- Food Ingredients & Additives

- Edible Films and Coatings Market

Edible Films and Coatings Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Edible Films and Coatings Market by Material Type (Proteins, Polysaccharides, Lipids, Others), Application (Dairy products, Bakery and Confectionery, Fruits and Vegetables, Meat, Poultry, and Seafood, Others), Function Type (Barrier Properties, Active Packaging, Structural and Mechanical Properties, Biodegradable Packaging Functionality, Others), and Regional Analysis from 2026 to 2033

Edible Films and Coatings Market Share and Trends Analysis

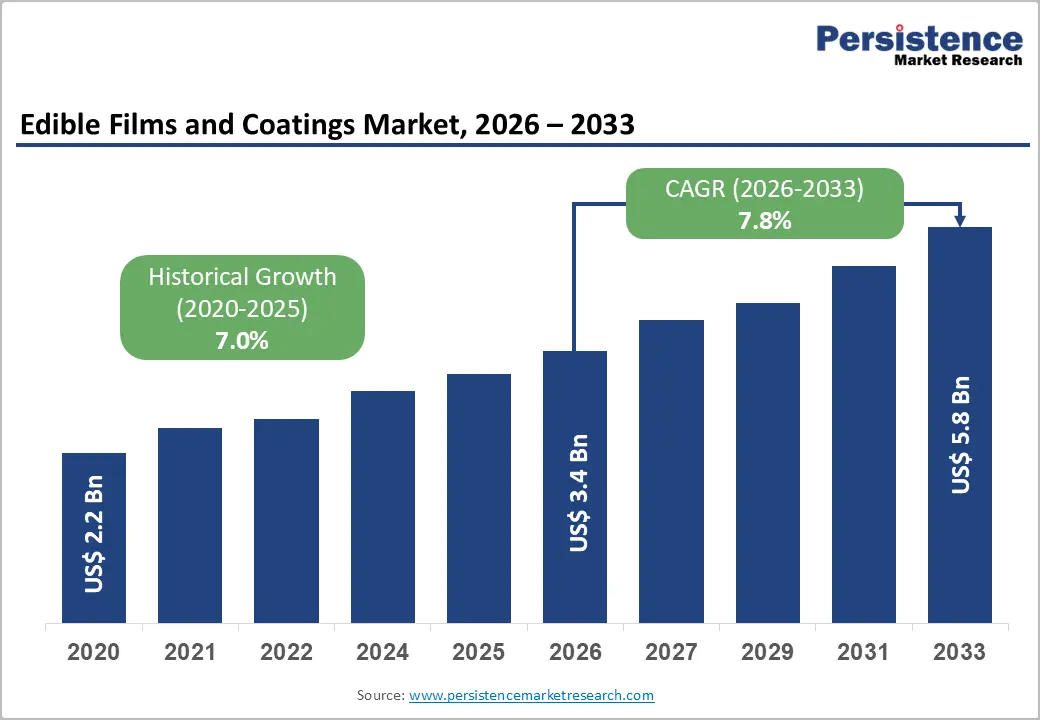

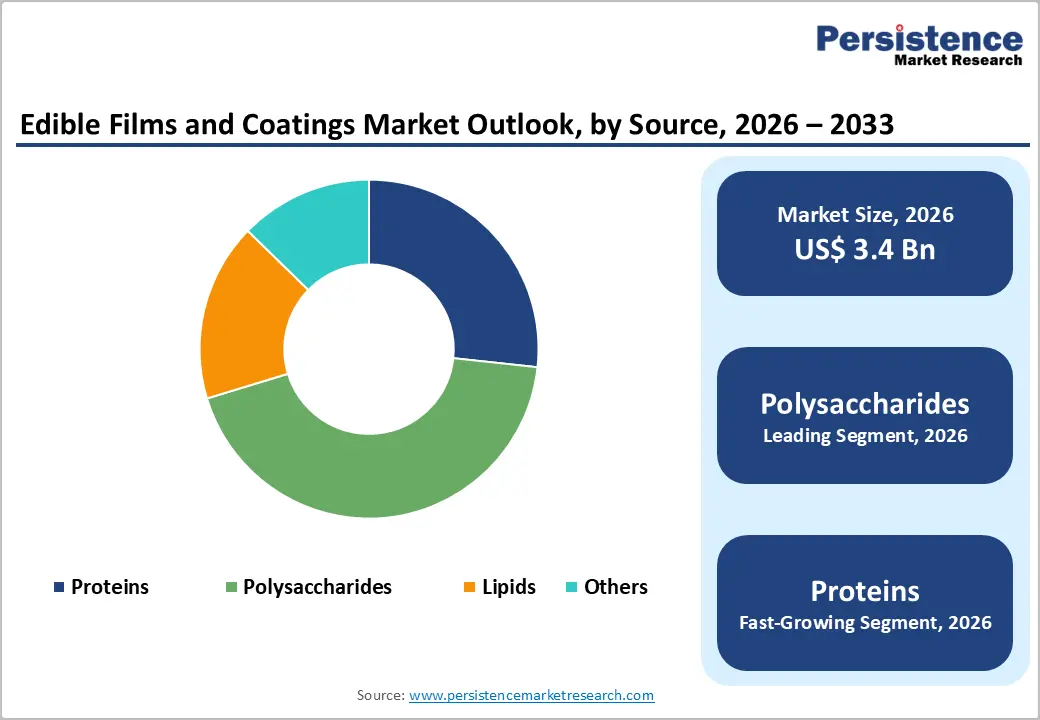

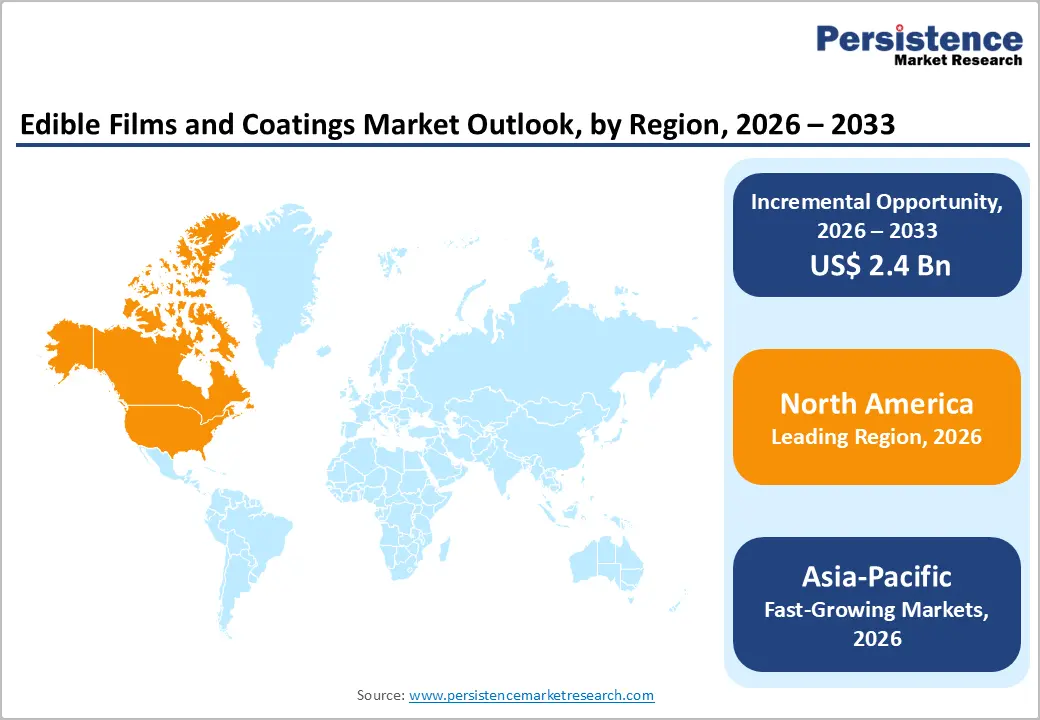

The global edible films and coatings market is estimated to grow from US$ 3.4 Bn in 2026 to US$ 5.8 Bn by 2033. The market is projected to record a CAGR of 7.8% from 2026 to 2033.

The global market is growing steadily, driven by rising demand for sustainable packaging, extended shelf life, and clean-label food solutions. North America leads due to advanced food processing and strong adoption of innovative coatings. Asia Pacific is the fastest-growing region, supported by expanding food industries, urbanization, and increasing demand for fresh and minimally processed foods.

Key Industry Highlights:

- Dominant Material Type: Polysaccharide-based films held the largest share 43.6% in 2025, driven by strong film-forming properties, cost-effectiveness, and wide application across fruits, vegetables, and processed foods.

- Regional Leadership: North America led the market in 2025 with 38.3% share, supported by advanced food processing infrastructure, high adoption of sustainable packaging, and strong demand for ready-to-eat products.

- Growth Indicator: Growth is driven by increasing demand for sustainable packaging, extended shelf life, clean-label ingredients, and rising consumption of fresh and minimally processed foods.

- Market Opportunity: Opportunities exist in composite films, expansion in Asia-Pacific and Latin America, innovation in biodegradable materials, and increasing adoption in fresh produce and meat preservation applications.

| Key Insights | Details |

|---|---|

| Global Edible Films and Coatings Market Size (2026E) | US$ 3.4 Bn |

| Market Value Forecast (2033F) | US$ 5.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

Market Dynamics

Driver: Rising demand for sustainable and biodegradable packaging solutions

The demand for sustainable packaging is strongly driven by the environmental burden of conventional plastics. According to the European Commission, packaging accounts for nearly 35% of total municipal solid waste in the European Union, highlighting the scale of packaging-related environmental impact. Additionally, petroleum-based plastics used in food packaging are non-biodegradable and contribute to greenhouse gas emissions during disposal and incineration, worsening climate change concerns. This has led governments and regulatory bodies globally to push for biodegradable alternatives, directly accelerating the adoption of edible films and coatings. At the same time, food waste reduction is becoming a parallel driver. The Food and Agriculture Organization estimates that around 1.3 billion tonnes of food is wasted globally each year, much of it due to spoilage and poor packaging. Edible films help extend shelf life by controlling moisture and microbial growth, thereby reducing waste. As consumers increasingly prefer eco-friendly and “zero-waste” solutions, edible coatings, being biodegradable and sometimes consumable align directly with sustainability goals, making them a key innovation in modern food packaging systems.

Restraint: Rising demand for sustainable and biodegradable packaging solutions

While sustainability drives adoption, it also introduces technical and economic constraints. Biodegradable edible films, though environmentally friendly, often lack the mechanical strength and moisture resistance of conventional plastics, limiting their large-scale industrial use. Studies show that polysaccharide- and protein-based films provide good gas barriers but perform poorly against water vapor, making them unsuitable for certain food categories. This creates a paradox where demand for sustainable solutions rises, but functional limitations slow widespread replacement of plastic packaging.

Additionally, lifecycle sustainability is not always straightforward. Research highlights that although edible films are biodegradable, their production processes must be carefully assessed for overall environmental impact, including energy use and raw material sourcing. Regulatory frameworks also add complexity, as edible coatings must comply with strict food safety standards across regions. These factors increase costs and delay commercialization. As a result, despite strong sustainability demand, adoption remains constrained by performance limitations, cost structures, and regulatory compliance requirements.

Opportunity: Development of composite and multifunctional edible films

The development of composite edible films presents a major opportunity to overcome existing limitations. By combining proteins, polysaccharides, and lipids, manufacturers can create films with enhanced mechanical strength, moisture resistance, and gas barrier properties, addressing the weaknesses of single-material films. These multifunctional films can also incorporate antimicrobial and antioxidant compounds, improving food safety and extending shelf life. This aligns with global priorities to reduce food spoilage while maintaining product quality across supply chains.

Furthermore, innovation in edible films supports circular economy principles. Research indicates that agri-food waste (such as fruit peels and by-products) can be used as raw materials for film production, transforming waste into value-added packaging solutions. This not only reduces industrial waste but also lowers raw material costs. With increasing regulatory pressure to reduce plastic use and improve sustainability, composite edible films offer a scalable, high-performance alternative, creating strong growth opportunities across fresh produce, meat, and processed food applications.

Category-wise Analysis

By Material Type Insights

Polysaccharides dominate the edible films and coatings market with 43.6% share in 2026, due to their abundance, cost-effectiveness, and strong functional properties. Derived from plant sources like starch, cellulose, and pectin, they are widely available and sustainable. Studies indicate polysaccharides are the most commonly used biopolymers in edible films because of their non-toxicity and ease of processing. They offer excellent oxygen and carbon dioxide barrier properties, which help in preserving food quality. Additionally, agro-food waste such as fruit peels can be utilized as raw material, supporting circular economy goals. Their compatibility with additives like antimicrobials further enhances shelf life, making them the preferred material despite moderate moisture barrier limitations.

By Application Insights

Fruits and vegetables dominate the edible films and coatings market due to their high perishability and significant global wastage. According to the Food and Agriculture Organization, about 1.3 billion tonnes of food are wasted annually, with fruits and vegetables contributing the largest share, and nearly 50% lost across the supply chain. This creates strong demand for preservation technologies. Edible coatings help reduce moisture loss, slow respiration, and inhibit microbial growth, thereby extending shelf life. With increasing global trade of fresh produce and rising consumer demand for minimally processed foods, natural preservation solutions are gaining importance, making fruits and vegetables the leading application segment.

Regional Insights

North America Edible Films and Coatings Market Trends

North America dominates the edible films and coatings market due to its advanced food supply chain, low food loss rates, and strong infrastructure. According to the Food and Agriculture Organization, food loss in North America is around 10%, among the lowest globally, reflecting efficient storage, packaging, and distribution systems. This creates a strong foundation for adopting advanced preservation technologies like edible coatings. Additionally, high consumption of packaged and ready-to-eat foods increases demand for shelf-life extension solutions, further supporting market dominance.

Furthermore, sustainability awareness and regulatory push strengthen adoption. Governments and agencies actively promote reducing food waste and environmental impact. The region also has high investment in food innovation and R&D, enabling the commercialization of novel coating technologies. With strong cold chain infrastructure, large-scale food processing, and consumer preference for clean-label and eco-friendly packaging, North America continues to lead in the adoption and commercialization of edible films and coatings.

Europe Edible Films and Coatings Market Trends

Europe is a key region due to its strong regulatory framework and high focus on sustainability and waste reduction. According to the European Commission, the EU generates over 59 million tonnes of food waste annually, with a significant environmental impact. This has led to strict policies under initiatives like the circular economy and food waste reduction targets, encouraging the adoption of biodegradable and edible packaging solutions.

Additionally, Europe has high consumer awareness regarding environmental sustainability and food safety. Regulations promoting reduced plastic use and eco-friendly alternatives drive innovation in edible coatings. The region also emphasizes reducing greenhouse gas emissions, with food waste contributing about 16% of emissions in the EU food system. These regulatory pressures, combined with advanced food processing and strong sustainability goals, make Europe a strategically important market.

Asia-Pacific Edible Films and Coatings Market Trends

Asia-Pacific is the fastest-growing region due to high food loss rates, expanding food production, and rapid urbanization. According to the Food and Agriculture Organization, food loss in several developing regions can exceed 20%, significantly higher than in developed regions. This creates strong demand for preservation technologies like edible coatings to reduce post-harvest losses.

In addition, fruits and vegetables, the major produce in Asia, experience 25-50% post-harvest losses globally, particularly in regions with limited cold-chain infrastructure. Rapid urbanization, rising middle-class population, and increasing consumption of packaged and fresh foods are further accelerating demand. Governments are also investing in improving food supply chains and reducing waste. These factors collectively drive strong adoption, making Asia-Pacific the fastest-growing region in the edible films and coatings market.

Competitive Landscape

The edible films and coatings market is competitive, driven by innovation in biodegradable materials and functional coatings. Companies focus on enhancing product performance, expanding production capacity, ensuring regulatory compliance, and strengthening distribution networks. Growing demand from the fresh produce, meat, and processed food industries is pushing advancements in sustainable and shelf-life extension solutions globally.

Key Industry Developments:

- In February 2026, Akorn Technology won the UAE FoodTech Challenge by showcasing its innovative edible coating solution designed to extend the shelf life of fresh produce. The company’s technology focuses on reducing food waste by forming a protective, biodegradable layer around fruits and vegetables, helping maintain freshness during storage and transportation.

- In June 2024, Tate & Lyle PLC invested in the edible films market through its venture arm, partnering with Scottish Enterprise to acquire BioFilm Limited, a manufacturer of dissolvable and edible films. The acquisition aimed to capitalize on the growing demand for edible films as delivery systems for active ingredients in nutraceutical and medical applications.

Companies Covered in Edible Films and Coatings Market

- Tate & Lyle PLC

- Ingredion

- Cargill Incorporated

- Apeel Sciences

- Akorn Technology

- Sufresca

- Kerry Group plc.

- Mantrose-Haeuser Co., Inc.

- Pace International LLC

- NatureSeal, Inc.

- MonoSol LLC

- Lactips

- Hazel Technologies, Inc.

- Flo Enterprises, LLC

- Others

Frequently Asked Questions

The global edible films and coatings market is projected to be valued at US$ 3.4 Bn in 2026.

Rising demand for sustainable packaging, shelf-life extension, clean-label products, and reduced food waste globally.

The global edible films and coatings market is poised to witness a CAGR of 7.8% between 2026 and 2033.

Growth in biodegradable films, composite materials, emerging markets, food preservation technologies, and sustainable packaging innovations.

Tate & Lyle PLC, Ingredion, Cargill Incorporated, Apeel Sciences, Akorn Technology, Sufresca.