- Specialty & Fine Chemicals

- Propylene Carbonate Market

Propylene Carbonate Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Propylene Carbonate Market by Grade (Electronic, Technical), Application (Electrolyte Solvent, Electronic Cleaning Fluids, Cosmetics & Personal Care, Textiles & Dyeing), Industry (Automotive, Pharmaceuticals, Textile), and Regional Analysis 2025 - 2032

Propylene Carbonate Market Share and Trends Analysis

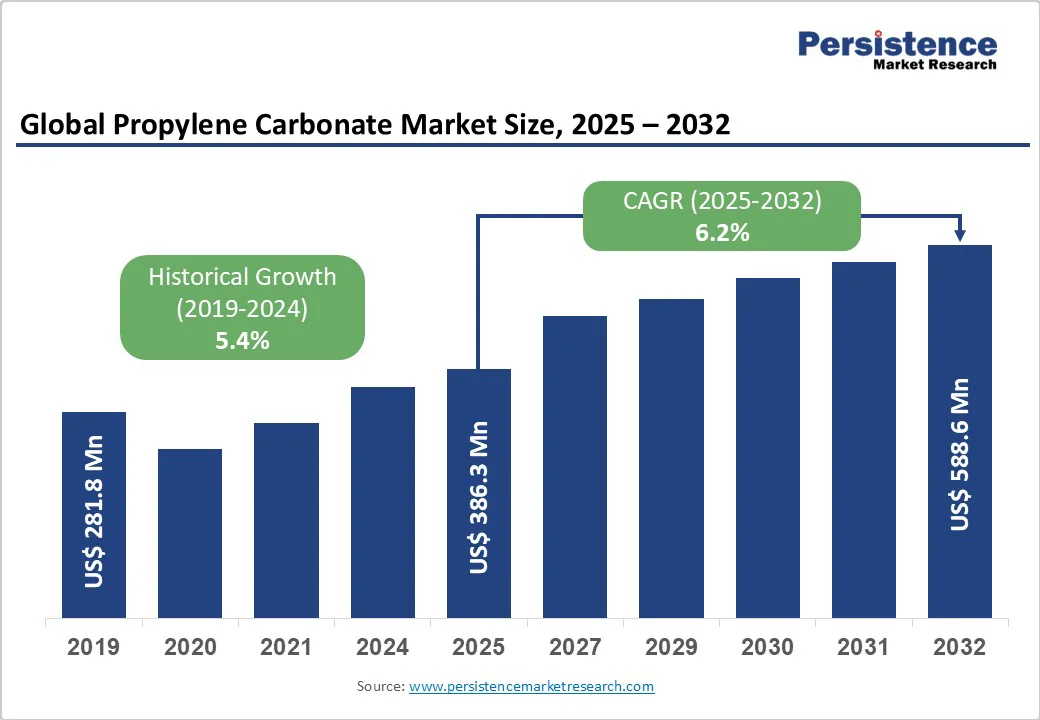

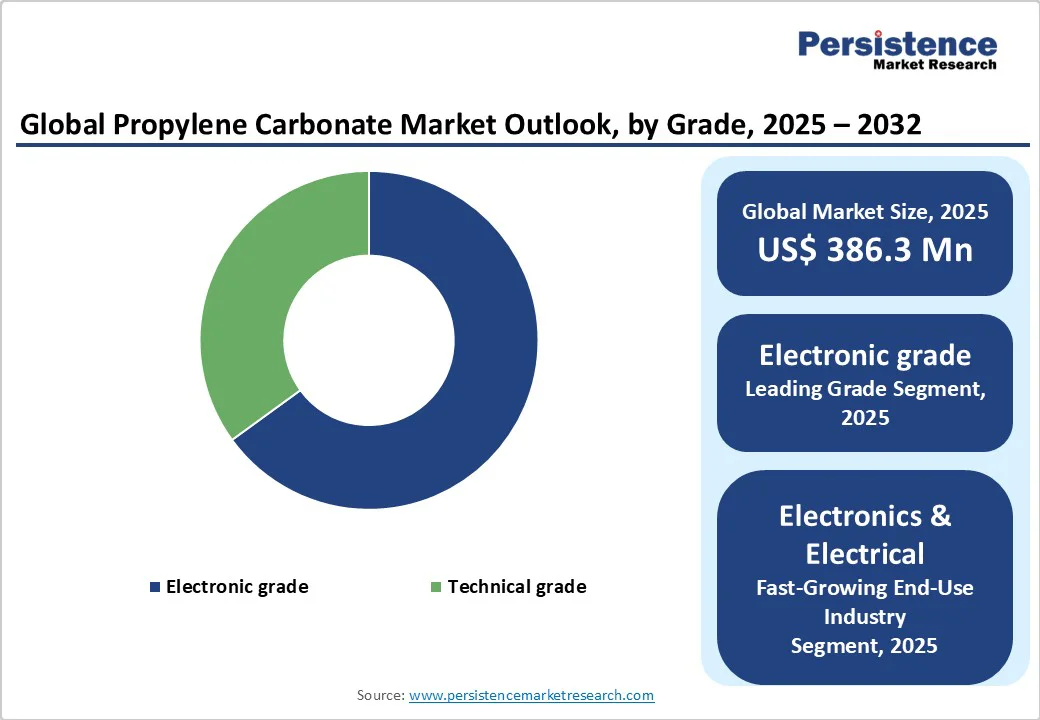

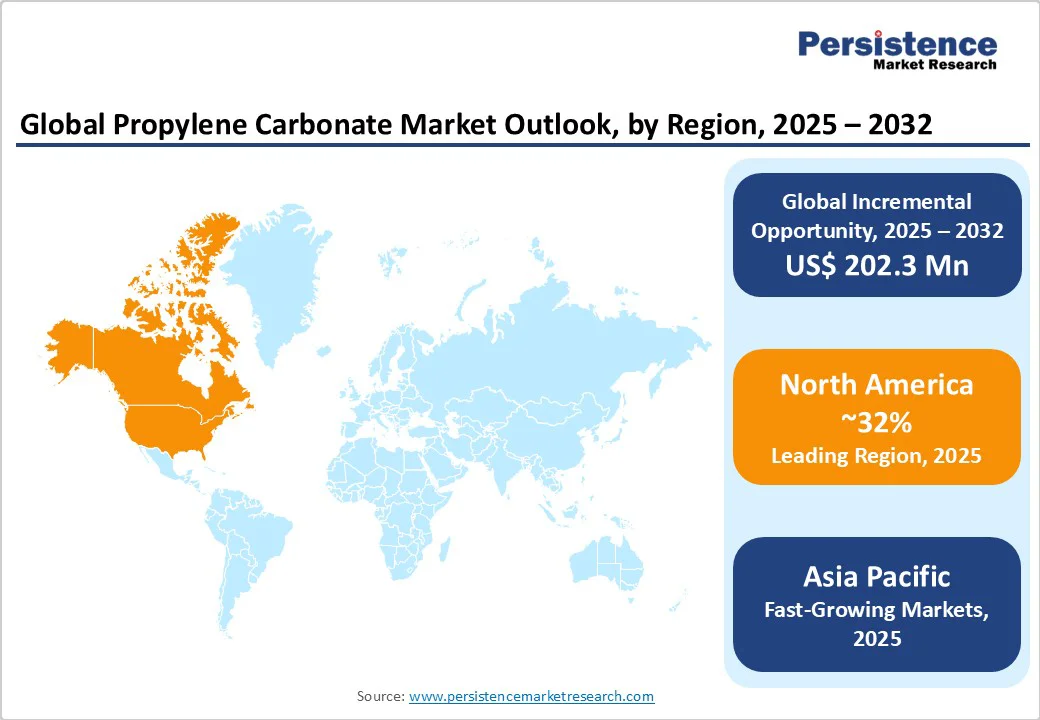

The global propylene carbonate market size is likely to value at US$ 386.3 Million in 2025 and is projected to reach US$ 588.6 Million by 2032, growing at a CAGR of 6.2% between 2025 and 2032.

Propylene carbonate’s exceptional solvency, high dielectric constant, and low toxicity have positioned it as a preferred solvent across multiple high-growth industries.

Its demand is driven by rapid expansion in the electric vehicle sector, where it serves as a critical electrolyte solvent, and by stringent environmental regulations that favor greener alternatives in coatings, cleaning fluids, and personal care formulations.

Key Highlights:

- North America commands the largest demand share due to extensive EV battery research funding and strict VOC regulations.

- Asia Pacific is the fastest-growing region, driven by China’s dominant battery manufacturing and supportive government incentives.

- Electrolyte solvent is the dominant application segment, accounting for over half of market consumption.

- Electronic grade leads the grade segment, reflecting high purification standards for battery and electronics uses.

- Grid-scale energy storage expansion represents the key growth opportunity, with stationary battery systems projected to grow at over 20% CAGR.

| Key Insights | Details |

|---|---|

| Propylene Carbonate Market Size (2025E) | US$ 386.3 Million |

| Market Value Forecast (2032F) | US$ 588.6 Million |

| Projected Growth CAGR (2025-2032) | 6.2% |

| Historical Market Growth (2019-2024) | 5.4% |

Market Dynamics

Driver - High Demand from the Electric Vehicle Battery Sector

The proliferation of lithium-ion batteries for electric vehicles has been the foremost driver for the Propylene Carbonate Market. As global EV sales exceeded 10 million units in 2024, a 40% year-on-year increase, battery manufacturers have prioritized high-performance electrolyte solvents with superior dielectric properties and oxidative stability.

Propylene carbonate, with its wide electrochemical window and low viscosity, enhances ion transport and thermal stability. Consequently, demand for propylene carbonate in battery applications grew by over 8% annually between 2021 and 2024, and is expected to maintain similar momentum as EV production capacity expands to meet targets set by major automakers by 2030.

Regulatory Push for Sustainable Solvents

Environmental regulations in key markets, notably the U.S. Environmental Protection Agency’s VOC limits and the European Chemicals Agency’s REACH restrictions, have accelerated the shift from chlorinated and high-toxicity solvents toward greener options.

Classified under REACH as a low-toxicity, biodegradable solvent, propylene carbonate has been widely adopted in industrial cleaning, paints, and coatings. This regulatory tailwind prompted a 6% annual increase in propylene carbonate usage in regulated segments during 2022 - 2024, as formulators reformulated products to comply with stricter environmental standards.

Market Restraints

Feedstock Price Volatility

Propylene carbonate production relies on propylene oxide, itself a derivative of petroleum feedstocks. Volatile crude oil prices, which fluctuated between US$ 50 and US$ 90 per barrel during 2022-2024, have translated into raw material cost swings, pressuring margins for propylene carbonate producers. Sudden price hikes can delay contract renewals or prompt end users-particularly in cost-sensitive sectors like textiles and dyes-to seek cheaper alternatives, thereby restraining market growth.

Competition from Lower-Cost Alternatives

Alternative carbonate solvents such as ethylene carbonate and dimethyl carbonate often cost 10-15% less than propylene carbonate. In 2023, dimethyl carbonate averaged US$ 1,200/ton, compared to propylene carbonate’s US$ 1,400/ton, leading some manufacturers in non-critical applications to opt for substitutes. While performance trade-offs exist, the cost differential remains a key barrier to broader adoption in price-sensitive end uses.

Market Opportunities

Growth in Grid-Scale Energy Storage

The global stationary energy storage market, valued at US$ 15 billion in 2024, is forecast to expand at a 20% CAGR through 2030. Propylene carbonate’s superior electrochemical stability and wide voltage window make it well-suited for large-format battery systems used in renewable energy integration. Partnerships between propylene carbonate suppliers and battery developers, along with government incentives for utility-scale storage projects, present significant growth avenues through co-development of optimized electrolytes.

Rising Demand in Cosmetics & Personal Care

Consumer preferences for non-irritating, eco-friendly ingredients have elevated propylene carbonate’s role as a solvent and penetration enhancer in cosmetics. Studies show formulations with propylene carbonate improve active ingredient delivery by up to 25%, driving adoption in premium skincare lines. With global beauty industry revenues surpassing US$ 500 billion in 2024, clean-beauty trends offer a lucrative opportunity for propylene carbonate producers to collaborate on high-margin, specialized formulations.

Category-wise Insights

By Grade Analysis

Electronic grade propylene carbonate, characterized by moisture content below 20 ppm and impurity levels under 5 ppm, commands approximately 65% market share. Its use in high-purity applications, notably battery electrolytes and precision electronics cleaning fluids, underpins this dominance. Technical grade, while more affordable, suits industrial manufacturing and solvent applications where ultra-low impurity levels are less critical, capturing the remaining share.

By Application Analysis

Electrolyte solvent leads with around 55% share of the application segment, supported by the surging lithium-ion battery market. Battery electrolyte formulations accounted for over 60% of global carbonate solvent consumption in 2024. Other applications-such as electronics cleaning fluids, pharmaceutical intermediates, and cosmetics-collectively constitute the balance, each projected to grow at mid-single-digit rates as industries refine product performance and safety profiles.

By Industry Analysis

The electronics & electrical sector represents the largest end-use, with 45% share, reflecting stringent cleanliness and performance requirements for printed circuit boards, semiconductors, and component assembly. Pharmaceutical intermediates follow at 20%, where propylene carbonate acts as a key reaction medium for synthesizing APIs under controlled conditions. Growth in medical device and drug manufacturing, supported by rising global healthcare expenditure, further boosts this segment.

Regional Insights

North America Propylene Carbonate Trends

North America’s leadership stems from robust investment in battery R&D and stringent environmental regulations. The U.S. Department of Energy allocated US$ 200 million in grants for advanced electrolyte research in 2024, incentivizing new propylene carbonate formulations.

Major producers such as LyondellBasell Industries expanded U.S. capacity by 15% to serve domestic EV and grid storage markets. Meanwhile, EPA VOC regulations have driven coatings and cleaning fluid manufacturers to adopt propylene carbonate, bolstering regional demand.

Europe Propylene Carbonate Trends

Europe’s market growth is underpinned by regulatory harmonization via REACH and significant automotive battery manufacturing. Germany, accounting for 30% of regional consumption, hosts several gigafactories backed by government incentives. The EU Green Deal’s net-zero targets by 2050 have spurred €50 million research grants in France for sustainable electrolyte materials. This regulatory and funding environment accelerates propylene carbonate adoption in battery and industrial applications.

Asia Pacific Propylene Carbonate Trends

Asia Pacific leads global production, representing over 60% of output in 2024. China’s battery manufacturing capacity exceeded 500 GWh in 2024, driving domestic electrolyte demand. Government subsidies and favorable labor costs support rapid capacity expansions by producers such as Shandong Depu Chemical. Japan and India are also scaling production to cater to regional electronics and automotive sectors, while ASEAN nations emerge as export hubs for industrial solvent applications.

Competitive Landscape

The global propylene carbonate Market is moderately consolidated, with top players such as LyondellBasell Industries, BASF SE, and Shandong Depu Chemical together holding over 50% share. Companies differentiate through proprietary purification technologies, integrated propylene oxide production, and sustainability initiatives like bio-based feedstock sourcing. Toll-manufacturing partnerships and backward integration strategies are gaining traction as firms seek supply security and cost efficiencies.

Key Market Developments

- March, 2025: BASF SE inaugurated a high-purity solvent unit in Ludwigshafen, boosting electronic-grade output by 20%.

- November, 2024: LyondellBasell Industries entered a co-development agreement with a leading EV battery manufacturer for high-voltage electrolyte formulations.

- July, 2024: Shandong Depu Chemical commissioned a 30 kt/year production facility in Zibo to meet surging domestic demand.

Companies Covered in Propylene Carbonate Market

- LyondellBasell Industries

- Shandong Depu Chemical

- BASF SE

- Empower Materials

- Huntsman International LLC.

- Dhalop Chemicals

- Tokyo Chemical Industry Co., Ltd. (TCI)

- Linyi Evergreen Chemical Co., Ltd.

- Central Drug House

- Carl Roth

- SMC-Global

Frequently Asked Questions

The propylene carbonate market was valued at US$ 386.3 Million in 2025 and is forecast to reach US$ 588.6 Million by 2032 at a 6.2% CAGR.

The expansion of the lithium-ion battery sector in electric vehicles and grid storage, where propylene carbonate is used as a high-performance electrolyte solvent, drives primary demand.

The electrolyte solvent segment dominates with approximately 55% share, propelled by soaring global battery production capacities.

North America leads, due to significant EV battery R&D investments and stringent environmental regulations favoring green solvents.

Growth in grid-scale energy storage systems presents the foremost opportunity, with stationary battery deployments projected to grow positively in the coming years.

Top players include LyondellBasell Industries, BASF SE, and Shandong Depu Chemical, renowned for integrated production capabilities, high-purity offerings, and capacity expansions.