- Metals & Minerals

- Lithium Carbonate Market

Lithium Carbonate Market Size, Share, and Growth Forecast for 2025 - 2032

Lithium Carbonate Market By Battery (Lithium-ion Batteries, Lithium-metal Batteries, Others), Grade (Battery Grade, Technical Grade, Industrial Grade), Application (Electric Vehicles, Pharmaceutical, Cement, Glass & Ceramics, Others), and Regional Analysis for 2025 - 2032

Lithium Carbonate Market Size and Trends Analysis

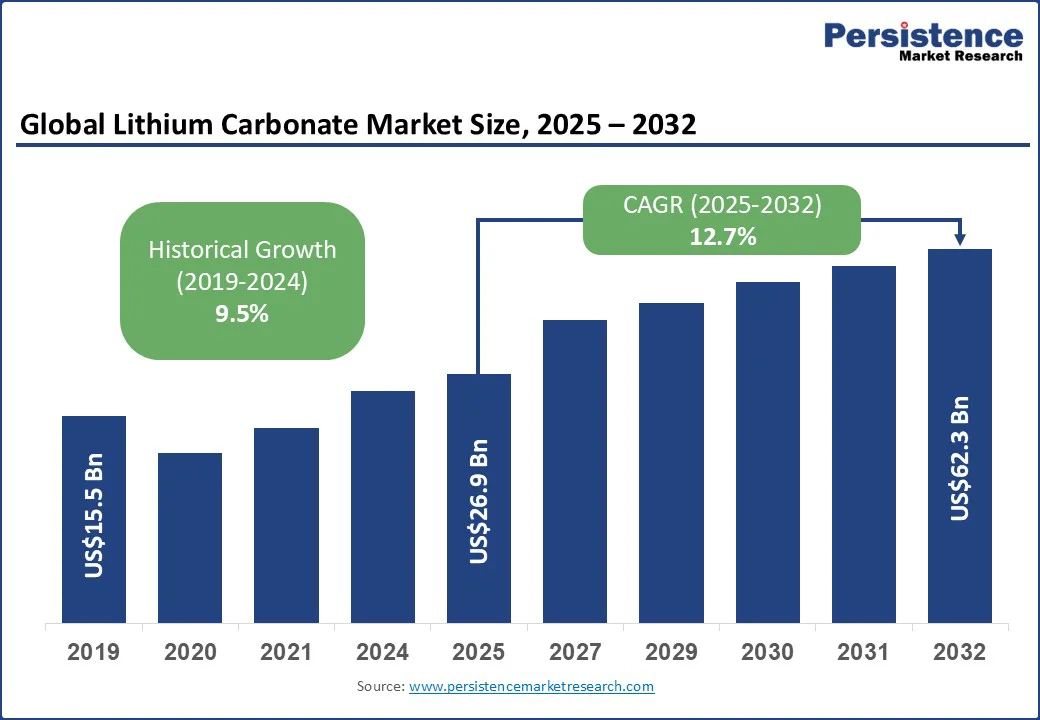

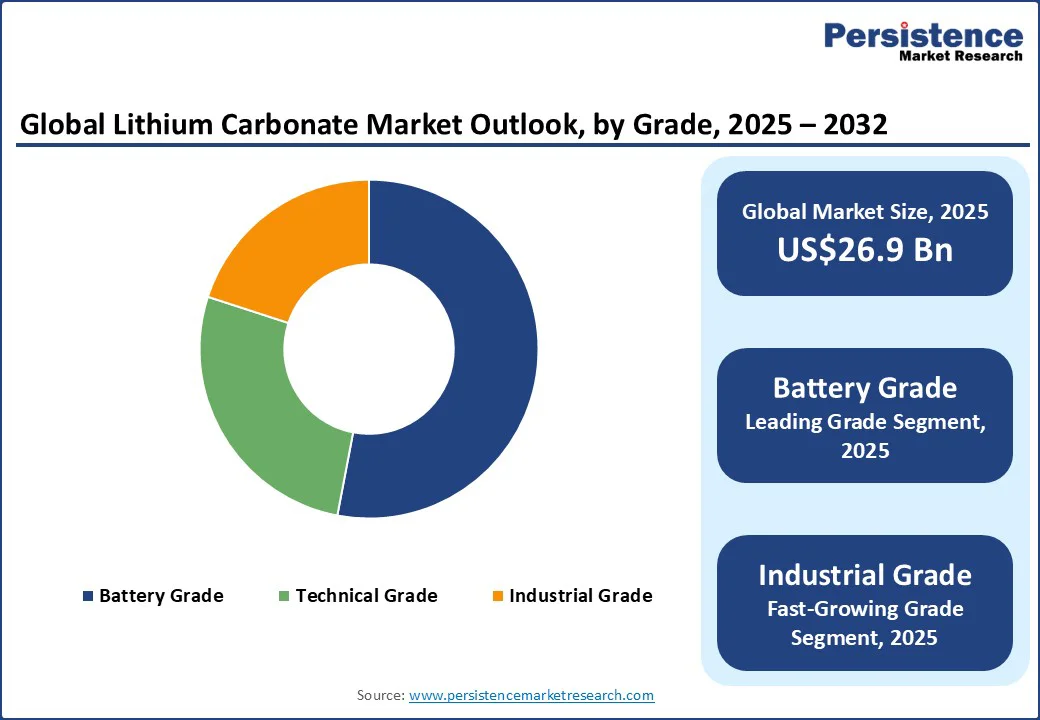

The global lithium carbonate market size is likely to be valued at US$26.9 Bn in 2025 and is expected to reach US$62.3 Bn by 2032, growing at a CAGR of 12.7% during the forecast period from 2025 to 2032.

The market growth is driven by stringent environmental regulations, the accelerating adoption of electric vehicles (EVs), the expansion of renewable energy storage solutions, and ongoing technological innovation in lithium extraction and processing techniques.

Key Industry Highlights

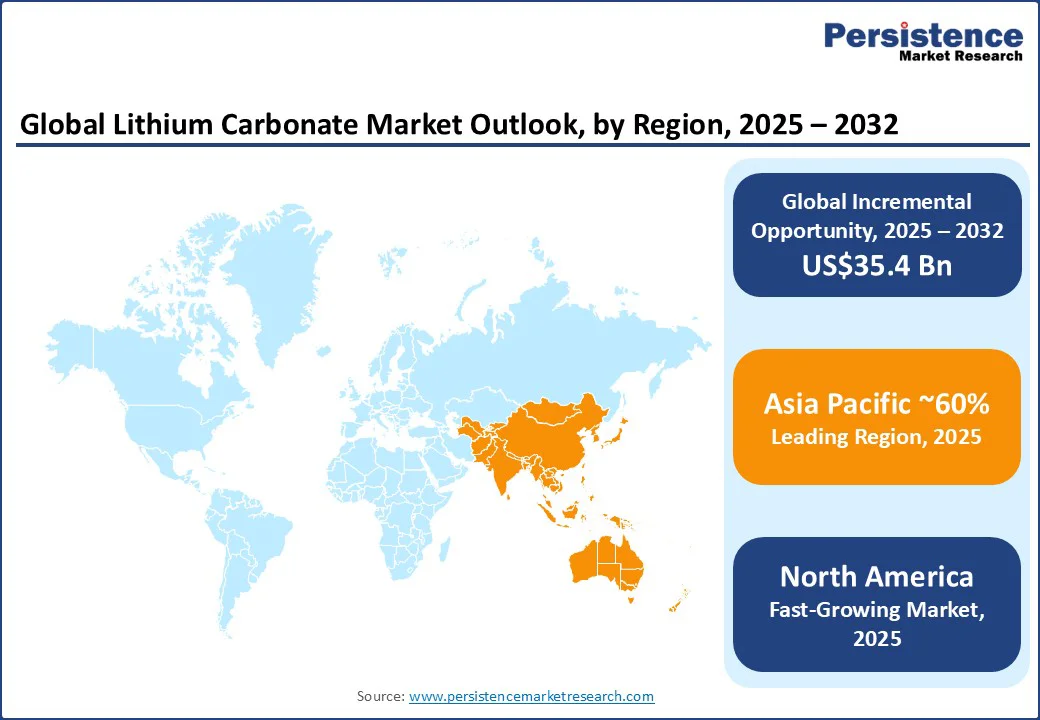

- Leading Region: Asia Pacific is projected to account for approximately 60% of the market in 2025, driven by massive electric vehicle adoption, a strong lithium-ion battery manufacturing ecosystem, and supportive government policies.

- Fastest-growing Region: North America is projected to be the fastest-growing region, with a CAGR of around 15.1% to 2032, fueled by investments in battery supply chains, expanding energy storage infrastructure, and initiatives to reduce import dependency.

- Leading Application Type: Electric vehicles (EVs) drive the global market with a 40% share in 2025, making it the fastest-growing application, fueled by increasing adoption, renewable energy storage, and innovations for higher energy density and cost efficiency.

- Dominant Battery Type: Lithium-ion batteries are expected to dominate global lithium carbonate consumption with around 64% of the market share in 2025, driven by the rapid adoption of electric vehicles, renewable energy storage, and consumer electronics.

|

Global Market Attribute |

Key Insights |

|

Lithium Carbonate Market Size (2025E) |

US$26.9 Bn |

|

Market Value Forecast (2032F) |

US$62.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.5% |

Market Dynamics

Driver - EV Revolution and Energy Storage Surge to Power Lithium Carbonate Demand

The primary driver for the lithium carbonate market is the significant demand from EVs and energy storage sectors, supported by rapid technological advancements and proactive regulatory measures. Lithium-ion batteries have become the fastest-growing energy technology, with deployment doubling annually across utility-scale storage, behind-the-meter systems, and EVs.

Between 2023 and 2024, EV battery deployment surged by nearly 40%, while global battery demand reached a record 1 terawatt-hour (TWh), highlighting lithium-ion’s pivotal role in the energy transition. This surge is driving strong, cross-sector demand, tying lithium carbonate consumption directly to the growth of clean energy and modern mobility solutions.

Robust quantitative indicators and strategic government support further strengthen this momentum. The U.S. federal government has allocated over US$3 Bn through the Bipartisan Infrastructure Law for critical mineral processing, recycling, and battery component manufacturing, backing key projects such as Ultium Cells, BlueOval SK, and Redwood Materials.

Globally, lithium demand has tripled since 2017 and is expected to rise tenfold by 2050 under the IEA’s “Net Zero Emissions” scenario. These market dynamics and policy initiatives make this driver both decisive and enduring for the market expansion.

Restraint - Supply Chain Volatility and Environmental Compliance Pressures Slow Market Expansion

The lithium carbonate market is affected by a volatile supply chain, largely due to the geographical concentration of lithium reserves. Over 70% of global production comes from Australia, Chile, and China, leaving the market exposed to export restrictions, trade tensions, and logistical bottlenecks. Such concentration can lead to supply disruptions and price volatility, impacting downstream industries such as EVs and energy storage.

Environmental and social compliance requirements further challenge market growth. Water-intensive brine operations in South America and the ecological impacts of hard-rock mining have prompted increased scrutiny from governments and local communities, often delaying project approvals and raising operational costs. Together, these factors supply fragility and sustainability obligations, pose significant hurdles for manufacturers and suppliers, and limit their ability to scale production and meet rising global demand for lithium carbonate.

Opportunity - Sustainable Innovation and Policy Support Unlock New Avenues

Sustainability-driven innovation combined with strong government support is creating significant growth momentum for the lithium carbonate market. Lithium carbonate is playing an increasingly critical role in next-generation batteries, powering EVs and grid-scale energy storage systems that support renewable energy integration. Advances in extraction technologies such as direct lithium extraction (DLE) enable more efficient and environmentally responsible production, allowing manufacturers to scale operations while meeting global sustainability standards.

Government initiatives and industry investments are reinforcing this trend. The European Union’s Critical Raw Materials Act aims to secure a sustainable lithium supply within Europe, while the U.S. Inflation Reduction Act provides substantial funding to strengthen domestic battery supply chains. Leading producers, including Albemarle and Ganfeng Lithium, are adopting greener refining technologies and recycling programs to minimize environmental impact.

Category-wise Analysis

Battery Insights

Lithium-ion batteries are anticipated to dominate the global lithium carbonate consumption in 2025, accounting for approximately 64% of the market share, driven by the rapid adoption of EVs, large-scale renewable energy storage, and widespread use in consumer electronics.

Government initiatives, including China’s EV subsidies, the EU’s CO2 emission regulations, and U.S. zero-emission mandates, further reinforce reliance on lithium-ion technology. Continuous improvements in cathode chemistry, charging efficiency, and battery lifespan make these systems increasingly competitive and indispensable, driving demand alongside global electrification.

Emerging lithium-metal batteries are gaining attention to enable solid-state batteries with higher energy density, offering transformative potential for electric mobility and aviation. Governments in Japan, the U.S., and South Korea are investing in R&D as the industry advances toward early commercialization. Niche battery applications continue to absorb steady volumes, supported by initiatives such as the U.S. Battery500 Consortium and the EU’s Horizon Europe program, signaling future diversification in lithium carbonate demand.

Application Insights

Electric vehicles (EVs) are expected to hold around 40% of market share, making it the fastest-growing application with strong projected growth. Expansion is fueled by its growing adoption, large-scale renewable energy storage, and innovations demanding higher energy density and cost efficiency. Policy support, including China’s EV subsidies, the U.S. Inflation Reduction Act, and Europe’s Green Deal, has strengthened investments, making lithium carbonate essential to the energy transition.

Beyond batteries, lithium carbonate maintains a broad industrial footprint across glass and ceramics, pharmaceuticals, and aluminum processing. Growing construction initiatives, critical pharmaceutical uses, and lightweighting strategies in vehicles and aerospace sustain steady demand. Supported by regional sustainability programs and industrial innovation, these applications ensure diversified consumption, allowing lithium carbonate to remain resilient and relevant even as battery-driven growth dominates the market.

Regional Insights

Asia Pacific Lithium Carbonate Market Trends - China Strengthens Its Hold in Asia Pacific

Asia Pacific is anticipated to lead, holding a market share of approximately 60% in 2025. China is projected to remain the dominant country in the region, driven by its extensive battery manufacturing ecosystem, robust domestic EV demand, and strategic government policies that secure the clean energy supply chain.

Its leadership is reinforced by upstream investments and global collaborations, exemplified by Ganfeng Lithium’s resource acquisitions and downstream partnerships, which ensure long-term production capacity, cost advantages, and advanced manufacturing capabilities. Japan and South Korea leverage innovation-driven electronics and battery sectors, with companies such as Panasonic and LG Chem driving high-performance applications reliant on stable lithium carbonate supplies.

India is emerging rapidly, supported by the National Electric Mobility Mission Plan and the Production-Linked Incentive (PLI) scheme for advanced chemistry cells, fostering a self-reliant EV ecosystem. Southeast Asian nations are also gaining attention as new demand hubs, boosted by clean energy initiatives and foreign investment attraction. Together, these developments illustrate Asia Pacific’s market as a dynamic, interconnected region where industrial expansion and policy support drive long-term growth.

North America Lithium Carbonate Market Trends - The U.S. Leads North America Lithium Market; Canada Strengthens Potential.

North America is projected to be the fastest-growing region in 2025. The U.S. leads the region, driven by strong EV adoption, a vast battery manufacturing ecosystem, and supportive policy initiatives. Programs such as the Inflation Reduction Act have accelerated domestic investments in critical minerals, exemplified by Lithium Americas securing a US$2.26 Bn loan in 2024 for the Thacker Pass project, one of the largest lithium sources in the country. These investments reduce import reliance and strengthen U.S. competitiveness in global battery supply chains.

Canada is emerging as a strategic regional player, leveraging abundant resources and supportive policies under its Critical Minerals Strategy. Partnerships between Canadian miners and global automakers are fostering ethically sourced, low-carbon lithium supply chains. Combined with rising EV adoption and domestic processing incentives, Canada complements the U.S., ensuring a secure and resilient North American lithium carbonate market.

Europe Lithium Carbonate Market - Europe’s Industrial Core Fuels Lithium Demand and Strengthens Supply Resilience

Germany holds the leading position in Europe, driven by its strong automotive sector, advanced chemical processing capabilities, and growing battery recycling and refining infrastructure. Industrial initiatives such as BASF’s “black mass” recycling plant in Schwarzheide and its geothermal-linked lithium project with Vulcan Energy highlight Germany’s focus on securing low-carbon, domestically processed lithium. These investments reinforce Germany’s role as both a processing hub and key offtake partner, connecting OEM demand with upstream resource and recycling operations.

Sweden and other Nordic countries attract gigafactory investments, with Northvolt-related asset transactions underscoring ongoing industrial interest. Southern and Central Europe, including projects in Serbia and France, are benefiting from Critical Raw Materials initiatives and EU funding, aiming to localize processing and recycling. EU policy, including the Critical Raw Materials Act and Battery Regulation, is driving supply diversification, due diligence, and recycling obligations, shaping investment flows, market demand, and the competitive landscape across the region.

Competitive Landscape

The global lithium carbonate market is highly competitive, with major players adopting strategic mergers, acquisitions, and offtake agreements, securing access to high-demand markets in EVs and energy storage. These initiatives enhance production capacity, advance technological capabilities, and align operations with ESG and sustainability standards. By fostering innovation and efficiency, these strategic moves create a healthier competitive environment, motivating all players to optimize performance and capture emerging growth opportunities.

Suppliers and distributors are also becoming more closely integrated across mining, refining, and recycling networks, ensuring reliable sourcing and efficient delivery to key industries. This strengthened supply chain enhances cost management, resilience, and flexibility, supporting rapid response to demand fluctuations and enabling the market to capitalize on next-generation battery technologies and expand energy storage applications.

Key Industry Developments

- In July 2025, Chile’s state-owned miner Codelco received approval to extract up to 2.5 million metric tons of lithium metal equivalent by 2060, potentially translating to 330,000 tons of lithium carbonate annually via its joint venture with SQM.

- In July 2025, Ganfeng Lithium completed its purchase of the remaining 40% stake in Mali Lithium for US$342.7 Mn, gaining full control of the Goulamina lithium project and reinforcing its global upstream supply strategy.

- In 2025, Albemarle mothballed its Chengdu lithium hydroxide plant in China due to low prices, while ramping up sales at its Kemerton facility and reinforcing its strategic position in Western Australia.

Companies Covered in Lithium Carbonate Market

- SQM S.A.

- Livent Corp.

- Albemarle Corp.

- Pilbara Minerals

- Lithium Americas Corp.

- Ganfeng Lithium Co., Ltd.

- Orocobre Limited Pty. Ltd.

- Tianqi Lithium Corporation

- Mineral Resources Group Co., Ltd.

Frequently Asked Questions

The lithium carbonate market is set to reach US$26.9 Bn in 2025.

The accelerating adoption of EVs and large-scale renewable energy storage systems is driving strong global demand for lithium carbonate as a core enabler of the clean energy transition.

The lithium carbonate market is anticipated to grow at a CAGR of 12.7% from 2025 to 2032.

Growing investments in sustainable technologies combined with supportive government policies are creating fresh opportunities for lithium carbonate expansion across the energy storage and mobility sectors.

The major players include SQM S.A., Livent Corp., Albemarle Corp., Pilbara Minerals, and Lithium Americas Corp.