- Agrochemicals

- Asia Textile Sizing Chemicals Market

Asia Textile Sizing Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Asia Textile Sizing Chemicals Market by Product Type (Starch-based Sizing Agents, Synthetic Polymer-based Sizing Agents, Natural Polymer-based Sizing Agents, and Others), Fiber/Yarn Type (Cotton Fibers/Yarns, Synthetic Fibers, Blended Fibers, and Others), Industry (Apparel / Garments, Home Textiles, Industrial / Technical Textiles, and Others), and Regional Analysis

Asia Textile Sizing Chemicals Market Size and Share Analysis

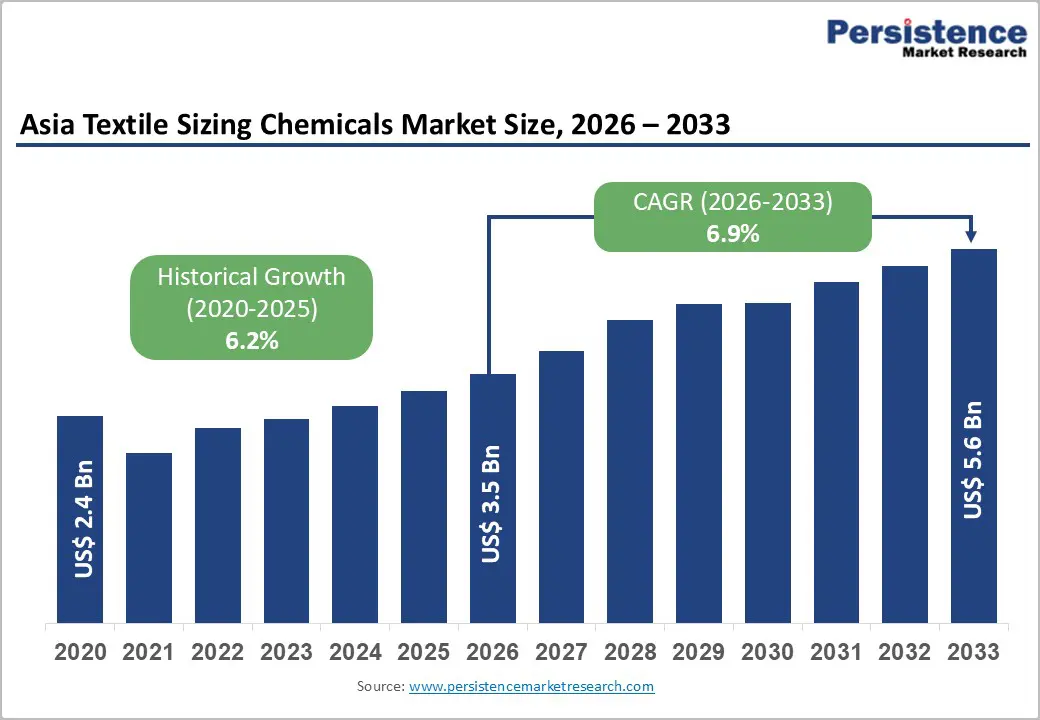

Asia textile sizing chemicals market size is likely to be valued at US$ 3.5 billion in 2026 and is projected to reach US$ 5.6 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

Robust growth in textile manufacturing across China, India, and other Asian economies, which collectively account for over 70% of global textiles and clothing exports, underpins sustained demand for sizing chemicals that enhance weaving efficiency and yarn performance. The rising penetration of synthetic and blended fibers, now accounting for approximately 69% of global fiber output, together with the rapid expansion of technical textiles, further increases the need for advanced starch- and synthetic-polymer-based sizing systems.

Key Industry Highlights:

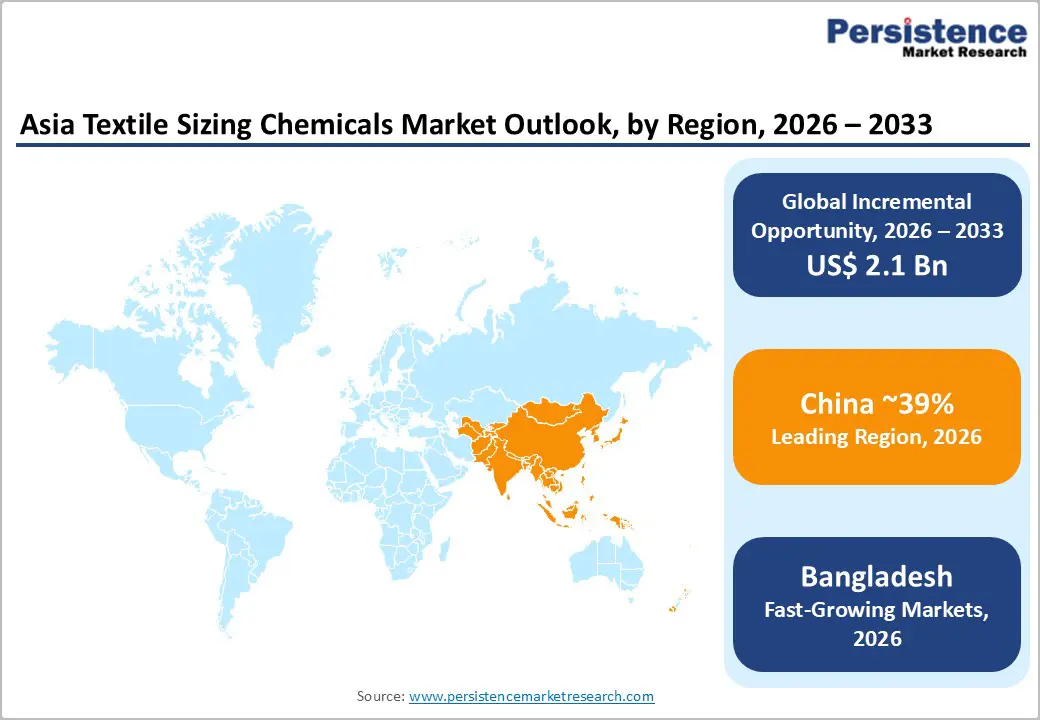

- Leading Country: China dominates the Asia Textile Sizing Chemicals Market, accounting for approximately 39% of global consumption in 2026, driven by massive textile manufacturing capacity, abundant raw material availability, and pro-manufacturing government policies, accelerating the regional market.

- Fastest Growing Country: Bangladesh represents the fastest-growing regional corridor within Asia, led by its $47 billion garment exports, and rapidly expanding manufacturing ecosystems.

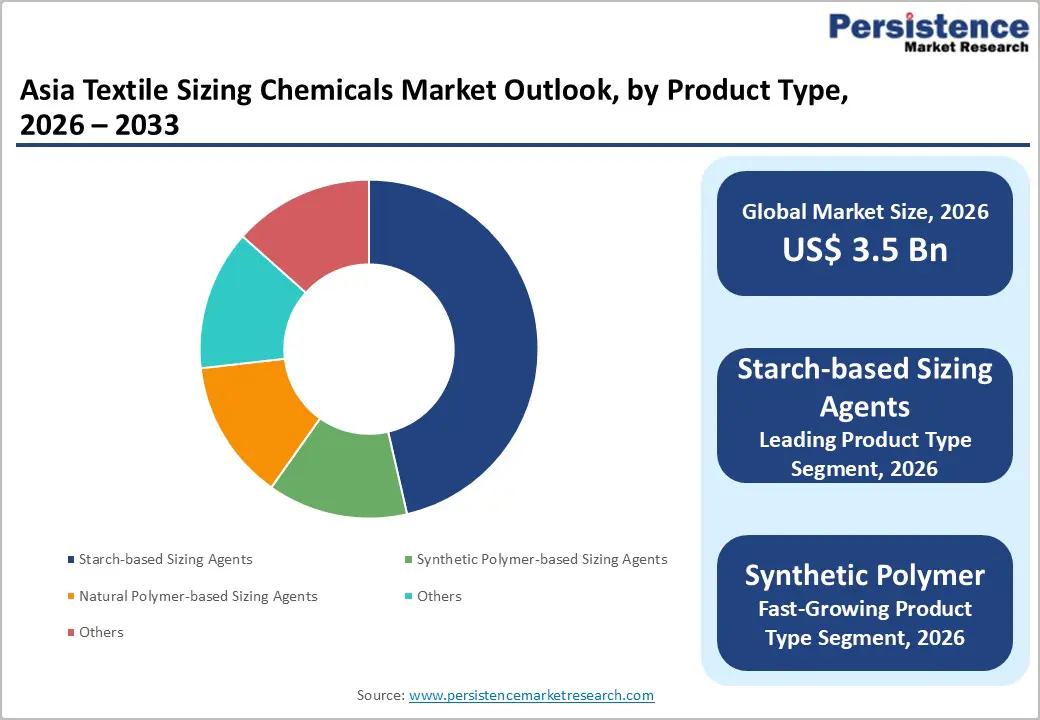

- Dominant Product Type: Starch-based sizing agents dominate the Asia textile sizing chemicals market, accounting for 55% of total consumption in 2026, owing to their cost-effectiveness, easy availability, and strong compatibility with cotton and blended yarn applications.

- Fastest-Growing Product Type: The Synthetic Fibers segment represents the fastest-growing fiber/yarn type application, expanding at an approximately 8.1% CAGR through 2033, driven by surging polyester and nylon production and by the growing demand for technical textiles, which require specialized sizing chemistries with enhanced adhesion and performance characteristics that exceed those of

- traditional starch-based agents.

- Key Opportunity: Rising environmental regulations, growing sustainability demand from global brands, and increasing adoption of green manufacturing practices are rapidly driving the adoption of bio-based, biodegradable, and low-impact sizing solutions.

| Key Insights | Details |

|---|---|

| Asia Textile Sizing Chemicals Market Size (2026E) | US$ 3.5 Bn |

| Market Value Forecast (2033F) | US$ 5.6 Bn |

| Projected Growth CAGR (2026 - 2032) | 6.9% |

| Historical Market Growth (2020 - 2025) | 6.2% |

Market Dynamics

Drivers - Rising dominance of Asian textile manufacturing and export capacity

Asia textile sizing chemicals market is strongly driven by the region’s growing dominance in global textile manufacturing and exports. Asia, led by major textile-producing countries such as China, India, Bangladesh, Vietnam, and Indonesia, has established itself as the world’s primary hub for yarn, fabric, and garment production. The presence of an extensive and cost-efficient manufacturing base, abundant availability of raw materials, skilled labor, and well-developed textile clusters has enabled Asian manufacturers to achieve large-scale production at competitive costs. Rising export demand from North America, Europe, and the Middle East for apparel, home textiles, and industrial fabrics has further accelerated textile output across the region. As weaving activity increases, the demand for sizing chemicals, used to enhance yarn strength, abrasion resistance, and weaving efficiency, rises proportionally.

Export-oriented manufacturers prioritize consistent fabric quality, low defect rates, and high loom efficiency to meet international quality standards, which increases reliance on advanced sizing formulations. Government initiatives supporting textile exports, infrastructure development, and integrated textile parks across several Asian economies are expanding installed weaving capacities. The rapid adoption of modern high-speed looms and automation in export-focused mills also necessitates high-performance sizing chemicals that ensure smooth yarn processing under demanding operating conditions.

Shift Toward Technical Textiles, Synthetic Fibers, and Performance Fabrics

Asian textile producers are increasingly diversifying beyond conventional cotton-based apparel into higher-value segments, including automotive textiles, industrial fabrics, medical textiles, sportswear, and protective clothing. These applications rely heavily on synthetic fibers, such as polyester, nylon, and acrylic, and on blended yarns, which exhibit different surface properties and processing requirements than natural fibers. As a result, specialized sizing chemicals with enhanced film-forming ability, adhesion, flexibility, and thermal stability are required to maintain yarn integrity during high-speed weaving. Performance fabrics also require superior properties, including dimensional stability, a smooth surface finish, uniform strength, and reduced breakage, all of which depend on effective sizing performance.

The growing use of advanced weaving technologies and complex fabric constructions in technical textiles increases mechanical stress on yarns, intensifying the need for high-efficiency sizing solutions. Chemical suppliers are developing synthetic-polymer-based and modified-starch-based sizing agents tailored for synthetic and blended yarns. This transition toward value-added textiles not only raises per-unit consumption of sizing chemicals but also shifts demand toward more advanced, higher-margin formulations, thereby significantly contributing to market growth across Asia.

Restraints - Geopolitical Tensions, Trade Tariffs, and Export Uncertainty as Key Market Restraints

The Asian textile sizing chemicals market is significantly restrained by geopolitical tensions, escalating trade tariffs, and evolving export dynamics that dampen demand. India’s textile and apparel exports witnessed a 12.9% decline in October 2025 compared with October 2024 following the introduction of reciprocal U.S. tariffs of up to 50%, reducing overall export volumes from $3.06 billion to $2.67 billion in that month alone. These high tariffs have cut Indian cotton textile shipments by roughly 30%, reflecting immediate disruptions to traditional trade flows. The U.S., historically accounting for up to 29-30% of India’s textile and apparel exports, remains a vital destination, meaning tariff volatility directly affects production planning and export forecasts.

The recent suspension of EU preferential tariff benefits for Indian exports, which previously covered about 87% of export categories, imposes additional cost burdens and reduces competitiveness in one of Asia’s largest markets. Such policy shifts create volatility in export earnings and deter long-term investment in textile-processing infrastructure, including sizing-chemical applications. Supply chain disruptions driven by geopolitical instability also led to higher freight costs and longer lead times, squeezing margins and reducing the appeal of long-term procurement contracts. Collectively, these trade barriers and geopolitical uncertainties constrain textile production volumes and, in turn, restrain demand growth for sizing chemicals in Asia.

Regulatory restrictions on hazardous substances in textiles and chemicals

Under the REACH regulation, the European Commission has added 33 carcinogenic, mutagenic, and reproductive toxicants (CMR 1A/1B) relevant to textiles to Annex XVII, setting stringent concentration limits for substances such as formaldehyde, certain phthalates, azo dyes, and heavy metals in apparel and home textiles. The EU Strategy for Sustainable and Circular Textiles aims to phase out hazardous chemistries and promote circularity, while the ZDHC Manufacturing Restricted Substances List (MRSL) targets the removal of problematic chemicals from textile processing supply chains. Suppliers of textile sizing chemicals that depend on legacy formulations face reformulation costs, testing requirements, and potential market access risks if they do not align quickly with these frameworks, dampening near-term profitability and acting as a barrier to entry for smaller regional formulators.

Opportunity - Acceleration of bio-based and low-impact sizing formulations

The accelerating shift toward bio-based and low-impact sizing formulations represents another major opportunity for the Asia Textile Sizing Chemicals Market. Growing environmental regulations, water-use restrictions, and sustainability commitments by global apparel brands are prompting textile producers to adopt environmentally friendly processing chemicals. Bio-based sizing agents derived from modified starches, natural polymers, and biodegradable additives offer advantages such as easier desizing, lower wastewater load, and reduced chemical oxygen demand (COD).

Asian manufacturers supplying export markets are increasingly adopting these formulations to comply with international sustainability standards and brand audits. Low-impact sizing chemicals enable mills to lower effluent treatment costs and improve overall process efficiency. As sustainability transitions from a compliance requirement to a competitive differentiator, suppliers offering high-performance, environmentally responsible sizing solutions are well positioned to capture new demand, premium pricing, and long-term partnerships within Asia’s evolving textile ecosystem.

Digitalization, High-Speed Weaving, and Premium Technical Textile Clusters Creating New Growth Opportunities

The rapid digitalization of textile manufacturing and the increasing adoption of high-speed weaving technologies across Asia present a strong opportunity for the textile sizing chemicals market. Leading textile clusters in China, India, Japan, South Korea, and Southeast Asia are investing in smart factories, automated warping systems, and digitally controlled looms to improve productivity, reduce defects, and meet global quality standards. High-speed and air-jet looms exert greater mechanical stress on yarns, increasing the need for advanced sizing chemicals with superior film strength, flexibility, and adhesion.

The emergence of premium technical textile clusters focused on automotive textiles, industrial fabrics, geotextiles, and protective clothing is driving demand for specialized sizing solutions tailored for synthetic and blended yarns. These segments typically require higher-value formulations, thereby increasing the per-unit revenue potential relative to conventional textile applications. As manufacturers upgrade equipment and shift toward complex fabric constructions, demand for customized, performance-enhancing sizing chemicals is expected to rise, creating long-term growth opportunities across advanced textile hubs in Asia.

Category-wise Analysis

Product Type Insights

Within the Asia textile sizing chemicals market, starch-based sizing agents account for the largest share, estimated at around 55% of total consumption in 2026. The majority of sizing agents used by the global textile industry are made of starch and starch derivatives, reflecting their ready availability from corn, potato, and tapioca and their favorable cost-to-performance ratio. Starch-based systems remain the standard for cotton and cotton-rich yarns, particularly in apparel and home textiles, where biodegradability and ease of desizing are critical for meeting wastewater regulations and buyer sustainability audits.

The ongoing R&D, including patents on advanced amylose starches and starch/PVA blends, has improved film strength, abrasion resistance, and loom efficiency, allowing starch-based agents to maintain their leadership even as synthetic polymers gain share in high-performance and fully synthetic yarn applications. This combination of cost competitiveness, renewability, and performance ensures that starch-based agents will remain the anchor chemistry segment in Asia through 2032.

Fiber/Yarn Type Insights

Cotton fibers and yarns account for the leading share of sizing chemical consumption in Asia, with an estimated 45% of regional textile sizing chemical demand in 2026. Although cotton’s share of global fiber production has declined to around 19-20%, up to 70% of cotton is still used in apparel and about 30% in home textiles, sectors where warp sizing of ring-spun and open-end cotton yarns remains indispensable. Asia hosts the world’s largest cotton spinning bases, with India ranking as the leading cotton producer by volume and China remaining a major consumer and processor of cotton and cotton-blend yarns for both domestic and export markets.

Cotton yarns typically require higher add-on levels of starch-based or starch/PVA sizing to control hairiness, improve tensile strength, and reduce end-breaks at high loom speeds. As Asian mills upgrade to faster looms and higher-Count yarns, demand for advanced sizing solutions specifically tailored to cotton and cotton-rich blends is expected to remain strong, even as synthetic filament and micro-filament yarns capture a growing share of total fiber usage.

Industry Analysis

The apparel/garments segment is the dominant end-use industry for textile sizing chemicals in Asia, accounting for an estimated 50% of regional sizing chemical consumption in 2024. Global data show that clothing accounts for the majority of textile usage in value terms, with the textiles and clothing industry representing about 3.7% of world merchandise exports, and Asia, particularly China, Bangladesh, Vietnam, and India, leading in garment exports. In this value chain, warp sizing is critical for denim, shirting, suiting, and knit-to-woven constructions, in which yarns must withstand high tensions and friction during weaving to prevent fabric defects and productivity losses.

The strong export orientation of Asian garment manufacturing, supported by integrated supply chains and growing intra-Asian sourcing of yarns and fabrics, directly translates into sustained demand for sizing chemicals for apparel-focused weaving operations. As global brands push for higher-quality, defect-free fabrics and commit to programs such as ZDHC and the EU Textile Strategy, demand is shifting toward eco-optimized sizing chemistries that deliver excellent loom performance while facilitating low-impact desizing, reinforcing the strategic importance of this end-use segment.

Regional Insights

China Textile Sizing Chemicals Trends

China represents the largest market within the Asia Textile Sizing Chemicals Market, accounting for an estimated 39% of regional demand, supported by its unmatched scale of textile and fabric production. The country hosts the world’s largest weaving capacity, with extensive production of cotton, polyester, blended, and technical fabrics, supplying both domestic consumption and exports. Continuous investments in modern air-jet and rapier looms, integrated textile parks, and large-scale fabric mills drive consistent demand for sizing chemicals to improve yarn strength, loom efficiency, and fabric quality.

China’s strong presence in technical textiles, including industrial fabrics, automotive textiles, and functional apparel, further boosts the consumption of advanced synthetic and polymer-based sizing formulations. In addition, tightening environmental regulations are encouraging a gradual shift toward low-impact and modified bio-based sizing agents, supporting value growth.

India Textile Sizing Chemicals Trends

India represents a high-growth and strategically significant market within the Asia textile sizing chemicals market, accounting for approximately 28% of regional demand. The country benefits from a large and diversified textile ecosystem spanning cotton, man-made fibers, blended yarns, and technical textiles. Strong domestic consumption, coupled with India’s position as a leading exporter of textiles and apparel, is driving sustained weaving activity and consistent demand for sizing chemicals.

Government initiatives such as the expansion of integrated textile parks, production-linked incentive (PLI) schemes for man-made fibers and technical textiles, and infrastructure investments are supporting capacity additions and modernization.

Indian mills are increasingly adopting high-speed looms and automated weaving systems, which require efficient and high-performance sizing formulations to reduce yarn breakage and improve loom productivity. At the same time, increasing regulatory scrutiny of wastewater treatment and sustainability is accelerating the shift toward modified starch, bio-based, and low-impact sizing chemicals. While short-term export volatility stemming from global trade uncertainties can affect volumes, India’s strong domestic textile base, expanding technical textile segment, and ongoing modernization efforts position it as a key growth engine within the regional market.

Japan Textile Sizing Chemicals Trends

Japan represents a mature and relatively stagnant segment of the Asia textile sizing chemicals Market, accounting for approximately 5.6% of regional consumption. Domestic textile production volumes have largely stabilized due to high labor costs, an aging workforce, and limited capacity expansion. However, Japan remains strategically important due to its focus on high-quality, specialty, and technical textiles, including carbon fiber fabrics, industrial materials, and advanced performance textiles.

Demand for sizing chemicals in Japan is driven more by innovation than volume, with strong emphasis on precision sizing, consistency, and compatibility with high-end fibers. Japanese mills prioritize premium, low-residue, and environmentally compliant sizing formulations to meet strict quality and sustainability standards. While overall growth remains modest, Japan plays a critical role in technology development, specialized applications, and benchmark-setting in advanced textile processing.

Bangladesh Textile Sizing Chemicals Trends

Bangladesh is emerging as the fastest-growing market for textile sizing chemicals in Asia, with demand projected to grow at a CAGR exceeding 7.8% over the medium term. The country has rapidly expanded its weaving and fabric manufacturing capacity to reduce reliance on imported textiles and support its globally competitive garment export industry. Strong growth in woven fabric production, rising foreign direct investment in backward integration, and government incentives for textile modernization are driving increased consumption of sizing chemicals.

Export-oriented mills are upgrading to modern looms, which require higher-performance sizing agents to minimize yarn breakage and improve productivity. Additionally, increasing pressure from international apparel brands to improve quality and sustainability is accelerating the adoption of more effective and efficient sizing formulations. These factors position Bangladesh as a high-growth opportunity market within the Asia Textile Sizing Chemicals landscape.

Competitive Landscape

Asia textile sizing chemicals market is moderately consolidated at the top, with global specialty chemical leaders such as Archroma, BASF SE, Evonik Industries AG, Huntsman Corporation (Textile Effects business now integrated into Archroma), and Solvay S.A. complemented by strong regional players including Resil Chemicals Pvt. Ltd., Kiri Industries Ltd., and Govi N.V. The acquisition of Huntsman Textile Effects by Archroma in 2023 created a larger technology and product portfolio spanning pretreatment, dyeing, finishing, and sizing, reinforcing scale advantages in R&D, technical service, and regulatory compliance.

Leading players differentiate through eco-optimized chemistries (e.g., low-COD starch systems, high-performance PVA grades), digital process support, and the ability to design customized formulations for specific fiber blends and loom configurations. Emerging business models focus on value-added services such as on-site process audits, wastewater footprint reduction roadmaps, and collaboration with machinery OEMs and brands under frameworks like ZDHC and Sustainable Chemistry for the Textile Industry (SCTI).

Key Developments:

- In January 2026, Archroma, a global leader in specialty chemicals focused on sustainable solutions, partnered with HeiQ, a Swiss deep-tech innovator specializing in functional textiles and sustainable fibers, through a co-marketing agreement. This collaboration leverages their complementary expertise to provide advanced, environmentally responsible anti-odor and antimicrobial technologies to brands, retailers, and textile manufacturers worldwide.

- In September 2025, Evonik and AMSilk, a global leader in silk protein-based biomaterials, strengthened their partnership through a long-term agreement to manufacture sustainable silk proteins at industrial scale. Expanding on their 2023 collaboration, the companies have commissioned a dedicated production line at Evonik’s facility in Slovakia to produce AMSilk’s high-performance silk materials.

- In April 2025, BASF announced the commissioning of the world’s first commercial Loopamid plant at its Caojing site in Shanghai, China. With an annual production capacity of 500 metric tons, the facility represents a significant milestone in supplying sustainable solutions to the textile industry. Loopamid is a fully recycled polyamide 6 made entirely from textile waste, supporting the rising demand for sustainable polyamide 6 fibers.

Companies Covered in Asia Textile Sizing Chemicals Market

- Archroma

- BASF SE

- Evonik Industries AG

- Huntsman Corporation

- Lanxess AG

- Solvay S.A.

- Kiri Industries Ltd.

- Omnova Solutions Inc.

- Fibro Chem, LLC

- Govi N.V.

- Resil Chemicals Pvt. Ltd.

- German Chemicals Ltd.

Frequently Asked Questions

The Asia Textile Sizing Chemicals Market is projected to reach US$ 5.6 Bn by 2033, expanding from US$ 3.5 Bn in 2026 at a compound annual growth rate of 6.9% during the 2026-2033 forecast period, driven by robust textile manufacturing growth across China, India, Bangladesh, and Vietnam.

The primary demand drivers include Asia's dominant position accounting for 48% of global textile production, major export growth with Vietnam achieving $46 billion in 2025 textile exports and Bangladesh exceeding $47 billion, transition toward high-speed weaving requiring superior sizing agents, and the $43 million regional sustainability initiative accelerating adoption of eco-friendly formulations.

Starch-based sizing agents dominate the market, accounting, 55% of total consumption in 2026, owing to their cost-effectiveness, easy availability, and strong compatibility with cotton and blended yarn applications.

China leads the Asia Textile Sizing Chemicals market, accounting for approximately 39% of the total market share in 2026, driven by its large textile manufacturing base and strong export-oriented production capacity.

Driven by rising environmental regulations, growing sustainability demand from global brands, and increasing adoption of green manufacturing practices, bio-based, biodegradable, and low-impact sizing solutions are rapidly gaining traction and are expected to be key growth drivers in the coming years.

Leading companies operating in the Asia Textile Sizing Chemicals market include Archroma, BASF SE, Evonik Industries AG, Huntsman Corporation, Lanxess AG, and Solvay S.A.