- Communication Infrastructure & Services

- Coatings and Application Technologies for Robotics Market

Coatings and Application Technologies for Robotics Market Size, Share, and Growth Forecast, 2026-2033

Coatings and Application Technologies for Robotics Market by Coating Technology (Spray Coating, Powder Coating, Electrostatic Coating, Plasma Coating, Automated Robotic Coating Cells), Robot Type (Industrial Robots, Collaborative Robots, Autonomous Mobile Robots, Surgical Robots), End-Use Industry (Automotive Manufacturing, Electronics & Semiconductor Assembly, Aerospace & Defense, Healthcare & Medical Devices), and Regional Analysis for 2026-2033

Coatings and Application Technologies for Robotics Market Share and Trends Analysis

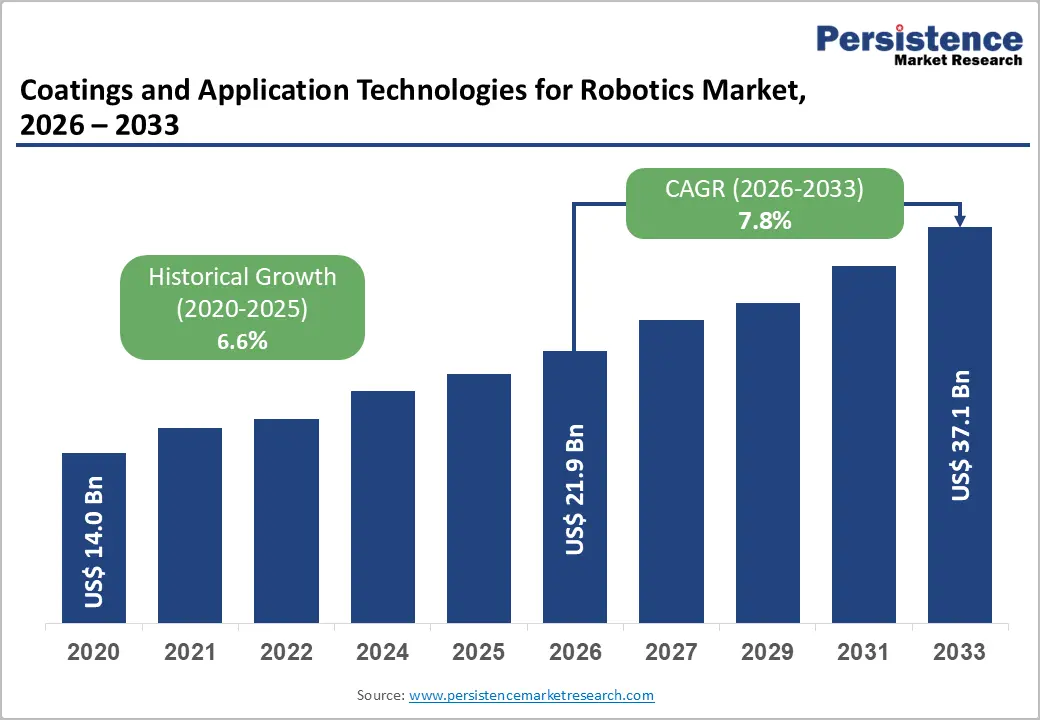

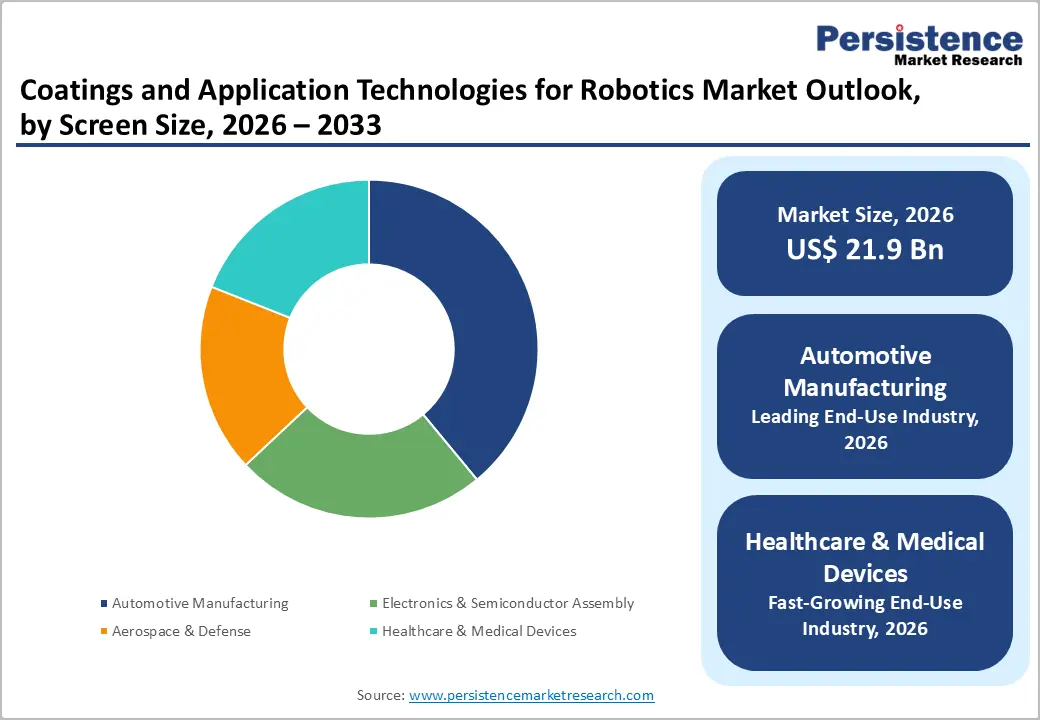

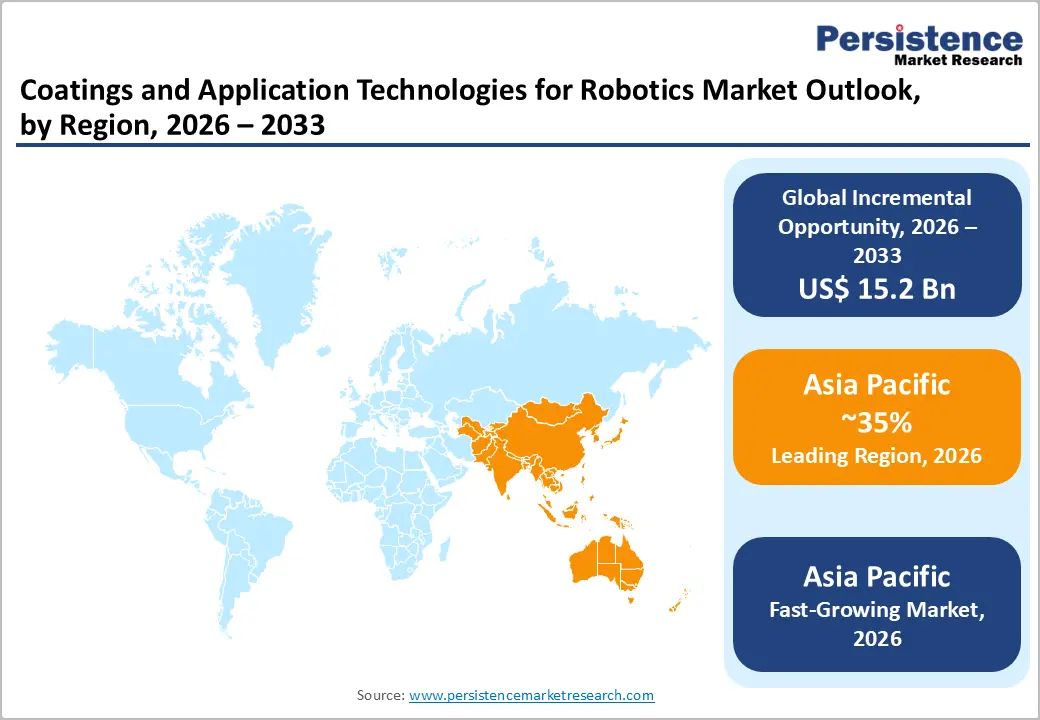

The global coatings and application technologies for robotics market size is likely to be valued at US$ 21.9 billion in 2026 and is projected to reach US$ 37.1 billion by 2033, growing at a CAGR of 7.8% during the forecast period 2026–2033.

This growth trajectory is supported by the accelerating adoption of automation across manufacturing and service sectors, as companies increasingly integrate advanced robotic systems to enhance operational efficiency. Rising investments in precision robotics enable high-quality coating applications that improve durability, corrosion resistance, and performance consistency, particularly in automotive, electronics, aerospace, and healthcare industries. Manufacturers prioritize robots that deliver repeatable results with minimal human intervention, ensuring faster throughput and reduced operational errors. The stringent environmental regulations and sustainability initiatives encourage the adoption of eco-friendly coatings, including low-volatile organic compound (VOC), water-based, and UV-cured solutions, further expanding market demand and technological innovation.

Key Industry Highlights

- Dominant End-Use Industries: Automotive manufacturing is set to command around 39% revenue share in 2026, while healthcare and medical devices are likely to grow the fastest at about 10.4% CAGR through 2033, driven by precision coating requirements.

- Leading Coating Technologies: Spray coating is expected to lead with approximately 38% share in 2026, while automated robotic coating cells are projected to grow the fastest during 2026–2033, reflecting rising demand for high-precision applications.

- Robot Type Leadership: Industrial robots are poised to hold around 43% of the market in 2026, while collaborative robots are likely to grow the fastest through 2033, owing to flexible deployment and safe human-robot interaction.

- Regional Leadership: Asia Pacific is expected to dominate with an estimated 35% share in 2026 and register 8.5% CAGR through 2033, led by smart factory investments and government incentives in China, Japan, and India.

- Innovation Focus: Advanced materials, eco-friendly formulations, and AI-integrated application technologies are driving growth, with sustainable and low-VOC coatings gaining rapid adoption across sectors.

| Key Insights | Details |

|---|---|

|

Coatings and Application Technologies for Robotics Market Size (2026E) |

US$ 21.9 Bn |

|

Market Value Forecast (2033F) |

US$ 37.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Widening Adoption of Automation and Robotics Worldwide

The global shift toward industrial automation has significantly increased the deployment of robotic systems across manufacturing and service sectors. Industrial robots and advanced collaborative robots (cobots) are now widely used to enhance operational efficiency, precision, and throughput in coating and finishing processes. Manufacturers invest in these systems to achieve higher productivity while maintaining consistent quality standards. Worldwide industrial robot installations exceeded 542,000 units in 2024, reflecting sustained global demand. Asia accounted for 74% of new deployments, highlighting regional adoption momentum. Strategic initiatives in Japan, including the RING Project and mass-production plans for humanoid robots, further emphasize government-backed automation expansion.

Coatings and application technologies play a critical role by protecting robotic platforms from abrasion, corrosion, and extreme operational conditions, reducing maintenance needs and extending service life. Industry movements, such as SoftBank’s acquisition of ABB’s robotics division, reinforced the adoption of collaborative and smart robotics. The automotive, electronics, and aerospace industries show particularly strong uptake due to stringent requirements for uniform surface finishes and consistent performance. The need for repeatable, high-precision coating processes has become a key driver for ongoing automation investments across global manufacturing hubs.

Technological Advancements in Coating Materials and Application Technologies

Innovations in material science and robotic application systems are transforming the capabilities of coatings for industrial robots. Developments in nano-engineered coatings, low-VOC and eco-friendly formulations, self-healing materials, and UV-cured systems have improved resistance to wear, chemicals, and extreme temperatures. These technologies enhance robot longevity and performance while helping manufacturers comply with environmental regulations and reduce operational costs. AI integration, advanced motion control, and sensor-based systems introduced in 2025–2026 enable highly accurate, automated coating applications with minimal human intervention.

On the application side, electrostatic spray systems, plasma deposition tools, and precision powder-coating robots deliver consistent, repeatable surface finishes with minimal waste. Industry adoption of AI-enabled robots and the growing deployment of collaborative robots reflect broader trends in flexible, high-precision automation. Global robotics conferences in 2026 highlighted these technological breakthroughs, signaling the rapid adoption of innovation. These advances collectively reduce the total cost of ownership, expand possible applications, and position manufacturers to capitalize on new market opportunities across automotive, aerospace, electronics, and medical device industries.

High Initial Capital Investment and Integration Costs

The adoption of advanced robotic coating technologies requires substantial capital investment to acquire sophisticated equipment, integrate systems into existing production lines, and train skilled personnel. Small and medium-sized enterprises (SMEs) face significant barriers due to high upfront costs and extended payback periods, which can restrict adoption in price-sensitive regions. High financing requirements and limited access to affordable credit further exacerbate these challenges, particularly for smaller manufacturers looking to modernize production capabilities.

Integration challenges, including ensuring compatibility with legacy machinery, programming customized coating sequences, and adapting systems for varying product dimensions, can delay deployment and increase operational complexity. The shortage of skilled robotics technicians and integration specialists in 2025–2026 further raises costs and extends rollout timelines, especially for SMEs. These factors collectively limit near-term uptake, making capital and integration requirements a critical restraint for sustained growth in the robotic coatings market.

Supply Chain and Materials Constraints

The market for advanced coating solutions relies heavily on specialized raw materials, including resins, pigments, rare earth metals, and high-performance polymers. The global shortages of rare earth elements, copper, and battery metals have affected robotics and manufacturing supply chains, raising costs and delaying equipment production. Supply volatility has highlighted the vulnerability of global manufacturing networks, reinforcing the need for strategic sourcing and inventory management.

Geopolitical tensions, tariff volatility, and shipping bottlenecks have further amplified these supply chain vulnerabilities, forcing manufacturers to adapt procurement strategies and extend lead times. Rising freight costs and complex customs procedures contribute to uncertainty in production planning and pricing for coatings and robotic systems. These constraints can slow market expansion, impact delivery schedules, and pose long-term risks for stakeholders seeking consistent, high-precision manufacturing outputs.

Expansion into Emerging Economies and Smart Factory Integration

Emerging markets in the Asia Pacific, Latin America, and the Middle East are rapidly industrializing and adopting automation to enhance manufacturing competitiveness. China’s government-led smart factory initiatives have driven local deployment of robotics and advanced coating technologies across automotive, electronics, and appliance production hubs. India’s Production Linked Incentive (PLI) schemes in the electronics and automotive sectors are also enabling the deployment of robotics to improve precision, productivity, and scalability. These macroeconomic and policy trends are creating new revenue opportunities for system integrators, coating suppliers, and automation service providers targeting untapped demand.

Recent developments further reinforce this trajectory, including government-backed investments in robotics infrastructure and incentives to increase industrial productivity. ASEAN nations are collaborating on digitalization roadmaps offering subsidies for automation technologies, supporting wider uptake among small and medium enterprises. The integration of AI-enabled robotics, smart coating cells, and connected manufacturing solutions is reducing operational barriers and unlocking larger investments. Collectively, these factors present a strategic opportunity for businesses to expand into high-growth markets with advanced, automated coating solutions.

Growth of Sustainable and Eco-Friendly Coating Solutions

The rising regulatory pressure to reduce VOC emissions and promote sustainable manufacturing has created significant demand for eco-friendly coating technologies. Policies such as updated U.S. Environmental Protection Agency (EPA) VOC standards and the European Union (EU) REACH VOC restrictions are accelerating the adoption of water-based, UV-cured, and low-emission formulations compatible with robotic application systems. These mandates encourage manufacturers to transition away from traditional solvent-heavy technologies, creating demand for greener alternatives that reduce environmental impact while maintaining performance standards.

Industry movements such as RadTech’s BIG IDEAS for UV+EB Technology 2026 highlight energy-efficient, next-generation coatings aligned with global sustainability goals. Adoption of recyclable, biodegradable, and low-emission formulations enables companies to comply with evolving supply-chain and ESG requirements while creating premium market segments. Integration of these solutions with AI-enabled and precision robotic systems supports high-quality applications, minimizes waste, and strengthens corporate sustainability strategies. This dual focus on environmental compliance and advanced technology offers profitable opportunities for innovation-driven suppliers.

Category-wise Analysis

Coating Technology Insights

Spray coating is likely to dominate, with an estimated 38% share of the coatings and application technologies for robotics market revenue in 2026, widely adopted across Toyota, Volkswagen, and Tesla assembly lines for high-volume automotive painting, industrial robot finish work, and electronics enclosure coatings. Robotic spray booths equipped with Fanuc LR Mate 200iD and Yaskawa Motoman systems enhance precision, reduce overspray, and improve workplace safety by controlling VOC exposure.

In 2025, Ford’s Michigan Assembly Plant reported significant consistency gains using automated spray cells, reducing rework and boosting throughput. Spray technology supports solvent-borne, water-based, and UV-cured coatings, and integrates with AI-enabled predictive quality systems for real-time finish monitoring. Regulatory emphasis on EPA VOC limits and EU REACH further drives adoption, as automated controls meet stringent emission standards and improve operational compliance.

Automated robotic coating cells are projected to grow at a 9.1% CAGR through 2033, driven by precision systems such as Nordson EFD robotic applicators and Nordson’s ProBlue™ automated platforms that enable consistent, high-quality coatings with minimal human input. Manufacturers deploying integrated ABB coating robots with advanced sensor feedback achieved tighter process control and reduced material waste, thereby supporting complex automotive, aerospace, and medical applications. These systems merge AI-driven motion control with real-time monitoring, enabling seamless transitions between part types and reducing changeover times.

Integration with Industry 4.0 connectivity solutions supports predictive maintenance and enhanced quality assurance. As manufacturers pursue leaner, data-driven production, automated cells are becoming essential for scaling coating operations across diverse product lines.

End-Use Industry Insights

The automotive sector is expected to hold about 39% of the coatings for robotics market in 2026, driven by extensive robotic use in painting and surface treatment on high-volume lines at Toyota, GM, and BMW plants. Robots such as KUKA KR-10 PA and Dürr EcoRP spray systems support body-in-white painting and multi-layer sealant applications with consistent quality and repeatability. In 2025, Tesla’s Gigafactory Texas expanded its automated painting cells, reducing finish defects and cycle times while improving environmental compliance.

Adoption of precision measurement tools and automated quality inspection further enhances finish reliability. With rising EV production and light-weight multi-material assemblies, automotive coating automation remains a foundational driver of market demand and technology investment.

Healthcare and medical devices are anticipated to be the fastest-growing end-use segment, with an approximate 10.4% CAGR through 2033, driven by precision coating requirements for products such as Zimmer Biomet orthopedics, Medtronic surgical instruments, and Boston Scientific devices. Robotic systems ensure sterile, defect-free coatings on implants, housings, and diagnostic equipment, meeting strict FDA and ISO sterilization standards. In 2025, Stryker’s medical device facility integrated automated robotic coating and inspection cells to support clean-room compliant workflows, reducing error rates and accelerating delivery times.

Adoption extends to biotech instrumentation and lab automation, where robotic coating of fluidic interfaces enhances performance consistency. This segment’s rapid growth reflects strong demand for medical devices and the critical role of precision robotics in delivering compliant, high-quality coatings.

Regional Insights

North America Coatings and Application Technologies for Robotics Market Trends

North America represents a significant market for robotics coatings and application technologies, with the U.S. driving adoption in automotive, aerospace, electronics, and defense sectors. The region reflects a high automation intensity and established industrial infrastructure. Large-scale deployment of industrial robots requires durable coatings and precision application systems, particularly in high-value manufacturing lines. In 2025, Hyundai Motor Group’s AI-driven Metaplant America facility in Alabama showcased smart robotic painting cells and digital twin integration, improving throughput, quality consistency, and predictive maintenance.

Key growth drivers include the reshoring of manufacturing operations, Industry 4.0 initiatives, and increased automation in precision industries. Regulatory frameworks such as EPA and CARB VOC standards support the adoption of waterborne and energy-efficient coatings. Collaboration between universities, OEMs, and integrators fosters technological leadership. Investment trends focus on AI-enabled application systems, digital twin platforms, and next-generation coating materials that enhance process control, reduce waste, and ensure regulatory compliance. North America remains a mature, innovation-driven market with steady growth and high technological adoption.

Europe Coatings and Application Technologies for Robotics Market Trends

Europe is a mature market for robotic coatings and application technologies, supported by high levels of industrial automation and regulatory compliance across Germany, France, the U.K., and Spain. German automotive and precision engineering sectors continue to drive demand for robotic spray and automated coating systems, while EU-wide REACH and VOC directives accelerate the adoption of eco-friendly formulations. In 2025, Volkswagen’s Zwickau plant integrated automated spray and inspection robots, enhancing production efficiency and sustainability outcomes in line with EU climate targets.

Key drivers include stringent environmental regulations, government stimulus for digital manufacturing, and high automation intensity. European manufacturers invest in smart application systems, predictive maintenance technologies, and advanced coatings to improve operational efficiency while maintaining compliance. Competitive dynamics feature partnerships between local and multinational players, emphasizing innovation in adaptive coating solutions and Industry 4.0 integration. Harmonized regulatory frameworks and a focus on sustainability position Europe as a stable, innovation-driven market for robotic coatings.

Asia Pacific Coatings and Application Technologies for Robotics Market Trends

Asia Pacific is projected to be the fastest-growing and leading regional market, expected to hold an estimated 35% value share in 2026 and register a CAGR of around 8.5% through 2033. Growth is driven by large-scale industrial expansion, escalating automation investments, and smart factory initiatives in China, Japan, and India. China remains a dominant force with over 295,000 industrial robot installations in 2024, supporting high-volume automotive and electronics manufacturing. Japan contributes with precision robotics for semiconductor and electronics production, while India’s PLI scheme encourages automation adoption in the automotive and electronics sectors.

Key drivers include cost-effective manufacturing, policy support for automation, and high-volume production requirements. Regulatory emphasis on emissions and sustainable manufacturing promotes the adoption of low-VOC and eco-friendly coatings, especially in urban industrial hubs. Investments in FDI, smart factory infrastructure, and localized innovation centers facilitate advanced coating and application technologies. Regional original equipment manufacturers (OEMs) collaborate with global suppliers to optimize robotic coating systems, while government incentives and smart manufacturing programs accelerate deployment. Asia Pacific’s combination of scale, technological expertise, and supportive policies positions it as the global leader in robotic coatings and application technologies.

Competitive Landscape

The global coatings and application technologies for robotics market landscape is moderately consolidated, with leading players such as ABB, Fanuc, Dürr, Yaskawa, and Nordson controlling a significant portion of the revenue share. These companies leverage established relationships with OEMs, deep expertise in robotic integration, and end-to-end coating solutions combining hardware, software, and process know-how. Heavy investments in R&D, AI-enabled application systems, and precision robotics allow them to maintain technological leadership and deliver higher efficiency, reduced waste, and consistent quality for industrial and high-value applications.

Meanwhile, regional and niche competitors such as KUKA, SAMES KREMLIN, and Motoman focus on specialized applications, including collaborative robots, automated coating cells, and small-scale precision tasks in healthcare, aerospace, and electronics. High capital investment requirements, system integration complexity, and regulatory compliance act as barriers to entry for newcomers. At the same time, digitalization trends, such as cloud-based process monitoring, AI-driven predictive maintenance, and IoT-enabled spray systems, are enabling smaller software-focused firms to participate via integration partnerships. Market consolidation is expected to grow gradually as leading players acquire regional vendors to expand geographically and technologically.

Key Industry Developments

- In October 2025, SoftBank’s acquisition of ABB Robotics strengthened its Physical AI strategy, integrating AI with industrial robotics. The deal adds US$ 2.3 billion in revenue and 7,000 employees, enabling global expansion of AI-driven automation solutions.

- In July 2025, Zimmer Biomet enhanced its surgical robotics portfolio by acquiring Monogram Technologies, supporting AI-guided orthopedic procedures. The deal complements its ROSA® platform and enables the commercialization of autonomous surgery systems by 2027.

- In July 2025, Cheetah Mobile acquired 60.8% of UFACTORY, integrating lightweight collaborative robotic arms into its AI-driven service robot platforms. The acquisition accelerates the commercialization and adoption of flexible industrial and service robotics.

Companies Covered in Coatings and Application Technologies for Robotics Market

- BASF SE

- Akzo Nobel N.V.

- Axalta Coating Systems

- The Sherwin Williams Company

- PPG Industries, Inc.

- Nordson Corporation

- Dürr Aktiengesellschaft

- Hempel A/S

- Jotun Group

- HMG Paints Limited

- The Lubrizol Corporation

- Carlisle Fluid Technologies Inc.

Frequently Asked Questions

The global coatings and application technologies for robotics market is projected to reach US$ 21.9 billion in 2026.

Adoption of industrial and collaborative robots, automation in manufacturing, and demand for durable, eco-friendly coatings are key drivers.

The market is poised to witness a CAGR of 7.8% from 2026 to 2033.

Integration of smart coating cells and sustainable coating solutions presents major growth opportunities.

ABB, Fanuc, Dürr, Yaskawa, Nordson, KUKA, and SAMES KREMLIN are a few among the leading players in the market.