- Specialty & Fine Chemicals

- Nano Calcium Carbonate Market

Nano Calcium Carbonate Market Size, Share, and Growth Forecast, 2026 – 2033

Nano Calcium Carbonate Market by Product Type (Precipitated, Ground), Application (Plastics, Rubber, Paper, Paints & Coatings, Ink Industry, Pharmaceuticals & Food, Adhesives & Sealants), End-User (Automotive, Construction & Building Materials, Packaging, Electronics, Healthcare, Agriculture), and Regional Analysis for 2026-2033

Nano Calcium Carbonate Market Share and Trends Analysis

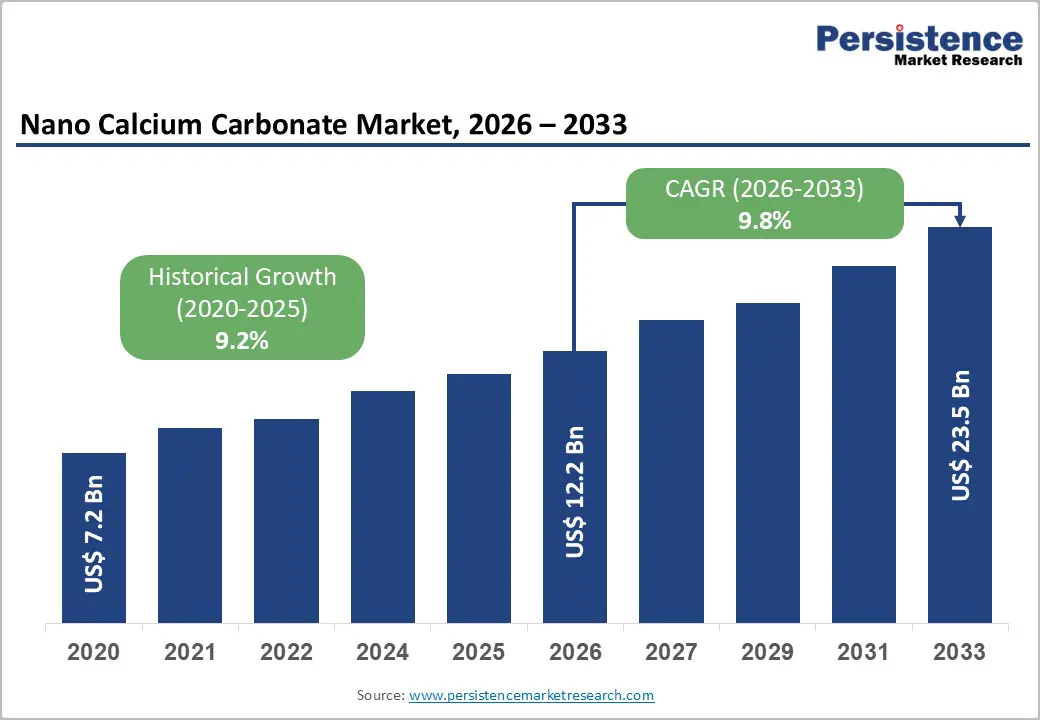

The global nano calcium carbonate market size is likely to be valued at US$ 12.2 billion in 2026, and is projected to reach US$ 23.5 billion by 2033, growing at a CAGR of 9.8% during the forecast period 2026−2033. The market demonstrates strong forward momentum, supported by expanding industrial modernization, rising material performance requirements, and increasing adoption of functional nanomaterials across high-volume manufacturing sectors. Growth primarily reflects the transition from conventional fillers toward engineered additives that improve mechanical strength, surface quality, and processing efficiency in end-use applications.

Industrial producers increasingly prioritize nanoscale materials to meet regulatory expectations regarding material efficiency, sustainability alignment, and waste reduction. Rising awareness of advanced materials science has accelerated the adoption of nano calcium carbonate across plastics, rubber, coatings, and pharmaceutical formulation workflows. Technological integration within compounding, dispersion, and surface treatment processes has enhanced consistency and scalability, thereby improving the viability of adoption across both developed and emerging economies.

Key Industry Highlights

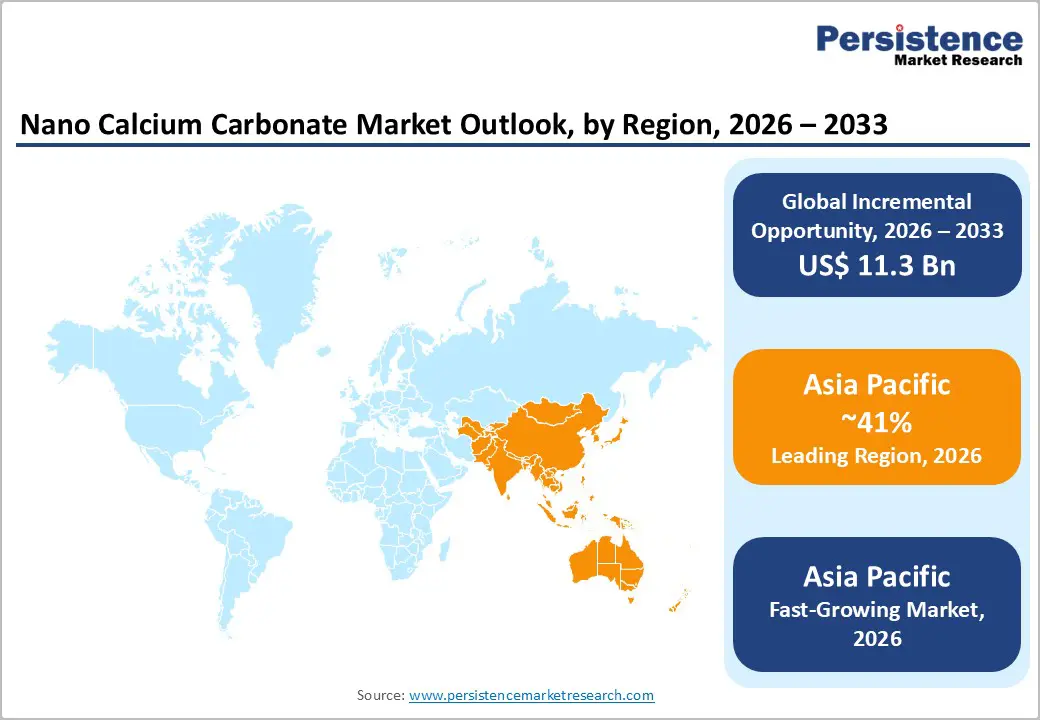

- Dominant Region: Asia Pacific is expected to hold about 41% market share in 2026, driven by strong industrial capacity and supportive government policies in China and India.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market through 2033, fueled by the increasing adoption of advanced composites and high-performance polymers across industries.

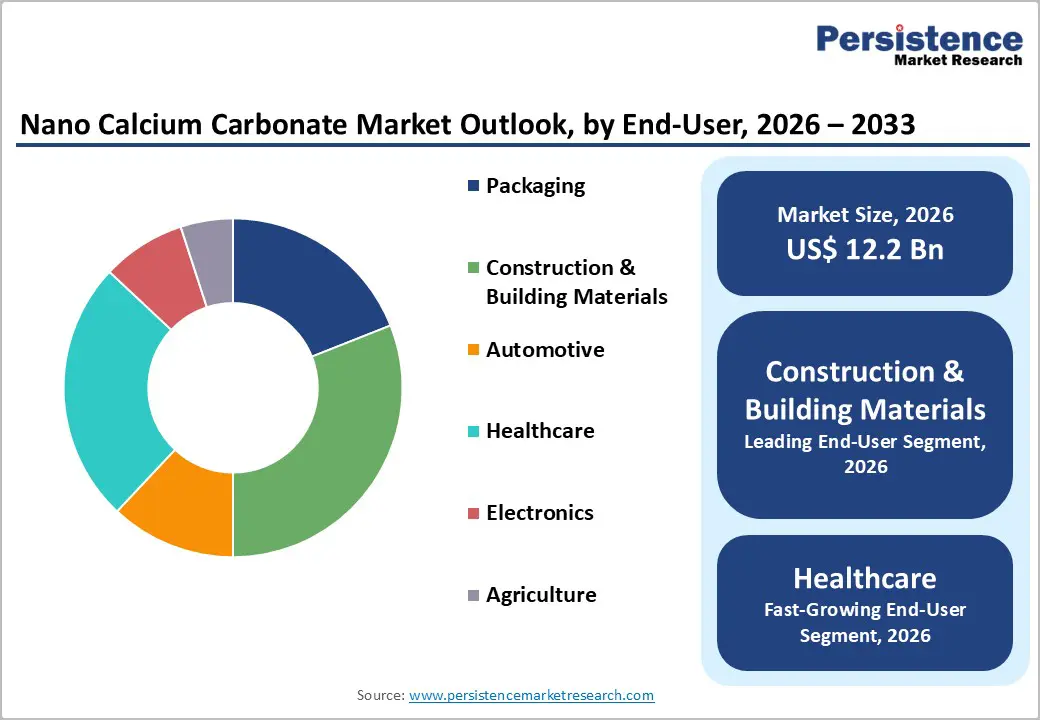

- Leading End-User: Construction and building materials are likely to lead, with about 31% market share in 2026, owing to the extensive use of nano calcium carbonate in cement, coatings, sealants, and insulation.

- Fastest-growing End-User: Healthcare is projected to grow the fastest through 2033, driven by increased emphasis on preventive care and expanding access to dietary supplements and fortified products.

| Key Insights | Details |

|---|---|

| Nano Calcium Carbonate Market Size (2026E) | US$ 12.2 Bn |

| Market Value Forecast (2033F) | US$ 23.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Shift toward High-Performance Functional Fillers

Industrial demand for high-performance functional fillers is driven by the need for materials that deliver enhanced mechanical strength, thermal stability, and dimensional precision in advanced applications. Government initiatives, such as the U.S. National Nanotechnology Initiative (NNI), highlight strategic investment in nanoscale research and commercialization, promoting the development of engineered materials with tailored functional properties. Sectors including automotive, electronics, and advanced manufacturing increasingly prioritize materials that improve performance, reduce weight, and extend product longevity, positioning functional fillers as a core component of modern material engineering strategies.

Support from government research programs fosters an innovation ecosystem in which nanoscale materials can meet stringent performance, safety, and sustainability requirements. These programs accelerate the integration of engineered fillers in industrial processes, enabling precise control over product attributes while optimizing manufacturing efficiency. Industrial adoption of such materials enhances competitiveness by improving durability, efficiency, and functional performance, thereby aligning with broader goals of technological advancement and sustainable production practices.

Expansion of Polymer, Rubber, and Coatings Manufacturing Capacity

Manufacturing capacity growth for polymers, rubber and coatings strengthens demand for nano calcium carbonate due to the foundational role these materials play in high-volume, industrial output, and value addition. Polymers and rubber products serve as critical feedstocks and functional materials for a wide range of end-use applications, from packaging and automotive components to industrial coatings and consumer goods. Government statistics for India indicate that the chemicals and petrochemicals sector, which includes base polymers and related intermediates, accounted for 8.1% of total manufacturing Gross Value Added (GVA) in FY-24 and has experienced steady increases in production through FY-25, as reported by the Department of Chemicals and Petrochemicals.

Demand for plastics, rubber and coating formulations expands in tandem with manufacturing capacity since downstream sectors continuously seek materials that balance enhanced performance with cost efficiency. Nano calcium carbonate provides high surface area reinforcement and improves mechanical, thermal and rheological properties that are often required as formulations become more complex in advanced polymer composites and protective coating systems. Rising production intensity in polymer and coating manufacturing amplifies reliance on functional fillers to maintain product quality, support operational efficiency, and optimize formulation performance across multiple industrial applications.

High Processing Complexity and Capital Intensity

The complexities associated with the manufacturing of nano-scale materials stem from the fundamental difference between research-scale synthesis and industrial-scale production. Nanomanufacturing involves processes that must consistently control matter at atomic and molecular levels while scaling throughput to industrial volumes. In the context of nanotechnology, maintaining nano-specific properties such as precise particle size, uniform distribution, and functional surface characteristics during production requires highly controlled environments, advanced fabrication tools, and tightly integrated quality assurance systems. These requirements translate into specialized capital equipment, such as cleanrooms, precision reactors, and high-resolution measurement instruments, that entail substantial upfront and operating expenditures. Public funding data indicate that the United States National Nanotechnology Initiative has allocated more than $45 billion in cumulative R&D funding through 2025 to support foundational nanoscience and infrastructure, underscoring the long-term investment required to advance technologies toward manufacturable processes.

The transition from prototype synthesis to mass production poses additional challenges that raise cost and technical barriers. Scaling nanomaterial production to high volumes while preserving nanoscale features is non-trivial; it requires novel manufacturing paradigms that integrate top-down and bottom-up techniques with reproducible process control to avoid defects and property variations. As documented in government nanomanufacturing discussions, scaling up these processes remains a primary technical challenge, as conventional manufacturing techniques often cannot economically sustain the complexity inherent in nanoscale assembly and defect control.

Regulatory Scrutiny surrounding Nanomaterials

Nanomaterials present distinctive challenges due to their nanoscale properties, including high surface area, enhanced chemical reactivity, and altered behavior compared to bulk materials. These characteristics can affect toxicity, environmental persistence, and bioaccumulation, necessitating detailed safety evaluation prior to industrial application. Governments have established regulatory frameworks to monitor and control the use of nanoscale substances. In the European Union, the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) and Classification, Labelling and Packaging (CLP) regulations mandate comprehensive characterization, hazard assessment, and reporting for all nanomaterials used in industrial and consumer products.

The regulatory landscape elevates production costs and influences commercialization strategies. Firms must implement exposure studies, risk mitigation plans, and safety protocols to meet both national and international requirements. In the United States, the Environmental Protection Agency (EPA) regulates nanoscale materials under the Toxic Substances Control Act (TSCA), which requires premanufacture notifications and reporting obligations for both existing and new substances. These obligations necessitate investment in testing, documentation, and occupational safety systems, thereby delaying scaling and product introduction.

Expanding Applications in Automotive Lightweighting and Composites

The automotive industry faces ongoing pressure to improve fuel efficiency and reduce emissions. Lightweighting materials play a pivotal role in achieving regulatory and performance targets. Nano calcium carbonate enhances polymer and composite formulations by increasing stiffness and mechanical strength while minimizing weight. Its fine particle size ensures uniform dispersion, improving material integrity and surface finish in components such as dashboards, bumpers, interior panels, and under-the-hood parts. The compatibility with thermoplastics and thermosets enables manufacturers to design parts with thinner walls and reduced material usage without compromising durability or safety standards.

The composite sector benefits from nanoscale reinforcement, which enhances thermal stability, impact resistance, and dimensional consistency. Integration into fiber-reinforced composites supports structural applications while maintaining lightweight characteristics. Manufacturers leverage this property to optimize material costs while achieving high-performance benchmarks in automotive assemblies. Demand from high-volume production lines and premium vehicle segments drives adoption, creating a sustained growth pathway.

Increasing Focus on Eco-Friendly and Bio-Based Materials

Government policy momentum toward bioeconomy expansion and regulatory sustainability frameworks is shifting industrial material demand profiles. National strategies such as India’s BioE3 (Biotechnology for Economy, Environment and Employment) Policy explicitly target the growth of renewable and bio-based product streams, including bio-based chemicals and biopolymers, aligning industrial development with climate objectives and circular resource models. This policy fosters research, innovation and commercialisation of materials with lower life-cycle environmental impact under a broader circular bioeconomy blueprint articulated by national science and technology authorities.

Public sector investment and outcomes illustrate why this strategic focus presents an opportunity. According to the Ministry of Science and Technology, India’s bioeconomy expanded from $10 billion to $165.7 billion by 2024 under supportive policy regimes, with targets set to reach $300 billion by 2030, reflecting the rapid scaling of renewable and bio-based industries within just over a decade. Firms incorporating bio-compatible materials can align their product portfolios with national decarbonization targets and increasingly stringent product standards in public procurement, and leverage government incentives aimed at scaling sustainable technologies.

Category-wise Analysis

Product Type Insights

Precipitated nano calcium carbonate is poised to lead with a forecasted 62% share in 2026, owing to its superior particle size control, uniform morphology, and enhanced surface modification capability. These characteristics enable consistent performance across high-precision applications such as plastics compounding, rubber reinforcement, and pharmaceutical excipients. Controlled precipitation processes allow manufacturers to tailor physical properties according to end-use requirements, supporting formulation stability and processing efficiency. Industrial users demonstrate strong preference for precipitated variants due to predictable dispersion behavior and compatibility with automated production systems.

Ground nano calcium carbonate is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by cost efficiency, expanding application scope, and improvements in grinding and classification technologies. Advances in micronization and surface treatment enhance performance characteristics, narrowing functional gaps relative to precipitated alternatives. Adoption accelerates across construction materials, adhesives, and sealants where volume efficiency and cost optimization remain critical. Accessibility advantages support penetration within emerging markets, where industrial expansion prioritizes scalable materials with flexible performance thresholds. Innovation in grinding equipment and dispersion techniques improves treatment effectiveness, enabling broader formulation acceptance.

End-User Insights

The construction and building materials segment is slated to hold a dominant position, with an anticipated 31% of the nano calcium carbonate market revenue share in 2026, driven by extensive use of the material in cementitious composites, coatings, sealants, and insulation materials. Its inclusion in cement and concrete enhances compressive strength, workability, and long-term durability, supporting structures exposed to high mechanical stress and environmental conditions. Coatings and sealants benefit from improved adhesion, opacity, and chemical resistance, thereby reducing lifecycle maintenance costs. Insulation materials exhibit improved thermal and moisture stability, thereby aligning with energy-efficiency standards. Rapid urbanization and large-scale infrastructure initiatives increase demand for high-performance materials that deliver both economic and operational efficiency.

The healthcare segment is projected to be the fastest-growing end-user segment between 2026 and 2033, driven by increased emphasis on preventive care, the clinical credibility of calcium-based formulations, and expanding access to nutritional products. Nano calcium carbonate is a reliable ingredient in dietary supplements, pharmaceuticals, and fortified foods, enhancing bioavailability and product stability. Technology-enabled formulation processes support uniform particle distribution, enhancing efficacy across dosage forms. Distribution channel digitalization enables a wider reach to urban and rural populations, while cost-efficient production methods lower barriers for institutional adoption. Public health initiatives emphasizing preventive care and supplementation further drive market penetration and sustained growth.

Regional Insights

North America Nano Calcium Carbonate Market Trends

North America is projected to account for a significant share of the nano calcium carbonate market in 2026, supported by advanced manufacturing capabilities, well-established chemical industries, and stringent regulatory frameworks. Countries such as the United States and Canada drive consumption across automotive, construction, plastics, and coatings sectors, leveraging nano-scale fillers to improve mechanical strength, thermal stability, and surface finish. Automotive manufacturers incorporate nano calcium carbonate into lightweight components, interior panels, and composite parts to enhance fuel efficiency and meet regulatory emissions standards. Construction and industrial applications benefit from its incorporation into cementitious composites, sealants, and coatings, thereby extending product service life and reducing maintenance cycles.

Adoption growth is reinforced by increasing emphasis on innovation, sustainability, and energy efficiency. Advanced polymer and composite industries integrate nano calcium carbonate to produce high-strength, lightweight materials suitable for electric vehicles, packaging, and specialty industrial applications. Public and private initiatives supporting technological innovation, materials research, and environmental compliance contribute to product development and improved performance. Expansion in healthcare and pharmaceutical applications, including bio-compatible formulations and dietary supplements, further diversifies demand. Access to skilled technical talent, robust logistics networks, and early adoption of digital manufacturing solutions accelerates material integration across multiple sectors.

Europe Nano Calcium Carbonate Market Trends

Europe maintains a substantial presence in the nano calcium carbonate market, supported by well-established industrial infrastructure, high-quality manufacturing standards, and advanced regulatory frameworks. Countries such as Germany, France, and Italy drive consumption across automotive, construction, and polymer applications, utilizing nano-scale fillers to enhance mechanical strength, thermal performance, and dimensional stability. Automotive manufacturers incorporate nano calcium carbonate into lightweight components, dashboards, and composite interiors to improve fuel efficiency and meet strict emission regulations. Construction applications include coatings, sealants, and cementitious composites, enhancing durability and reducing maintenance requirements.

Steady expansion in material adoption is supported by the shift toward sustainable and eco-efficient solutions. Environmental regulations on emissions and resource efficiency encourage replacement of conventional fillers with high-purity nano calcium carbonate for lightweighting and energy-efficient production. Research collaborations and public-private initiatives in countries such as Germany and Sweden foster the development of biocompatible and functionalized particles for healthcare, food fortification, and high-performance composites. Awareness of material efficiency, circular economy practices, and demand for high-quality industrial standards accelerates utilization across automotive, construction, and specialty polymer sectors.

Asia Pacific Nano Calcium Carbonate Market Trends

Asia-Pacific is expected to dominate the nano calcium carbonate market, accounting for an estimated 41% of the market in 2026, reflecting robust industrial scale and strategic policy support in major countries such as China and India. China anchors market leadership with extensive manufacturing capacity across automotive, plastics, construction, and electronics sectors, supported by long-term industrial initiatives such as the Made in China 2025 plan, which emphasizes advanced materials and high-performance industrial inputs. China’s National Development and Reform Commission committed significant funding to bolster advanced manufacturing capabilities, thereby enabling the widespread integration of nanoscale fillers that improve product performance in high-volume applications. India’s expanding automotive and packaging industries benefit from incentives such as the Production Linked Incentive (PLI) scheme for automotive components, which encourages the adoption of next-generation materials and supports the local production of engineered fillers.

Asia Pacific is forecasted to be the fastest-growing market for nano calcium carbonate market between 2026 and 2033, stimulated by accelerated industrial modernization, expanding R&D investment, and growing end-use diversification. Rapid automation of production lines and adoption of digital design tools enhance the integration of nano-additives into lightweight composites and high-performance polymers used in healthcare products, advanced coatings, and electric vehicle components. Institutional research bodies and government-Supported material research centers in India and Southeast Asian economies contribute to innovation in particle modification and functional dispersion, which drives uptake in emerging applications. National programs to expand electronics and semiconductor ecosystems, such as India’s Semiconductor Mission 2.0 to strengthen materials supply chains, further stimulate demand for advanced nanoparticle solutions that improve thermal and mechanical performance.

Competitive Landscape

The global nano calcium carbonate market structure reflects moderate consolidation, with major multinational producers such as Omya International AG, Imerys S.A., Minerals Technologies Inc., and MARUO CALCIUM CO., LTD. accounting for a significant share alongside regional specialists. These leading companies leverage extensive production capacities, advanced processing technologies, and deep expertise in nano calcium carbonate applications to maintain a competitive advantage. Their operations span multiple end-use industries, including automotive, construction, polymers, coatings, and healthcare, allowing them to serve high-volume global demand while customizing solutions for specialized requirements.

Competitive positioning in this environment centers on technological capability, application knowledge, and regulatory compliance. Companies optimize processing techniques to ensure uniform particle size, high purity, and compatibility with diverse material systems, which is critical for automotive lightweighting, high-performance composites, and specialty coatings. Compliance with environmental and safety regulations, particularly in chemical handling and nanoparticle management, influences market access and customer trust. Firms that integrate technical expertise with responsive service and global distribution networks strengthen relationships with industrial clients and end-users.

Key Industry Developments

- In January 2026, DIAMOND QUANTUM Biotech showcased its nano calcium carbonate technology at the nano tech 2026 exhibition in Tokyo, highlighting applications in chemical manufacturing and sustainable agriculture. The company demonstrated how recycled carbon dioxide can be transformed into high-surface-area nano calcium carbonate for use in polymers, coatings, and soil-enhancing fertilizers.

- In November 2025, researchers at Alexandria University and Al-Jouf University reported the development of novel polystyrene blends doped with polycaprolactone and nano calcium carbonate that enhanced biodegradation and modified mechanical properties, offering potential for more environmentally friendly polymer applications.

- In October 2025, Amorphical reported positive interim results from its ongoing open-label clinical trial of a nano-amorphous calcium carbonate (ACC) therapy for moderate-to-severe Crohn’s disease, with approximately 71% of patients showing meaningful clinical improvement and nearly half achieving clinical remission when the treatment is added to standard care.

Companies Covered in Nano Calcium Carbonate Market

- Omya International AG

- Imerys S.A.

- Minerals Technologies Inc.

- MARUO CALCIUM CO., LTD.

- Huber Engineered Materials.

- Qingdao ECHEMI Digital Technology Co., Ltd.

- Takehara Chemical

Frequently Asked Questions

The global nano calcium carbonate market is projected to reach US$ 12.2 billion in 2026.

Rising demand for lightweight, high-performance composites and multifunctional fillers across automotive, construction, plastics, and healthcare applications are driving the market.

The market is poised to witness a CAGR of 9.8% from 2026 to 2033.

Integration of nano calcium carbonate in automotive lightweighting, high-performance composites, and sustainable construction materials presents key market opportunities.

Some of the key market players include International AG, Imerys S.A., Minerals Technologies Inc., MARUO CALCIUM CO., LTD., and Huber Engineered Materials.