- Inks, Coatings, Adhesives & Sealants (ICAS)

- Solar Panel Coatings Market

Solar Panel Coatings Market Size, Share, and Growth Forecast 2026 - 2033

Solar Panel Coatings Market by Coating Type (Anti-reflective, Hydrophobic, Self-cleaning, Anti-soiling, Anti-abrasion), Material Type (Nanomaterial-Based Coatings, Metal Oxide Coatings: Titanium Dioxide/TiO₂, Silicon Dioxide/SiO₂, Magnesium Fluoride/MgF₂; Polymer-Based Coatings, Fluoropolymer Coatings, Polysiloxane Coatings, Others), Application End-User, and Regional Analysis for 2026 - 2033

Solar Panel Coatings Market Size and Trend Analysis

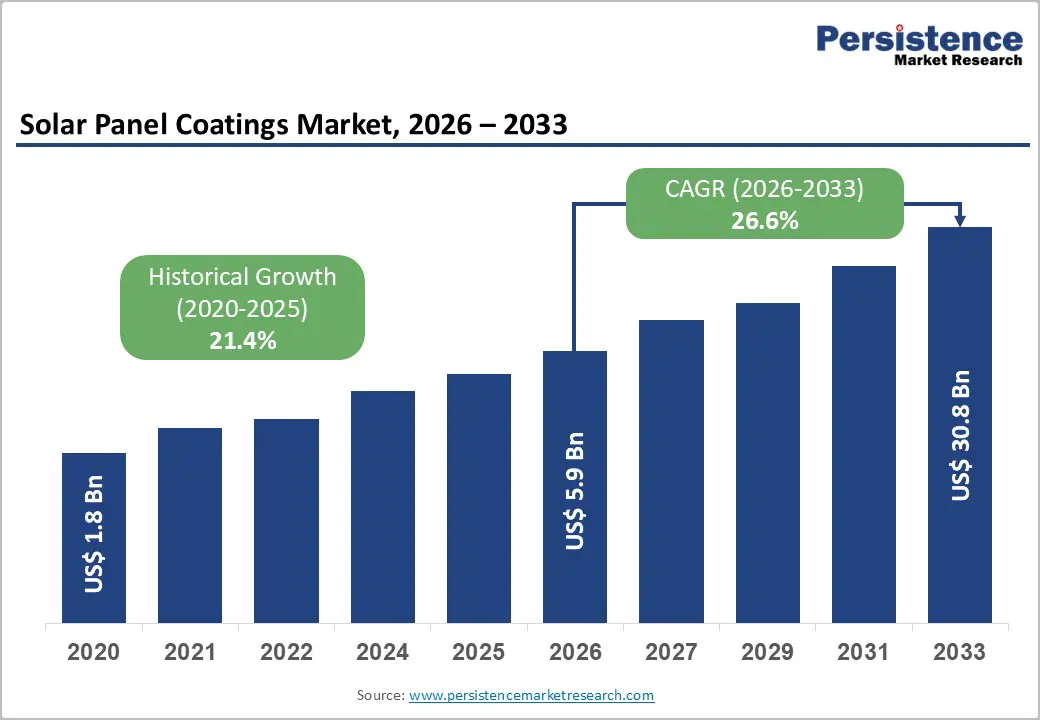

The global Solar Panel Coatings market size is supposed to be valued at US$ 5.9 Billion in 2026 and is projected to reach US$ 30.8 Billion by 2033, growing at a CAGR of 26.6% between 2026 and 2033.

The global Solar Panel Coatings market is experiencing one of the most explosive growth trajectories in the advanced materials sector, driven by the irreversible global acceleration in solar photovoltaic installation, the demonstrably proven efficiency and lifetime economics of high-performance anti-reflective, self-cleaning, and hydrophobic coatings, and the proliferation of next-generation solar cell architectures including perovskite solar cells and bifacial monocrystalline panels that require sophisticated protective coating chemistry to achieve commercial-grade durability.

Key Market Highlights

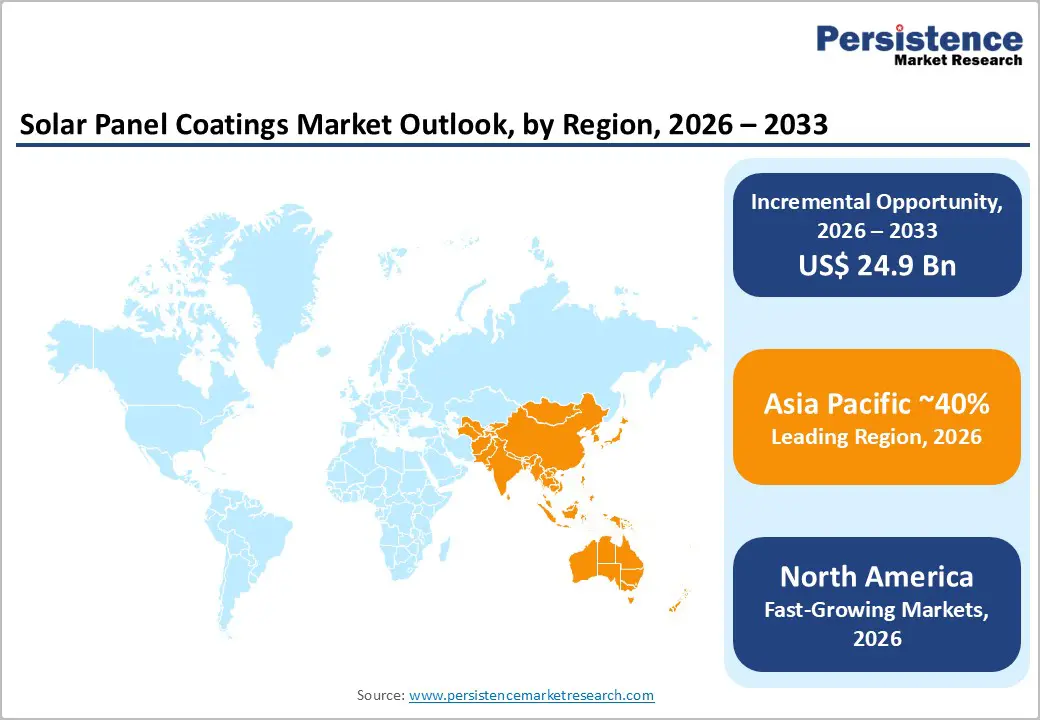

- Leading Region: Asia Pacific leads the global Solar Panel Coatings market, anchored by China's world-dominant 80%+ share of global solar panel manufacturing, 217 GW of Chinese domestic solar installations in 2023 documented by China's NEA, and AGC's and Sumitomo Chemical's Japan-headquartered premium coating supply platforms serving the world's largest solar manufacturing geography cluster.

- Fastest Growing Country: India is the fastest-growing region for Solar Panel Coatings, driven by India's MNRE target of 280 GW solar by 2030 under PLI-stimulated domestic manufacturing, and India's high-dust deployment environments making anti-soiling coating ROI economics particularly compelling for domestic installers.

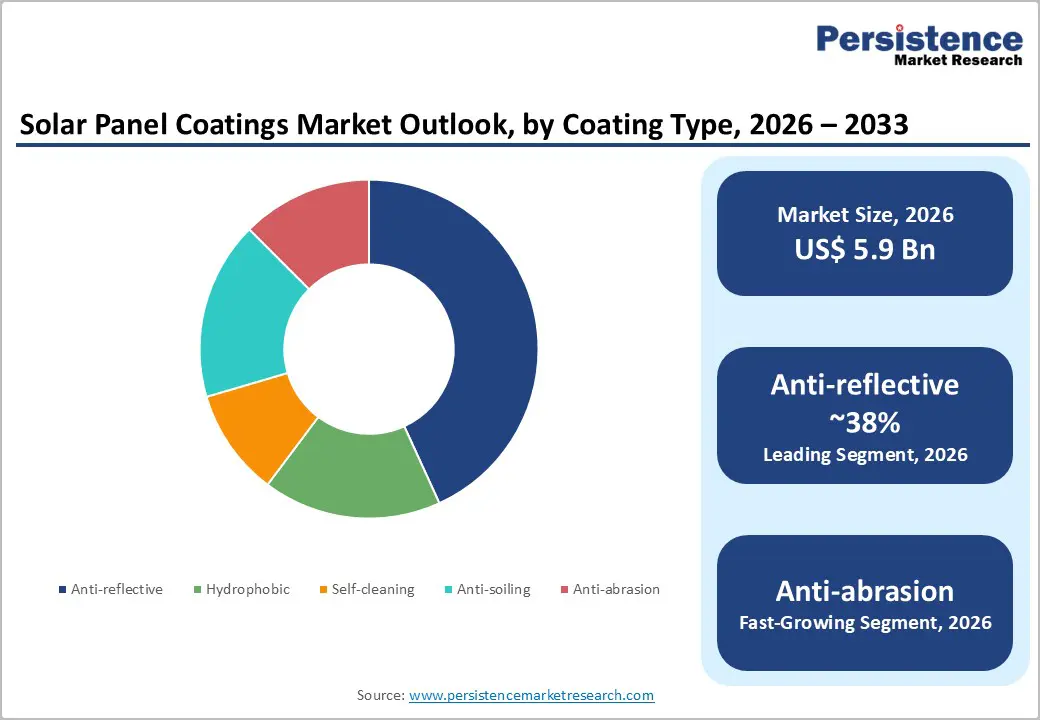

- Dominant Coating Type: Anti-reflective coatings dominate the Coating Type segment with approximately 38% revenue share, validated by pv magazine's August 2024 peer-reviewed field study documenting 5.5% higher electricity generation and 2.7% LCOE reduction at utility-scale installations, and by standard anti-reflective glass specification in virtually all premium monocrystalline PERC, TOPCon, and bifacial solar module manufacturing globally.

- Fastest Growing Application: Perovskite Solar Cells represent the fastest-growing Application segment, propelled by Northwestern University's 26.3% PCE achievement with tripled coating-enabled stability (November 2024), the international team's 27% PCE fluorinated coating breakthrough (January 2026), and NREL-certified perovskite efficiency milestones confirming imminent commercial module scale-up creating premium specialized coating chemistry demand.

- Key Market Opportunity: Agrivoltaics and BIPV represent the dual key market opportunities, with IRENA's documented 14+ GW global agrivoltaic deployment generating anti-soiling coating demand, the EU Solar Rooftop Initiative mandating building-integrated solar from 2026–2027, and premium BIPV architectural coating applications supplied by AGC's SUNMAX®, Saint-Gobain's ALBARINO®, and Guardian Glass serving structurally growing premium solar coating revenue pools through 2033.

| Key Insights | Details |

|---|---|

|

Solar Panel Coatings Market Size (2026E) |

US$ 5.9 Billion |

|

Market Value Forecast (2033F) |

US$ 30.8 Billion |

|

Projected Growth CAGR (2026–2033) |

26.6% |

|

Historical Market Growth (2020–2025) |

21.4% |

Market Dynamics

Drivers - Record Global Solar PV Capacity Additions and IEA-Documented 5,500 GW Deployment Trajectory Driving Structural Coating Demand Acceleration

The International Energy Agency (IEA)'s documentation of record 420 GW global solar PV capacity additions in 2023, surpassing all prior single-year deployment records, and its projection of cumulative global solar capacity reaching 5,500 GW by 2030 under announced government pledges are the most commercially significant demand drivers for the Solar Panel Coatings market, as each gigawatt of solar panel manufacturing and installation generates direct procurement demand for anti-reflective glass coatings, hydrophobic encapsulant coatings, and self-cleaning surface treatments applied during panel manufacturing or post-installation field application. Every modern solar module incorporates at least one coating layer, with premium bifacial monocrystalline panels incorporating 3–5 discrete coating layers, across anti-reflective front glass treatment, hydrophobic rear encapsulant protection, and UV-stabilizing frame sealant applications that collectively constitute the Solar Panel Coatings addressable market.

The Solar Energy Industries Association (SEIA) documented that the U.S. alone installed a record 32.4 GW of solar capacity in 2023, with the Inflation Reduction Act (IRA)'s 30% Investment Tax Credit (ITC) sustained through 2032 providing long-term investment certainty for U.S. solar project pipelines that directly sustain domestic coating procurement growth. 3M Company and PPG Industries are among the dominant global suppliers of anti-reflective and protective solar panel coating materials to the global solar PV manufacturing supply chain.

Perovskite Solar Cell Commercialization and Advanced Coating Science Creating Premium ESG Coating Demand Category

The commercialization of Perovskite Solar Cells and advances in coating science are emerging as a major driver for the global solar panel coatings market. Perovskite-based photovoltaic technology is gaining attention due to its high power-conversion efficiency, lightweight structure, and potential for low-cost manufacturing compared with conventional Silicon Photovoltaic Cells. However, perovskite materials are highly sensitive to environmental factors such as moisture, oxygen, ultraviolet radiation, and temperature fluctuations, which can degrade cell performance over time. To address these stability challenges, advanced protective and functional coatings are increasingly integrated into solar module designs. These coatings include hydrophobic barrier layers, UV-resistant films, anti-reflective coatings, and self-cleaning surfaces that enhance durability, improve light transmission, and extend module lifespan. As the solar industry scales toward high-efficiency tandem architectures, such as perovskite-silicon tandem modules, the need for specialized coatings becomes even more critical to maintain optical performance and environmental protection.

Global energy developers, investors, and governments are placing stronger emphasis on Environmental, Social, and Governance (ESG) standards in renewable energy projects. This trend is encouraging the adoption of premium, environmentally responsible coating formulations with low volatile organic compounds (VOC), longer service life, and improved recyclability. Advanced coating technologies can enhance panel efficiency by reducing reflection losses and preventing dust accumulation, thereby improving energy yield while lowering maintenance requirements, key metrics for ESG-focused solar assets.

Restraints - High Performance Coating Application Cost and Field Retrofit Economic Justification Challenging Mass Residential Market Adoption

Despite the documented efficiency and LCOE economics of premium solar panel coatings, the upfront cost of high-performance multi-functional coating systems, with premium anti-reflective and self-cleaning nano-coating treatments adding US$ 0.02–0.08 per Wp to solar module manufacturing costs, creates an economic barrier to adoption in cost-sensitive residential and developing market installations where buyers prioritize the lowest upfront system cost over the lifetime value optimization achieved through coating-enhanced panel performance.

The solar panel manufacturing industry's relentless cost reduction trajectory, with BNEF documenting a 90%+ reduction in crystalline silicon solar module prices since 2010, creates paradoxical pressure on coating adoption economics as falling panel prices reduce the proportional economic justification for adding premium coating costs to the overall system bill of materials for standard residential installations.

Durability and Weathering Performance Consistency Concerns Under Diverse Climate Exposure Conditions Limiting Premium Coating Confidence

Solar panel coatings must sustain performance across 25–30 year solar module operational lifetimes while exposed to UV radiation, thermal cycling between -40°C and +85°C, humidity, dust, rain impact, and chemical atmospheric pollutants, a multi-decade durability requirement that is exceptionally challenging to validate through accelerated laboratory testing and that has generated documented field performance inconsistency concerns for some early-generation nano-coating products.

The IEC 61215 and IEC 61730 international solar module qualification standards, administered by the International Electrotechnical Commission (IEC), do not yet include standardized coating-specific durability test protocols that provide independent third-party performance verification for solar panel coating products, creating a customer confidence gap that slows premium coating adoption particularly among risk-averse utility-scale solar project developers requiring bankable performance warranties.

Opportunities - Agrivoltaics and Utility-Scale Solar Expansion in Dust-Prone Geographies Creating Premium Anti-Soiling Coating Demand

The global agrivoltaics sector, where solar panels are co-deployed with agricultural crops or livestock grazing operations, is one of the fastest-growing solar deployment models worldwide, with the International Renewable Energy Agency (IRENA) documenting that agrivoltaic systems have been commissioned or announced across 35+ countries with combined global installed capacity exceeding 14 GW by 2024, and is generating specialized anti-soiling, self-cleaning, and anti-abrasion coating demand for solar panels deployed in environments with elevated particulate contamination from agricultural dust, pollen, bird activity, and irrigation spray.

Self-cleaning and anti-soiling coatings provide particularly compelling economic value in dust-prone utility-scale installations across the Middle East, North Africa, India's Rajasthan, and Australia's outback solar zones, where soiling losses without coating treatment can reduce solar output by 5–30% annually, generating return-on-investment periods of 2–4 years for premium anti-soiling coating investment that is well within the procurement approval economics of utility-scale solar project developers. AkzoNobel (headquartered in Amsterdam, Netherlands) and Nanotech Coatings are both commercially active in the anti-soiling and self-cleaning solar coating segment targeting utility-scale and agricultural solar deployment geographies. Saint-Gobain (headquartered in Courbevoie, France) supplies ALBARINO® anti-reflective solar glass coatings to the global utility-scale solar glass manufacturing market.

Bifacial Monocrystalline Panel Manufacturing Boom and Building-Integrated Photovoltaics Creating Multi-Layer Coating System Demand

The global solar panel manufacturing industry's near-complete transition to bifacial monocrystalline PERC (Passivated Emitter and Rear Cell) and TOPCon (Tunnel Oxide Passivated Contact) panel architectures, with BloombergNEF documenting bifacial panels representing over 70% of new solar module shipments in 2023, is creating a structural shift in solar panel coating requirements toward dual-surface coating systems protecting both front anti-reflective glass and rear transparent backsheet surfaces, effectively doubling the coating material content per module compared to conventional single-side coated panels. Building-Integrated Photovoltaics (BIPV), where solar cells are incorporated into building facade cladding, roof tiles, skylights, and curtain wall glazing, represent a rapidly expanding premium solar coating application category requiring specialized architectural coating aesthetics, color customization capabilities, and building certification-grade durability that command substantially higher coating prices per square meter than standard utility-scale solar module coating applications.

AGC Inc. (headquartered in Tokyo, Japan), the world's largest flat glass manufacturer, and Guardian Glass (a Koch Industries company) are both major suppliers of anti-reflective coated solar glass for BIPV applications, with AGC's SUNMAX® anti-reflective solar glass coating product family serving global BIPV and premium utility-scale solar glass procurement programs. The European Commission's mandatory EU Solar Rooftop Initiative, targeting 320 GW of additional rooftop solar by 2025 and 600 GW by 2030 under REPowerEU, is directly stimulating the BIPV and rooftop solar coating demand category across European markets.

Category-wise Analysis

By Coating Type Insights

Anti-reflective coatings lead the global Solar Panel Coatings market by coating type, commanding approximately 38% of total coating type segment revenue in 2026, a dominant market position. Anti-reflective coating applied to solar panels achieves 5.5% higher annual electricity generation and 2.7% LCOE reduction in utility-scale installations, providing the most financially quantifiable performance enhancement among all solar panel coating categories and making it the standard specification for premium solar glass across virtually all major global panel manufacturers.

Anti-reflective coatings, primarily based on Silicon Dioxide (SiO2), Magnesium Fluoride (MgF2), and nanomaterial sol-gel formulations, reduce front glass surface reflection losses from approximately 4% to below 1% at optimized wavelength ranges, directly translating into electricity yield improvements that sustain above-industry-average coating procurement growth.

AGC Inc., Saint-Gobain, Guardian Glass, and Fenzi Group are the dominant global anti-reflective solar glass coating suppliers serving flat glass manufacturers whose solar glass products incorporate anti-reflective treatment as a standard premium specification for monocrystalline and bifacial panel applications. Self-cleaning and anti-soiling coatings hold the second-largest combined coating type share at approximately 27% and are the fastest-growing coating type driven by utility-scale and agrivoltaic deployment growth in high-soiling geographies.

By Material Type Analysis

Nanomaterial-Based Coatings lead the global solar panel coatings market by material type, accounting for approximately 33% of total material type segment revenue in 2026, reflecting the superior optical, hydrophobic, and self-cleaning functional performance achieved through engineered nanoparticle coating formulations compared to conventional non-nanostructured polymer or metal oxide coatings, and their growing commercial adoption as the premium coating technology platform across anti-reflective, self-cleaning, and anti-soiling solar panel coating applications by leading panel manufacturers globally.

Nanomaterial coatings, incorporating TiO2, SiO2, ZnO, and hybrid silica-fluoropolymer nanoparticle systems, achieve simultaneously enhanced light transmittance through anti-reflective nanostructuring, photocatalytic self-cleaning through TiO2 UV-activated surface chemistry, and superhydrophobic water-sheeting through nanostructured lotus-effect surface topology, combining multiple protective functions in a single ultra-thin 50–200 nm coating layer that minimizes added weight and optical path interference.

3M Company's nanostructured anti-reflective coating product families and BASF SE's specialty coating dispersion platforms are among the most commercially referenced nanomaterial-based solar coating solutions globally. Metal Oxide Coatings (TiO2, SiO2, MgF2) hold the second-largest material type share at approximately 28%, anchored in their established sol-gel glass coating deposition process compatibility with large-area flat glass solar coating production lines.

By Application Insights

Monocrystalline Solar Panels lead the global Solar Panel Coatings market by application, commanding approximately 52% of total application segment revenue in 2026, a dominant position reflecting the near-complete market transition to monocrystalline silicon technology as the global solar industry's dominant panel architecture, with BloombergNEF documenting monocrystalline panels representing over 85% of global solar module shipments by 2023 driven by their superior power conversion efficiency (20–24% PCE) versus polycrystalline (16–18% PCE) and thin-film panels, making monocrystalline the priority technology platform for coating investment across anti-reflective, self-cleaning, and encapsulant coating applications.

Premium monocrystalline PERC, TOPCon, and HJT (Heterojunction Technology) panels command the highest coating specification requirements, with HJT panels requiring specialized low-temperature curing coating formulations compatible with the silicon-heterojunction cell structure's maximum processing temperature limits. Perovskite Solar Cells hold a small but fast-growing application share, projected to be the highest-CAGR application segment driven by Northwestern University's documented 26.3% efficiency achievements and the January 2026 fluorinated coating breakthrough reaching 27% efficiency with 1,200-hour stability, signaling imminent commercial scale-up.

By End-User Insights

Utility-Scale Solar Power Plants lead the global Solar Panel Coatings market by end-user, accounting for approximately 45% of total end-user segment revenue in 2026, anchored by utility-scale solar's structural dominance of global new solar capacity additions, with the IEA documenting utility-scale ground-mounted solar representing over 60% of 2023's record 420 GW global solar additions, and the compelling economics of anti-reflective and anti-soiling coating investment at utility-scale project economics where even 1–2% annual yield improvements generate millions of dollars in additional revenue over a 25-year project lifetime.

Agriculture (Agrivoltaics) represents the fastest-growing end-user segment, with IRENA's documented 14+ GW global agrivoltaic installed capacity by 2024 and governmental policy support in Japan, South Korea, Germany, France, and India for agrivoltaic land-use dual-purpose optimization programs generating specialized coating demand for self-cleaning and anti-soiling treated panels optimized for agricultural environment co-deployment.

Regional Insights

North America Solar Panel Coatings Market Trends

North America leads the global market in premium product adoption and innovation investment, anchored by the U.S.'s position as the world's second-largest solar energy deployment market, with the Solar Energy Industries Association (SEIA) documenting a record 32.4 GW of U.S. solar capacity installed in 2023, and the Inflation Reduction Act (IRA)'s 30% Investment Tax Credit sustained through 2032 providing the most commercially significant renewable energy investment incentive in U.S. history.

The U.S. Department of Energy (DOE)'s Solar Energy Technologies Office (SETO) actively funds advanced coating research, including anti-reflective coating durability programs and perovskite stabilization coating development under its National PV Manufacturing Roadmap, positioning U.S. institutions as global leaders in next-generation solar coating science.

3M Company's advanced nanostructured anti-reflective coating technologies, PPG Industries' solar glass coating product portfolio, and DuPont's Tedlar® PVF backsheet coating platform are developed and manufactured in the U.S., sustaining North America's position as the world's most commercially innovative solar coating supplier geography. The U.S. EPA's chemical management frameworks under TSCA regulate solar panel coating VOC formulations, driving adoption of low-VOC water-borne coating chemistries by Sherwin-Williams and AkzoNobel for U.S. solar manufacturing facility coating application compliance.

Europe Solar Panel Coatings Market Trends

Europe is a commercially significant and innovation-active Solar Panel Coatings market, driven by the European Commission's REPowerEU Plan targeting 600 GW of solar capacity by 2030, the EU Solar Rooftop Initiative mandating solar installation on new commercial buildings from 2026 and all existing commercial buildings from 2027, and Germany, Spain, Italy, France, and the Netherlands collectively sustaining some of the world's highest per-capita solar deployment rates that generate substantial European solar panel coating procurement.

SolarPower Europe's Solar Outlook 2024 documented that the EU installed 56 GW of new solar capacity in 2023, confirming Europe's structural solar deployment momentum sustaining panel coating demand growth.

Europe's REACH Regulation environmental chemical compliance framework, administered by the European Chemicals Agency (ECHA), is driving European solar panel coating manufacturers toward fluorine-free and low-hazardous-substance coating formulations that sustain long-term regulatory compliance and European OEM procurement qualification. Fenzi Group (headquartered in Tribiano, Italy), a leading specialty glass coatings company, supplies anti-reflective solar glass coatings to European solar glass manufacturers including Guardian Glass and AGC.

Germany's Fraunhofer Institute for Solar Energy Systems (ISE), the world's largest solar energy research institute, is actively collaborating with European coating companies on advanced anti-soiling, self-cleaning, and perovskite stabilization coating development programs that reinforce Europe's position in solar coating technology innovation.

Asia Pacific Solar Panel Coatings Market Treds

Asia Pacific dominates the global solar panel coatings market by volume, anchored by China's position as the world's largest solar panel manufacturing geography, contributing over 80% of global solar module production according to the IEA's solar manufacturing supply chain analysis, generating by far the largest single-geography solar panel coating procurement volume globally as virtually every module manufactured in China incorporates at least one anti-reflective glass or protective coating layer.

China's National Energy Administration (NEA) documented record 217 GW of new solar capacity installed in China alone in 2023, more than the rest of the world combined, with the Chinese government's "14th Five-Year Plan for Renewable Energy" targeting 1,200 GW cumulative solar and wind capacity by 2030 sustaining structural long-term coating demand growth.

India is the fastest-growing Asia Pacific solar coating market, with the Ministry of New and Renewable Energy (MNRE) documenting India's target of 500 GW of renewable energy capacity by 2030, including 280 GW of solar, supported by Production Linked Incentive (PLI) schemes stimulating domestic solar module manufacturing investment in Rajasthan, Gujarat, Tamil Nadu, and Andhra Pradesh that generate growing domestic procurement demand for anti-reflective, anti-soiling, and self-cleaning coatings for panels deployed in India's high-dust-load solar environments where soiling losses of 5–15% annually make self-cleaning coating ROI economics particularly compelling.

ASEAN solar markets, particularly Vietnam, Thailand, Malaysia, and Indonesia, are emerging as both solar coating manufacturing and consumption hubs, with regional governments implementing Feed-in Tariff and Renewable Portfolio Standard policies that are accelerating solar installation growth and correspondingly expanding solar panel coating procurement.

Competitive Landscape

The global Solar Panel Coatings market is moderately fragmented, with multinational specialty chemicals and glass companies PPG Industries, BASF SE, 3M, AkzoNobel, Saint-Gobain, and AGC Inc. commanding leadership positions through broad coating technology portfolios, global manufacturing scale, and direct solar glass OEM supply relationships. Arkema, Covestro, DuPont, and Solvay lead in fluoropolymer and high-performance polymer coating segments. Specialty players Nanotech Coatings and Fenzi Group compete through focused solar coating technology differentiation.

Key market differentiators include coating durability certification to IEC 61215, photocatalytic self-cleaning performance credentials, perovskite-compatible coating chemistry, and low-VOC regulatory compliance. Emerging trends include multifunctional single-layer coatings combining anti-reflective and self-cleaning properties, BIPV-optimized architectural coating aesthetics, and agrivoltaic-specific anti-soiling formulation development.

Key Developments:

- In January 2026, An international research team, including researchers from Southeast University, Nanjing, developed a fluorinated Teflon-like molecular coating for perovskite solar cells achieving 27% power conversion efficiency with maintained performance after 1,200 hours of continuous operation, representing a breakthrough in perovskite coating stability directly enabling commercial-scale perovskite module development.

- In November 2024, Northwestern University scientists announced a new protective coating for perovskite solar cells achieving 26.3% power conversion efficiency and tripling stability to retain 90% initial efficiency after 1,100 hours under heat and light testing, providing the most commercially significant perovskite stability breakthrough enabling imminent module commercialization requiring specialized coating supply.

Companies Covered in Solar Panel Coatings Market

- 3M Company

- PPG Industries

- BASF SE

- Solvay

- DuPont

- AkzoNobel

- Sherwin‑Williams

- Arkema

- Covestro

- Eastman Chemical Company

- Guardian Glass

- AGC Inc.

- Saint‑Gobain

- Nanotech Coatings

- Fenzi Group

Frequently Asked Questions

The global Solar Panel Coatings market is estimated to be valued at US$ 5.9 Billion in 2026 and is projected to reach US$ 30.8 Billion by 2033, registering a forecast CAGR of 26.6% from 2026 to 2033. The market recorded a historical CAGR of 21.4% between 2020 and 2025.

The primary drivers are the IEA's projection of cumulative global solar capacity reaching 5,500 GW by 2030 and the SEIA-documented 32.4 GW U.S. solar installation record in 2023 sustained by IRA's 30% Investment Tax Credit through 2032, combined with perovskite solar cell coating science breakthroughs including Northwestern University's 26.3% PCE achievement (November 2024) and the January 2026 fluorinated coating reaching 27% efficiency with 1,200-hour operational stability confirming coating-enabled commercialization pathway.

Anti-reflective coatings lead the Coating Type segment with approximately 38% revenue share in 2026, validated by pv magazine's August 2024 peer-reviewed field study documenting 5.5% higher electricity output and 2.7% LCOE reduction at a 40 MW utility-scale plant using anti-reflective coated panels versus uncoated equivalents. The segment is dominated by AGC's SUNMAX®, Saint-Gobain's ALBARINO®, PPG Industries' solar glass coating platform, and 3M's nanostructured anti-reflective coating product families serving global solar glass manufacturers.

Asia Pacific leads the global Solar Panel Coatings market, anchored by China's world-dominant 80%+ share of global solar panel manufacturing volume documented by the IEA, China's NEA-recorded 217 GW domestic solar installation in 2023 alone, India's MNRE target of 280 GW solar by 2030, and the region's concentration of the world's largest solar glass manufacturers consuming AGC's, Fenzi Group's, and PPG's anti-reflective coating products as standard premium glass specification.

The most significant opportunities are perovskite solar cell specialized coating commercialization and agrivoltaics anti-soiling coating procurement, with January 2026 fluorinated coating achieving 27% PCE enabling imminent module commercialization creating premium ESG coating demand, while IRENA's 14+ GW global agrivoltaic deployment and the EU Solar Rooftop Initiative mandating building-integrated solar from 2026–2027 generate structurally growing anti-soiling and BIPV architectural coating procurement streams through 2033.