- Inks, Coatings, Adhesives & Sealants (ICAS)

- Textile Coating Market

Textile Coating Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Textile Coating Market by Polymer Type (Thermoplastic, Thermosets, Other), Industry (Transportation, Construction & Building, Protective Clothing, Industrial, Medical, Other), and Regional Analysis for 2026 - 2033

Textile Coating Market Size and Trend Analysis

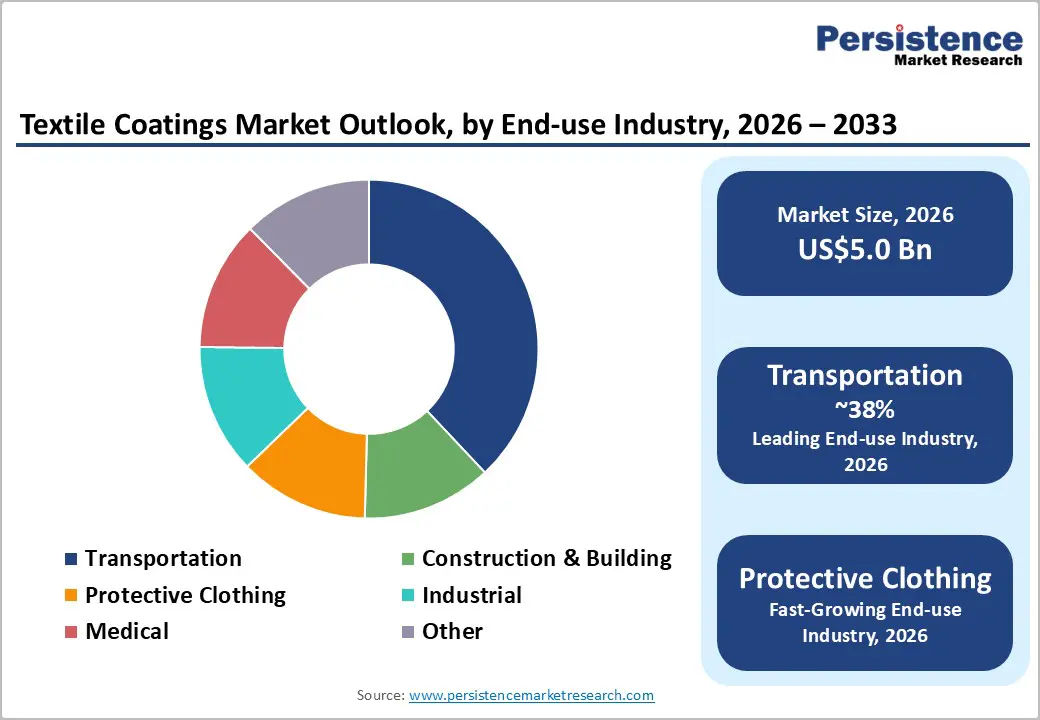

The global textile coating market size is supposed to be valued at US$ 5.0 Bn in 2026 and is projected to reach US$ 6.8 Bn by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

Market expansion is primarily driven by increasing demand for functional textiles with enhanced durability, water resistance, and flame retardancy across the transportation and industrial sectors. The growing adoption of protective clothing in manufacturing facilities, coupled with stringent safety regulations and increased investment in technical textile development, particularly in the Asia-Pacific region, are key factors supporting sustained market growth. Rising consumer awareness regarding sustainable and eco-friendly coating formulations, combined with technological advancements in polymer-based solutions, further accelerates market momentum.

Key Market Highlights:

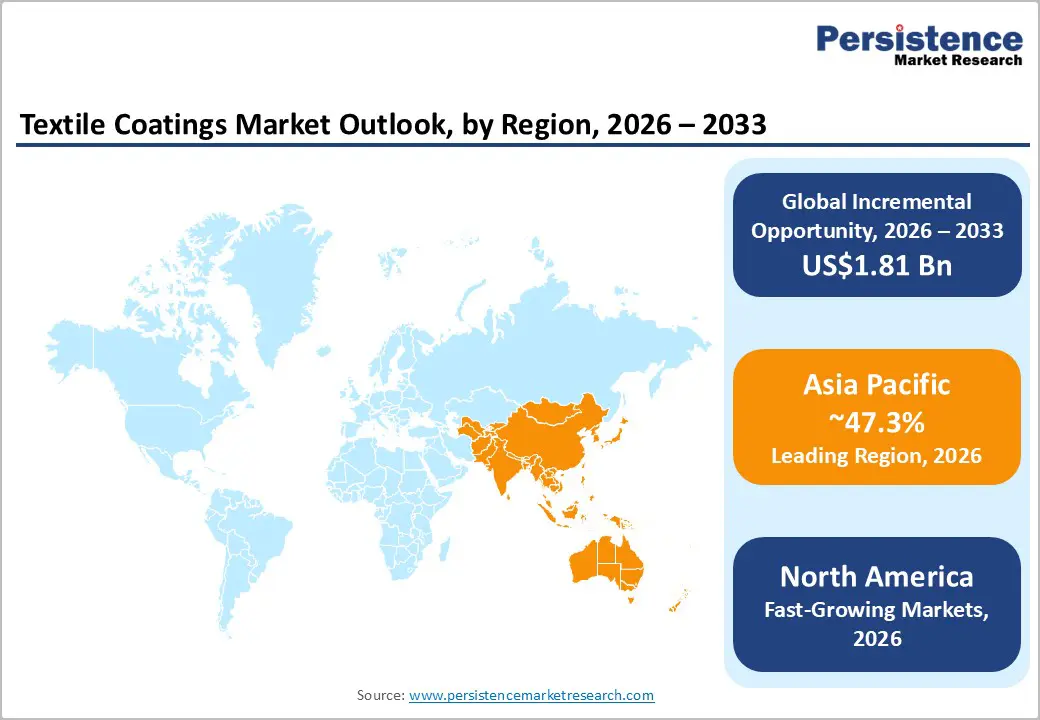

- Leading Region: Asia Pacific leads the market, with 47.3% market share, due to its dominance in global textile manufacturing and rapid infrastructure growth in China and India.

- Fastest Growing Region: North America emerges as the fastest growing region, supported by advanced technical textile infrastructure and robust research capabilities that drive innovation-led growth.

- Dominant Segment: Thermoplastic coatings command approximately 55% market revenue share, representing the dominant polymer category due to exceptional versatility, cost-effectiveness, superior flexibility, and ease of application across diverse textile substrates.

- Fastest Growing Segment: Protective Clothing is the fastest-growing application segment, driven by stricter global safety regulations and healthcare needs.

- Key Market Opportunity: The development and commercialization of bio-based, sustainable coatings and the integration of smart textiles represent primary growth opportunities, creating a significant addressable market for manufacturers that combine sustainability with advanced functionality.

| Key Insights | Details |

|---|---|

| Textile Coating Size (2026E) | US$ 5.0 Bn |

| Market Value Forecast (2033F) | US$ 6.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.5% |

| Historical Market Growth (2020 - 2025) | 3.8% |

Market Dynamics

Drivers - Increasing Demand for Protective and Functional Textiles

The growing demand for advanced protective textiles across diverse industrial sectors serves as a primary driver of the textile coating market. Protective clothing applications, including chemical-resistant garments, account for a substantial share of overall consumption, as end users seek coatings that provide superior barrier performance, flame resistance, and thermal protection.

Heightened workplace safety regulations, particularly in developed economies, mandate the use of advanced protective equipment, prompting manufacturers to invest in innovative coating technologies that enhance durability while ensuring comfort and breathability. Furthermore, compliance with regulatory frameworks such as OSHA standards and EU chemical safety directives continues to sustain global demand for specialized textile coatings.

Expansion of the Automotive and Transportation Sector

The transportation sector, encompassing automotive, aerospace, and maritime applications, has emerged as the fastest-growing end-use category for textile coatings. Coated textiles are widely used in automotive interiors, including seat covers, airbags, door panels, and protective coverings, where they provide essential properties such as durability, fire resistance, and abrasion resistance. Polyurethane (PU) coatings dominate this segment due to their exceptional flexibility, impact resistance, and superior performance in harsh environmental conditions.

As automotive manufacturers increasingly prioritize vehicle safety standards, particularly FMVSS regulations and ECE regulations in Europe, demand for specialized coating solutions continues to rise. Furthermore, the growing trend toward electric vehicles necessitates lightweight materials with enhanced thermal management properties, driving innovation in thermoplastic and thermoset-based textile coatings specifically designed for next-generation automotive applications.

Restraint - Stringent Environmental Regulations and REACH Compliance

Escalating environmental regulations regarding volatile organic compound (VOC) emissions present significant challenges for textile coating manufacturers, particularly in developed markets. The European Union's Directive 2004/42/EC, commonly referred to as the Paints Directive, establishes maximum VOC limits ranging from 30 g/L for water-based primers to 850 g/L for preparatory coatings, thereby requiring manufacturers to reformulate existing products and to invest substantially in research and development. Similarly, the United States Environmental Protection Agency (EPA) enforces strict VOC regulations under 40 CFR 59, mandating continuous monitoring and compliance documentation.

These regulatory constraints increase production costs and necessitate a transition toward water-based and solvent-free coating formulations, which often require significant infrastructure investments and process modifications. Regulatory bodies across the Asia-Pacific region are progressively implementing stricter environmental standards, creating compliance complexities for multinational manufacturers operating across diverse jurisdictions and increasing operational costs.

Price Volatility of Raw Materials and Supply Chain Disruptions

Fluctuating prices of key raw materials, including polyurethane resins, polyester resins, and specialized polymers, directly affect the economics and profitability of textile coating manufacturing. Raw material costs typically represent 40-50% of total production expenses, making manufacturers vulnerable to commodity price volatility. Global supply chain disruptions have intensified material scarcity and elevated procurement costs, particularly for specialty polymers sourced from limited suppliers.

Furthermore, geopolitical tensions, trade tariffs, and logistics bottlenecks have constrained the availability of critical inputs, forcing manufacturers to maintain higher inventory levels and accept unfavorable procurement terms. These cost pressures are particularly acute for small and mid-sized coating manufacturers lacking the scale and financial resources to absorb price fluctuations, thereby limiting their competitive positioning and market share growth.

Opportunity - Development of Bio-Based and Sustainable Textile Coating Solutions

The shift toward circular economy principles and sustainability-focused consumer preferences is creating significant growth opportunities for manufacturers developing eco-friendly textile coating solutions. Covestro AG exemplifies innovation in this space with Impranil® CQ DLU, a partially bio-based polyurethane dispersion containing 34% renewable carbon, highlighting strong market potential for sustainable alternatives. The global sustainable textile chemicals market expanded, driven by rising consumer and brand-owner demand for environmentally responsible products.

Regulatory incentives in the European Union and the U.S. further encourage the adoption of bio-based formulations, fostering favorable conditions for innovation. Companies investing in water-based, low-VOC coatings and advanced technologies, such as microencapsulation and nanotechnology, are well-positioned to capture market share. Emerging applications in hometech textiles, including smart temperature-regulating fabrics and antimicrobial coatings, represent a promising long-term growth segment.

Rapid Expansion of Smart Textiles and Advanced Functional Applications

The integration of coating technologies with smart textiles presents a transformative growth opportunity as industries increasingly adopt sensor-enabled garments and adaptive materials. The global smart textile market continues to expand, driven by advancements in conductive fibers, bio-sensing capabilities, and real-time data transmission. Textile coatings facilitate the incorporation of phase-change materials for thermal regulation, antimicrobial agents for hygiene, and conductive polymers for wearable electronics.

High-growth applications include healthcare monitoring, sports analytics, and industrial safety, where specialized coatings maintain breathability while delivering advanced functionality. Nanotechnology-based coatings featuring graphene, silver nanoparticles, and biodegradable antimicrobial agents are accelerating innovation and creating premium product opportunities. Rising adoption across the medical, defense, and sports sectors, coupled with consumer willingness to pay for functionally enhanced apparel, positions this segment as a critical driver for coating solution providers.

Category-wise Analysis

Polymer Type Insights

Thermoplastic coatings hold a dominant position in the textile coating market, accounting for approximately 55% of total revenue and representing the fastest-growing polymer category. Their popularity stems from superior versatility and high-performance attributes essential for modern textile applications, including exceptional flexibility, cost-efficiency, and ease of application across varied substrates. Among thermoplastics, polyvinyl chloride (PVC) and polyurethane (PU) are leading variants, with PU coatings prevailing due to outstanding moisture resistance, water repellency, and chemical durability.

Widespread adoption in automotive interiors, protective clothing, and industrial textiles underscores their strategic importance. Furthermore, thermoplastic coatings enable cost-effective production through direct and transfer coating processes, supporting rapid penetration in price-sensitive markets. The ability to reformulate solutions to meet evolving environmental regulations, such as water-based PU dispersions, reinforces their long-term relevance.

Industry Insights

The transportation industry remains the leading end-use segment in the textile coating market, accounting for approximately 38% of total revenue and exhibiting strong growth. This dominance is driven by extensive use of coated textiles in automotive seating, aircraft interiors, rail upholstery, and marine applications, where performance requirements include fire resistance, durability, abrasion resistance, and aesthetic appeal. Compliance with stringent safety standards, such as FMVSS 302 and European directives, requires advanced polymer-based coatings.

The automotive sector’s transition to electric vehicles further amplifies demand for lightweight fabrics with superior thermal management, creating opportunities for thermoplastic and polyurethane-based solutions. Industrial applications, including filters, conveyor belts, and protective barriers, constitute the second-largest segment, whereas medical textiles, such as wound dressings and orthopedic supports, are the fastest-growing subsegment, driven by regulatory mandates and rising demand for antimicrobial, breathable coatings.

Regional Insights

North America Textile Coating Market Trends

North America holds a strong position in the textile coating market, supported by advanced technical textile infrastructure and robust research capabilities that drive innovation-led growth. The region benefits from established aerospace and defense ecosystems, where specialized coatings for protective textiles and technical applications command premium demand. Leading aerospace manufacturers such as Boeing and Lockheed Martin, along with medical device companies, require high-performance coatings that meet stringent safety and regulatory standards, including EPA VOC limits and OSHA compliance.

Canada and Mexico contribute significantly through manufacturing scale and proximity to major end-use industries. A strong focus on sustainability, driven by LEED adoption and corporate environmental commitments, accelerates the transition to water-based and bio-based formulations. Strategic investments by major chemical companies in U.S. innovation centers further support the development of next-generation technologies.

Europe Textile Coating Market Trends

Europe is the most regulated textile coating market globally, with stringent environmental and safety directives driving innovation toward sustainable formulations. Germany, the U.K., France, and Spain collectively account for 40% of the region’s market volume, with Germany leading as a hub for technical textile innovation and automotive supply. Compliance with EU Paints Directive VOC limits, along with REACH and Construction Products Regulation, necessitates significant investment in low-VOC and water-based coating technologies.

France and the U.K. maintain strong automotive and aerospace manufacturing bases, reinforcing demand for high-performance coatings. The European Green Deal’s emphasis on circular economy principles accelerates the development of recyclable and bio-based solutions. Strategic partnerships between chemical manufacturers and textile producers foster technology transfer and product innovation.

Asia Pacific Textile Coating Market Trends

Asia Pacific is the fastest-growing regional market, accounting for approximately 47.3% of global coated textile revenue in 2024 and serving as the primary growth driver for international manufacturers. China dominates production, accounting for 65% of global textile coating output and consuming about 25% domestically, reinforcing its role as a critical hub for global supply chains. China’s textile sector continues to expand, supported by rising domestic demand and export growth. Its leadership in polyurethane utilization, accounting for nearly 90% of global PU textile coatings, underscores its strategic importance.

India ranks second, leveraging skilled labor and cost-efficient manufacturing to capture market share. Japan and South Korea lead in technology, specializing in advanced coatings for automotive and medical applications. Rapid urbanization, industrialization, and growing automotive production across Southeast Asia further fuel demand, while rising incomes and stricter safety standards accelerate the adoption of protective and industrial textiles.

Competitive Landscape

The global textile coatings market is moderately consolidated, dominated by established multinational chemical manufacturers alongside specialized regional players. Leading companies such as Covestro AG, BASF SE, Solvay SA, and Huntsman International LLC maintain significant market share through extensive product portfolios, global production capabilities, and strong research and development initiatives. Market dynamics increasingly emphasize innovation, sustainability, and regulatory compliance as key differentiators. Smaller manufacturers typically compete on cost efficiency and regional specialization, focusing on niche applications or geographic markets. Strategic mergers and acquisitions remain prevalent, enabling major players to expand portfolios and geographic reach. The competitive landscape is shifting toward eco-friendly formulations, smart textile integration, and customized solutions tailored to specific client requirements.

Key Market Developments

- March 2025: BASF unveiled innovative chemical recycling technology that transforms textile waste into new polyamide 6 fibers with identical quality and 70% lower CO2 emissions, addressing circular economy requirements and sustainability mandates for apparel and technical textile manufacturers.

- April, 2024: Solvay SA inaugurated its new Alve-One® production unit in Rosignano, Italy. This facility produces eco-designed chemical blowing agents for thermoplastic foams, offering a safer alternative to hazardous additives in coated textile applications.

- February, 2023: Archroma officially completed the acquisition of the Textile Effects business from Huntsman International LLC. This merger created a comprehensive portfolio of textile chemicals and dyes, significantly strengthening Archroma's position in the coating and finishing market.

Top Companies in Textile Coating

- Covestro AG (Germany) is a leading global supplier of high-tech polymer materials. In the textile coating space, they are renowned for their INSQIN® technology, which enables water-based, solvent-free PU coatings. The company is aggressively pursuing a circular economy strategy, focusing on bio-based raw materials to reduce the carbon footprint of textile manufacturing.

- BASF SE (Germany) is the world's largest chemical producer. Their portfolio includes a vast range of dispersions, additives, and resins for textile coatings. BASF leverages its "Verbund" system to achieve operational efficiency. Recently, they have focused on "biomass balance" approaches, in which renewable feedstocks are integrated into the production chain to deliver sustainable, certified products.

- Solvay SA (Belgium) specializes in advanced materials and specialty chemicals. They are a key player in high-performance coatings, particularly for flame retardancy and water repellency. Solvay distinguishes itself through its "Solvay One Planet" sustainability roadmap, developing products like Amni Soul Eco® that address the end-of-life environmental impact of textiles.

Companies Covered in Textile Coating Market

- Covestro AG

- Solvay SA

- BASF SE

- Sumitomo Chemical Co., Ltd.

- The Lubrizol Corporation

- Arkema

- Clariant

- Huntsman International LLC

- OMNOVA North America Inc.

- Tanatex Chemicals B.V.

- Formulated Polymer Products Ltd.

Frequently Asked Questions

The global textile coatings market is projected to reach US$ 6.8 billion by 2033, expanding from US$ 5.0 billion in 2026, representing a 4.5% CAGR during the forecast period, driven by escalating demand for functional textiles across transportation, protective clothing, and industrial applications.

Primary demand drivers include increasing necessity for protective textiles across manufacturing and industrial sectors, expansion of automotive and aerospace industries requiring advanced coating solutions, and rising adoption of technical textiles with flame-retardant and water resistance properties.

Thermoplastic coatings, particularly polyurethane (PU) based variants, dominate the market with approximately 55% market revenue share for thermoplastics, due to superior versatility, flexibility, cost-effectiveness, and exceptional performance characteristics across diverse end-use applications.

Asia-Pacific commands approximately 47.3% of the global coated textiles market revenue in 2026, with China accounting for 65% global production and India emerging as the fastest-growing market.

The development and commercialization of sustainable, bio-based coating formulations and integration of advanced technologies, including smart textiles, antimicrobial functionalities, and thermo-regulating capabilities, represent primary growth opportunities.

Key players include Covestro AG, BASF SE, Solvay SA, The Lubrizol Corporation, and Huntsman International LLC among others.