosures, and lightweight structural components. Regulatory frameworks, including comprehensive chemical safety regulations and circular economy initiatives, set global benchmarks while accelerating the adoption of sustainable fluids through incentives and strict workplace safety limits on mist exposure. The competitive environment combines large European-based global suppliers with specialized regional players, all of whom are responding to corporate sustainability mandates that prioritize renewable formulations and lower environmental impact.

North America Cutting Oils Market Trends

The North America cutting oils market plays a strategically important role in the global landscape, supported by a large and technologically advanced manufacturing base. The United States drives majority of the regional demand through its extensive automotive, aerospace, industrial machinery, and medical device production, while Mexico adds momentum through integrated automotive manufacturing and machining activities linked to North American supply chains. High-value applications in aerospace and medical devices are particularly influential, as they require stringent quality control, tight tolerances, and sophisticated metalworking fluids capable of handling difficult-to-machine materials such as titanium and superalloys. Defense modernization programs, including combat aircraft, naval platforms, and precision components, further reinforce steady demand for qualified high-performance cutting oils.

Market development is also shaped by a robust innovation ecosystem and stringent regulatory environment. Leading manufacturers in the region invest heavily in research focused on bio-based chemistries, nano-enhanced formulations, and Industry 4.0-compatible fluid monitoring and management solutions. Environmental regulations targeting emissions and waste, along with workplace safety requirements governing exposure to metalworking fluids, are accelerating the shift toward low-emission, safer, and more sustainable products. This regulatory pressure supports adoption of advanced filtration, recycling, and conditioning technologies. Competitive dynamics feature a mix of major global suppliers and specialized regional players, while growing investment interest in sustainable manufacturing and smart fluid management positions North America as an innovation leader, even as volume growth remains more moderate than in emerging regions.

Competitive Landscape

Leading companies such as Quaker Houghton, Fuchs Petrolub SE, BP Castrol, Chevron Corporation, and TotalEnergies dominate the moderately consolidated global cutting oils market structure. These firms excel through superior product formulations, extensive research and development (R&D) investments, broad distribution networks, and value-based pricing strategies. They address end-user priorities by creating fluids that enhance tool durability, process stability, and material compatibility in demanding applications. Buyers should partner with these providers to access proven innovations that reduce total cost of ownership and support regulatory adherence.

Competitive advantages increasingly center on sustainability credentials and compliance with tightening environmental standards. Organizations that pioneer low-toxicity, biodegradable cutting oils gain preference among forward-thinking manufacturers. Regional challengers must differentiate via localized service models and rapid customization. Suppliers benefit by offering bundled solutions that include fluid management programs, performance audits, and recycling partnerships, thereby locking in customer loyalty and capturing premium margins in a maturing landscape.

Key Industry Developments

- In December 2025, Halocarbon launched three PCTFE-based metalworking fluids on its InfinX e-commerce platform for demanding CNC machining in aerospace, defense, and automotive sectors. These non-flammable, inert formulations boost throughput 20X, extend tool life 5X, cut forces 50%, and improve finishes by 200% on tough alloys. They integrate seamlessly with MQL systems, reducing costs and enhancing quality.

- In May 2025, PETRONAS Lubricants International (PLI) and Quaker Houghton formed a strategic partnership to expand their industrial fluids offering in Malaysia and India. PLI will exclusively distribute Quaker Houghton’s metalworking fluids in Malaysian transportation and industrial markets, while Quaker Houghton will supply PLI’s maintenance lubricants and industrial fluids to steel mill customers in India, aiming to enhance product availability, service quality, and support modern manufacturing needs.

- In May 2025, Clariant showcased its Hostagliss™ synthetic metalworking fluids at Inter Lubric 2025 in Shanghai, highlighting Hostagliss SEE, Hostagliss 1520, and Hostagliss LS for water-based applications. These self-emulsifying esters offer stable emulsions, hard water tolerance, low foam, and superior lubrication to cut emulsifier use and boost efficiency in modern machining.

Companies Covered in Cutting Oils Market

- Quaker Houghton

- Fuchs Petrolub SE

- BP Castrol

- TotalEnergies

- Chevron Corporation

- Shell Lubricants

- Indian Oil Corporation Limited

- Blaser Swisslube AG

- PETROFER Chemie

- Cimcool Industrial Products

- Henkel AG

- Exxon Mobil Corporation

- Sinopec Lubricant Company

- Master Chemical Corporation

Frequently Asked Questions

The global cutting oils market is projected to reach US$ 1.6 billion in 2026.

Expanding manufacturing automation, automotive/aerospace production growth, and stringent environmental regulations demanding advanced formulations are driving the market.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Industrialization of developing economies, formulation of bio-based sustainable fluids, and Industry 4.0 fluid management integration represent major growth opportunities.

Quaker Houghton, Fuchs Petrolub SE, BP Castrol, Chevron Corporation, and TotalEnergies are some of the key players in the market.