- Biotechnology

- Cancer Molecular Biomarkers Market

Cancer Molecular Biomarkers Market Size, Share and Growth Forecast, 2026-2033

Cancer Molecular Biomarkers Market by Biomarker Type (Genetic, Transcriptomic, Proteomic, Epigenetic, Metabolic, Cell-based, Exosome-derived), Profiling Technology (Next-Generation Sequencing (NGS), Omics, Spectrometry, Bioinformatics Analytics, Others), Cancer Type (Breast Cancer, Lung Cancer, Cervical Cancer, Ovarian Cancer, Others), End-Use (Clinical Diagnostics, Therapeutic Monitoring, Clinical Research, Biopharmaceutical Companies, Others), and Regional Analysis for 2026-2033

Cancer Molecular Biomarkers Market Share and Trends Analysis

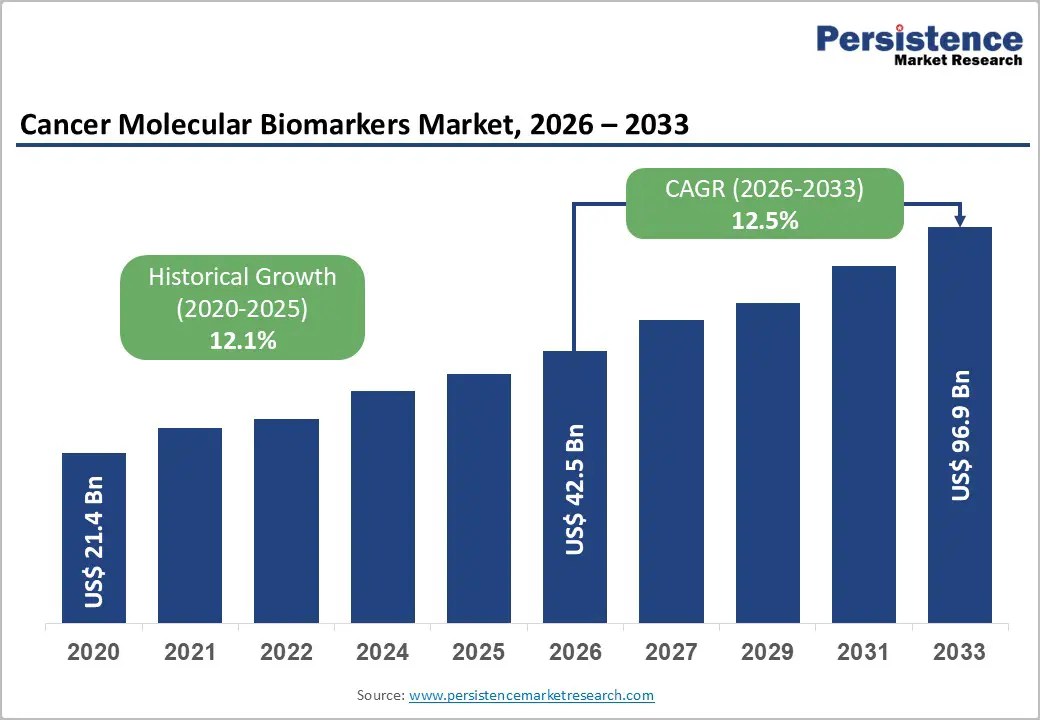

The global cancer molecular biomarkers market size is likely to be valued at US$ 42.5 billion in 2026, and is projected to reach US$ 96.9 billion by 2033, growing at a CAGR of 12.5% during the forecast period 2026?2033. This expansion is reflecting the increasing global burden of cancer and the rising clinical shift toward precision oncology. Healthcare systems are adopting biomarker driven decision making to improve treatment selection and patient outcomes.

Providers are integrating advanced diagnostic platforms such as next-generation sequencing (NGS) and polymerase chain reaction (PCR)-based assays into routine workflows. As oncology pipelines are becoming more targeted, stakeholders are aligning diagnostic capabilities with therapeutic innovation to ensure timely and accurate intervention. Healthcare investments in personalized medicine and companion diagnostics are strengthening the clinical relevance of molecular biomarkers. Diagnostic developers are advancing liquid biopsy solutions and multi omics profiling approaches to support early detection, risk stratification, and real time therapy monitoring. These technologies are enabling minimally invasive testing and longitudinal disease tracking. Regulatory frameworks are supporting faster approvals for breakthrough diagnostics, while public and private research institutions are increasing research and development (R&D) spending. Market participants are prioritizing strategic collaborations, technology integration, and portfolio expansion to capture emerging opportunities.

Key Industry Highlights

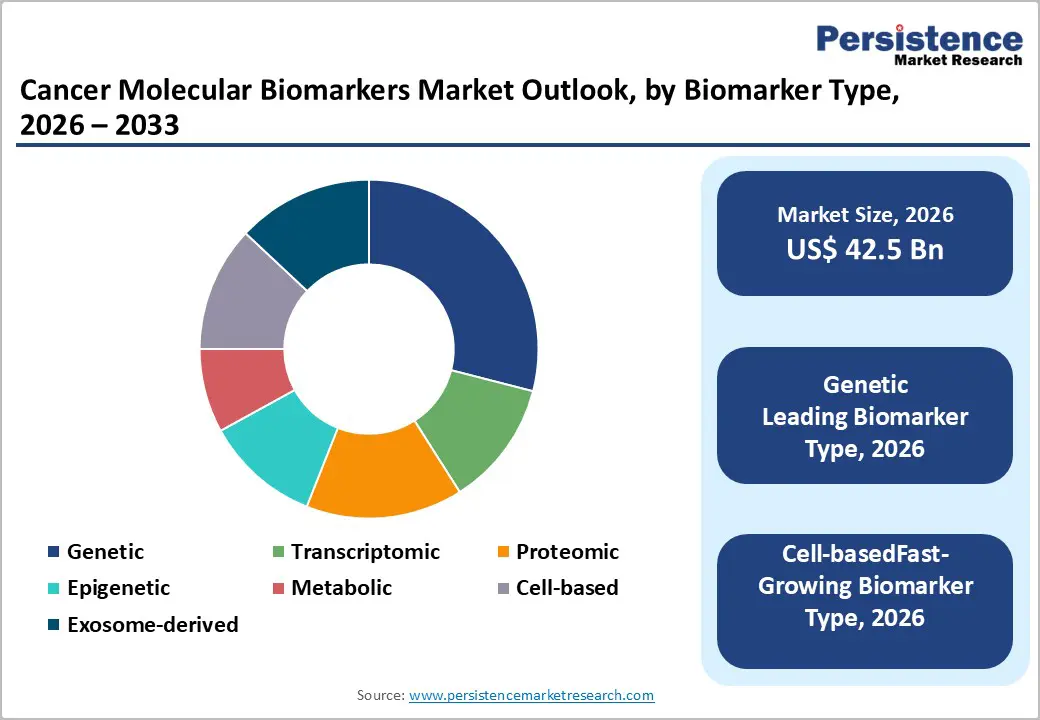

- Dominant Biomarker Types: Genetic biomarkers are projected to command around 29% of the revenue share in 2026, while cell-based ones are likely to be the fastest-growing at about 13.2% CAGR through 2033, driven by advances in liquid biopsy.

- Leading Profiling Technologies: NGS is expected to lead with roughly 30% market share in 2026, with bioinformatics analytics growing the fastest through 2033, reflecting increasing integration of AI and multi-omics data interpretation.

- Dominant Cancer Type: Breast cancer is anticipated to hold the largest revenue share at 25% in 2026, whereas lung cancer is set to be the fastest-growing segment from 2026 to 2033, supported by expanded molecular screening adoption.

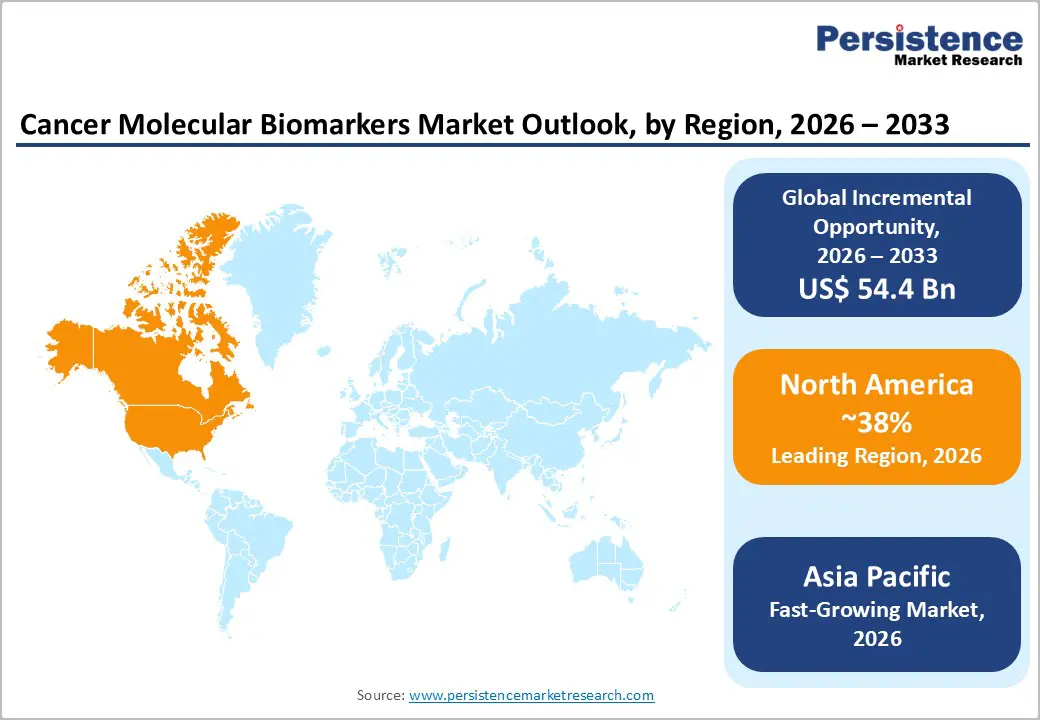

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026, owing to precision oncology adoption and strong reimbursement policies.

- Prime Driver: Market expansion is fueled by liquid biopsy commercialization, AI-enabled bioinformatics partnerships, and growing integration of companion diagnostics in clinical workflows

| Key Insights | Details |

|---|---|

| Cancer Molecular Biomarkers Market Size (2026E) | US$ 42.5 Bn |

| Market Value Forecast (2033F) | US$ 96.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Cancer Burden and Advanced Diagnostics

The cancer burden is rapidly increasing worldwide. As per the World Health Organization (WHO), 20?million new cases and 9.7?million cancer-related deaths were reported in 2022, making it one of the leading causes of mortality globally. This growth is driven by ageing populations, lifestyle risk factors such as tobacco use and obesity, and disparities in screening and early detection across regions. As traditional diagnostics often detect disease at later stages, there is rising reliance on molecular biomarkers that enable earlier and more precise detection, risk stratification, and improved treatment decisions for major cancers such as lung, breast, and colorectal cancers, which together account for a significant portion of reported cases.

The advancements in molecular profiling technologies are enhancing both the scope and quality of cancer diagnostics. Investments in NGS guidelines and quality management initiatives are improving laboratory practices and reliability of genomic testing, critical for tumor characterization. Innovations such as high-sensitivity PCR, multi-omics integration, and advanced bioinformatics analytics enable interpretation of complex genomic and proteomic datasets, accelerating biomarker discovery and clinical implementation. These tools support personalized therapeutic monitoring and companion diagnostics, allowing clinicians to tailor treatments to individual molecular profiles, a key factor in improving outcomes and expanding the clinical impact of biomarker-driven care.

High Costs and Complex Adoption Barriers in Molecular Diagnostics

The high cost of advanced molecular testing, including next?generation sequencing panels and specialized assays, remains a major barrier to wider clinical adoption. In many healthcare settings, comprehensive genomic profiling can exceed US$ 3,000–US $7,000 per test, yet only a minority of private insurers provide consistent coverage outside clinical trials, leaving significant out?of?pocket burden for patients. Limited reimbursement policies and inconsistent payer support also discourage providers from ordering broad molecular panels, particularly where evidence of clinical utility is still emerging. Financial strain affects both hospitals and patients, slowing the integration of biomarker testing into routine oncology care and creating disparities in access across different regions and patient groups.

In addition, regulatory and implementation complexities constrain market progress. Approval pathways for new assays vary by jurisdiction, requiring separate validations without coordinated review frameworks, which can extend commercialization timelines and increase development costs. Misalignment between regulatory and reimbursement processes adds unpredictability, as policymakers and payers demand robust evidence of clinical benefit before granting coverage. Workforce constraints, including shortages of trained specialists and bioinformatics expertise, further complicate deployment of complex molecular tests in routine labs. These combined cost, reimbursement, and operational barriers limit the speed at which precision biomarkers can be adopted into standard oncology practice, even as clinical demand continues to rise.

Expansion of Advanced Molecular and AI-Enabled Diagnostics

The adoption of liquid biopsy and minimally invasive testing presents a significant growth opportunity in cancer diagnostics. These assays enable real-time monitoring of tumor evolution and minimal residual disease (MRD), expanding the utility of biomarkers beyond traditional tissue sampling. With increasing sensitivity and broader regulatory acceptance, liquid biopsies are gaining traction for early detection, longitudinal patient monitoring, and therapy assessment, allowing clinicians to tailor treatment strategies more effectively. Rising cancer incidence, particularly in emerging regions, further fuels demand, while integration into routine clinical workflows strengthens the case for widespread adoption. These factors collectively position advanced molecular diagnostics as a cornerstone of precision oncology.

The strategic pharmaceutical investment is supported by recent breakthroughs, such as the FDA’s 2025 Breakthrough Therapy Designation for daraxonrasib (RMC?6236), a multi-selective RAS(ON) inhibitor targeting KRAS mutations in hard-to-treat tumors like pancreatic cancer. In parallel, novel cell-free RNA liquid biopsy assays are demonstrating potential for early cancer detection and treatment resistance monitoring. These innovations provide pharma companies opportunities to invest in precision oncology pipelines, accelerate drug development, and expand biomarker-guided therapeutic programs. Combined with AI-enabled analytics and regional expansion in emerging markets, these developments create a compelling landscape for next-generation molecular diagnostics and companion therapy strategies through 2033.

Category-wise Analysis

Biomarker Type Insights

Genetic biomarkers are estimated to hold approximately 29% of the market in 2026, reflecting their dominant role in early detection and targeted therapy. Key genetic alterations such as BRCA, EGFR, and KRAS guide treatment decisions for breast and lung cancers. Companies including ACT Genomics provide comprehensive profiling integrating DNA sequencing and bioinformatics. Roche Diagnostics, Illumina, and Qiagen continue expanding test menus to enhance clinical actionability. Advances in sequencing improve reproducibility and reliability in therapy selection. National guidelines recognize genetic profiling in standard treatment pathways. Recent studies report ANPEP and PIGR blood biomarkers can detect early-stage pancreatic cancer with 92% accuracy.

Exosome-derived and Cell-based biomarkers are projected to grow at a CAGR of around 13.2% between 2026 and 2033, driven by minimally invasive monitoring applications. They capture tumor biology through vesicles or intact cells in blood and urine, enabling longitudinal assessment without repeated biopsies. INOVIQ Ltd develops sensitive exosome capture tools for breast and ovarian cancer detection. Clinical validation is expanding across trials, improving translational potential. Regulatory recognition of non-tissue biomarkers is increasing. Automated workflows and advanced analytics accelerate adoption in diagnostic labs. Integration with clinical decision systems supports broader implementation in cancer management.

Profiling Technology Insights

Next-generation sequencing is estimated to account for approximately 30% of the cancer molecular biomarkers market revenue share in 2026 due to its ability to analyze multiple genomic regions simultaneously. Multi-gene panels guide targeted therapy and clinical trial enrollment. Illumina, Thermo Fisher Scientific, and Qiagen provide standardized NGS workflows for diagnostic labs. Collaboration with pharmaceutical firms produces companion diagnostics aligning molecular profiles with therapies. Reduced cost and faster turnaround times increase clinical adoption. NGS integration with digital pathology enhances reporting efficiency. Expanded panels now detect actionable and resistance-related mutations.

Bioinformatics analytics is projected to grow at a CAGR of approximately 14.2% during the 2026–2033 forecast period, fueled by an increasing demand for multi-omics data interpretation. Companies such as Epigene Labs apply AI and machine learning to accelerate biomarker discovery and patient stratification. Cloud-based solutions improve access for smaller laboratories. Predictive models enhance early detection and therapy response monitoring. Integration with clinical decision systems ensures actionable insights. Analytics platforms reduce turnaround time and operational burden. Investment in infrastructure supports adoption across clinical and research settings.

Cancer Type Insights

Breast cancer is expected to hold nearly 25% of the market share in 2026, supported by ER/PR, HER2, and genomic risk score panels guiding therapy and prognosis. Multi-marker blood tests such as Cantel™ by PrecisionRNA Biotech offer non-invasive early detection alternatives. Diagnostic companies continue optimizing panels for guideline-based decisions. Integration with clinical workflows enhances diagnostic accuracy and patient outcomes. National screening programs expand reach and early intervention. Multi-parameter immune markers predict therapeutic response in metastatic cases. Adoption remains strong in both routine care and research trials.

Lung cancer biomarkers are estimated to expand at a CAGR of about 12.8% from 2026 to 2033, driven by increased adoption of molecular profiling for therapy selection. Liquid biopsies facilitate real-time monitoring of ctDNA and mutations. Free NGS testing initiatives in select regions increase patient access and data availability. Panels targeting EGFR, ALK, and ROS1 mutations guide treatment decisions. Integration with proteomic and genomic markers improves early detection. Clinical validation studies support broader adoption. Personalized monitoring improves therapy outcomes and enhances the market trajectory.

Regional Insights

North America Cancer Molecular Biomarkers Market Trends

North America is estimated to hold about 38% of the cancer molecular biomarkers market share in 2026, supported by strong adoption of precision oncology and supportive insurance policies. A notable development is the January 2026 state mandate in Connecticut requiring private insurers to cover biomarker testing, expanding access and reducing financial barriers to molecular diagnostics in cancer care. The U.S. formulary also saw expanded approvals for biomarkers linked to novel therapies, elevating demand in clinical workflows. High adoption of NGS platforms and reimbursement support across Medicare and Medicaid enhance utilization in major oncology centers. Large oncology hospitals embed molecular profiling into routine diagnostics, supporting early detection and therapy selection. Investment continues in infrastructure and analytical platforms that support biomarker integration.

Regulatory pathways in the U.S. are accelerating innovation with defined frameworks for companion diagnostics, encouraging investment from diagnostics and biotech firms. Major diagnostic networks are aligning molecular assays with treatment guidelines, improving patient stratification. Research partnerships between academic institutions, national labs, and industry catalyze translational validation of new biomarkers. State?level insurance reforms are expected to reduce disparities in access to testing. Growth in clinical trials using biomarker endpoints is strengthening adoption, while venture funding and infrastructure grants are expanding genomics capabilities at leading cancer centers.

Europe Cancer Molecular Biomarkers Market Trends

Europe is likely to command a strong presence in the market for cancer molecular biomarkers in 2026 and beyond, driven by national screening initiatives and regulatory harmonization. A notable recent development is the regulatory approval and rollout of ColoAlert® for colorectal cancer screening in Switzerland in 2025, which expands non-invasive early detection options and demonstrates uptake of advanced diagnostics in clinical practice. Germany’s extensive laboratory networks and the U.K.’s national precision medicine programs support widespread biomarker testing. France and Spain are enhancing reimbursement frameworks for routine molecular assays, enabling broader clinical use. Harmonized quality standards under the European Union In-Vitro Diagnostic Regulation (EU IVDR) have improved assay reliability and clinician confidence across member states. Regional consortia and cross-border research initiatives facilitate multi-center clinical validation studies, accelerating adoption.

Healthcare systems across Europe continue to invest in advanced oncology diagnostics as part of cancer care strategies. Collaborative networks and academic research clusters support evidence generation for new biomarker panels. Conferences and professional forums, such as international cancer biomarker symposia in Paris and Rome, are shaping clinical and research agendas. These events promote knowledge sharing and highlight advancements in early detection and molecular profiling. Continuous investment in genomics infrastructure and reimbursement reforms further supports testing integration. The competitive landscape includes established diagnostics firms and emerging local players delivering tailored solutions, primed by Europe’s structured regulatory environment and clinical programs.

Asia Pacific Cancer Molecular Biomarkers Market Trends

Asia Pacific is estimated to be the fastest?growing regional market for cancer molecular biomarkers, projected to register a 12.9% CAGR through 2033, propelled by rising cancer incidence and healthcare investments. In April 2025, a Bengaluru?based laboratory partnership with the LuNGS Alliance launched free NGS biomarker testing for lung cancer patients across India, supported by AstraZeneca, Pfizer, Roche, and 4baseCare, illustrating how collaborative programs expand access and accelerate adoption. China’s investments in genomic initiatives and precision medicine fuel innovation and clinical uptake. Japan’s longstanding LC?SCRUM?Asia lung cancer genomic screening network continues to expand, facilitating biomarker-matched trials and accelerated regulatory approvals.

Regulatory landscapes across Asia Pacific are aligning with international standards, enabling broader test approvals and clinical integration. Government agencies are prioritizing precision oncology through funding and public?private partnerships that support infrastructure development and talent growth in molecular pathology. ASEAN health programs are incorporating cancer screening mandates that include molecular diagnostics in national plans. Rapid adoption of NGS and AI?enhanced analytics improves early detection and treatment monitoring. Regional initiatives and pilot programs demonstrate how coordinated efforts can overcome resource limitations and support long?term biomarker testing scale?up. The competitive landscape sees both multinational and regional firms targeting localized solutions to capture emerging demand.

Competitive Landscape

The global cancer molecular biomarkers market structure is moderately consolidated, with leading players such as Roche, Illumina, Thermo Fisher Scientific, Qiagen, and NeoGenomics Laboratories controlling a significant portion of the revenue. These established companies leverage extensive relationships with hospitals, research institutions, and pharmaceutical firms, while offering integrated biomarker testing platforms combining NGS, PCR, and bioinformatics analytics. They continue to invest heavily in R&D to maintain leadership in advanced sequencing, liquid biopsy, AI-driven biomarker interpretation, and companion diagnostics.

Regional and niche competitors, including ACT Genomics, Epigene Labs, and INOVIQ Ltd, focus on specialized applications such as exosome-based assays, cell-based biomarker platforms, and regional clinical validation studies. Barriers such as regulatory compliance, reimbursement variability, and complex laboratory integration limit new entrants. However, digital health adoption, AI-enabled analytics, and cloud-based molecular reporting platforms are enabling software-centric firms and startups to participate. Market consolidation is expected to rise gradually as leading firms acquire smaller specialized players to expand capabilities, while collaborative partnerships with biopharmaceutical companies accelerate innovation and market penetration.

Key Industry Developments

- In February 2026, a study conducted by researchers from researchers from the Shanghai Institute of Materia Medica, University of Chinese Academy of Sciences, Fudan University, and The First Affiliated Hospital of Naval Medical University found that glucoside xylosyltransferase 2 (GXYLT2) is strongly linked with tumor aggressiveness and poor outcomes in patients with gastric cancer, serving as a significant prognostic biomarker. Elevated GXYLT2 levels correlate with advanced disease stage, lower overall survival, and increased invasive behavior in tumor cells, particularly in diffuse-type gastric cancer.

- In October 2025, Guardant Health and Zephyr AI entered a strategic partnership to combine Guardant’s multimodal molecular data with Zephyr’s AI and machine learning (ML) capabilities to accelerate drug development and cancer biomarker discovery for targeted therapies. The collaboration is creating scalable, actionable insights for biopharmaceutical research and aims to improve therapy response prediction and support personalized oncology treatments.

- In August 2025, Aptamer Group launched a new biomarker discovery service that uses its proprietary Optimer® technology combined with advanced proteomic analysis to rapidly identify and validate disease biomarkers for pharmaceutical, biotechnology, and diagnostic research. This integrated approach accelerates target discovery by providing both validated biomarkers and high-specificity binding tools, reducing traditional timelines and supporting applications such as therapeutic target identification.

Companies Covered in Cancer Molecular Biomarkers Market

- Illumina, Inc.

- Thermo Fisher Scientific

- Roche Diagnostics

- Qiagen NV

- F. Hoffmann La Roche AG

- Abbott Laboratories

- Bio Rad Laboratories

- Agilent Technologies

- Becton, Dickinson and Company

- Guardant Health

- Foundation Medicine

- Exact Sciences Corporation

- Novartis AG

Frequently Asked Questions

The global cancer molecular biomarkers market is projected to reach US$ 42.5 billion in 2026.

Rising cancer incidence and the shift toward precision oncology supported by advanced diagnostics and regulatory backing are driving the market.

The market is poised to witness a CAGR of 12.5% from 2026 to 2033.

Key opportunities include liquid biopsy adoption, AI‑enabled analytics, biomarker‑guided drug development, and utilization growth in emerging economies.

Roche, Illumina, Thermo Fisher Scientific, Qiagen, NeoGenomics Laboratories, and ACT Genomics are a few among the leading players.