- Inks, Coatings, Adhesives & Sealants (ICAS)

- Hull Coatings Market

Hull Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

Hull Coatings Market by Product Type (Self-polishing Coatings SPCs, Fouling Release Coatings FRC, Others), Applications (Rings, Vessels, Liquefied Natural Gas Carriers, Others), and Regional Analysis for 2026 - 2033

Hull Coatings Market Size and Trends Analysis

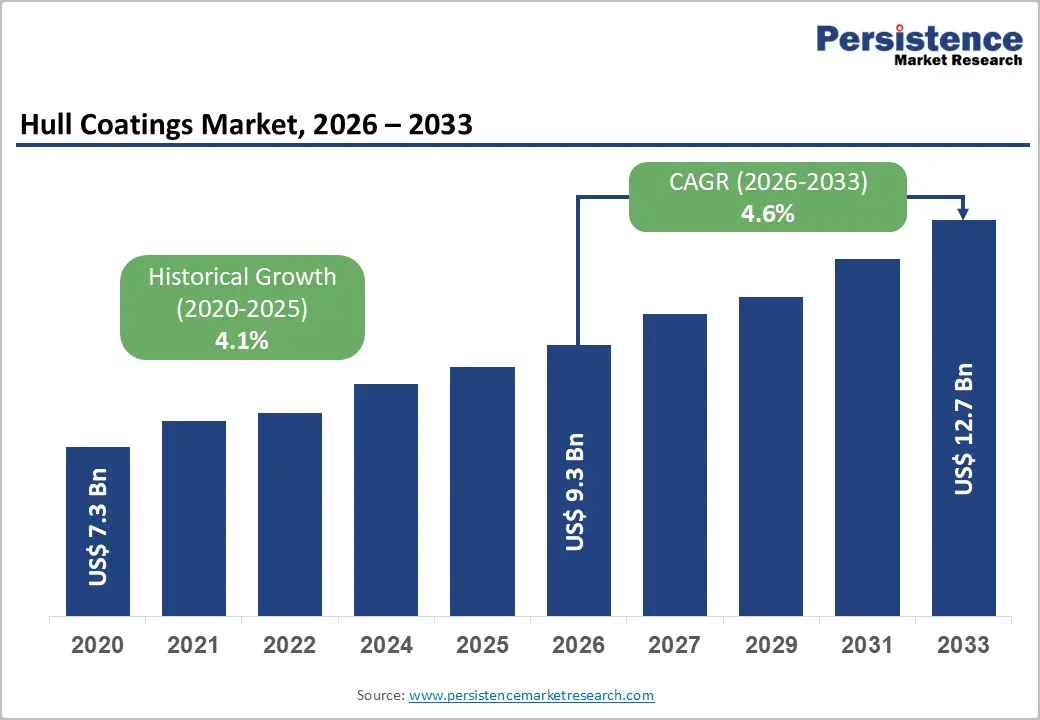

The global hull coatings market size is likely to be valued at US$9.3 billion in 2026, and is expected to reach US$12.7 billion by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of IMO 2020 sulfur cap compliance, rising focus on hull performance optimization, and growing demand for low-friction, antifouling coatings to reduce fuel consumption in commercial shipping.

Rising demand for high-performance hull coatings, particularly fouling-release coatings (FRCs) for vessels and LNG carriers, is driving greater adoption among shipowners and operators. Innovations in silicone-based FRCs, biocide-free self-polishing copolymers (SPCs), and nano-structured surface technologies are further accelerating uptake by delivering enhanced drag reduction and longer dry-docking cycles. Growing awareness of hull coatings as a key enabler of fuel efficiency, emissions reduction, and lower operating costs, especially within green shipping initiatives and expanding LNG fleets, continues to propel market growth.

Key Industry Highlights:

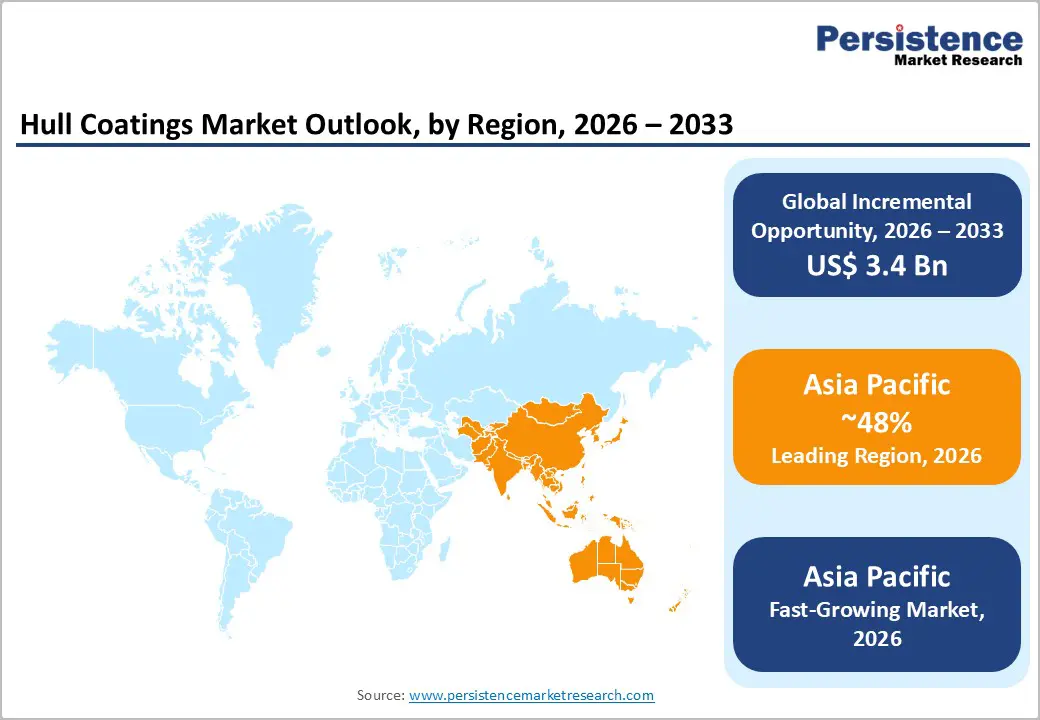

- Leading Region: Asia Pacific, anticipated to account for a 48% market share in 2026, driven by dominant shipbuilding activity, a large merchant fleet, and strong demand in China, South Korea, and Japan.

- Fastest-growing Region: Asia Pacific, fueled by rapid fleet expansion, increasing LNG carrier orders, and growing retrofitting of eco-friendly coatings.

- Dominant Product Type: Self-polishing Coatings (SPCs), to hold approximately 52% of the market share, as they remain the workhorse for most commercial vessels.

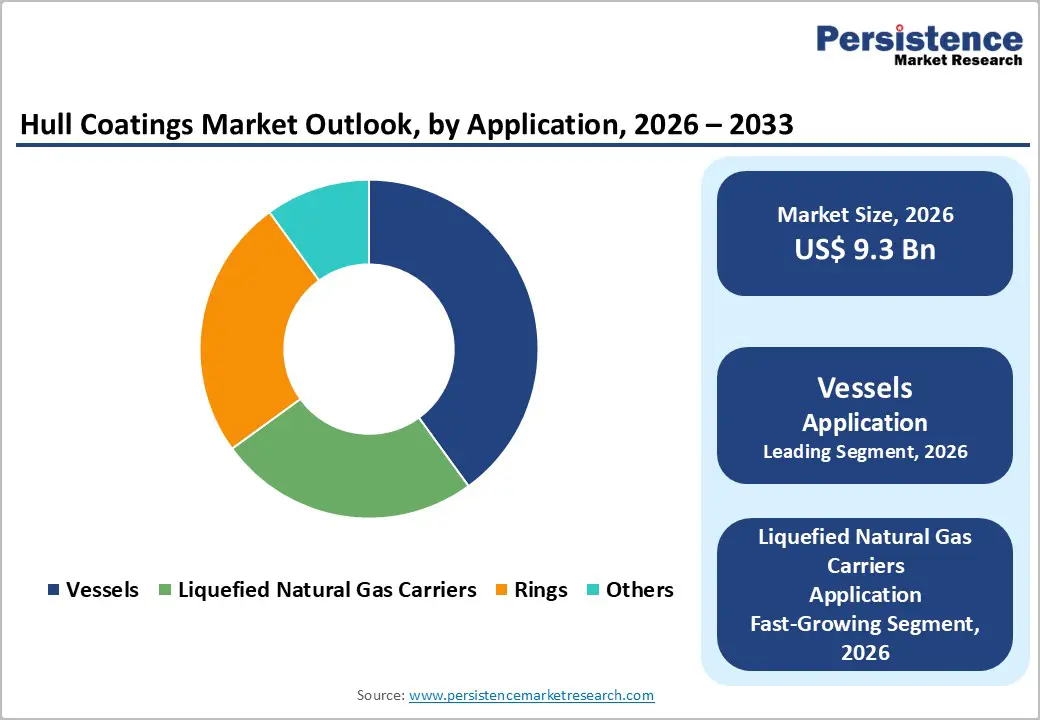

- Leading Application: Vessels, contributing nearly 68% of the market revenue, due to the highest volume of merchant ships and tankers.

- Cybutryne Ban Amendment (2023): In 2021, the IMO amended the AFS Convention to ban the application or re-application of hull coatings containing the biocide cybutryne as of 1 January 2023. Ships with existing cybutryne coatings must remove or seal them by the next scheduled renewal survey, but no later than 60 months after the last application.

| Key Insights | Details |

|---|---|

|

Hull Coatings Market Size (2026E) |

US$9.3 Bn |

|

Market Value Forecast (2033F) |

US$12.7 Bn |

|

Projected Growth CAGR (2026-2033) |

4.6% |

|

Historical Market Growth (2020-2025) |

4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - IMO Regulations and Fuel Efficiency Imperatives

International maritime emissions rules and energy-efficiency targets have been tightened to curb air pollution and cut fuel use across the global fleet, prompting shipowners to adopt advanced hull coatings that limit biofouling and drag. The International Maritime Organization (IMO) adopted binding carbon-intensity measures under MARPOL Annex VI, requiring operational efficiency improvements across vessels engaged in international trade. The U.K. Government (Department for Transport) policy brief reported that shipping accounted for 3% of global CO2 emissions in 2018, reinforcing regulatory pressure to deploy drag-reducing technologies that deliver measurable fuel savings and emissions cuts.

Fuel-efficiency mandates are being translated into national compliance frameworks that elevate the commercial value of high-performance antifouling and foul-release coatings. Guidance issued by the U.S. Government (Environmental Protection Agency) documented that hull fouling can raise vessel fuel consumption by up to 40%, validating coatings as a near-term lever for efficiency gains and regulatory compliance. Operators pursuing carbon-intensity targets, port-state control conformity, and lower bunker exposure are prioritizing coatings with longer service intervals and smoother finishes, driving sustained demand across newbuilds and dry-docking maintenance cycles.

Technological Advancements in Coating Chemistry

Technological progress in coating chemistry is lifting performance standards for hull protection by pairing low-friction surfaces with durable fouling resistance. Modern formulations engineer ultra-smooth polymer matrices that cut boundary-layer turbulence, lowering hydrodynamic drag and steady-state fuel burn across operating profiles. Controlled-release antifouling systems meter active ingredients at predictable rates, extending service intervals and keeping surfaces cleaner for longer periods at sea. Hybrid foul-release chemistries combine elastomeric backbones with silicone or fluoropolymer segments to discourage organism attachment while maintaining mechanical toughness under abrasion during port maneuvers and dry-dock cycles.

Material science advances also aim to improve environmental compliance and lifecycle efficiency. Waterborne and high-solids systems trim solvent loads, supporting stricter discharge rules and safer application conditions. Nanostructured fillers tune surface energy and micro-roughness, sustaining smoothness after months of exposure to cavitation, debris, and variable salinity. Self-polishing mechanisms refresh the outer layer under shear forces, preserving consistent performance between dockings. Formulators refine crosslink density and cure kinetics to shorten turnaround time in yards without sacrificing adhesion on steel or composite substrates.

Barrier Analysis - High Upfront Cost and Long Payback Periods

High initial investments and prolonged return on investment can act as a restraint for the uptake of advanced hull coatings, particularly for smaller operators or vessels with lower utilization. Premium antifouling and foul-release systems often cost significantly more at the time of dry-docking than standard coatings, with capital outlay varying widely by vessel size and product choice, from tens of thousands to several hundred thousand U.S. dollars in incremental coating cost for high-performance options relative to basic coatings. Government technical guidance on energy efficiency measures acknowledges that such coatings are a capital expense every dry-dock cycle, and the difference between standard and advanced hull coating systems can range from approximately US$30,000 to US$600,000, depending on vessel dimensions and product selected. Although the long-term fuel savings from reduced friction and fouling are quantifiable, the upfront cost can deter shipowners who must weigh it against near-term budget constraints.

Payback periods hinge on a vessel’s operating profile and fuel price environment. According to the U.S. Government (Maritime Administration) technical material, typical reductions in hull resistance may translate into modest energy demand drops of 1–4% in total fuel consumption when comparing a well-maintained coating to less effective alternatives, making it challenging to recoup significant coating premiums in scenarios with limited sailing time or lower fuel costs. As a result, operators with intermittent use or older tonnage may defer or downgrade coating investments to manage cash flow, dampening broader adoption of high-performance coatings despite their environmental and operational benefits.

Regulatory Uncertainty and Biocide Restrictions

Varying regulatory frameworks and evolving restrictions on harmful biocides create uncertainty that restrains innovation and deployment of hull coatings. Governments and international bodies have tightened rules on substances historically used to prevent biofouling on vessel hulls. For instance, the International Maritime Organization’s International Convention on the Control of Harmful Anti-fouling Systems on Ships (AFS Convention) banned the use of cybutryne as a biocidal antifouling agent globally as of January 2023, reflecting environmental concerns about persistence and toxicity in marine ecosystems. This has forced coating manufacturers to reformulate products or seek alternative chemistries that must be evaluated against emerging standards in major markets such as the EU, the U.S., and other nations with their own approval processes, complicating product development and market entry.

Differing regulatory approaches across jurisdictions further compound compliance risk for global operators and suppliers. In the EU, broad biocidal product regulations and reviews of active compounds have led to the prohibition of some biocidal coatings and to tighter scrutiny of copper-based systems widely used for fouling control. Shipowners and coating developers face a patchwork of approval requirements, varying timelines, and uncertain future limits on key active ingredients. This fragmentation slows the adoption of new technologies and can dissuade investment in innovative solutions due to the high costs and lengthy approval cycles required to demonstrate environmental safety and efficacy across multiple regulatory environments.

Opportunity Analysis - Advancements in Biocide-Free FRC and Nano-Structured Hull Coatings

Advances in biocide-free foul-release coatings (FRCs) and nano-structured hull coatings offer a significant opportunity for the hull coatings market by combining environmental friendliness with improved vessel performance. Biocide-free FRCs minimize the release of toxic substances into marine environments, aligning with stricter regulations that favor non-toxic solutions such as silicone-based foul-release surfaces. U.S. technical guidance on marine energy efficiency states that effective antifouling coatings can reduce hull resistance and contribute to overall fuel savings, with reductions in total energy demand of up to 10% compared to standard coatings in some cases, indicating the potential operational gains from advanced coating technologies.

Nano-structured coatings enhance surface characteristics at micro- and nanoscales, creating ultra-smooth, low-adhesion surfaces that disrupt biofouling settlement and reduce drag. Government sources highlight this trend toward coatings that improve fuel efficiency and lower hydrodynamic resistance, key drivers for ship operators aiming to reduce fuel costs and emissions within regulatory frameworks. FRCs and nano-coatings support longer service intervals, reducing dry-dock frequency and maintenance overheads, while simultaneously enabling compliance with environmental mandates that encourage reduced reliance on biocidal agents. These innovations bridge sustainability and efficiency goals, presenting a compelling value proposition for newbuilds and retrofit programmers seeking long-term cost savings and performance improvements.

Expansion in LNG Carrier Newbuilds and Retrofit Market

Growth in liquefied natural gas (LNG) carrier newbuild orders and retrofit activity is creating a meaningful opportunity for the hull coatings market by boosting demand for high-performance, fuel-efficient antifouling and foul-release systems. LNG trade has expanded rapidly as nations diversify energy sources and shift toward lower-carbon fuels, prompting shipowners to order new LNG carriers with larger capacities and more advanced propulsion systems. These vessels operate at sea for extended periods and at steady service speeds, making drag reduction and fouling control critical contributors to operational efficiency and bunker cost management. Ship designers and owners prioritize coatings that maintain smooth hull surfaces over long voyages to protect efficiency gains afforded by modern hull forms and propulsion configurations.

The retrofit market also contributes to sustained coatings demand as existing LNG carriers undergo life-extension upgrades or compliance-oriented enhancements during scheduled dry-dock windows. Retrofitting advanced hull coatings to older tonnage helps operators improve hydrodynamic performance and approach the efficiency levels of newer vessels without the capital expense of replacement. LNG carriers often face strict environmental and safety regulations at their ports of call, motivating maintenance regimes that include state-of-the-art hull protection.

Category-wise Analysis

Product Type Insights

Self-polishing coatings (SPCs) are anticipated to dominate the market, accounting for approximately 52% of the market share in 2026. Their dominance is driven by the fact that they maintain an actively renewing surface that continually exposes fresh, smooth layers during vessel operation. Unlike traditional antifouling paints that rely on passive leaching of biocides, SPCs use controlled hydrolysis to shed worn layers in a predictable way, reducing biofouling buildup and hydrodynamic drag over longer service intervals. This performance advantage translates into more consistent fuel savings and fewer dry-dock repaint cycles, making SPCs especially attractive for large commercial vessels with high utilization. Maersk Line is applying Jotun’s SeaQuantum X200 self-polishing antifouling system across its Triple-E series of large container ships to enhance fuel efficiency and maintain hull smoothness over long service periods. The SeaQuantum range, based on advanced silyl acrylate technology, offers controlled erosion and sustained fouling control, helping these vessels optimize operational performance and reduce fuel costs over dry-dock intervals.

Fouling release coatings (FRC) represent the fastest-growing product type, as they minimize organism adhesion without relying heavily on traditional biocides, creating ultra-smooth, low surface-energy layers that organisms cannot easily cling to. Vessels with FRCs tend to stay cleaner at sea, reducing hydrodynamic resistance and improving fuel efficiency on long voyages. Their suitability for a range of vessels from containerships to LNG carriers and compatibility with stricter environmental rules on toxic additives further boost adoption. Carisbrooke Shipping Ltd is choosing AkzoNobel’s Intersleek 1100SR biocide-free foul release coating for its Jasmine C vessel to improve hull smoothness and drive fuel efficiency gains. This silicone-based FRC has been specifically applied to reduce underwater hull roughness and lower fuel consumption, marking a significant operational move toward sustainable fouling control technology for the operator’s fleet.

Applications Insights

The vessels segment is expected to dominate the market, accounting for nearly 68% of revenue in 2026, driven by demand, as commercial ships account for the largest share of coated surface area and maintenance cycles. Large fleets of container ships, tankers, bulk carriers, and gas carriers undergo routine dry-docking that requires full underwater hull recoating to control biofouling and preserve hydrodynamic performance. High utilization profiles mean small efficiency gains translate into meaningful fuel savings over long voyages, making premium antifouling and foul-release systems standard on vessels. BW LPG is a leading global owner and operator of liquefied petroleum gas vessels. BW LPG signed an agreement to apply Jotun’s Hull Performance Solutions (HPS) coatings across 38 of its LPG vessels to maintain low hull fouling and sustain operational efficiency over multi-year dry-dock cycles. The coated fleet has shown sustained hull performance with minimal speed loss and has helped enhance fuel savings by reducing resistance during service.

Liquefied natural gas carriers are the fastest-growing application, driven by global demand for LNG transport, which is expanding with energy diversification and fuel transition strategies. These vessels operate at high service speeds and long durations, where even small reductions in hull roughness can yield meaningful fuel savings over long-distance voyages. Operators of LNG carriers are prioritizing advanced antifouling and foul-release systems to preserve hull smoothness and manage lifecycle costs, especially on larger, modern units with sophisticated propulsion. MOL LNG Transport (Europe) Limited’s Al Deebel, an LNG carrier that received Jotun’s SeaQuantum X200 high-performance coating system during dry-dock. The coating package, including antifouling and anticorrosive layers, was selected to enhance fouling protection and maintain low speed loss over long voyages, a key priority for LNG carriers operating at high service speeds and on global trade routes.

Regional Insights

North America Hull Coatings Market Trends

North America is driven by the region’s large tanker and bulk carrier fleet, strong environmental regulations, and high public awareness of fuel-saving benefits. Distribution systems in the U.S. and Canada provide extensive support for hull coatings programs, ensuring wide accessibility across FRC, vessels, and shipyards. The increasing demand for biocide-free, convenient, and easy-to-apply forms is further accelerating adoption, as these formats improve efficiency and reduce the barriers associated with traditional coatings.

Innovation in hull coatings technology, including stable silicone FRC, improved nano-structured delivery, and targeted LNG carrier enhancement, is attracting significant investment from both public and private sectors. Government initiatives and EPA/IMO campaigns continue to promote use against emissions risks, fuel-cost concerns, and emerging green shipping threats, creating sustained market demand. The growing focus on retrofit grades and specialty uses, particularly for vessels and others, is expanding the target applications for hull coatings.

Europe Hull Coatings Market Trends

Europe is seeing significant growth driven by increased awareness of green shipping benefits, strong regulatory systems, and government-led FuelEU Maritime programs. Countries such as Greece, Norway, Germany, and Denmark have well-established shipping frameworks that support routine hull coatings use and encourage the adoption of innovative antifouling delivery methods, including biocide-free FRC. These high-performance formulations are particularly appealing for vessel populations, regulation-conscious owners, and LNG operators, improving fuel efficiency and coverage rates.

Technological advancements in hull coatings development, such as enhanced silicone FRC, application-targeted delivery, and improved nano-structured grades, are further boosting market potential. European authorities are increasingly supporting research and trials for coatings against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-friction options is aligned with the region’s focus on preventive emissions reduction and EEXI/CII compliance. Public awareness campaigns and promotional drives are expanding reach across both the tanker and container segments, while suppliers are investing in sustainable formulations and novel variants to increase efficacy.

Asia Pacific Hull Coatings Market Trends

Asia Pacific is projected to dominate and experience the fastest growth, capturing the 48% revenue share in 2026, driven by rising shipbuilding awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, South Korea, Japan, and Singapore are actively promoting coatings campaigns to address fleet efficiency and emerging green shipping needs. Hull coatings are particularly attractive in these regions due to their cost-effective administration, ease of application, and suitability for large-scale newbuild and retrofit drives in both tanker and container fleets.

Technological advancements are enabling the development of stable, effective, and easy-to-apply hull coatings that can withstand challenging operational conditions and minimize reliance on fouling. These innovations are critical for reaching domestic shipyards and improving overall fleet efficiency. The growing demand for FRC, vessels, and SPC applications is driving market expansion. Public-private partnerships, increased shipping expenditure, and rising investment in coatings research and application capacity are further accelerating growth. The convenience of coatings delivery, combined with improved fuel savings and reduced emissions, positions it as a preferred choice.

Competitive Landscape

The global hull coatings market is characterized by intense competition between established marine paint leaders and emerging green-technology specialists, each striving to deliver innovative solutions that meet evolving environmental and operational demands. In Europe and Asia Pacific, AkzoNobel N.V. and Jotun dominate through strong investments in R&D, extensive dry-dock networks, and longstanding relationships with shipowners, enabling rapid adoption of advanced products such as fouling release coatings (FRCs) and biocide-free self-polishing coatings (SPCs). These technologies not only reduce underwater hull roughness but also support fuel efficiency and emissions reduction, aligning with international maritime regulations.

In North America, PPG Industries Inc. leverages localized solutions and service support to improve accessibility and adoption across diverse fleets, particularly for commercial vessels operating in coastal and offshore routes. FRCs, with their low-friction and environmentally friendly properties, enhance operational efficiency by lowering hydrodynamic drag, decreasing fuel consumption, and reducing emissions risks. Strategic partnerships, collaborations, and acquisitions among coating manufacturers combine technical expertise, broaden product portfolios, and accelerate the commercialization of next-generation solutions.

Key Industry Developments:

- In June 2025, Hempel announced that its market-leading Hempaguard range was expanded with the launch of Hempaguard NB, a high-performance silicone hull coating designed specifically for newbuild vessels. For the first time, Hempaguard’s trusted fuel savings and fouling protection were made available to shipowners and shipyards during the construction phase, marking a significant step forward in hull coating innovation.

- In June 2025, Jotun, a global leader in marine coatings, announced that the next generation of its Hull Performance Solutions (HPS) was launched. Included in HPS 2.0 were two new products tailored for different trades and environments, alongside the established and newly speed-loss verified SeaQuantum X200. Best-in-class technical service, hull condition management, and performance guarantees were provided to deliver a solution that was tailored to specific trade requirements.

Companies Covered in Hull Coatings Market

- AkzoNobel N.V.

- Axalta Coating Systems Ltd.

- Chugoku Marine Paints Ltd.

- Hempel A/S

- Jotun

- KCC Corporation

- NIPSEA Group

- PPG Industries Inc.

- The Sherwin-Williams Company

Frequently Asked Questions

The global hull coatings market is projected to reach US$9.3 billion in 2026.

Stricter international regulations on fuel efficiency, emissions, and biocidal antifouling agents, such as IMO’s MARPOL Annex VI and the AFS Convention, are compelling shipowners to adopt advanced hull coatings that reduce drag, improve fuel efficiency, and meet environmental mandates.

The hull coatings market is poised to witness a CAGR of 4.6% from 2026 to 2033.

The rapid growth of global LNG trade and fleet modernization offers opportunities for advanced hull coatings that enhance fuel efficiency, reduce fouling, and extend maintenance intervals on both newbuilds and retrofitted vessels.

AkzoNobel N.V., Jotun, Hempel A/S, PPG Industries Inc., and Chugoku Marine Paints Ltd. are the key players.