- Healthcare Services

- China Lung Cancer Screening Market

China Lung Cancer Screening Market Size, Share, and Growth Forecast 2026 - 2033

China Lung Cancer Screening Market by Screening Type (Population-Based Screening, Opportunistic Screening, Follow-up Surveillance Screening), by Technology (Low-Dose Computed Tomography, Chest X-ray, Artificial Intelligence in Medical Imaging, Liquid Biopsy and Biomarker-Based Screening, PET-CT), Cancer Type (Non-Small Cell Lung Cancer, Small Cell Lung Cancer), End-user (Hospitals, Diagnostic Imaging Centers, Cancer Specialty Centers, Mobile Screening Units, Others), 2026-2033

China Lung Cancer Screening Market Size and Trend Analysis

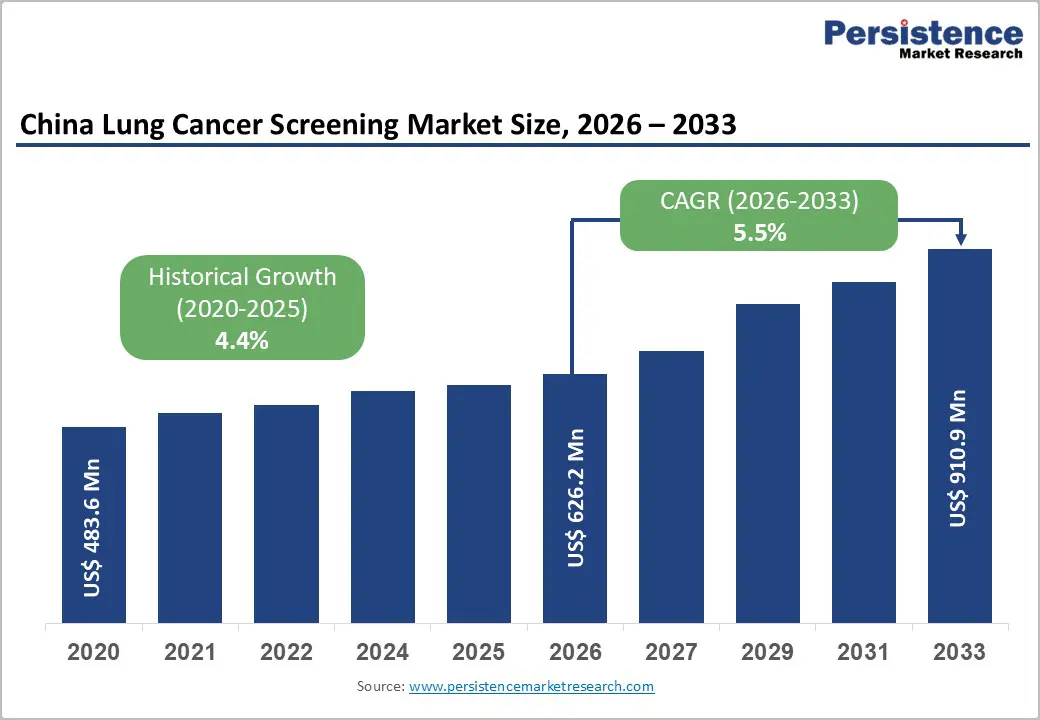

The China lung cancer screening market size is expected to be valued at US$ 626.2 million in 2026 and projected to reach US$ 910.9 million by 2033, growing at a CAGR of 5.5% between 2026 and 2033. China's lung cancer screening market is growing steadily, driven by the country's position as the world's highest-burden lung cancer nation and expanding government-funded population screening initiatives under the Healthy China 2030 plan.

According to the National Cancer Center of China, lung cancer is the most common and fatal malignancy in China, with approximately 820,000 new cases and 714,000 deaths recorded in 2022, accounting for nearly 20% of all cancer deaths nationally. The rapid scale-up of Low-Dose Computed Tomography (LDCT) screening programs, integration of AI-based image analysis to address radiologist capacity constraints, and expanding liquid biopsy-based biomarker screening adoption in China's premium private hospital sector are collectively sustaining above-average value growth through 2033.

Key Industry Highlights:

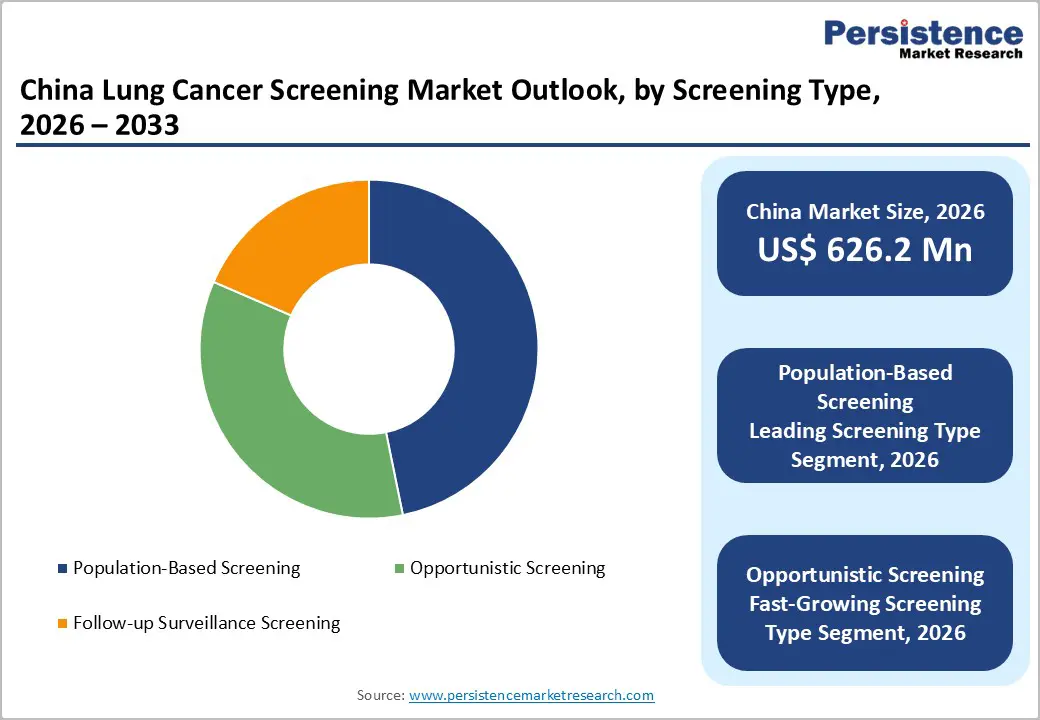

- Leading Screening Type – Population-Based Screening: Population-Based Screening leads the China lung cancer screening market with approximately 46.8% share in 2026, supported by national and provincial early cancer detection initiatives that use organized low-dose CT (LDCT) programs to screen high-risk populations, particularly long-term smokers and individuals with occupational exposure.

- Fastest Growing Screening Type – Follow-up Surveillance Screening: Follow-up Surveillance Screening is the fastest-growing screening type, driven by increasing detection of indeterminate pulmonary nodules and the need for structured repeat imaging and monitoring protocols in hospitals and specialty cancer centers.

- Dominant Technology – Low-Dose Computed Tomography (LDCT): Low-Dose Computed Tomography holds the largest technology share at approximately 63.9% in 2026, owing to its superior sensitivity for detecting early-stage lung nodules and its widespread inclusion in China's public health screening programs.

- Fastest Growing Technology – Artificial Intelligence in Medical Imaging: Artificial Intelligence in Medical Imaging is the fastest-growing technology segment, as platforms developed by Chinese companies such as Beijing Infervision Technology and Huiying Medical Technology improve nodule detection efficiency and help address radiologist shortages across lower-tier cities.

- Key Opportunity - Liquid Biopsy for Non-Smoking Lung Cancer Detection: Liquid biopsy ctDNA screening for non-smoking lung cancer validated in Chinese populations by Burning Rock Biotech and Genetron Health represents the core premium market opportunity, targeting China's growing non-smoking NSCLC population in private hospitals and health check-up channels.

Market Dynamics

Drivers - Healthy China 2030 National Cancer Screening Policy Mandating LDCT Scale-up

China's Healthy China 2030 Plan and the National Cancer Prevention and Control Action Plan (2019-2023) identify lung cancer early detection as a national health priority, with the National Health Commission of China (NHC) actively expanding government-funded lung cancer screening programs across high-risk population cohorts. The Chinese Guidelines for Lung Cancer Screening and Early Detection (2021 Edition) formally recommend LDCT as the standard screening modality for high-risk individuals aged 50-74 with a smoking history directly generating structured, policy-driven demand for LDCT equipment procurement and related consumables.

The National Cancer Center's lung cancer early detection program has deployed screening services across multiple provinces, with Shanghai, Beijing, Guangzhou, and Shenzhen establishing model LDCT screening programs integrated into routine health check-up packages. This policy infrastructure creates non-discretionary institutional purchasing of screening technology from companies including GE HealthCare and Shanghai United Imaging Healthcare.

China's Massive High-Risk Population and World-Leading Lung Cancer Burden

China's extraordinarily high lung cancer burden creates the world's largest addressable screening population providing an unparalleled structural demand foundation for the screening market. The National Cancer Center of China reported approximately 820,000 new lung cancer cases in 2022, representing the highest lung cancer incidence globally. China has approximately 316 million current smokers according to WHO data the world's largest smoking population, creating a vast primary high-risk screening cohort. Additionally, non-smoking-related lung cancer driven by air pollution, occupational exposures, and genetic predisposition is increasingly recognized in Chinese epidemiology, particularly among non-smoking women in South China and Northeast China industrial corridors. The Chinese Society of Clinical Oncology (CSCO) guidelines actively promote annual LDCT screening in this expanded high-risk population, driving growing institutional demand for screening capacity across public and private hospital systems.

Restraints - Radiologist and CT Technician Shortage Limiting LDCT Screening Throughput Capacity

China faces a significant shortage of trained radiologists capable of interpreting LDCT lung nodule findings at the volume scale required by national screening programs. The Chinese Medical Doctor Association has highlighted that China's radiologist-to-population ratio remains significantly below WHO-recommended levels, with qualified thoracic radiologists particularly scarce in Tier-3 and Tier-4 cities and rural areas where screening program expansion is most needed. This constraint creates diagnostic quality inconsistency, increases nodule misclassification rates, and limits the scalable deployment of LDCT screening programs in lower-tier healthcare settings, suppressing market volume growth potential in geographies with large eligible screening populations.

High False-Positive Rate in LDCT Generating Patient Anxiety and System Costs

LDCT lung cancer screening generates substantial false-positive nodule findings that create patient psychological burden and high downstream diagnostic costs. Clinical data from China's national programs, aligned with international evidence including the U.S. National Lung Screening Trial (NLST), demonstrate that LDCT yields approximately 20-30% positive scan rates in initial screening rounds, with the vast majority representing benign nodules requiring resource-intensive follow-up imaging. These false-positive rates and the associated cascade of follow-up CT scans, biopsies, and specialist consultations increase total healthcare system cost per true cancer detected, creating payer resistance in China's cost-sensitive public hospital reimbursement environment and limiting program scale-up velocity.

Opportunities - AI-Powered Medical Imaging in LDCT Interpretation: Addressing Radiologist Capacity Constraints

Artificial intelligence (AI)-powered medical imaging analysis represents the most transformative technological growth opportunity in China's lung cancer screening market, directly addressing the critical radiologist shortage that constrains LDCT program scalability. Beijing Infervision Technology's InferRead CT Lung and Huiying Medical Technology's deep learning LDCT analysis platform have received NMPA (National Medical Products Administration) clearance and are actively deployed across Chinese hospital networks, demonstrating AI-assisted nodule detection sensitivity exceeding 95% in published clinical validations.

A landmark study published in Nature Medicine demonstrated that AI systems achieved radiologist-equivalent LDCT interpretation performance, validating AI as a qualified screening tool. As China's NHC integrates AI-assisted reading into national lung cancer screening guidelines, demand for validated AI imaging solutions will grow structurally, creating a high-margin software-as-a-medical-device revenue stream alongside hardware procurement for companies including Siemens Healthineers and GE HealthCare.

Liquid Biopsy and Biomarker-Based Screening for Non-Smoking Lung Cancer Detection

Liquid biopsy and biomarker-based lung cancer screening represent a high-growth adjacent opportunity within China's lung cancer screening market, particularly for the significant population of non-smoking lung cancer patients poorly served by LDCT-only screening pathways. Chinese companies including Burning Rock Biotech Limited, Genetron Health, and Berry Genomics are developing and commercializing circulating tumor DNA (ctDNA) and cell-free DNA methylation-based lung cancer early detection assays validated in Chinese patient populations.

A multi-center study published in Cell Research demonstrated that ctDNA-based liquid biopsy achieved high sensitivity for Stage I-II lung cancer detection in Chinese patient cohorts. The NMPA's progressive regulatory framework for IVD biomarker cancer screening tests combined with growing premium private hospital adoption of multi-cancer early detection (MCED) panels creates a compelling commercial expansion opportunity through 2033 for Chinese liquid biopsy innovators operating in adjacent oncology diagnostics markets.

Category-wise Analysis

Screening Type Insights

The population-based screening segment leads by screening type, commanding approximately 47% share in 2026. Population-based screening characterized by organized, government-funded programs targeting defined high-risk cohorts across defined geographic populations dominates due to China's strong policy infrastructure under Healthy China 2030 and the National Cancer Center's lung cancer screening expansion programs.

Government-organized programs in municipalities including Shanghai, Beijing, and Tianjin have established systematic LDCT screening registries for high-risk populations aged 50-74 with 20+ pack-year smoking histories, generating high-volume, institutionally procured screening demand. Opportunistic Screening conducted in the context of individual clinical encounters or health check-up packages is the fastest-growing screening type, driven by China's rapidly expanding private health examination center sector offering premium multi-cancer screening packages.

Technology Insights

The low-dose computed tomography (LDCT) technology segment leads the China Lung Cancer Screening market, accounting for approximately 58% of total technology market share in 2026. LDCT's leadership is firmly anchored by its status as the only technology with Level I evidence for lung cancer mortality reduction demonstrated by the U.S. National Lung Screening Trial (NLST) showing a 20% relative reduction in lung cancer mortality and formal recommendation in China's 2021 Lung Cancer Screening Guidelines. The NHC has specified LDCT as the mandated technology for all government-funded lung cancer screening programs, directly driving procurement from leading CT manufacturers including GE HealthCare, Siemens Healthineers, Shanghai United Imaging Healthcare, and Shenzhen Mindray Bio-Medical Electronics. AI in Medical Imaging is the fastest-growing technology, driven by NMPA-cleared deep learning platforms from domestic innovators addressing China's radiologist shortage.

Cancer Type Insights

The non-small cell lung cancer (NSCLC) segment leads the China lung cancer screening market by cancer type, commanding approximately 85% share in 2026. NSCLC comprising adenocarcinoma, squamous cell carcinoma, and large cell carcinoma, represents approximately 85% of all lung cancer cases in China according to the National Cancer Center, making it the primary target of both LDCT and liquid biopsy screening programs. The significantly better prognosis of NSCLC when detected at Stage I-II (5-year survival rate >70% for Stage I per CSCO guidelines) versus advanced-stage diagnosis provides strong clinical and health economic rationale for population screening programs. Adenocarcinoma in particular increasingly prevalent among Chinese non-smoking women is a key NSCLC subtype driving specific early detection innovations, including low-attenuation nodule management protocols and ctDNA biomarker validation studies in Chinese clinical research programs.

End-user Insights

Hospitals represent the leading end-user segment in China's Lung Cancer Screening market, commanding approximately 52% of total revenue in 2026. Tier-1 and Tier-2 public hospitals, including Grade III-designated hospitals under China's hospital grading system, drive this dominance through their role as the primary sites for government-funded lung cancer screening programs, clinical trial recruitment for novel screening modalities, and complex pulmonary nodule management after LDCT-positive screening results. Cancer Specialty Centers, including national cancer center networks affiliated with the Chinese Academy of Medical Sciences (CAMS) are growing rapidly as dedicated lung cancer screening service providers. Diagnostic Imaging Centers and Mobile Screening Units are the fastest-growing end-user segments, with mobile LDCT screening buses deployed by municipal health bureaus in Guangdong, Jiangsu, and Sichuan provinces extending screening access to communities without fixed hospital infrastructure.

China Lung Cancer Screening Market – Province-Level Insights

Anhui Lung Cancer Screening Market Trends and Insights

Anhui accounts for an estimated 3.7% of the China lung cancer screening market in 2026, supported by expanding tertiary care infrastructure in Hefei, Wuhu, and Bengbu and growing participation in government-funded low-dose computed tomography (LDCT) screening initiatives. The province is strengthening oncology and radiology capabilities through healthcare modernization programs, while broader adoption of artificial intelligence-assisted pulmonary nodule detection is improving diagnostic efficiency and enabling earlier identification of high-risk patients across urban and semi-rural population.

Guizhou Lung Cancer Screening Market Trends and Insights

Guizhou represents approximately 2.4% of the national market and is among the fastest-growing provincial markets due to increasing central government investment in healthcare infrastructure and cancer prevention services. Mobile LDCT screening units, tele-radiology networks, and cloud-based AI interpretation platforms are helping address radiologist shortages and expanding access to early lung cancer detection in mountainous and underserved counties, particularly among smoking and environmentally exposed population.

Guangdong Lung Cancer Screening Market Trends and Insights

Guangdong holds roughly 9.1% in 2026, making it one of the country's largest and most technologically advanced provincial markets. Extensive tertiary hospital networks, strong private healthcare spending, and a substantially high-risk population are driving widespread adoption of LDCT, AI-assisted imaging, and premium liquid biopsy-based screening. Major cities, including Guangzhou and Shenzhen, are leading the commercialization of integrated preventive oncology and executive health screening programs.

Competitive Landscape

The China lung cancer screening market is moderately consolidated in LDCT hardware, dominated by GE HealthCare, Siemens Healthineers, Shanghai United Imaging Healthcare, and Shenzhen Mindray Bio-Medical Electronics, but increasingly competitive and fragmented in the high-growth AI imaging and liquid biopsy software segments.

Domestic Chinese companies, including Beijing Infervision Technology, Huiying Medical Technology, Burning Rock Biotech, and Genetron Health are rapidly gaining share through NMPA-cleared, China-specific validated products. Key competitive differentiators include NMPA regulatory clearance, AI algorithm clinical validation, government program procurement relationships, price competitiveness for public hospital tenders, and clinical evidence breadth. Strategic priorities include AI software commercialization, ctDNA biomarker panel development, and mobile screening unit program expansion.

Key Developments:

- In February 2026, Chinese researchers announced the development of a new diagnostic kit for the early detection of lung cancer, designed to identify disease-associated biomarkers at an earlier stage and improve screening accuracy among high-risk populations.

- In October 2025, Caretia, a technology startup based at Hong Kong Science Park, announced that its AI-powered lung cancer screening platform had reached key development milestones and advanced into the next phase, supporting the Hong Kong government's 2025 policy initiative to expand AI-assisted lung cancer screening and strengthen cancer prevention and early diagnosis.

- In April 2025, researchers at the Guangzhou Institute of Respiratory Disease in China found that lung cancer screening detected diseases in non-smokers at comparable rates as their smoking peers. Low-dose CT was found to be the most effective screening tool for those at the risk of lung cancer.

China Lung Cancer Screening Market – Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 483.6 Mn |

| Current Market Value (2026) | US$ 626.2 Mn |

| Projected Market Value (2033) | US$ 910.9 Mn |

| CAGR (2026-2033) | 5.5% |

| Dominant Technology | Low-Dose Computed Tomography, 63.9% share |

| Top-ranking Screening Type | Population-Based Screening. 46.8% |

| Incremental Opportunity | US$ 18.6 Mn |

Companies Covered in China Lung Cancer Screening Market

- Biodesix

- GE HealthCare

- DELFI Diagnostics

- Shenzhen Mindray Bio-Medical Electronics

- CANON MEDICAL SYSTEMS CORPORATION

- Siemens Healthineers

- Medtronic

- Koninklijke Philips

- Freenome Holdings

- Shanghai United Imaging Healthcare

- Burning Rock Biotech Limited

- Genetron Health

- Berry Genomics

- Huiying Medical Technology

- Beijing Infervision Technology

- Others

Frequently Asked Questions

The China Lung Cancer Screening market is projected to reach US$ 626.2 million in 2026, having grown at a historical CAGR of 4.4% during 2020-2025. The market is forecast to expand to US$ 910.9 million by 2033, driven by the Healthy China 2030-mandated LDCT program expansion, NMPA-cleared AI imaging platform commercialization, and liquid biopsy adoption in China's premium private hospital segment serving 820,000 annual new lung cancer cases.

Rising lung cancer incidence, expanding government-funded low-dose CT screening programs under Healthy China 2030, and increasing adoption of AI-assisted imaging are the primary demand drivers in the China lung cancer screening market.

The China lung cancer screening market is poised to witness a CAGR of 5.5% from 2026 to 2033.

The key growth opportunity lies in liquid biopsy and biomarker-based screening for early detection of lung cancer, particularly among China's growing non-smoking and high-risk population.

Leading companies include GE HealthCare, Siemens Healthineers, Shanghai United Imaging Healthcare, Shenzhen Mindray Bio-Medical Electronics, Beijing Infervision Technology, Huiying Medical Technology, Burning Rock Biotech Limited, Genetron Health, Berry Genomics, CANON MEDICAL SYSTEMS CORPORATION, Koninklijke Philips, Neusoft Medical Systems, Biodesix, and DELFI Diagnostics, among others. These players compete through NMPA regulatory clearance portfolios, AI algorithm clinical validation in Chinese patient populations, LDCT equipment cost competitiveness for public hospital procurement, and liquid biopsy assay sensitivity for early-stage NSCLC detection.