- Biotechnology

- Esophageal Cancer Diagnostics Market

Esophageal Cancer Diagnostics Market Size, Share, and Growth Forecast, 2026 - 2033

Esophageal Cancer Diagnostics Market by Diagnostic Type (Endoscopic Procedures, Biopsy, Imaging Tests, Others), Technology (Immunohistochemistry, Others) Application (Hospitals, Diagnostic Centers, Research Institutes), and Regional Analysis for 2026 - 2033

Esophageal Cancer Diagnostics Market Size and Trends Analysis

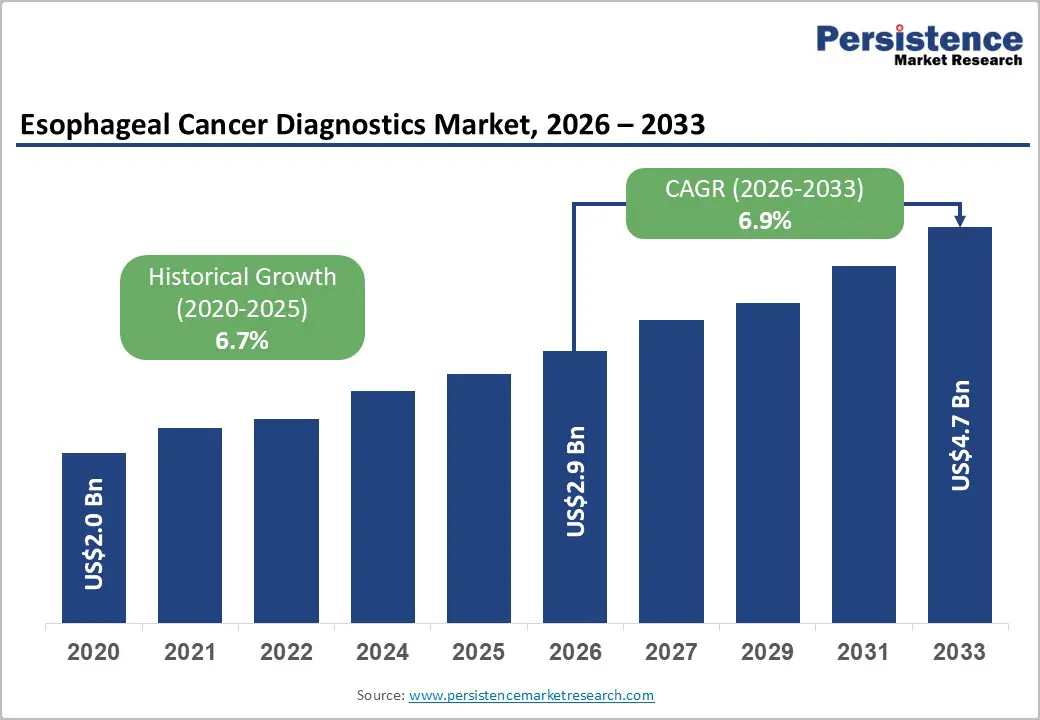

The global esophageal cancer diagnostics market size is likely to be valued at US$2.9 billion in 2026 and is expected to reach US$4.7 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the increasing incidence of esophageal cancer worldwide, particularly in regions with aging populations and lifestyle-related risk factors such as smoking, alcohol consumption, and gastroesophageal reflux disease.

Technological advancements in diagnostic modalities, including endoscopic procedures, imaging techniques, molecular profiling, and liquid biopsy, are enhancing the precision and efficiency of esophageal cancer detection. According to the World Cancer Research Fund (based on WHO/IARC data 2022), esophageal cancer ranks among the top common cancers globally, being the 11th most common cancer worldwide. Healthcare systems are increasingly prioritizing minimally invasive and patient-friendly diagnostics, which allow for better staging, treatment planning, and monitoring of disease progression.

Key Industry Highlights:

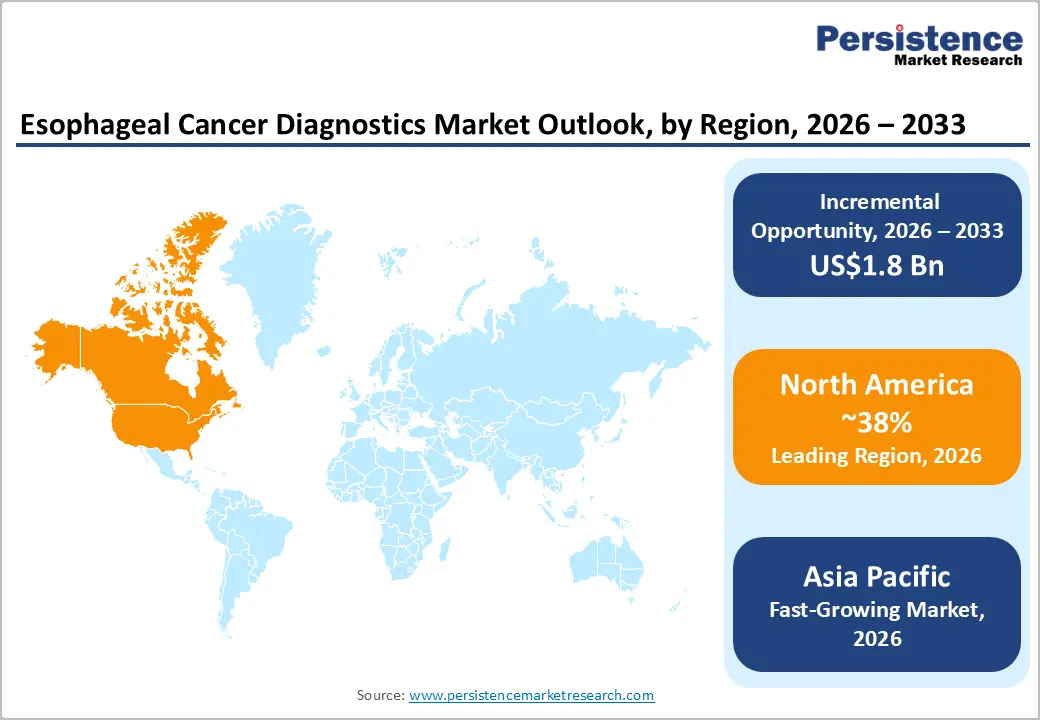

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by advanced healthcare infrastructure, high adoption of innovative technologies, and strong emphasis on precision medicine.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by large patient populations, expanding diagnostic infrastructure, and rising healthcare access in key countries.

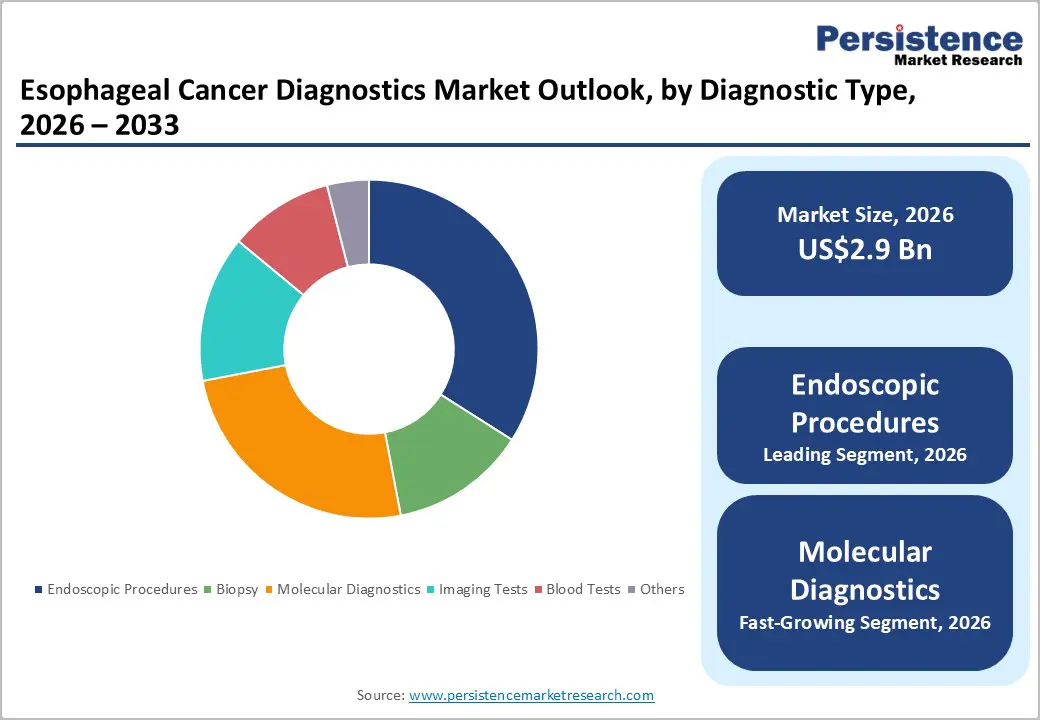

- Leading Diagnostic Type: Endoscopic procedures are projected to represent the leading diagnostic type in 2026, accounting for 45% of the revenue share, driven by their ability to provide direct visualization, enable immediate biopsy sampling, and serve as the cornerstone of esophageal cancer evaluation in clinical practice.

- Leading Technology Type: Immunohistochemistry (IHC) is anticipated to be the leading technology type, accounting for over 42% of the revenue share in 2026, supported by its widespread use in protein biomarker detection and routine pathological assessment.

| Key Insights | Details |

|---|---|

| Esophageal Cancer Diagnostics Market Size (2026E) | US$2.9 Bn |

| Market Value Forecast (2033F) | US$4.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

DRO Analysis

Driver - Rising Incidence of Esophageal Cancer and Early-Detection Emphasis

The rise in esophageal cancer cases, particularly among aging populations and regions with lifestyle-related risk factors, is driving demand for effective diagnostic solutions. Early detection significantly improves patient outcomes, encouraging healthcare providers to adopt advanced diagnostic technologies. Clinicians increasingly rely on endoscopic procedures, imaging modalities, and molecular testing to identify disease at treatable stages. Preventive screening programs, especially in high-risk populations, reinforce the necessity for reliable diagnostics.

Expansion of awareness campaigns and national screening initiatives reinforces early detection strategies, prompting hospitals and diagnostic centers to invest in comprehensive diagnostic infrastructures. The integration of multi-modal diagnostic approaches, including liquid biopsy, molecular profiling, and AI-assisted imaging, facilitates precise and timely detection. Clinical guidelines are increasingly emphasizing the importance of routine surveillance in high-risk patients, such as those with Barrett’s esophagus or chronic gastroesophageal reflux disease (GERD).

Expansion of Molecular Diagnostics and Personalized-Medicine Adoption

The integration of molecular diagnostics into esophageal cancer care is transforming detection and treatment pathways. Genetic and biomarker-based testing enables precise disease stratification, guides targeted therapies, and supports personalized medicine initiatives. Next-generation sequencing, immunohistochemistry, and PCR-based tests allow clinicians to identify mutations and molecular alterations critical for individualized treatment plans. Healthcare systems increasingly adopt these technologies to optimize therapeutic outcomes and reduce unnecessary interventions.

Advancements in molecular diagnostics also support the evolution of companion diagnostics, aligning therapeutic selection with individual genetic profiles. The trend toward precision medicine encourages investment in laboratory infrastructure, training, and regulatory compliance to facilitate routine clinical integration. Increasing adoption of genomic testing in hospitals and specialty clinics provides clinicians with actionable insights, enhancing early detection, prognosis, and treatment efficacy.

Restraint - Structural Challenges in Early Detection Infrastructure

Despite growing demand, structural limitations in early detection infrastructure restrict widespread adoption of advanced diagnostics. Many regions lack sufficient endoscopic equipment, molecular laboratories, and standardized screening programs, limiting patient access to timely evaluation. High initial investment costs for sophisticated diagnostic platforms and training requirements impede healthcare facilities from scaling these services.

Disparities in technological deployment across regions result in uneven availability of cutting-edge diagnostics. Limited access to specialized personnel, such as trained endoscopists and molecular pathologists, compounds these structural challenges. Supply chain inefficiencies for reagents, devices, and maintenance services restrict diagnostic throughput. Regulatory and procedural complexities in implementing new technologies can delay adoption, reducing the ability to capitalize on emerging diagnostic innovations.

Limited Diagnostic Infrastructure and Skilled Workforce in Emerging Economies

Emerging economies face persistent limitations in diagnostic infrastructure and trained personnel, which hinder market penetration for advanced esophageal cancer diagnostics. Hospitals and diagnostic centers in these regions often lack endoscopic equipment, imaging systems, and molecular testing facilities. Skilled specialists, including gastroenterologists, pathologists, and lab technicians, are in short supply, reducing the capacity to conduct timely and accurate testing. Limited awareness and resource constraints exacerbate access issues, particularly in rural areas.

The shortage of trained personnel also affects quality and consistency in test interpretation, impacting clinical decision-making and patient outcomes. Emerging markets require investment in educational programs, professional training, and certification initiatives to build local expertise. Infrastructure gaps ranging from laboratory automation to maintenance of advanced devices pose operational challenges. Without strategic interventions to strengthen workforce capabilities and diagnostic capacity, these regions struggle to match standards in esophageal cancer detection.

Opportunity - Liquid-Biopsy-Centric and AI-Integrated Diagnostic Platforms

Liquid biopsy and AI-integrated diagnostic platforms represent a major growth opportunity in esophageal cancer diagnostics. Non-invasive blood-based testing enables early detection, disease monitoring, and recurrence surveillance without relying solely on invasive procedures. AI algorithms enhance image analysis in endoscopy and radiology, improving lesion detection accuracy and reducing interpretation time. Integration of AI with molecular and imaging data supports predictive modeling, risk stratification, and personalized treatment planning.

Collaboration between technology providers, biotech firms, and healthcare institutions fosters the rapid adoption of AI and liquid biopsy solutions. The platforms enable real-time data analytics and predictive insights, facilitating precision medicine approaches. Early pilot programs and clinical studies demonstrate improved detection sensitivity, workflow efficiency, and patient convenience, which enhances market confidence.

Rapid Expansion of Molecular Diagnostics

The growing adoption of molecular diagnostics offers significant opportunities in esophageal cancer detection and management. Techniques such as next-generation sequencing, PCR, and immunohistochemistry provide detailed molecular profiles that guide targeted therapies and clinical decision-making. Expansion of laboratory infrastructure, declining sequencing costs, and increasing availability of high-throughput platforms accelerate routine integration of molecular testing into clinical workflows.

Hospitals and diagnostic centers are investing in molecular diagnostics to improve early detection, staging accuracy, and treatment personalization. Partnerships between diagnostic companies, research institutions, and healthcare providers facilitate the rapid deployment and adoption of molecular platforms. Training programs and clinical education initiatives support effective utilization of these technologies. Molecular diagnostics also enable companion diagnostic development, providing actionable insights for emerging targeted therapies.

Category-wise Analysis

Diagnostic Type Insights

Endoscopic procedures are expected to lead the esophageal cancer diagnostics market, accounting for approximately 45% of revenue in 2026, driven by their central role in clinical evaluation and ability to provide direct visualization of the esophageal lining along with immediate biopsy sampling. For example, upper gastrointestinal endoscopy is routinely used in tertiary care hospitals to detect early-stage lesions, demonstrating its practical importance in improving diagnostic timelines and enabling timely therapeutic interventions in esophageal cancer management.

Molecular diagnostics are likely to represent the fastest-growing segment, supported by the increasing need for biomarker-based profiling and precision oncology approaches. This segment benefits from advancements in genomic technologies that allow clinicians to identify genetic mutations and molecular alterations associated with disease progression. For example, next-generation sequencing-based panels are increasingly used to identify actionable mutations in esophageal tumors, enabling tailored treatment decisions.

Technology Type Insights

Immunohistochemistry (IHC) is projected to lead the market, capturing around 42% of the revenue share in 2026, supported by its widespread use in routine pathological assessment and biomarker detection. It plays a critical role in identifying protein expression patterns such as HER2 and PD-L1, which are essential for guiding therapeutic decisions in esophageal cancer. For example, PD-L1 testing through IHC is routinely performed to determine patient eligibility for immunotherapy, highlighting its clinical significance and reinforcing its leadership in the technology landscape of esophageal cancer diagnostics.

Next-generation sequencing (NGS) is likely to be the fastest-growing technology type, driven by its ability to provide comprehensive genomic profiling and detect multiple genetic alterations simultaneously. This capability supports the growing emphasis on precision medicine and personalized oncology, where treatment decisions are increasingly based on molecular characteristics. For example, multi-gene panel testing using NGS is increasingly applied to identify mutations linked to esophageal cancer progression, enabling clinicians to design more effective and individualized treatment strategies, thereby driving rapid growth in this segment.

Regional Insights

North America Esophageal Cancer Diagnostics Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by advanced healthcare infrastructure and strong clinical research ecosystems. The region is witnessing increasing integration of artificial intelligence in endoscopic procedures, enhancing early lesion detection and diagnostic accuracy. Molecular diagnostics and liquid biopsy are gaining traction, enabling non-invasive testing and personalized treatment planning. Strong reimbursement policies and regulatory support encourage rapid adoption of novel diagnostic solutions.

Healthcare providers are increasingly adopting multi-modal diagnostic approaches that combine imaging, molecular profiling, and pathology to improve patient outcomes. Investments in digital pathology and automation are enhancing efficiency and reducing turnaround times. For example, Thermo Fisher Scientific supports molecular testing and genomic profiling solutions, enabling clinicians to make data-driven decisions.

Europe Esophageal Cancer Diagnostics Market Trends

Europe is likely to be a significant market for esophageal cancer diagnostics, due to structured screening programs and widespread adoption of standardized clinical guidelines. Countries across the region emphasize early detection through organized healthcare systems, ensuring consistent use of endoscopic and imaging technologies. Increasing demand for minimally invasive diagnostics and molecular testing is driving innovation, while government support and funding initiatives promote research and development. The region also benefits from strong collaboration between public health institutions and private companies, facilitating the adoption of advanced diagnostic solutions and improving access to care across diverse populations.

Laboratories are increasingly adopting next-generation sequencing and immunohistochemistry to guide targeted therapies. Digital health technologies, including AI-based imaging tools, are enhancing diagnostic accuracy and workflow efficiency. For example, Siemens Healthineers plays a significant role in advancing imaging and diagnostic platforms across Europe, supporting early-stage detection and disease monitoring. These developments highlight Europe’s focus on combining innovation with standardized care delivery to improve patient outcomes.

Asia Pacific Esophageal Cancer Diagnostics Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by a high disease burden and expanding healthcare infrastructure. The adoption of endoscopic procedures remains strong, while demand for molecular diagnostics and minimally invasive technologies is rising. Rapid urbanization, lifestyle changes, and improved healthcare access are contributing to increased diagnostic volumes, positioning the region as a key growth hub for diagnostic technologies.

Asia Pacific is witnessing significant investments in healthcare infrastructure and local manufacturing capabilities, which enhance accessibility and affordability of diagnostic solutions. The presence of regional players fosters competitive innovation and technology adoption. Public-private partnerships are accelerating the deployment of advanced diagnostic tools in both urban and rural areas. For example, Fujifilm Holdings Corporation is actively advancing endoscopic and imaging technologies across the region, supporting early detection initiatives.

Competitive Landscape

The global esophageal cancer diagnostics market exhibits a moderately fragmented structure, driven by the presence of established multinational corporations alongside emerging biotech and specialized diagnostic firms. The market is characterized by continuous technological innovation, particularly in imaging, endoscopy, and molecular diagnostics, which together dominate diagnostic practices.

With key leaders including Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Olympus Corporation, and Thermo Fisher Scientific, the competitive landscape reflects a mix of device manufacturers, molecular diagnostics providers, and laboratory service companies. These players compete through continuous R&D investments, product innovation, and expansion of advanced diagnostic portfolios such as next-generation sequencing and AI-integrated platforms.

Key Industry Developments:

- In July 2025, UCLPartners announced the launch of a new “sponge-on-a-string” esophageal cancer test pilot across London, enabling early detection through a quick, minimally invasive method conducted in community pharmacies and diagnostic settings.

- In March 2025, Lucid Diagnostics announced that updated National Comprehensive Cancer Network (NCCN) clinical guidelines now include esophageal precancer screening, recognizing non-endoscopic biomarker tests such as EsoGuard® as an acceptable alternative to traditional endoscopy, supporting broader adoption of minimally invasive diagnostic approaches.

- In December 2025, Lucid Diagnostics announced positive data from the largest real-world study of esophageal precancer detection, demonstrating strong performance, safety, and rapid sample collection using its EsoGuard® DNA test and EsoCheck® device across nearly 12,000 patients, supporting its effectiveness as a non-invasive screening tool.

Companies Covered in Esophageal Cancer Diagnostics Market

- Abbott Laboratories

- Olympus Corporation

- Fujifilm Holdings Corporation

- Boston Scientific Corporation

- Medtronic plc

- Cook Medical

- Siemens Healthineers

- GE Healthcare

- Roche Diagnostics

- Koninklijke Philips N.V.

- Pentax Medical (HOYA Corporation)

- Bio-Rad Laboratories

- Quest Diagnostics

- Exact Sciences Corporation

- Bruker Corporation

- Laboratory Corporation of America Holdings (LabCorp)

- Shimadzu Corporation

Frequently Asked Questions

The global esophageal cancer diagnostics market is projected to reach US$2.9 billion in 2026.

The rising incidence of esophageal cancer and increasing demand for early, accurate, and minimally invasive diagnostic solutions drive the market.

The esophageal cancer diagnostics market is expected to grow at a CAGR of 6.9% from 2026 to 2033.

Growth opportunities lie in the adoption of liquid biopsy, AI-integrated diagnostics, and the expansion of molecular and non-invasive screening technologies.

Abbott Laboratories, Olympus Corporation, Fujifilm Holdings Corporation, Boston Scientific Corporation, and Medtronic plc are the leading players.