- Specialty & Fine Chemicals

- Ammonium Bicarbonate Market

Ammonium Bicarbonate Market Size, Share, and Growth Forecast 2026–2033

Ammonium Bicarbonate Market by Form (Powder, Granule, Crystal), Grade (Tech Grade, Food Grade, Pharma Grade), Distribution Channel (Direct, Wholesale, Online), Application (Leavening Agent, Baking Agents, Others), and Regional Analysis 2026 – 2033

Ammonium Bicarbonate Market Share and Trends Analysis

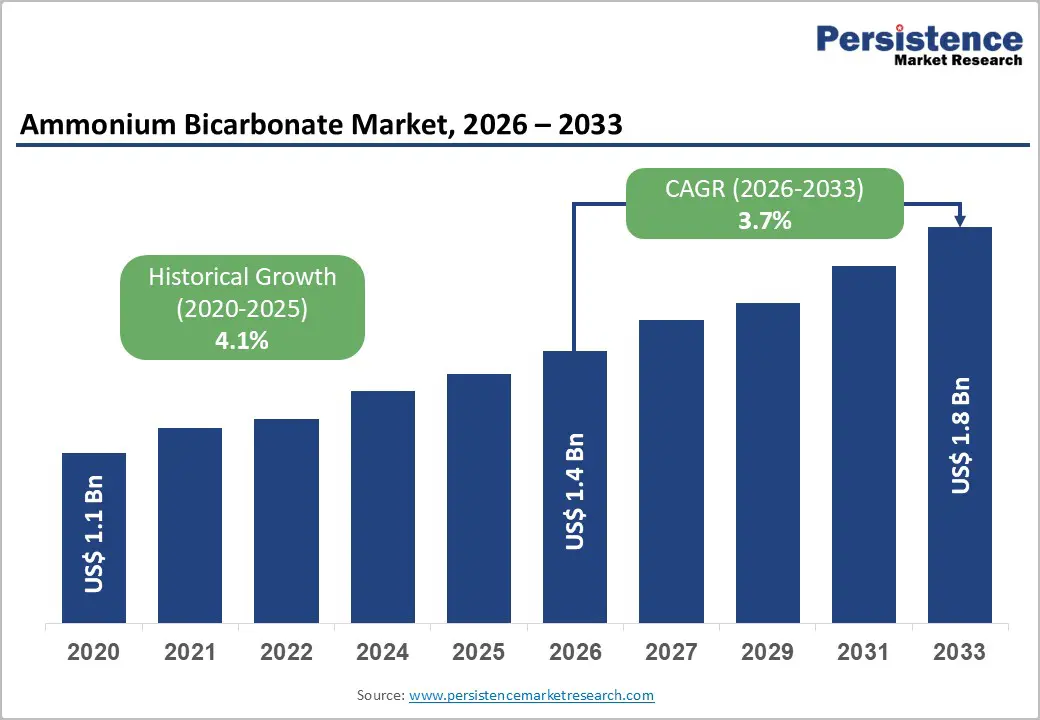

The global ammonium bicarbonate market size is likely to be valued at US$1.4 billion in 2026 and is projected to reach US$1.8 billion by 2033, growing at a CAGR of 3.7% during the forecast period between 2026 and 2033, driven by the stabilization of the global food processing sector and shifting agricultural priorities toward high-efficiency nitrogen sources.

The market expansion is driven by persistent demand from the food and beverage industry, where ammonium bicarbonate serves as a critical leavening agent in bakery products, coupled with sustained agricultural applications as a nitrogen-rich fertilizer. Growing emphasis on sustainable production methodologies, technological advances in manufacturing efficiency, and expanding pharmaceutical formulations are expected to sustain market momentum.

Key Industry Highlights

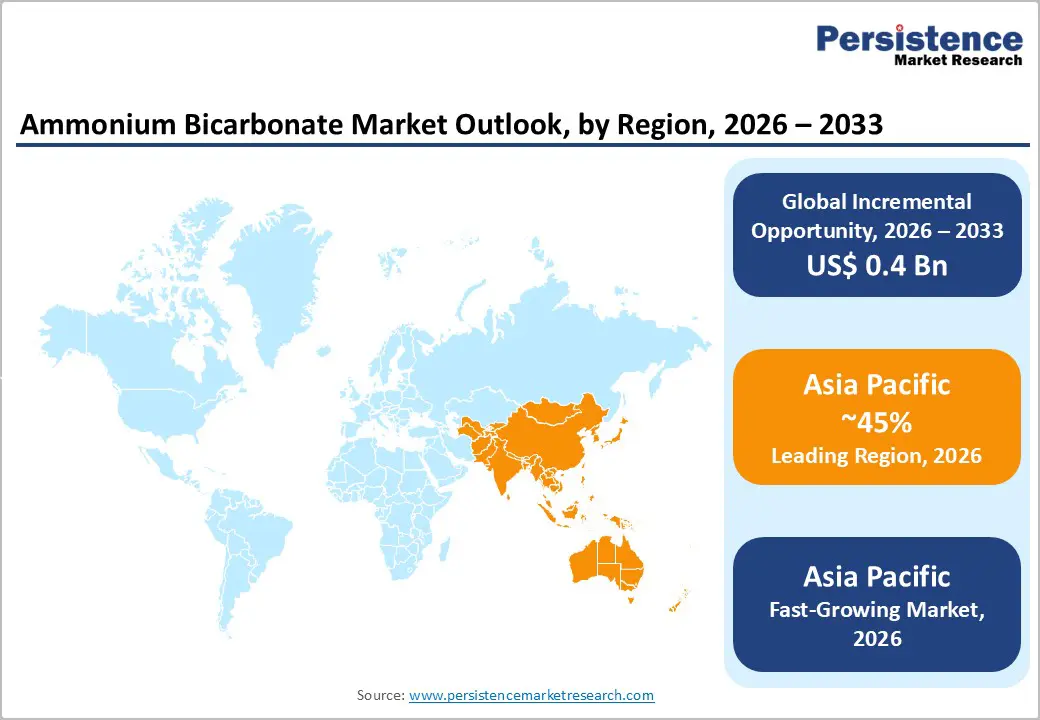

- Leading Market Region: Asia Pacific leads the global ammonium bicarbonate market, holding around 45% share, supported by large-scale, driven by chemical manufacturing, and gradual regulatory harmonisation with international standards.

- Leading Form Type: Powdered ammonium bicarbonate is expected to be the leading form, accounting for approximately 62% of total market revenue. Growth is anticipated to be driven by its compatibility with automated, high-throughput production lines, superior dosing accuracy, and consistent thermal decomposition behaviour required in industrial baking and pharmaceutical processing.

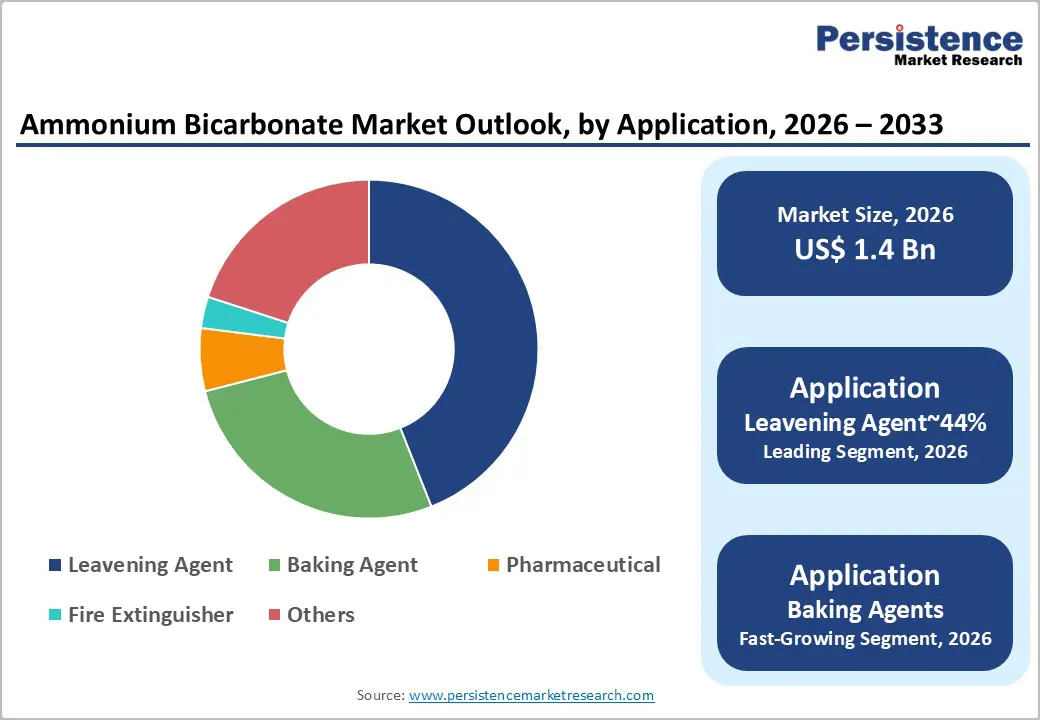

- Leading Application Type: Leavening agent applications are expected to remain the leading use case, accounting for approximately 44% of total demand, supported by sustained industrial bakery production of crackers, biscuits, and dry cookies.

- Key Industry Developments: Major developments include large-scale green ammonia financing initiatives, USDA-supported fertilizer production expansion, and rising chemical and pharmaceutical investments, positioning India as an emerging hub. In December 2024, the USDA (U.S. Department of Agriculture) announced a US$116 million investment under the Fertilizer Production Expansion Program (FPEP). This investment specifically targets expanding domestic fertilizer production capabilities, including ammonium bicarbonate, to lower resource expenditures for farmers and reduce consumer food costs.

| Key Insights | Details |

|---|---|

| Ammonium Bicarbonate Market Size (2026E) | US$1.4 Bn |

| Market Value Forecast (2033F) | US$1.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Nitrogen-based Fertilizer Applications in Sustainable Agriculture

The expansion of nitrogen-based fertilizer applications within sustainable agriculture frameworks is emerging as a core growth driver for the ammonium bicarbonate market. Regulatory bodies and agricultural agencies increasingly recognize ammonium bicarbonate as a viable nitrogen source that enhances soil fertility while avoiding chloride accumulation and long-term salinity stress. This positioning aligns with broader sustainability mandates emphasizing soil health, nutrient efficiency, and reduced environmental externalities.

As fertilizer policies progressively favor balanced nitrogen inputs, ammonium bicarbonate is being integrated into customized nutrient programs targeting yield stability rather than maximum short-term output. At the market level, intensifying food security pressures across emerging agrarian economies are reinforcing demand for cost-efficient nitrogen enrichment solutions. Ammonium bicarbonate benefits from favorable economics, compatibility with blended fertilizer formulations, and adaptability across diverse cropping systems.

Adoption is further supported by institutional efforts to localize fertilizer production and diversify nitrogen supply chains, reducing exposure to import dependency and price volatility. These structural forces collectively position ammonium bicarbonate to capture incremental share within sustainable and region-specific fertilizer strategies.

Volatility in Raw Material Pricing and Supply Chain Instability

Volatility in raw material pricing and persistent supply chain instability represent a structural restraint for the ammonium bicarbonate market. Production economics are tightly linked to the availability and cost dynamics of ammonia and carbon dioxide, both of which remain highly exposed to upstream energy market disruptions. Fluctuations in natural gas markets directly compress producer margins, reducing pricing visibility and weakening cost pass-through mechanisms.

This instability complicates capacity planning and undermines the feasibility of long-term supply agreements across agricultural and industrial end-uses. Heightened input volatility disproportionately impacts smaller and mid-sized manufacturers with limited hedging capability and balance sheet resilience. The resulting risk asymmetry reinforces market concentration, as larger integrated producers are better positioned to absorb short-term shocks and secure feedstock access.

In June 2025, the ammonia market prices surged by nearly 30% year on year, indicating a return to cost-driven pricing due to feedstock pressures. This confirms that the market remains highly vulnerable to sudden, significant price surges in natural gas (the primary feedstock) and geopolitical factors, which directly squeeze producer margins and create persistent long-term planning risks.

Green Ammonia and Sustainable Manufacturing Innovations

Green ammonia and sustainable manufacturing innovations are creating a structurally attractive opportunity for the ammonium bicarbonate market. Policy-backed decarbonization agendas and corporate net zero commitments are accelerating the shift toward low-emission ammonia synthesis, including waste-to-ammonia pathways and renewable energy-integrated production systems. These advances materially improve the environmental footprint of ammonium bicarbonate, strengthening compliance alignment across agriculture, food processing, and pharmaceutical supply chains.

As regulatory scrutiny around lifecycle emissions intensifies, cleaner production routes are becoming a prerequisite rather than a differentiator. Technology convergence between renewable power generation, hydrogen sourcing, and ammonia synthesis is reshaping capital allocation across the nitrogen value chain. Sustainable manufacturing capabilities enhance margin durability by reducing exposure to fossil fuel volatility while enabling participation in green procurement programs and preferential regulatory frameworks.

Producers with early access to scalable green ammonia infrastructure are positioned to capture premium demand in environmentally regulated markets, reinforcing competitive barriers and expanding long-term addressable demand without reliance on volume-led pricing strategies.

Category–wise Analysis

Form Insights

Powdered ammonium bicarbonate is expected to remain the leading and fastest-growing form, accounting for approximately 62% of total market revenue. This dominance is anticipated to persist as powdered formulations align closely with the operational needs of large-scale food processing, precision agriculture, and pharmaceutical manufacturing. The fine particle structure enables rapid and complete thermal decomposition, which supports consistent texture development in baked products such as crackers and biscuits.

Manufacturers favor powder for its dosing accuracy, uniform dispersion, and reduced risk of batch variability in automated production lines. Food ingredient suppliers and processors associated with brands such as BASF, Nutrien, and Sumitomo Chemical increasingly prioritize powdered grades to meet clean-label and performance consistency expectations. Cost efficiency in bulk handling and compatibility with high-throughput systems further reinforce its structural advantage across industrial end-use environments.

Crystal and granule forms are likely to represent the fastest-growing segment, supported by industrial users requiring defined particle morphology, controlled reactivity, and improved storage stability. High-purity crystalline variants continue to serve specialized pharmaceutical synthesis, electronics processing, and advanced ceramics manufacturing.

Producers such as DCW Limited, Addcon, and Hubei Xingfa Chemicals are increasingly investing in precision crystallization and anti-caking technologies to strengthen performance consistency. Despite these advantages, adoption is expected to remain functionally driven, positioning crystal and granule forms as structurally important but secondary to powder-led demand expansion.

Application Insights

Leavening agent applications are anticipated to remain the leading use case for ammonium bicarbonate, accounting for approximately 44% of total demand over the forecast period. This segment is expected to retain its dominance due to ammonium bicarbonate’s residue-free thermal decomposition, a property that continues to be indispensable for low-moisture baked products such as crackers, thin biscuits, and dry cookies.

Industrial bakeries supplying global snack brands are likely to sustain high-volume consumption, particularly across Asia Pacific and Europe, where packaged bakery penetration remains strong. Established ingredient suppliers such as BASF, Shandong Hualu-Hengsheng, Mangalore Chemicals & Fertilizers, and Sumitomo Chemical are expected to benefit from long-standing formulations that rely on baker’s ammonia for texture-critical SKUs. Regulatory clarity under E 503(ii) and FDA GRAS status is also anticipated to support continuity, even as manufacturers invest in emission-control systems to address ammonia release during large-scale baking operations.

Baking agent applications are expected to emerge as the fastest-growing segment, supported by the expansion of processed food portfolios and increasing formulation sophistication across emerging and mature markets. Demand is likely to be driven by product innovation in dry and shelf-stable baked goods, where ammonium bicarbonate is used as part of broader baking agent systems rather than as a single-function leavener.

Food manufacturers in China, India, and Southeast Asia are anticipated to expand cracker, wafer, and snack biscuit lines, reinforcing usage in compound baking solutions. Growth is also expected to be reinforced by improved automation in commercial bakeries, enabling precise dosing, and by wider access through specialty ingredient distributors serving artisanal and mid-scale producers. As clean-label positioning and lower-sodium formulations gain traction, ammonium bicarbonate suppliers are likely to focus on purity optimization and compatibility within hybrid baking agent systems to sustain momentum in this application category.

Regional Insights

Asia Pacific Ammonium Bicarbonate Market

Asia Pacific is expected to remain both the leading and fastest-growing regional market, accounting for approximately 45% of the global demand in 2026, supported by large-scale production capacity, rapid urbanization, and expanding packaged food consumption. China dominates regional output, supplying the majority of volume, while India represents the fastest-expanding consumption market, driven by rising bakery product demand and agricultural fertilizer requirements to support food security.

Government initiatives promoting domestic chemical manufacturing and sustainability investments further reinforce regional self-sufficiency and attract foreign capital, strengthening Asia Pacific’s structural market position. Regulatory frameworks across the region increasingly align with international standards, though implementation varies by jurisdiction, creating both compliance obligations and opportunities for technologically advanced producers.

Stringent environmental mandates in China encourage production upgrades, while India’s gradual harmonization with global norms supports standardized, high-quality output. Competitive dynamics emphasize cost efficiency, production scale, and distribution network robustness, with local manufacturers capturing volume-led demand and multinational entrants targeting premium food and pharmaceutical applications. Collectively, these forces position Asia Pacific to sustain market leadership while driving high growth trajectories through structural demand and regulatory alignment.

North America Ammonium Bicarbonate Market

North America is expected to remain a significant and mature regional market, supported by advanced food processing and pharmaceutical manufacturing infrastructure, a robust bakery industry, and expanding fertilizer production capacity. The U.S. forms the core consumption base, driven by industrial-scale bakeries, pharmaceutical production, and mechanized agriculture. Government initiatives, including the USDA Fertilizer Production Expansion Program, reinforce domestic nitrogenous fertilizer supply, sustaining steady demand for food-grade ammonium bicarbonate across commercial and industrial applications.

Regulatory oversight through the FDA and EPA establishes clear compliance frameworks for food, agricultural, and industrial uses, while progressive environmental mandates encourage adoption of low-carbon production and sustainable sourcing practices. Multinational producers, including BASF SE and Honeywell International, leverage technological capabilities, global distribution networks, and specialty-grade offerings to maintain market presence. Regional manufacturers focus on niche segments and sustainability alignment, collectively ensuring moderate, stable growth driven by structural demand, regulatory compliance, and strategic investments in production efficiency.

Europe Ammonium Bicarbonate Market

Europe is expected to remain a significant regional market, supported by a mature food processing sector, established pharmaceutical manufacturing, and diversified specialty chemical applications. Germany, France, and the U.K. lead regional consumption, driven by stable bakery production and industrial use in pharmaceuticals, textiles, and ceramics. Demand is reinforced by clean-label trends, eco-certification requirements, and consistent regulatory harmonization under the EU REACH framework, which enhances supply chain predictability and enables manufacturers to maintain quality-compliant operations across member states.

Regulatory stringency and environmental compliance dominate regional market dynamics, with strict ammonia emission limits and water pollution prevention measures shaping production practices. These mandates encourage technical-grade and specialty applications while moderating growth in certain food-grade segments. European manufacturers, including Solvay and Alzchem Group AG, leverage sustainability credentials, long-standing customer networks, and circular economy practices, such as CO2 recycling in synthesis processes, to reinforce competitive positioning. Collectively, these structural factors sustain moderate but stable growth, emphasizing quality, environmental performance, and regulatory alignment as key determinants of market leadership and operational continuity.

Competitive Analysis

The global ammonium bicarbonate market is moderately consolidated, with the top five players, including BASF, Solvay, and UBE Corporation, controlling approximately 55–60% of total market revenue. Market concentration is strongest in the food-grade segment, where regulatory compliance and safety certifications, such as GMP and HACCP, create high entry barriers and favor established manufacturers.

The technical-grade segment remains fragmented, with regional producers in China and India capturing volume through cost advantages and proximity to growing markets. Competitive differentiation is increasingly driven by scale, technological capability, and regulatory adherence, while mid-tier players focus on specialized applications in food or pharmaceuticals. Forward-looking dynamics indicate sustained consolidation in premium segments, alongside continued regional competition in price-sensitive markets.

Key Industry Developments:

- In May 2025, Sumitomo Chemical India Ltd conducted its Q4 FY25 earnings call and achieved its highest-ever annual profit after tax of INR 506.4 crore (US$6.09 million). The company’s leadership team outlined a roadmap for continued growth through strategic capital expenditures and a focus on operational efficiency and volume expansion.

- In December 2024, BASF SE started up an expanded ammonium chloride facility at its Ludwigshafen site, increasing its capacity by 50%. The expansion utilized advanced, highly efficient production processes to ensure a long-term supply of high-purity chemical precursors required for strict food and feed regulatory standards.

- In July 2024, BASF SE announced a production network restructuring to source active ingredients from third-party suppliers. This strategic shift toward a "light asset" model allowed the company to maintain competitiveness and profitability in the ammonium derivative market while managing global overcapacity.

- In April 2024, JERA Co. & ReNew Power announced a joint venture for a major green ammonia production project in India. The project aimed to produce 100,000 tons of green ammonia annually using renewable energy, securing a sustainable feedstock for downstream bicarbonate and fertilizer products.

Companies Covered in Ammonium Bicarbonate Market

- BASF SE

- Solvay S.A.

- UBE Corporation

- Shandong ShunTian Chemical Group

- Sumitomo Chemical Co.

- Shandong Hualu-Hengsheng

- Nissan Chemical Corporation

- Esseco UK

- Anhui Jinhe Industrial Co.

- Wanhua Chemical Group

- Sumitomo Chemical Co.

- Tata Chemicals Ltd.

- JERA Co.

- Sumitomo Chemical India Ltd.

- Honeywell International Inc.

- Shandong Haihua Group Co.

- Yara International ASA

- YNC (Yongye Chemical)

- Ankitraj Expotrade

- Weijiao Holdings Group

Frequently Asked Questions

The global ammonium bicarbonate market is valued at US$1.4 billion in 2026 and is projected to reach US$1.8 billion by 2033, reflecting steady demand across food, fertilizer, and pharmaceutical applications.

Asia Pacific dominates due to large-scale manufacturing capacity in China, accelerating agricultural modernization in India, and strong downstream demand from food processing and fertilizer industries.

The ammonium bicarbonate market is expected to grow at a CAGR of 3.7% between 2026 and 2033, indicating moderate but stable expansion supported by diversified end-use demand.

Key opportunities are emerging in green ammonia integration, government-backed fertilizer expansion programs, and capacity additions aligned with sustainability and cost stabilization initiatives, particularly in Asia and North America.

Major players include BASF SE, Solvay S.A., UBE Corporation, Sumitomo Chemical Co., Tata Chemicals Ltd., Yara International ASA, Shandong Hualu-Hengsheng, Nissan Chemical Corporation, Esseco UK, and Wanhua Chemical Group.