- Inks, Coatings, Adhesives & Sealants (ICAS)

- High Temperature Coatings Market

High Temperature Coatings Market Size, Share, and Growth Forecast 2026 - 2033

High Temperature Coatings Market by Resin Type (Epoxy, Silicone, Polyethersulfone, Polyester, Acrylic, Alkyd, Others), Technology (Solvent-based, Water-based, Powder-based), by Substrate Type (Metal, Ceramics, Composites, Glass), Application (Energy & Power, Metal Processing, Cookware, Stove and Grills, Coil Coating & Fabrication, Automotive, Aerospace & Defence, Building & Construction, Marine, Others), and Regional Analysis, 2026 - 2033

High Temperature Coatings Market Size and Trend Analysis

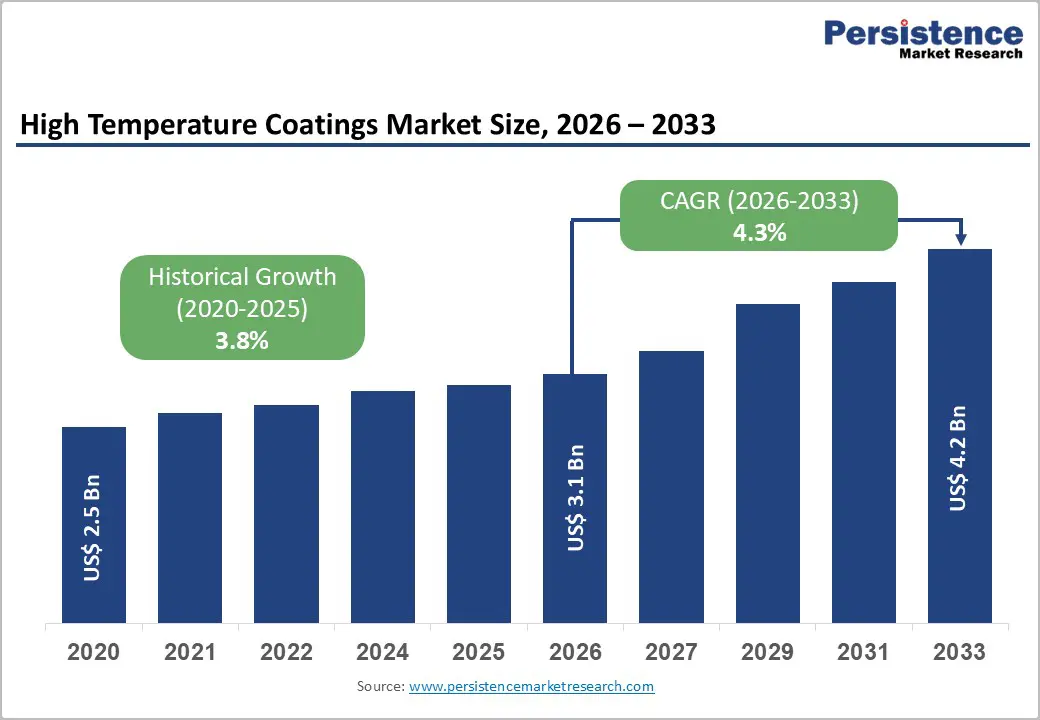

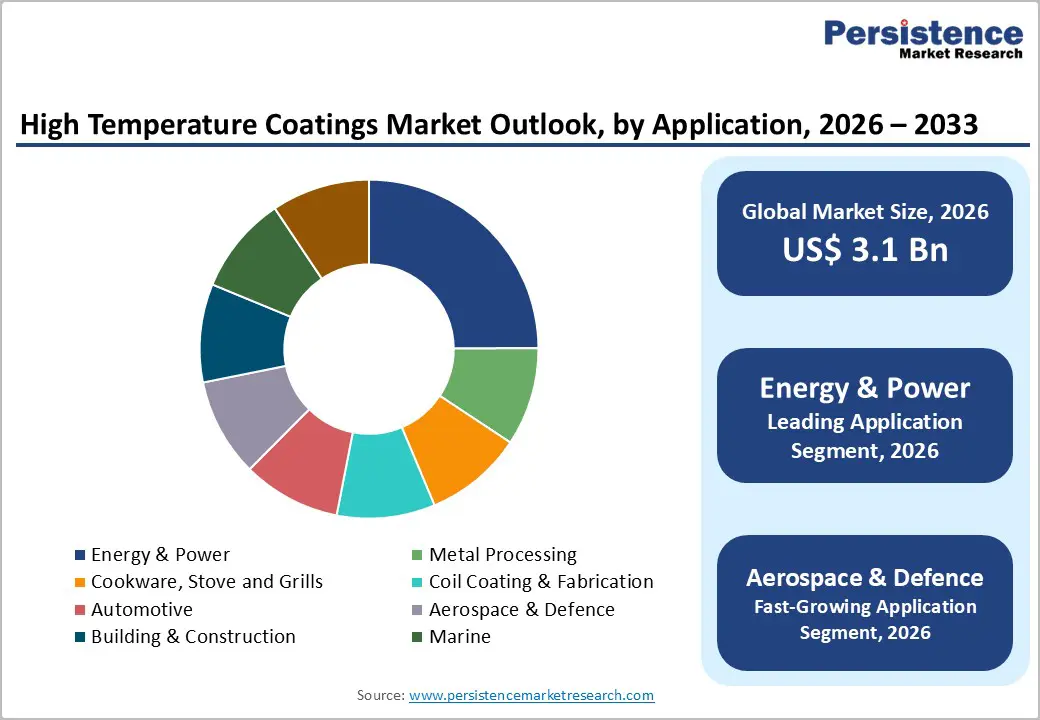

The global high temperature coatings market size is expected to be valued at US$ 3.1 billion in 2026 and projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033. This steady growth trajectory is driven by accelerating demand from the energy & power, aerospace & defence, and automotive sectors, where components operating under sustained thermal stress require protective coatings that maintain structural integrity and corrosion resistance over extended service lives.

Simultaneously, stringent global environmental regulations, including the U.S. EPA's January 2025 amendments to National VOC Emission Standards and the European Union's REACH directives, are compelling manufacturers to innovate toward waterborne and low-VOC formulations, repositioning high-temperature coatings as a compliance-driven investment rather than a discretionary expenditure for industrial operators.

Key Industry Highlights:

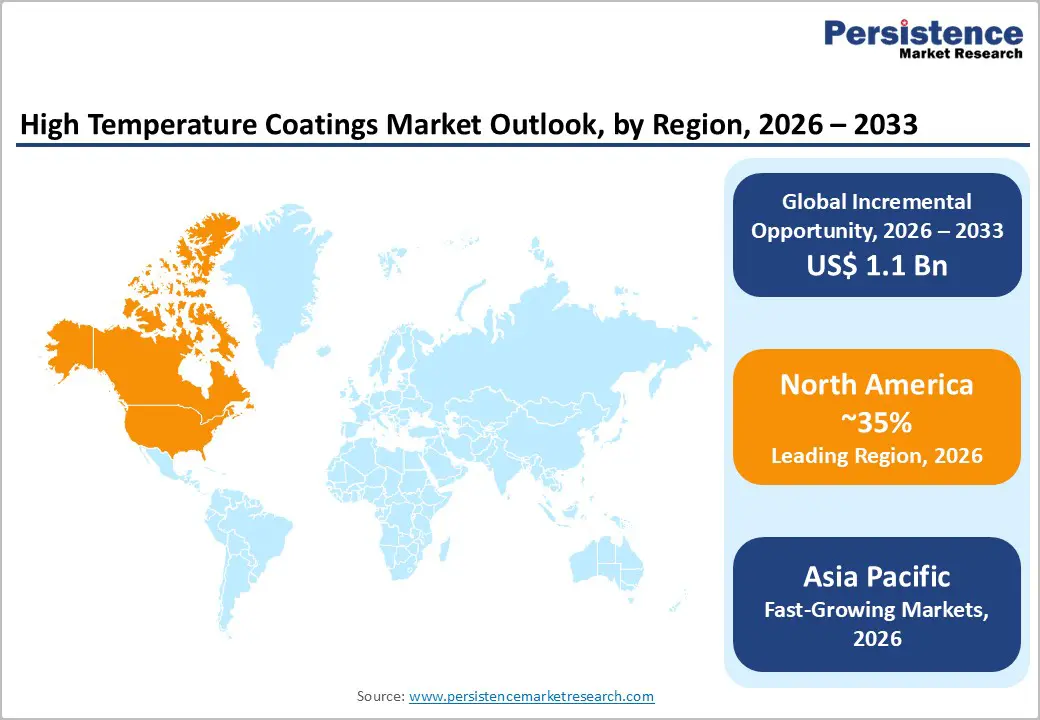

- Leading Region: North America held nearly 35% of global share in 2025, driven by the world's largest aerospace manufacturing base, major petrochemical infrastructure, and active industrial maintenance programs supported by federal compliance mandates.

- Fastest Growing Region: Asia Pacific is the fastest growing region, projected at a CAGR exceeding 5% through 2033, catalyzed by China's US$ 91.5 billion petrochemical capex pipeline, India's automotive production boom, and rapid industrialization across Southeast Asian manufacturing hubs.

- Dominant Segment: Silicone resin commands approximately 38% of the market in 2025, sustained by its unmatched thermal stability at temperatures exceeding 600°C across exhaust, gas turbine, and industrial furnace applications where no organic resin alternative can compete.

- Fastest Growing Segment: Powder-based coatings are the fastest growing technology segment, driven by EPA and EU REACH VOC regulations that are compelling industrial buyers to transition from solvent-based systems, while powder coatings deliver zero VOC emissions and superior adhesion on metal substrates.

- Key Market Opportunity: The global EV battery segment represents an actionable, high-margin growth window for validated powder coating specialists; with the EV market surpassing 20 million units in 2025, OEM-certified thermal runaway protection coatings command premium pricing and long-term supply agreements.

Market Dynamics

Drivers - Expansion of Energy Infrastructure and Industrial Asset Protection Mandates

For manufacturers and suppliers of industrial coatings, the global expansion of power generation infrastructure, covering gas turbines, boilers, heat exchangers, and petrochemical processing units, represents the most structurally durable demand driver in the market. High-temperature coatings serve a functionally non-negotiable role in these environments: without thermal barrier and corrosion protection coatings, critical equipment in energy & power applications would face dramatically shortened service lifespans, increasing maintenance costs and unplanned downtime.

China alone has 305 planned and announced petrochemical plants with a combined capacity of approximately 152.4 million tonnes per annum (mtpa) by 2030, representing a capital expenditure pipeline of approximately US$ 91.5 billion that will generate sustained demand for high-performance protective coatings. In India, the chemical industry valued at US$ 250 billion in 2024 and is expected to reach US$ 300 billion by 2028, further amplifying regional procurement of industrial thermal-protection solutions.

Automotive Electrification and Aerospace Modernization Creating New Thermal Performance Requirements

The convergence of electric vehicle adoption and aerospace modernization programs is reshaping the performance specification for high-temperature coatings, creating premium-priced demand segments that reward technical differentiation. In the automotive sector, the rapid scale-up of electric vehicle (EV) production, with the global EV market on track to surpass 20 million units in 2025, representing over a quarter of all vehicles sold, is driving demand for battery thermal management coatings capable of withstanding extreme heat events.

Axalta Coating Systems responded to this need in October 2025 by launching the Alesta® e-PRO product family, including a powder coating engineered to maintain integrity under direct flame exposure at temperatures exceeding 1,200°C. In aerospace, high-temperature coatings protect components of aircraft engines, exhaust-washed surfaces, and hypersonic leading edges from aero-thermal loading, a category where the aerospace industry is projected to remain one of the highest-growth applications, as growing air travel in developing economies drives fleet expansion and maintenance programs globally.

Restraints - Stringent Environmental Regulations Increasing Reformulation Costs and Compliance Burden

Environmental compliance is fast becoming one of the most tangible cost pressures for high-temperature coatings manufacturers, particularly for producers relying on solvent-based systems that remain dominant in performance-critical industrial applications. The U.S. EPA's January 2025 final rule amending National VOC Emission Standards for Aerosol Coatings introduced new reactivity factors, tightened ozone controls, and expanded the list of regulated compounds, with a mandatory compliance deadline of January 2027. California's SCAQMD Rule 1113 caps architectural coatings at under 50 g/L VOC, a benchmark that many manufacturers now apply nationally to streamline production.

The EU's Deco Paint Directive and REACH regulations reinforce these pressures across European markets. For manufacturers, reformulating products to meet these evolving standards typically increases production costs and can create performance trade-offs in high-temperature resistance, a constraint that especially disadvantages smaller regional producers lacking R&D resources to develop compliant next-generation formulations.

Raw Material Price Volatility and Supply Chain Disruptions Compressing Margins

Volatility in the prices of key raw materials, including specialty silicone intermediates, epoxy resins, titanium dioxide, and high-purity ceramic precursors, creates a persistent margin compression risk for high-temperature coatings producers that is particularly difficult to offset through pricing, given that many industrial buyers operate under long-term contract frameworks.

Price disruptions in specialty chemical supply chains can originate from energy market shocks, geopolitical events, or upstream capacity constraints, and their downstream effects are amplified in high-temperature coatings formulations because these products rely on a relatively narrow range of thermally stable binders and pigments, unlike commodity coatings, which can be more readily reformulated with substitute materials. The high-temperature coatings sector's historic growth rate of 4.4% from 2020 to 2024 reflected in part the drag from pandemic-era supply disruptions in the specialty chemicals sector. New entrants face the additional challenge of establishing supplier relationships and inventory buffers that incumbents have built over decades, a structural barrier that reinforces consolidation among tier-one players.

Opportunities - Electric Vehicle Battery Thermal Management as a High-Value Emerging Application

The electric vehicle battery system represents one of the most technically demanding and commercially significant new application segments for high-temperature coatings, and companies that establish validated OEM supply relationships now will secure preferred-supplier positions in a market set to scale rapidly through 2033. The core technical need is compelling: when a single battery cell overheats, it can trigger thermal runaway, releasing temperatures exceeding 1,200°C and causing fires, explosions, and structural failure.

Coating solutions that can delay fire propagation, maintain electrical insulation, and produce zero smoke during thermal events directly address a safety priority that is regulatory-critical for every EV manufacturer globally. Axalta's Alesta® e-PRO FG Black, launched in October 2025, has been tested against UL 2596 TaG and direct flame exposure standards, demonstrating the viability of powder coatings in this role. With the global EV fleet expanding rapidly and battery pack OEM specifications becoming increasingly standardized, suppliers of validated thermal protection coating systems that meet emerging IEC and UL safety standards are positioned to command long-term supply agreements with premium pricing from automakers prioritizing battery safety.

Renewable Energy Infrastructure Build-Out Creating Sustained Demand for Protective Coatings

The global energy transition, characterized by a massive scale-up in wind turbines, solar thermal plants, concentrated solar power (CSP) systems, and next-generation gas-fired power generation, is opening a substantial and underappreciated demand channel for high-temperature coatings in infrastructure environments that require multi-decade asset protection. Gas turbine components, exhaust systems, heat exchangers, and structural steel in power stations all require thermal barrier coatings with documented long-term performance to maintain plant efficiency and meet safety certification requirements.

The International Energy Agency (IEA) has estimated that global clean energy investment surpassed US$ 2 trillion in 2024 for the first time, with significant capital directed toward power generation assets that require protective coating systems at installation and during periodic maintenance cycles. Companies with proven high-temperature coating portfolios specifically certified for turbine and heat exchange applications, such as those offered by Oerlikon's Advanced Coating Technology Center, opened in June 2024 in Westbury, NY, are strategically positioned to capture a share of this multi-decade infrastructure maintenance cycle, particularly if they secure specification listings with major engineering procurement and construction (EPC) contractors.

Category-wise Analysis

Resin Type Insights

The Silicone resin segment commands approximately 38% of the high temperature coatings market in 2025, a leadership position that reflects its unmatched thermal stability among organic resin systems, silicone-based coatings retain functional integrity at temperatures from 150°C to well above 600°C, enabling their deployment across the broadest range of industrial, automotive, and aerospace applications in the market.

Silicone's chemical structure, with its alternating silicon-oxygen backbone, provides inherent resistance to oxidation and thermal degradation that epoxy and alkyd chemistries cannot replicate at the high end of the temperature range, making it the resin of choice for exhaust systems, industrial furnaces, and gas turbine components.

The Fastest Growing Resin Segment is Epoxy, driven by its versatility across metal protection applications, superior adhesion, excellent chemical resistance, and growing adoption in EV battery and energy sector applications where its thermal stress tolerance and formulation flexibility are increasingly valued by OEMs seeking cost-effective compliance with demanding performance specifications.

Technology Analysis

The Solvent-based technology segment holds the leading market position with approximately 48% share in 2025, a dominance grounded in its proven performance characteristics across the most demanding industrial environments: solvent-based systems provide superior film formation, high adhesion on diverse substrates, and consistent curing behavior even in field-applied conditions at oil & gas facilities, power plants, and marine structures where surface preparation is imperfect and ambient conditions are variable.

Powder-based coatings are a fast-growing technology that has gained rapid traction as industries face tightening VOC emissions regulations from the U.S. EPA and EU REACH directives. Powder coatings emit virtually zero VOCs and offer exceptional thickness consistency and adhesion on metal substrates, aligning performance requirements with regulatory compliance in automotive, appliance, and architectural applications.

Substrate Type Analysis

The Metal substrate segment accounts for approximately 65% of the high temperature coatings market by substrate type in 2025, reflecting the fundamental reality that the most voluminous high-temperature coating applications, industrial equipment, pipelines, exhaust systems, boilers, and structural steel in energy plants, are overwhelmingly applied to metal surfaces that require protection from combined thermal, corrosive, and mechanical stresses.

Steel remains the dominant substrate material across energy, petrochemical, marine, and building and construction end-use industries, and high-temperature coatings manufacturers have decades of formulation expertise and certified performance data specific to steel and aluminum substrates that creates a durable barrier to displacement.

Composites are fastest-growing substrate, driven by the aerospace and automotive sectors' increasing use of carbon fiber and polymer matrix composite structures in high-heat zones, where conventional metal-optimized coatings are inadequate and purpose-developed composite-compatible thermal barrier solutions command significant price premiums.

Application Insights

The Energy & Power application segment holds the leading share of approximately 25% of the high temperature coatings market in 2025, driven by the sector's continuous procurement of thermal barrier and corrosion protection coatings for turbines, boilers, heat exchangers, furnaces, and industrial pipelines where equipment failure carries significant safety and financial consequences. The energy sector's asset-intensive nature and long equipment service life create recurring demand, both for new installations and periodic maintenance recoating, that provides stable, predictable revenue for leading coatings suppliers.

Aerospace & Defense is the fast-growing application where stringent performance certification requirements and the sustained expansion of commercial aviation fleets in emerging markets, particularly in Asia Pacific, are driving procurement of advanced thermal barrier coatings for engine components, airframe surfaces, and defense platform protection systems that must meet MIL-SPEC and OEM certification standards.

Regional Insights

North America High Temperature Coatings Market Trends and Insights

North America leads the global High Temperature Coatings market with approximately 35% share in 2025, anchored by its dominant aerospace and defence sector, large base of petrochemical and energy processing infrastructure, and active industrial maintenance culture. The region's demand is structurally supported by federal asset protection requirements for critical infrastructure and by strict environmental compliance mandates, particularly the EPA's 2025 VOC amendments, which are simultaneously constraining solvent-based product sales and accelerating investment in next-generation waterborne and powder coating systems.

The U.S. market is heading toward a premium, performance-differentiated landscape where suppliers with certified low-VOC, high-temperature formulations will gain structural advantages as environmental compliance timelines tighten across industrial end markets through 2033.

U.S. High Temperature Coatings Market Size

The United States accounts for approximately 85% of North American demand for high temperature coatings, driven by the world's largest aerospace manufacturing base, which the Aerospace Industries Association (AIA) values at over US$ 400 billion annually, alongside a vast petrochemical and energy sector. The U.S. is also home to a significant and growing EV manufacturing base, with battery thermal coating procurement expanding in lockstep with domestic cell production. Government-funded infrastructure modernization programs further sustain maintenance coating demand, positioning the U.S. as the single most important national market globally through 2033.

Europe High Temperature Coatings Market Trends and Insights

Europe holds approximately 21% of the global High Temperature Coatings market in 2025, shaped by a regulatory environment that is among the world's most demanding for coatings formulations. The EU's REACH regulations, Deco Paint Directive, and expanding Green Deal industrial sustainability requirements are structurally incentivizing the transition from solvent-based to waterborne and powder coating technologies, a shift that is both constraining legacy product revenue and creating R&D investment opportunities for manufacturers with low-VOC high-temperature formulations.

Europe's automotive, steel processing, and energy sectors generate consistent baseline demand, while industrial manufacturing clusters in Germany, France, and Italy sustain procurement through planned asset maintenance cycles.

Germany High Temperature Coatings Market Size

Germany is Europe's largest single-country market for high temperature coatings, estimated at approximately US$ 257 million in 2024, supported by its leadership positions in automotive manufacturing, industrial machinery, and engineered steel processing. Germany's Gigabitstrategie, combined with its robust Mittelstand industrial base and leadership in chemical engineering, positions the country as both a major end-user and an innovation hub for advanced coating formulations. With the EU Green Deal mandating progressive decarbonization of industrial assets, demand for energy-efficient high-temperature coatings in German industrial facilities is expected to remain elevated through 2033.

U.K. High Temperature Coatings Market Size

The United Kingdom contributes approximately 14% of European high temperature coatings revenue, underpinned by its significant aerospace and defence sector, anchored by Rolls-Royce and BAE Systems, as well as oil and gas infrastructure in the North Sea that requires corrosion and thermal protection coatings for offshore assets operating in harsh marine environments. The UK's commitment to net-zero emissions by 2050 is driving investment in new power generation infrastructure where high-temperature coatings play a protective role. Growing demand from advanced manufacturing and defence modernization programs positions the UK as a stable, high-value coatings market through the forecast period.

France High Temperature Coatings Market Size

France accounts for approximately 11% of European market revenue for high temperature coatings, driven primarily by its nuclear energy sector, which accounts for approximately 70% of national electricity generation, and aerospace manufacturing centered on Airbus and related tier-1 suppliers. These sectors demand thermally stable, corrosion-resistant coatings for reactors, heat exchangers, turbine components, and structural aircraft parts that must meet rigorous safety certification standards. France's Plan France Relance industrial recovery program has sustained capital investment in energy and aerospace infrastructure, providing a stable regulatory and fiscal environment that supports continued procurement of high-performance protective coatings through 2033.

Asia Pacific High Temperature Coatings Market Trends and Insights

Asia Pacific is the fastest growing region for high temperature coatings, accounting for approximately 37% of global market volume in 2025 and expanding at the highest regional CAGR through 2033. The region’s growth is driven by multiple sectors, with China’s large petrochemical investment pipeline of about US$ 91.5 billion through 2030 supporting strong industrial coatings demand.

Increasing industrial activity, stricter enforcement of coating quality standards, and cost-competitive production environments further strengthen the region’s attractiveness. As a result, Asia Pacific remains the key focus area for capacity expansion, supply chain localization, and distribution partnerships among global coating manufacturers.

India High Temperature Coatings Market Size

India accounts for approximately 13% of Asia Pacific high temperature coatings revenue, underpinned by the country's status as the second-largest automotive vehicle manufacturer in the region and a rapidly growing petrochemical sector projected to reach US$ 300 billion by 2025 per the Department of Chemicals & Petrochemicals. India's ambitious infrastructure modernization programs, including national highway and railway expansion, are generating additional demand for thermal and corrosion protection coatings on structural steel assets.

As domestic manufacturing capacity expands under Make in India initiatives, India is expected to emerge as one of the two largest growth markets in Asia Pacific for industrial coatings through 2033.

Japan High Temperature Coatings Market Size

Japan contributes approximately 15% of Asia Pacific revenue for high temperature coatings, supported by its world-leading position in precision automotive manufacturing, steel production, and industrial machinery, sectors that collectively generate sustained, specification-driven demand for thermally stable protective systems. Japanese OEM-grade quality standards for automotive coatings are among the strictest globally, driving consistent investment in premium, high-performance formulations.

The country's renewed commitment to nuclear energy following the Green Transformation (GX) policy and the restart of existing nuclear reactors is expected to generate incremental demand for high-temperature industrial coatings in reactor containment and heat management applications through the forecast period.

Southeast Asia High Temperature Coatings Market Size

Southeast Asia accounts for approximately 10% of Asia Pacific high temperature coatings revenue and is one of the region's highest-growth sub-markets, driven by rapid industrialization in Vietnam, Indonesia, Thailand, and Malaysia. The expansion of manufacturing supply chains, particularly automotive assembly, electronics, and petrochemical processing, is creating new procurement demand for thermal barrier coatings on industrial equipment and structural assets.

The ASEAN Plan of Action for Energy Cooperation is driving investment in power generation infrastructure across the region, providing an additional demand channel for energy-sector coating applications. Southeast Asia is expected to record among the highest CAGRs within Asia Pacific through 2033 as industrialization accelerates and environmental coating standards are progressively enforced.

Competitive Landscape

The global high temperature coatings market is moderately consolidated at the premium end, where a small group of large multinational producers hold significant share through broad industrial portfolios, strong global distribution networks, and advanced formulation capabilities. However, the market remains fragmented in specialized and niche applications, particularly where highly engineered solutions are required for extreme operating conditions.

Competitive positioning is largely driven by technical differentiation rather than scale alone. End users in aerospace, energy, and defense prioritize coatings that meet stringent OEM certifications, regulatory standards, and long-term performance validation, often accepting premium pricing for proven reliability. As environmental regulations tighten globally, companies are increasingly investing in low-VOC and sustainable formulations to ensure continued market access.

Strategic focus areas include R&D-led innovation, particularly in high-durability and corrosion-resistant chemistries, along with vertical integration into specialty raw materials to improve cost control and supply stability. Strong collaboration with industrial OEMs is also shaping competitive advantage through specification-driven demand. Meanwhile, specialized players focus on high-performance niche segments where application complexity supports higher margins despite lower volumes.

Key Developments

- April, 2026: PPG Industries announced the introduction of end-to-end protective coatings solutions and application services for data centers, designed to enhance corrosion, thermal, fire, and electrical protection while improving construction efficiency and operational reliability for rapidly expanding digital infrastructure.

- October 2025: Axalta Coating Systems launched Alesta® e-PRO FG Black and Alesta® e-PRO Dielectric Gray, powder coatings engineered for EV battery thermal stability and electrical insulation, tested to withstand direct flame at 1,200°C under UL 2596 TaG and UL 94 V0 standards.

- May, 2025: AkzoNobel announced the launch of a new coating system in China featuring a thermal insulation solution designed to reduce building surface temperatures and improve energy efficiency through advanced radiative cooling and heat-reflective coating technology.

- April, 2025: Cosmo Specialty Chemicals announced the launch of its COSEAL-601 heat seal coating solution, designed to deliver superior sealing strength, high-speed machine compatibility, and improved thermal and chemical resistance for flexible packaging applications, strengthening its advanced coatings portfolio in the packaging chemicals segment.

High Temperature Coatings Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 2.5 Billion |

| Current Market Value (2026) | US$ 3.1 Billion |

| Projected Market Value (2033) | US$ 4.2 Billion |

| CAGR (2026 - 2033) | 4.3% |

| Leading Region | North America, 35% market share (2025) |

| Dominant Resin Type | Silicone, 38% share (2025) |

| Top-ranking Technology | Solvent-based, 48% share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 1.1 Billion |

Companies Covered in High Temperature Coatings Market

- BASF SE

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Valspar

- Carboline Company

- Axalta Coating Systems, LLC

- Jotun

- Aremco

- Belzona International Ltd.

- Chemco International Ltd

- Hempel A/S

- Weilburger Coatings GmbH

- GENERAL MAGNAPLATE CORPORATION

- Oerlikon Group

- Kansai Paint Co., Ltd.

- RPM International Inc.

- Dow Chemical Company

Frequently Asked Questions

The global High Temperature Coatings market is valued at US$ 3.1 billion in 2026 and is expected to reach US$ 4.2 billion by 2033, growing at a CAGR of 4.3%.

The primary driver is the expansion of energy and industrial infrastructure, such as petrochemical plants, turbines, and power generation assets requiring thermal and corrosion protection.

North America leads the market with about 32-35% share in 2025, supported by strong aerospace manufacturing and energy infrastructure demand.

The key opportunity lies in EV battery thermal management coatings driven by rising EV adoption and safety requirements.

Key players include major global coating manufacturers and specialty players such as BASF, AkzoNobel, Sherwin-Williams, PPG, Axalta, Jotun, Hempel, and others.