- Medical Devices

- Cancer Tissue Diagnostics Market

Cancer Tissue Diagnostics Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cancer Tissue Diagnostics Market by Product (In Situ Hybridization (ISH) Test Kits, Molecular Diagnostics Test Kits, Companion Diagnostics Test Kits, and Immunohistochemistry (IHC) Test Kits), by Application (Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, Ovarian Cancer, Hematologic Cancer, Liver Cancer, Pancreatic Cancer, Skin Cancer (Melanoma), and Others) by End User (Hospitals, Specialty Centers, Long-term Care Centers, Diagnostic Centers, and Academic & Research Institutes), and Regional Analysis from 2026 to 2033

Cancer Tissue Diagnostics Market Share and Trend Analysis

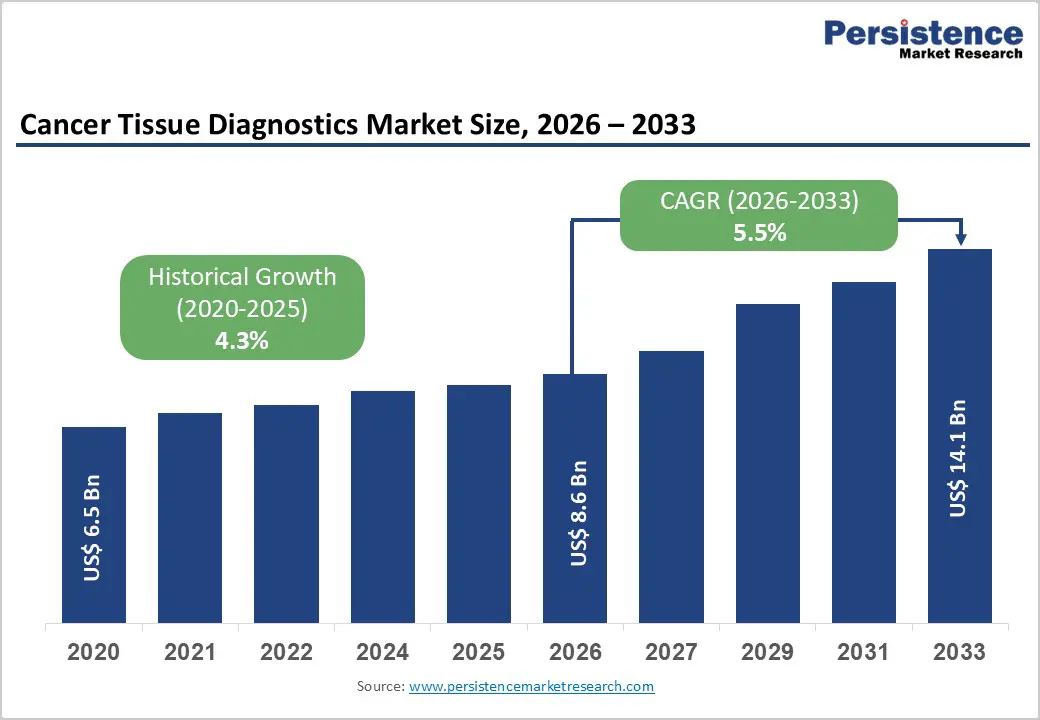

The global cancer tissue diagnostics market size is estimated to grow from US$ 8.6 Bn in 2026 to US$ 14.1 Bn by 2033. The market is projected to record a CAGR of 5.5% during the forecast period from 2026 to 2033.

The global shift toward precision oncology is significantly accelerating the uptake of tissue-based cancer diagnostics across hospital laboratories and reference centers. Histopathology, immunohistochemistry, in situ hybridization, and molecular profiling are now central to tumor classification, biomarker identification, and therapy selection. Rising cancer incidence, expanding screening programs, and the growing use of targeted and immuno-oncology drugs are increasing the demand for accurate tissue characterization.

Technological advancements such as automated staining platforms, multiplex biomarker assays, next-generation sequencing integration, and AI-enabled digital pathology are improving diagnostic accuracy and turnaround times. Standardized sample preparation workflows and closed-system reagent platforms are enhancing reproducibility across institutions. Continuous biomarker discovery and companion diagnostic co-development with pharmaceutical innovators are further embedding tissue testing into oncology treatment algorithms. Additionally, modernization of pathology infrastructure in emerging economies and increasing participation in global clinical trials are broadening accessibility. As personalized treatment strategies become routine, tissue diagnostics remain indispensable for delivering evidence-based cancer care across developed and developing healthcare systems.

Key Industry Highlights:

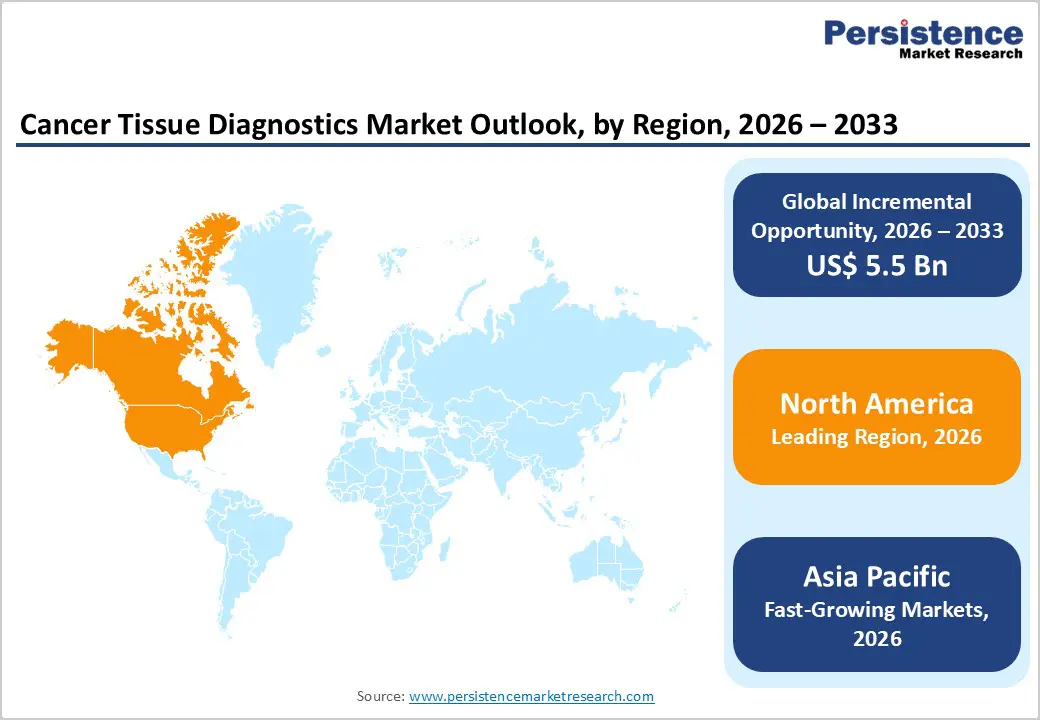

- Leading Region: North America holds 46.7% of the global market, driven by advanced oncology infrastructure, strong biomarker testing guidelines, rapid adoption of genomic profiling, and early deployment of digital pathology systems across major cancer centers. Fastest-Growing Region: Asia Pacific is expanding at the quickest rate, supported by laboratory modernization initiatives, rising cancer awareness, improved access to molecular testing, and growing investment in tertiary oncology facilities.

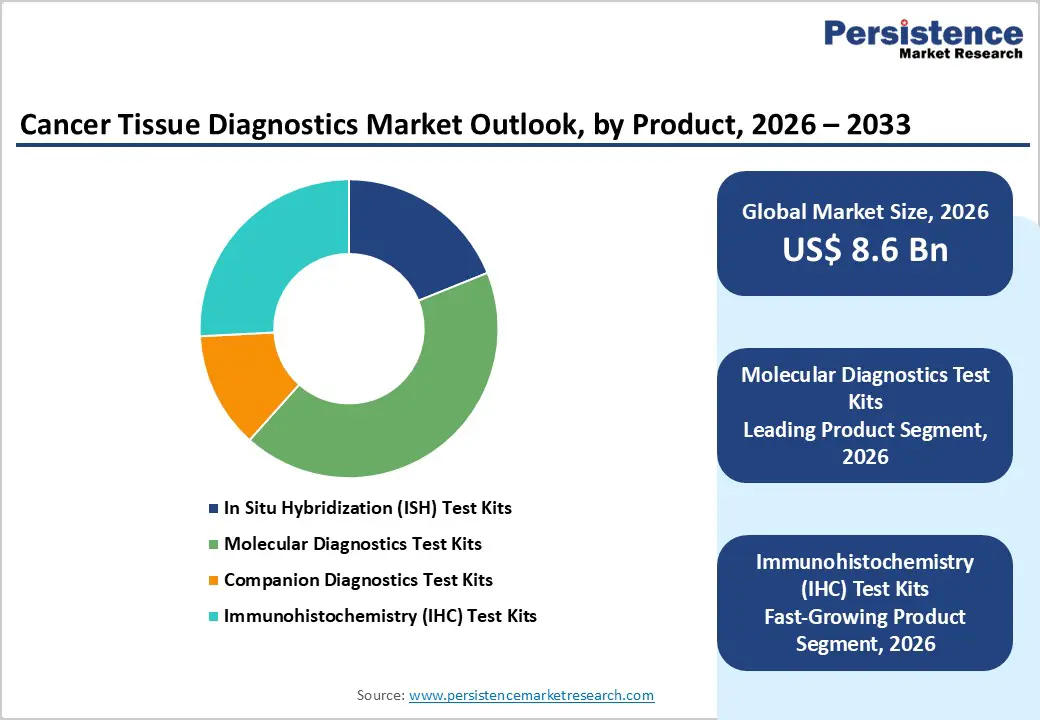

- Leading Product Segment: Molecular diagnostics test kits account for 42.7% share, reflecting their critical role in genomic mutation detection, companion diagnostics integration, and precision therapy stratification.

- Fastest-Growing Product Segment: Immunohistochemistry (IHC) test kits are witnessing strong momentum due to multiplex biomarker evaluation capabilities, cost-effectiveness, and widespread clinical reliance for tumor typing.

- Leading Application Segment: Breast cancer represents 50.5% of total demand, underpinned by established screening programs, mandatory biomarker assessment protocols, and high testing frequency.

- Fastest-Growing Application Segment: Lung cancer is advancing rapidly, fueled by increasing adoption of molecular profiling for EGFR, ALK, and PD-L1 testing within targeted treatment pathways.

| Key Insights | Details |

|---|---|

| Cancer Tissue Diagnostics Market Size (2026E) | US$ 8.6 Bn |

| Market Value Forecast (2033F) | US$ 14.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Rising Global Cancer Burden and Rapid Integration of Precision Oncology

The steady increase in global cancer incidence remains the most powerful catalyst accelerating demand for tissue-based diagnostic solutions. The rising prevalence of breast, lung, colorectal, prostate, and hematologic malignancies has intensified the need for early detection, accurate tumor classification, and biomarker-driven therapeutic planning. Modern oncology increasingly depends on histopathology, immunohistochemistry, in situ hybridization, and molecular profiling to guide targeted therapies and immuno-oncology regimens. Companion diagnostics linked to precision drugs are becoming mandatory components of treatment algorithms, significantly expanding testing volumes.

Advancements in next-generation sequencing (NGS), multiplex staining, and AI-assisted digital pathology are enhancing analytical sensitivity and reducing turnaround times, making tissue diagnostics more clinically actionable. Growing participation in oncology clinical trials further drives biomarker screening requirements across tertiary hospitals and reference laboratories. Additionally, structured cancer screening initiatives and national cancer control programs are increasing biopsy rates globally. As healthcare systems prioritize personalized treatment selection and evidence-based therapeutic stratification, tissue diagnostics have evolved from supportive tools into foundational elements of oncology decision-making, sustaining long-term market momentum.

Restraints - High Capital Investment, Reimbursement Gaps, and Technical Complexity

Despite strong demand fundamentals, several operational and economic barriers continue to moderate broader adoption. Advanced molecular platforms, automated staining systems, and digital pathology infrastructure require substantial capital expenditure, which can limit deployment in resource-constrained healthcare environments. Implementation also demands skilled pathologists, molecular biologists, and laboratory technicians, creating workforce dependency and training challenges. Reimbursement inconsistencies across regions further complicate market penetration. While biomarker testing is guideline-recommended in many developed economies, coverage for comprehensive genomic profiling remains variable, particularly in emerging markets.

Differences in regulatory approval pathways for companion diagnostics can delay commercialization timelines. Technical variability in pre-analytical processes including tissue fixation quality, sample preservation, and processing methods can influence test accuracy and reproducibility. Additionally, integration of genomic data into electronic medical systems requires robust digital infrastructure and cybersecurity safeguards. Limited access to standardized quality-control frameworks in smaller laboratories may affect consistency. Collectively, high costs, infrastructure requirements, and regulatory heterogeneity continue to temper adoption speed despite strong clinical necessity.

Opportunity - Digital Pathology Expansion, Biomarker Discovery, and Emerging Market Penetration

Significant expansion potential lies in the convergence of digital pathology, artificial intelligence, and advanced molecular analytics. AI-driven image interpretation tools are improving diagnostic precision, reducing inter-observer variability, and enabling remote consultation models that expand access to expert pathology services. Increasing discovery of predictive and prognostic biomarkers across solid and hematologic tumors is broadening the clinical scope of tissue-based assays. Emerging economies in Asia Pacific, Latin America, and parts of the Middle East are investing heavily in oncology infrastructure modernization, presenting untapped revenue pools for reagent manufacturers and platform providers. Localized production of consumables and strategic laboratory partnerships are improving affordability and distribution reach.

Integration of tissue diagnostics with liquid biopsy and multi-omics platforms represents another transformative avenue, enabling comprehensive tumor profiling from diagnosis through disease monitoring. Growing collaboration between pharmaceutical developers and diagnostic companies to co-develop companion tests further strengthens commercial prospects. As personalized oncology becomes increasingly standardized, technological innovation and geographic expansion collectively position tissue diagnostics for sustained structural growth.

Category-wise Analysis

By Product Insights

Molecular diagnostics test kits are projected to command a 42.7% revenue share in 2026, sustaining their top position within cancer tissue diagnostics. Their prominence is driven by increasing reliance on biomarker-driven oncology, including PCR- and NGS-based tissue profiling for actionable mutations. These assays enable accurate tumor characterization, therapy stratification, and monitoring of resistance pathways, making them indispensable in targeted treatment protocols. Compared with conventional staining techniques, molecular platforms deliver superior sensitivity and reproducibility across complex tumor types. Expanded use of companion diagnostics alongside targeted biologics further strengthens demand. Automation, closed-cartridge systems, and AI-assisted genomic interpretation tools are improving laboratory throughput while reducing variability. Growing integration of tissue genomics into routine pathology workflows across tertiary hospitals and reference laboratories ensures sustained utilization. As oncology transitions toward individualized treatment algorithms, molecular diagnostics remain the backbone of tissue-based cancer decision-making worldwide.

By Application Insights

The breast cancer segment is expected to remain the largest application area in 2026, capturing 50.5% of the global market. Growth is closely tied to the increasing prevalence of osteoarthritis, tendon injuries, ligament damage, and age-related degenerative joint conditions. PRP therapy has gained strong physician acceptance as a minimally invasive alternative to corticosteroids and surgical interventions, particularly for knee osteoarthritis and chronic tendon pathologies. Sports medicine programs increasingly incorporate PRP injections to accelerate tissue repair and reduce athlete recovery timelines, further strengthening procedural demand. Advancements in imaging-guided injection techniques have improved treatment accuracy and clinical confidence, encouraging wider adoption across orthopedic practices. Additionally, growing patient preference for regenerative therapies that utilize autologous biological material aligns with global healthcare trends favoring natural healing approaches. As healthcare systems emphasize outpatient musculoskeletal management and cost-effective pain reduction strategies, orthopedic applications continue to represent the most stable and procedure-driven revenue contributor.

By End-user Insights

Hospitals are anticipated to hold a 37.8% market share in 2026, reflecting their central role in multidisciplinary cancer management. Large hospital networks integrate pathology, surgical oncology, radiology, and molecular laboratories within unified clinical pathways, enabling efficient tissue processing and rapid diagnostic turnaround. High patient inflow across solid tumor indications supports continuous test utilization. Institutional settings also possess advanced automation platforms, digital pathology systems, and in-house molecular capabilities that support complex biomarker analysis. Clinical trial participation and translational oncology programs further increase testing demand within hospital-based laboratories. Stringent quality-control frameworks and accreditation standards enhance reliability, encouraging adoption of high-value assays. Moreover, reimbursement structures and centralized procurement contracts allow hospitals to deploy comprehensive diagnostic portfolios at scale. As precision oncology becomes embedded in routine care, hospitals remain the dominant environment for tissue-based cancer diagnostics globally.

Regional Insights

North America Cancer Tissue Diagnostics Market Trends

North America is forecast to retain a 46.7% value share in 2026, underpinned by mature oncology infrastructure and early adoption of advanced tissue-based technologies. The United States drives regional growth through high cancer screening penetration, strong biomarker testing mandates, and rapid integration of next-generation sequencing into standard oncology protocols. Regulatory support from the U.S. Food and Drug Administration has accelerated approval of companion diagnostics linked to targeted therapies, reinforcing clinical uptake.

The region benefits from well-established reference laboratory networks and digitized pathology ecosystems that enhance workflow efficiency and inter-laboratory collaboration. Academic cancer centers actively contribute to translational research, validating novel biomarkers and expanding testing indications. Additionally, reimbursement coverage for guideline-recommended molecular assays supports sustained test volumes. Continuous investment in AI-driven image analytics and genomic data platforms ensures North America maintains its position as the most technologically advanced and revenue-intensive market for cancer tissue diagnostics.

Europe Cancer Tissue Diagnostics Market Trends

Europe is expected to witness steady progress in 2026, supported by structured oncology pathways and harmonized regulatory standards across key markets such as Germany, France, Switzerland, and Italy. The region emphasizes validated diagnostic algorithms and quality-certified laboratory practices, ensuring consistent integration of histopathology and molecular profiling. National cancer screening initiatives contribute to stable biopsy volumes, particularly in breast and colorectal malignancies.

European laboratories demonstrate strong adoption of automated staining platforms and multiplex tissue assays to enhance analytical precision. Cost-containment policies encourage optimized reagent utilization and centralized laboratory consolidation, improving operational efficiency. Research institutions collaborate extensively on biomarker discovery and translational oncology programs, broadening the clinical scope of tissue diagnostics. Increasing digital pathology deployment across tertiary centers further strengthens diagnostic accuracy and workflow standardization, enabling Europe to sustain a high-value, quality-focused market position.

Asia Pacific Cancer Tissue Diagnostics Market Trends

Asia Pacific is projected to register a CAGR of approximately 7.4% between 2026 and 2033, positioning it as the fastest-growing regional market. Expanding healthcare infrastructure in China and India is significantly increasing access to histopathology and molecular oncology services. Rising cancer incidence, coupled with growing awareness of early detection, is stimulating biopsy-based diagnostic demand. Governments are investing in laboratory modernization initiatives and public oncology programs to strengthen diagnostic capacity at tertiary hospitals.

Local production of reagents and automation systems has improved affordability, facilitating broader laboratory adoption. In parallel, medical tourism hubs such as South Korea and Thailand are integrating advanced tissue testing to support comprehensive cancer care packages. Increasing participation in global clinical trials and precision oncology initiatives is further accelerating technological uptake, establishing Asia Pacific as the primary growth engine for future market expansion.

Competitive Landscape

The global cancer tissue diagnostics market is highly competitive, with strong participation from F. Hoffmann-La Roche Ltd., Danaher Corporation, Agilent Technologies, Inc., Thermo Fisher Scientific Inc., Abbott Laboratories, and Becton, Dickinson and Company (BD). These players leverage extensive oncology portfolios, global distribution networks, companion diagnostics expertise, and continuous innovation in immunohistochemistry (IHC), in situ hybridization (ISH), molecular assays, and digital pathology platforms to strengthen their market position. Rising cancer prevalence and the shift toward precision oncology are accelerating demand, prompting manufacturers to focus on automated staining systems, AI-enabled image analysis, workflow standardization, and expansion across emerging healthcare markets to ensure accurate, scalable, and reproducible diagnostic outcomes.

Key Industry Developments:

- In March 2026, diagnostics company Droplet Biosciences announced a collaboration with Nvidia to leverage the chipmaker’s AI-driven computing infrastructure to accelerate post-surgical cancer testing turnaround times. As part of the partnership, Droplet Biosciences is utilizing Nvidia Parabricks, a GPU-enabled genomic analysis platform, to significantly enhance the speed and efficiency of DNA sequencing data processing, enabling faster and more precise interpretation of tumor genomic profiles.

- In March 2026, Myriad Genetics, Inc. a prominent provider of molecular diagnostics and precision medicine solutions, announced the introduction of its Precise MRD™ assay. The company is initiating deployment of the test in collaboration with a selected group of oncology practices to support molecular residual disease monitoring in patients diagnosed with breast cancer.

- In February 2026, Illumina, Inc. reported significant customer advancements in oncology enabled by its spatial transcriptomics, 5-base sequencing, and proteomics platforms. By integrating multiple omics layers, researchers can achieve deeper biological characterization and enhanced molecular resolution. These capabilities are unified through Illumina Connected Multiomics, which streamlines multimodal data interpretation. The comprehensive technology portfolio is facilitating improved precision diagnostics, accelerating development of targeted therapies, and advancing understanding of complex tumor microenvironments.

- In November 2025, Abbott Laboratories and Exact Sciences announced a definitive agreement under which Abbott will acquire Exact Sciences to strengthen its presence in rapidly expanding cancer diagnostics categories and broaden patient access. According to the transaction terms, Exact Sciences shareholders will receive $105 per common share, valuing the company at approximately $21 billion in total equity.

Companies Covered in Cancer Tissue Diagnostics Market

- F. Hoffmann-La Roche Ltd.

- Danaher Corporation

- Agilent Technologies, Inc.

- Thermo Fisher Scientific Inc.

- Abbott Laboratories

- Becton, Dickinson and Company

- Merck KGaA

- QIAGEN N.V.

- Illumina, Inc.

- Bio-Rad Laboratories, Inc.

- Sakura Finetek Japan Co., Ltd.

- Quest Diagnostics Incorporated

- BioGenex Laboratories, Inc.

- Bio SB, Inc.

- Enzo Life Sciences, Inc.

- Others

Frequently Asked Questions

The global cancer tissue diagnostics market is projected to be valued at US$ 8.6 Bn in 2026.

The market is driven by the rapidly rising global incidence of cancer, advancements in diagnostic technologies (IHC, ISH, molecular profiling, AI/digital pathology), and increasing adoption of precision medicine and early detection programs.

The global cancer tissue diagnostics market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Key opportunities include expansion of digital pathology and AI-integrated diagnostics, growing adoption in emerging markets, and development of novel biomarkers and point-of-care tissue tests for personalized oncology.

F. Hoffmann-La Roche Ltd., Danaher Corporation, Agilent Technologies, Inc., Thermo Fisher Scientific Inc., Abbott Laboratories, and Becton, Dickinson and Company (BD) are some of the key players in the cancer tissue diagnostics market.