- Automotive Components & Materials

- Automotive Fuel System Market

Automotive Fuel System Market Size, Share, and Growth Forecast for 2026 - 2033

Automotive Fuel System Market by Component Type (Intake Manifold, Throttle Body, Air Filters, PCMs/ECMs, Fuel Filters, Fuel Pumps, Fuel Tanks, Pressure Regulators), by Engine Type (Petrol, Diesel), by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Off-road Vehicles), and Regional Analysis for 2026 - 2033

Automotive Fuel System Market Share and Trends Analysis

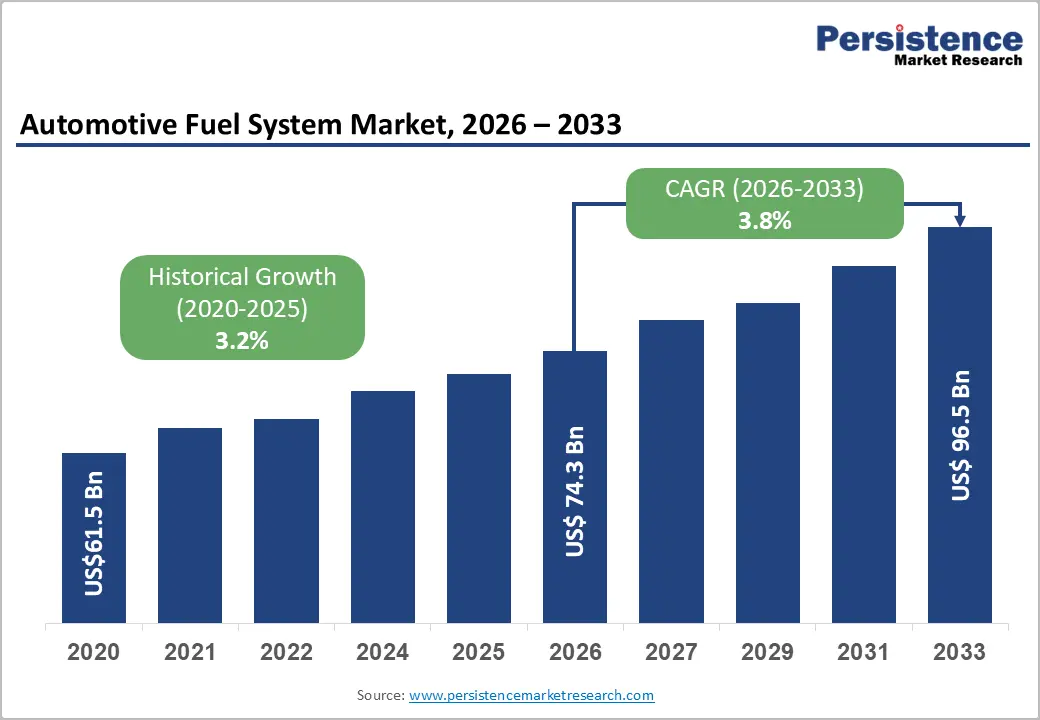

The global automotive fuel system market size is likely to be valued at US$ 67.1 billion in 2026 and is projected to reach US$ 87.1 billion by 2033, growing at a CAGR of 3.8% between 2026 and 2033.

The market expansion is primarily driven by increasing global vehicle production across passenger and commercial segments, rising consumer demand for fuel-efficient and high-performance vehicles, and continuous technological advancements in fuel injection systems. The transition toward alternative fuels, including compressed natural gas (CNG), liquefied natural gas (LNG), and biofuels, presents substantial growth opportunities, while stringent emission regulations worldwide compel automotive manufacturers to integrate advanced fuel delivery systems that optimize combustion efficiency and reduce harmful emissions.

Key Highlights Summary

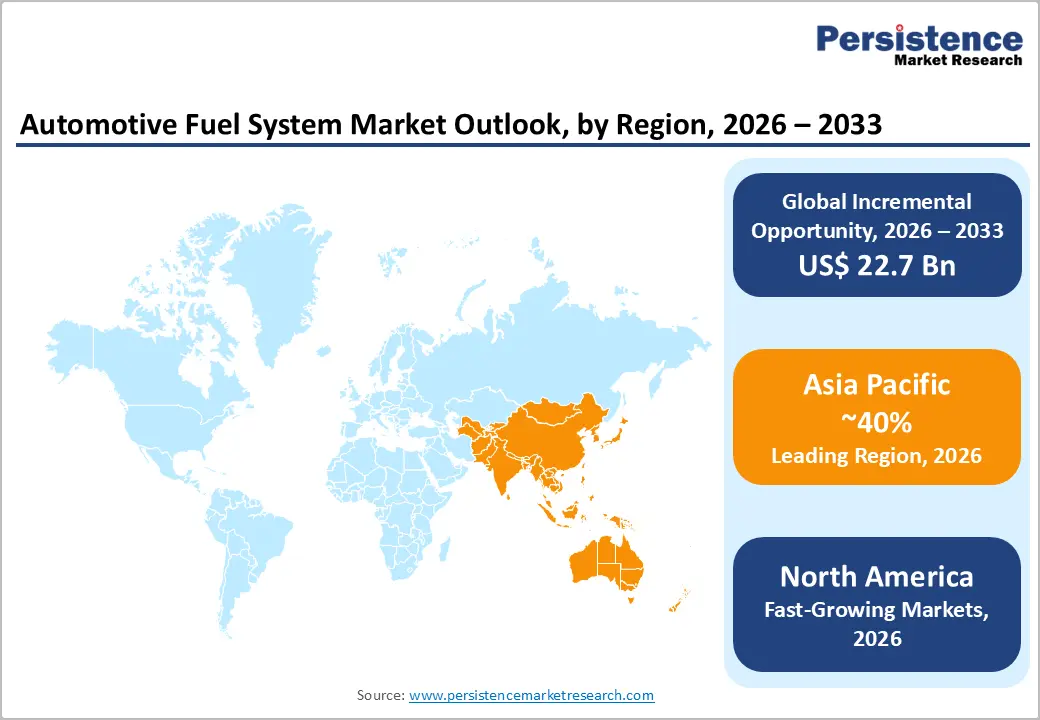

- Leading Region: Asia Pacific leads with 47% global market share, with China accounting for 28% independently and India demonstrating exceptional growth with 31 million vehicle production in FY25

- Leading Segment: Fuel injectors command 23% component market share with gasoline direct injection systems growing fastest at 6% CAGR, supported by regulatory mandates for improved fuel economy and reduced emissions

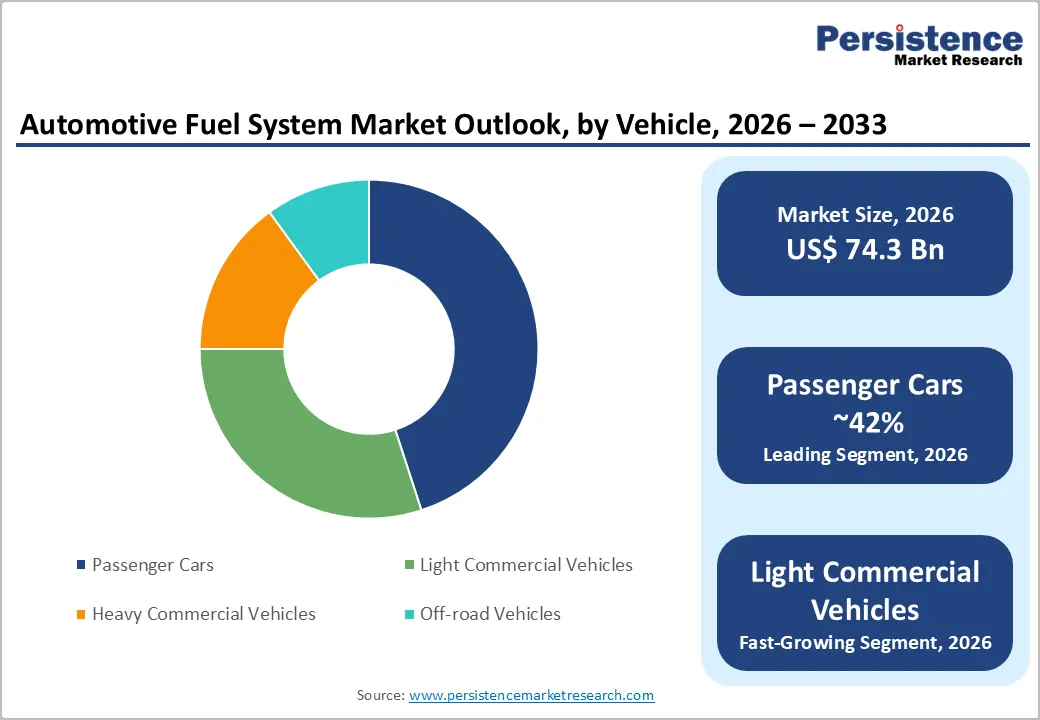

- Leading Segment: Passenger cars dominate vehicle type segmentation with 68% market share, while light commercial vehicles demonstrate the strongest growth at 5% CAGR driven by e-commerce logistics expansion.

- Fastest Growing Segment: Petrol engine fuel systems hold 52% market share with alternative fuel systems growing at 7% CAGR, reflecting diversification toward CNG, LNG, and biofuel-compatible technologies.

- Opportunities: Robert Bosch GmbH launched a next-generation GDI system in January 2024, reducing particulate emissions by 35%, addressing Euro 7 compliance requirements. Electric vehicle adoption poses a significant market challenge with 17 million EV sales in 2024 representing 25% annual growth, compressing long-term demand for conventional fuel systems.

| Key Insights | Details |

|---|---|

| Automotive Fuel System Size (2026E) | US$ 67.1 Bn |

| Market Value Forecast (2033F) | US$ 87.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.8% |

| Historical Market Growth (CAGR 2020 to 2024) | 3.2% |

Market Dynamics Analysis

Drivers - Rising Global Vehicle Production and Consumer Demand for Performance Enhancement

Global automotive production reached 75.5 million units in 2024 according to the International Organization of Motor Vehicle Manufacturers (OICA), with passenger vehicles constituting the majority segment. This substantial production volume directly correlates with increased demand for automotive fuel systems across all vehicle categories. The automotive fuel delivery and injection system market reflects robust demand for advanced fuel management technologies. Consumer preferences have shifted decisively toward performance-oriented vehicles equipped with sophisticated drivetrain systems capable of delivering optimal power output and acceleration characteristics. The automotive fuel system market benefits significantly from this trend as high-performance vehicles and supercars require precision-engineered fuel delivery mechanisms including high-pressure fuel pumps, advanced electronic control units (ECUs), and direct fuel injection (DFI) systems that ensure accurate fuel metering and combustion optimization.

Stringent Emission Regulations and Technological Advancements in Fuel Injection Systems

Governments worldwide have implemented progressively stricter emission standards to combat air pollution and reduce greenhouse gas emissions from the transportation sector. The European Union's Euro 7 emission standards and the United States Environmental Protection Agency's (EPA) Tier 5 norms mandate substantial reductions in carbon dioxide (CO2), nitrogen oxides (NOx), and particulate matter emissions from internal combustion engine vehicles. These regulatory frameworks necessitate the adoption of advanced fuel injection technologies such as Gasoline Direct Injection (GDI) and common rail diesel injection systems that optimize fuel atomization, improve combustion efficiency, and minimize emission levels. The automotive fuel injection system market is projected to grow from USD 15.24 billion in 2026 to USD 24.64 billion by 2034, exhibiting a CAGR of 6.19%, underscoring the critical role of fuel injection technology in meeting compliance requirements.

Restraints - Accelerating Electric Vehicle Adoption and Government Policy Support

The most significant structural challenge confronting the automotive fuel system market is the rapid transition toward electric vehicles (EVs) driven by governmental sustainability initiatives and consumer environmental consciousness. Global electric car sales surpassed 17 million units in 2024, representing a 25% increase from the previous year, exceeding the total number of electric cars sold globally in 2020. This exponential growth trajectory reflects substantial governmental investments in EV infrastructure development, including charging station networks, and generous subsidy programs designed to accelerate EV market penetration. For instance, India sold 100,000 electric vehicles in 2024, while the United States experienced a 2.3% increase in car sales in 2025 ahead of federal subsidy expirations, demonstrating policy-driven market dynamics. Electric vehicles eliminate the requirement for conventional fuel delivery systems including fuel tanks, fuel pumps, fuel injectors, pressure regulators, and intake manifolds, thereby directly reducing addressable market opportunities for traditional fuel system manufacturers.

Opportunity - Growing Adoption of Alternative Fuel Systems and Hybrid Powertrains

The increasing adoption of alternative fuels including CNG, LNG, biofuels (E85), and hydrogen fuel cells presents substantial expansion opportunities for fuel system manufacturers capable of engineering adaptable, multi-fuel compatible delivery systems. The Automotive Fuel System Market benefits from diversification strategies as consumers and fleet operators seek cost-effective fuel alternatives amid volatile petroleum prices and environmental sustainability concerns. Governments in emerging economies, particularly across South Asia and Latin America, actively promote CNG and LNG adoption through favorable taxation policies, fuel subsidies, and infrastructure investment programs, creating dedicated market segments for compressed gas fuel systems. Brazil's automotive sector demonstrated 14.1% sales growth in 2024, with flex-fuel vehicles accounting for a significant proportion, highlighting consumer preference for fuel flexibility. Hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs) represent transitional technologies that combine internal combustion engines with electric propulsion, requiring advanced fuel delivery and management systems optimized for intermittent engine operation patterns.

Expansion Opportunities in Emerging Automotive Markets

Rapid motorization in emerging economies including India, Indonesia, Vietnam, Brazil, and Africa creates substantial volume opportunities for fuel system manufacturers across both OEM and aftermarket channels. India produced over 31 million vehicles in FY25 and exported 5.3 million units, demonstrating dual prospects for domestic market supply and export-oriented manufacturing. The expanding middle-class population in these regions, coupled with improving road infrastructure and increasing urbanization rates, drives sustained growth in passenger vehicle ownership and commercial vehicle fleet expansion. Southeast Asian markets (ASEAN) exhibit particularly strong growth trajectories with Indonesia, Thailand, and Vietnam experiencing 6-8% annual increases in vehicle registrations, supported by government automotive industry development policies and foreign direct investment incentives.

Category-wise Analysis

By Component Type Insights

Fuel injectors dominate the component type segment with approximately 23% market share, driven by universal application across all internal combustion engine vehicles and increasing adoption of multi-point fuel injection (MPFI) and direct injection technologies. The Automotive Fuel System Market witness’s continuous innovation in fuel injector design, with manufacturers developing piezoelectric injectors capable of multiple injection events per combustion cycle, enabling precise fuel metering and optimized combustion characteristics. Fuel pumps represent the fastest-growing component subsegment with an estimated CAGR of 4%, supported by technological transitions toward high-pressure electric fuel pumps required for GDI systems that operate at pressures exceeding 200 bars. Intake manifolds maintain significant market presence with 17% share in 2024, as manufacturers engineer variable geometry intake systems that optimize airflow dynamics across different engine operating conditions. Air filters and fuel filters constitute essential maintenance components with consistent replacement demand, while throttle bodies increasingly incorporate electronic throttle control systems integrated with engine management computers, enhancing throttle response precision and fuel efficiency optimization.

By Vehicle Type Insights

Passenger cars command the dominant market share at approximately 68%, reflecting the segment's substantial production volumes and widespread consumer ownership globally. Within passenger cars, compact and mid-size vehicles account for the largest proportion in emerging markets where affordability and fuel economy considerations drive purchasing decisions, while premium sedans and SUVs demonstrate higher per-vehicle fuel system component values due to sophisticated multi-cylinder engine configurations and performance-oriented specifications.

Light commercial vehicles represent the fastest-growing vehicle type segment with estimated CAGR of 5%, driven by expanding e-commerce logistics requirements, last-mile delivery services, and urban commercial transportation demand in rapidly urbanizing Asian and Latin American markets. Heavy commercial vehicles including trucks, trailers, buses, and coaches maintain steady demand for robust, high-capacity fuel systems engineered for extended operational lifecycles and demanding duty cycles, with diesel fuel systems predominating in this segment due to superior torque characteristics and fuel economy advantages in long-haul applications.

By Engine Type Insights

Petrol engine fuel systems lead with approximately 52% market share, supported by global passenger car market preferences and regulatory advantages in emissions compliance compared to diesel alternatives. Gasoline direct injection (GDI) technology represents the fastest-advancing petrol fuel system variant with CAGR of 6%, as automakers leverage GDI's capability to deliver improved fuel economy ratings while meeting stringent particulate emission standards through advanced multi-pulse injection strategies. Diesel engine fuel systems hold significant market presence particularly in European commercial vehicle segments and Asian markets where diesel passenger car penetration remains substantial, with common rail diesel injection systems operating at ultra-high pressures exceeding 2,500 bar to achieve complete fuel atomization and minimize NOx and particulate emissions.

Regional Market Insights

North America Automotive Fuel System Market Share and Trends

North America accounts for approximately 12% of the global automotive fuel system market share, with the United States representing the dominant national market within the region. The U.S. automotive market demonstrates substantial commercial vehicle penetration, with pickup trucks and full-size SUVs commanding significant market shares, necessitating robust, high-capacity fuel systems engineered for larger displacement engines and towing applications. Light truck sales in the United States consistently exceed 12 million units annually, sustaining strong demand for fuel system components across this vehicle category.

The regulatory environment significantly influences market dynamics, with EPA enforcing stringent Corporate Average Fuel Economy (CAFE) standards that mandate fleet-wide fuel efficiency improvements, compelling manufacturers to integrate advanced GDI systems, turbocharging technologies, and cylinder deactivation strategies paired with sophisticated fuel management systems. North American automotive manufacturers prioritize innovation ecosystems, investing substantially in research and development facilities focused on next-generation fuel injection technologies, alternative fuel system compatibility, and hybrid powertrain integration.

Europe Automotive Fuel System Market Analysis

Europe holds approximately 19% of the global share, with Germany representing the continent's largest automotive production and innovation hub, producing 4.1 million vehicles in 2024. The region demonstrates leadership in diesel engine technology, particularly in passenger car applications, although regulatory pressures and consumer sentiment shifts following emission norms have accelerated transitions toward gasoline and electrified powertrains. France, the United Kingdom, Spain, and Italy constitute additional significant markets with established automotive manufacturing sectors and sophisticated supply chain ecosystems.

The European regulatory framework exerts profound influence on fuel system technology development, with REACH regulations restricting hazardous substances in automotive components and Euro 7 emission standards establishing the world's most stringent limits on NOx, particulate matter, and CO2 emissions from internal combustion engines. These requirements necessitate ultra-high-pressure fuel injection systems, advanced combustion management strategies, and comprehensive evaporative emission control technologies.

Asia Pacific Automotive Fuel System Market Trends

Asia Pacific emerges as the largest and fastest-growing regional market with approximately 40% global market share, led by China's dominant position, accounting for 28% of the worldwide automotive fuel system market. China's automotive production ecosystem encompasses both mass-market and premium vehicle segments, with annual production volumes exceeding 23 million units in 2024, creating unparalleled scale advantages for fuel system component manufacturers.

India demonstrates exceptional growth potential with vehicle production surpassing 31 million units in FY25 and exports reaching 5.3 million units, supported by the government's Production-Linked Incentive (PLI) scheme that incentivizes domestic manufacturing expansion and technology upgradation. The Indian market exhibits strong demand for affordable, fuel-efficient vehicles in compact segments, driving adoption of cost-optimized multi-point fuel injection systems.

Competitive Landscape

The global automotive fuel system market exhibits moderately concentrated competitive dynamics, with several multinational corporations commanding substantial market shares while numerous regional and specialized players contribute to market diversity and innovation. Market concentration reflects the industry's capital-intensive nature, stringent quality certification requirements, and the significant research and development investments necessary to develop fuel system technologies compliant with evolving emission regulations and performance specifications.

Leading manufacturers leverage technological innovation capabilities, global manufacturing footprints, established OEM relationships, and comprehensive product portfolios spanning multiple fuel system component categories to maintain competitive advantages. The market witness’s active consolidation through mergers and acquisitions as companies seek to expand technological capabilities, access new geographic markets, and achieve economies of scale in component manufacturing.

Key Developments:

- In March 2025, Standard Motor Products expanded its Standard® gasoline fuel-injector range with new-manufacture units engineered for OE spray patterns and flow, boosting durability and efficiency.

- In February 2024, GB Remanufacturing enlarged its gasoline direct-injection program with injectors, seal kits, multi-packs, and a premium seal-tool kit announced at AAPEX 2023.

Companies Covered in Automotive Fuel System Market

- Plastic Omnium

- Denso Corporation

- Robert Bosch GmbH

- YAPP Automotive Systems Co., Ltd

- TI Automotive

- Delphi Technologies PLC

- Continental AG

- Hitachi Automotive Systems Ltd

- Federal-Mogul Corporation

- Edelbrock LLC

- Woodward, Inc

- Kinsler Fuel Injection

- Other Key Players

Frequently Asked Questions

The global Automotive Fuel System Market is projected to reach US$ 87.1 billion by 2033, growing from US$ 67.1 billion in 2026 at a compound annual growth rate (CAGR) of 3.8% throughout the forecast period.

The primary growth drivers include rising global vehicle production volumes that reached 75.5 million units in 2024, increasing consumer demand for fuel-efficient and high-performance vehicles requiring advanced fuel delivery systems, and stringent emission regulations such as Euro 7 and EPA Tier 5 standards that mandate adoption of sophisticated fuel injection technologies including gasoline direct injection systems.

Significant opportunities include the growing adoption of alternative fuel systems compatible with CNG, LNG, biofuels, and hydrogen, which create new market segments as governments promote fuel diversification through favorable policies and infrastructure investments. The hybrid and plug-in hybrid electric vehicle segment, projected to grow at 8-10% annually through 2030, requires specialized fuel delivery systems optimized for intermittent engine operation.

Asia Pacific dominates the global Automotive Fuel System Market with approximately 40% market share, led by China's commanding 28% share independently. China's automotive production exceeded 23 million units in 2024, representing the world's largest manufacturing base and consumer market.

Leading companies include Robert Bosch GmbH with approximately 22% global market share through comprehensive fuel injection and fuel pump portfolios, Denso Corporation holding 18% market share with strengths in hybrid vehicle fuel systems, and Continental AG commanding 12% market share focused on integrated fuel system solutions.