- Home Appliances

- Southeast Asia Residential Water Treatment Equipment Market

Southeast Asia Residential Water Treatment Equipment Market Size, Share, and Growth Forecast 2026 – 2033

Southeast Asia Residential Water Treatment Equipment Market by Equipment Type Purification Equipment, Reverse Osmosis, UV, Gravity/Media, Filtration Equipment, Faucet Filters, and Others), Installation Type (Point of Use and Point of Entry), and Country Analysis

Southeast Asia Residential Water Treatment Equipment Market Size and Share Analysis

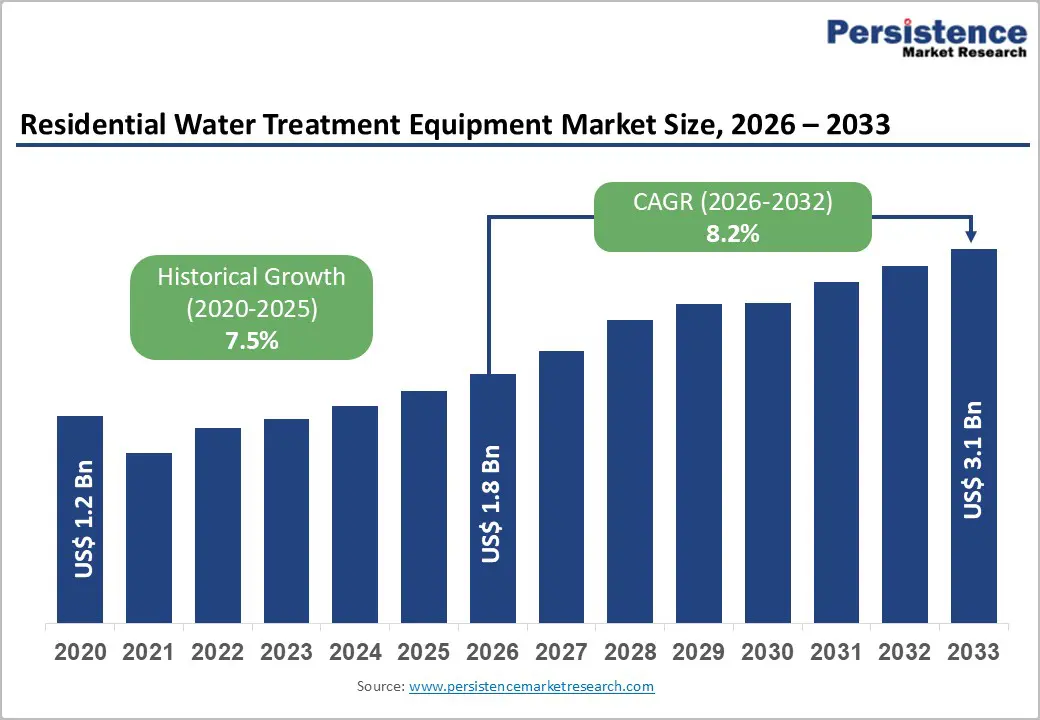

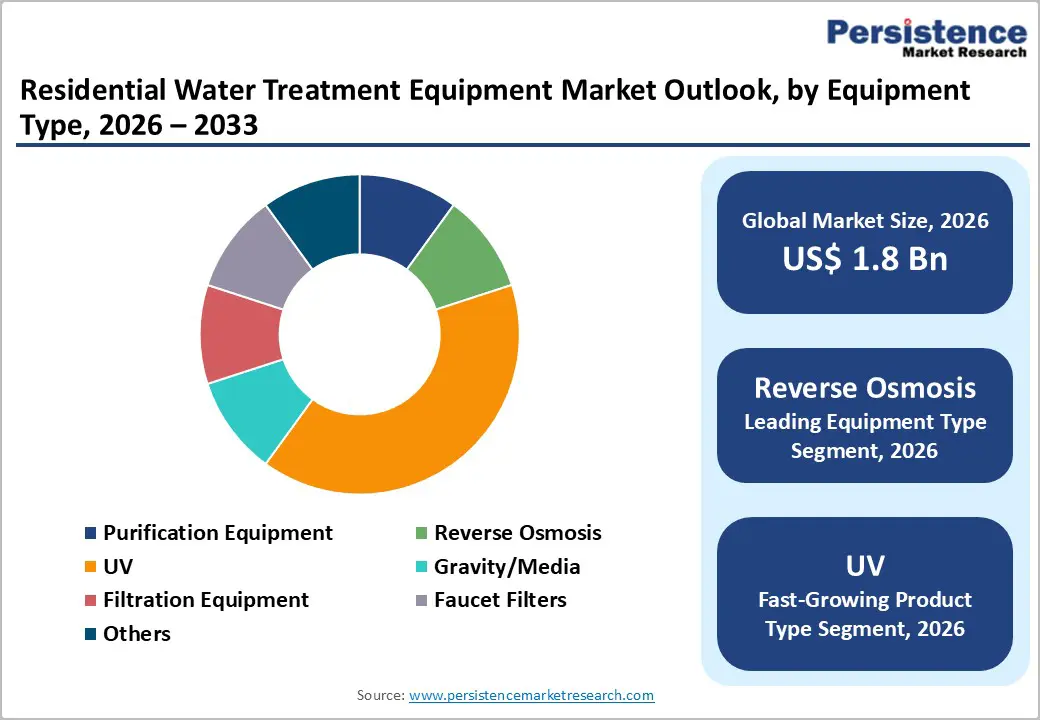

The Southeast Asia Residential Water Treatment Equipment market size was valued at US$ 1.8 Bn in 2026 and is projected to reach US$ 3.1 Bn by 2033, growing at a CAGR of 8.2% between 2026 and 2033. The Southeast Asia residential water treatment equipment market is experiencing robust growth driven by escalating concerns about waterborne illnesses, rapid urbanization, and government initiatives promoting universal access to clean drinking water. The WHO estimates that unsafe water leads to approximately 500,000 deaths annually from diarrheal diseases, intensifying consumer demand for residential purification systems.

Key Market Highlights

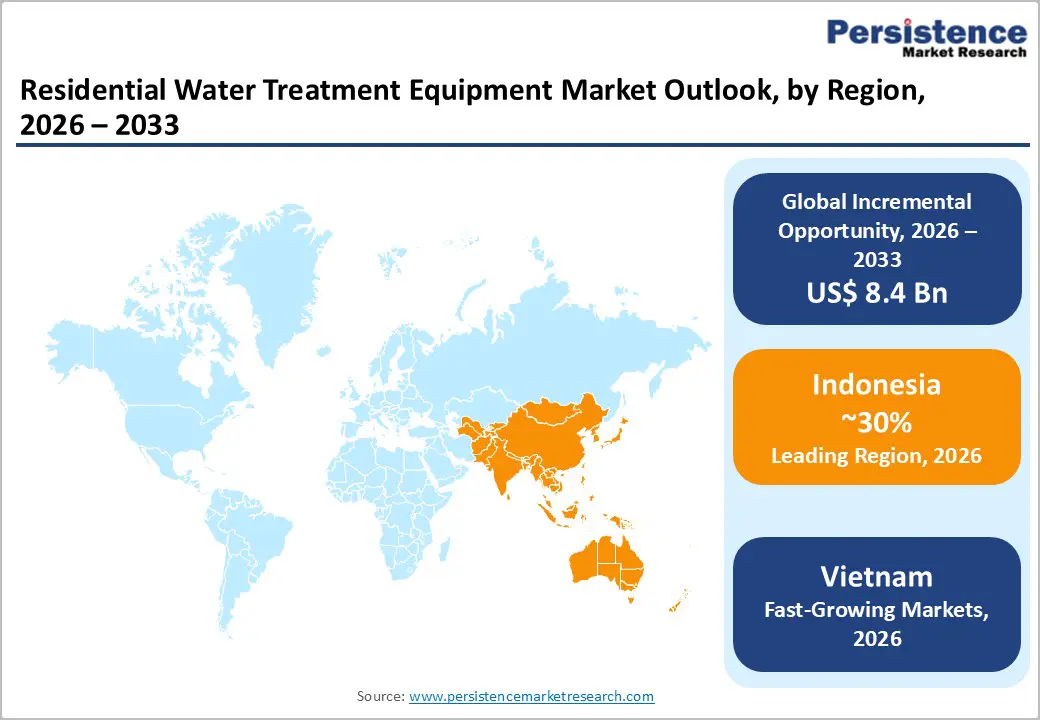

- Leading Country: Indonesia dominates the Southeast Asia residential water treatment equipment market, commanding 30.4% regional market share, driven by widespread water quality challenges, with approximately 70% of surface water unsafe for human consumption, and a transformative government.

- Fastest-Growing Country: Vietnam and the Philippines collectively represent the fastest-growing Southeast Asian subregions, with robust 8-10% annual growth in residential water treatment equipment adoption.

- Dominant Product Type: Reverse Osmosis technology maintains overwhelming market dominance within the Southeast Asia residential water treatment equipment sector, commanding approximately 55% market share in 2026.

- Growing Product Type: Point-of-Entry whole-house water treatment systems represent the fastest-growing installation category, with a projected 10-12% CAGR through 2032, driven by escalating consumer desire to protect household plumbing infrastructure, water-dependent appliances, including washing machines and dishwashers.

- Key Market Opportunity: Smart Water Treatment System Integration and IoT-Enabled Connected Device Proliferation represents the paramount market opportunity for manufacturers through 2033, as exponential growth in smart home adoption, increasing consumer digitization comfort, and technological maturation of IoT platforms.

| Key Insights | Details |

|---|---|

|

Southeast Asia Residential Water Treatment Equipment Market Size (2026E) |

US$ 1.8 Bn |

|

Market Value Forecast (2033F) |

US$ 3.1 Bn |

|

Projected Growth CAGR (2026-2033) |

8.2% |

|

Historical Market Growth (2020-2025) |

7.5% |

Market Dynamics

Market Growth Drivers

Escalating Waterborne Disease Prevalence and Health Awareness

Growing consumer awareness of contaminated water sources and the associated health risks is a primary market catalyst. Recent data from ASEAN health surveillance systems show rising cases of flood-associated waterborne diseases in Indonesia, Malaysia, Thailand, and Singapore from 2022 to 2025. The prevalence of bacterial pathogens ,including Escherichia coli, Aeromonas species, and antibiotic-resistant microorganisms in Southeast Asian water systems has intensified consumer perception of water safety risks.

Government health campaigns promoting clean water use and greater awareness of waterborne illnesses such as cholera, typhoid, and leptospirosis have led to heightened demand for residential water treatment equipment. Consumer education initiatives highlighting the relationship between untreated water and communicable diseases have positioned water purifiers from premium brands like Kent RO Systems and Eureka Forbes as essential household appliances rather than luxury items, thereby catalyzing widespread adoption across both urban and semi-urban residential segments.

Rapid Urbanization and Municipal Water Infrastructure Challenges

Accelerating urbanization across Southeast Asia, with 3% annual growth rates according to World Bank assessments, is driving exponential demand for decentralized water treatment solutions. Urban centers, including Bangkok, Jakarta, Manila, and Ho Chi Minh City, are experiencing unprecedented population concentrations that strain aging municipal water distribution infrastructure. The combination of industrial pollution, inadequate sewage treatment facilities, and contamination from urban development has compromised conventional tap water quality in metropolitan areas.

This infrastructure deficit has created compelling market opportunities for point-of-use filtration systems, which offer households immediate access to safe drinking water without awaiting government infrastructure improvements. Nations such as Vietnam, Indonesia, and the Philippines are experiencing particularly acute urban water quality challenges, driving residential consumers to invest in advanced purification technologies, including reverse osmosis and ultraviolet disinfection systems, as complementary solutions to municipal water supplies.

Market Restraints

High Capital and Maintenance Cost Barriers

The elevated initial investment requirements and substantial ongoing maintenance expenditures associated with advanced water treatment systems present significant obstacles to market penetration, particularly in price-sensitive segments. Reverse osmosis systems with integrated ultraviolet and ultrafiltration stages command premium price points ranging from $300 to $1,500, positioning these technologies beyond the financial reach of low-income households in rural and semi-urban areas across Southeast Asia. Beyond initial equipment costs, recurring expenses for filter cartridge replacements, routine servicing, and electricity consumption for operation accumulate to represent 15-25% of total lifecycle expenses annually.

The Asian Development Bank reports that rural households in Bangladesh and Myanmar face severe funding constraints that indefinitely delay the adoption of residential water purification systems. This cost impediment has effectively segmented the market between affluent urban consumers who can sustain premium purifier investments and economically disadvantaged populations who continue relying upon untreated or minimally treated water sources despite documented health risks.

Counterfeit Product Proliferation and Regulatory Fragmentation

The proliferation of substandard and counterfeit water purification products across Southeast Asian markets represents a critical restraint to legitimate market growth. Price-sensitive consumers in rural regions frequently purchase low-cost purifiers that fail basic safety standards, creating consumer health hazards while simultaneously eroding confidence in the product category. ASEAN member states currently lack harmonized technical standards for water and sanitation, enabling manufacturers and importers to circumvent stringent quality requirements by operating across jurisdictional boundaries. This regulatory fragmentation increases complexity and compliance costs for multinational manufacturers while simultaneously enabling non-compliant producers to flood cost-sensitive markets with substandard equipment.

Limited public awareness of quality certifications and performance standards enables counterfeit products to capture market share that would otherwise accrue to established brands such as Panasonic and LG Electronics. The absence of coordinated enforcement mechanisms across ASEAN member states has constrained efforts by legitimate manufacturers to eliminate substandard competition and establish quality-based market differentiation.

Market Opportunities

Rural Electrification Integration and Decentralized Water Treatment Expansion

Significant investment in rural electrification infrastructure across Southeast Asian economies is creating unprecedented opportunities for compact and energy-efficient residential water treatment solutions in previously underserved communities. Vietnam, Indonesia, and the Philippines are implementing comprehensive rural electrification projects that simultaneously extend reliable electricity access to remote households, thereby enabling deployment of electrically powered reverse osmosis and ultraviolet purification systems. Emerging demand for decentralized and scalable water treatment technologies in rural settings aligns with ongoing infrastructure development initiatives, creating potential for substantial volume growth in gravity-based filters, portable purification units, and solar-powered treatment systems.

Innovations in lightweight and affordable purifier designs from manufacturers such as A.O. Smith (following the 2024 acquisition of Pureit from Unilever for approximately $120 million) have dramatically improved accessibility for budget-conscious rural consumers. The convergence of rural electrification expansion and technological innovations in affordable purification systems positions manufacturers to capture high-volume sales opportunities in Southeast Asian rural markets, where population bases exceed 150 million individuals currently lacking reliable access to treated drinking water.

E-Commerce Expansion and Direct-to-Consumer Service Model Proliferation

The rapid acceleration of e-commerce adoption across Southeast Asia, coupled with emerging direct-to-consumer service models featuring subscription-based filter replacement, represents a transformative market opportunity for residential water treatment manufacturers. Digital platforms, including Shopee, Lazada, and localized e-commerce marketplaces, have fundamentally altered distribution economics by enabling manufacturers to bypass traditional retail intermediaries and engage consumers directly through online channels. Eureka Forbes expanded its direct-to-consumer presence in India during February 2025 by introducing subscription-based filter replacement services bundled with smart purifiers featuring WiFi connectivity and automated filter life alerts. This business model innovation addresses the persistent consumer frustration regarding filter maintenance complexity and cost unpredictability while simultaneously generating recurring revenue streams for manufacturers.

Rising internet penetration, improved logistics infrastructure, and growing consumer confidence in online shopping have created favorable conditions for scaling direct-to-consumer operations across metropolitan and emerging urban centers throughout Southeast Asia. Manufacturers who successfully leverage e-commerce platforms and develop integrated digital service ecosystems can achieve rapid market penetration while establishing direct consumer relationships that enhance brand loyalty and generate valuable customer usage data for product optimization.

Category-wise Insights

Equipment Type Analysis

Reverse osmosis technology maintains dominant market positioning within the Southeast Asia residential water treatment equipment market, commanding approximately 55% market share in 2024, according to industry assessments. This segment's leadership reflects the superior efficacy of RO systems in removing dissolved impurities, heavy metals, chemical contaminants, and microbiological pathogens that characterize water quality challenges across the region. Regions with exceptionally high total dissolved solids (TDS) concentrations, particularly in arid areas of Southeast Asia, exhibit pronounced demand for RO technology due to its unmatched ability to address saline and brackish water conditions.

Innovations in energy-efficient RO membrane design and declining equipment costs have expanded access to RO purifiers for middle-income households, sustaining the segment's dominant market position. Leading manufacturers, including Kent RO Systems, Eureka Forbes, and LG Electronics, have concentrated product development investments on RO technology enhancements, further solidifying this segment's market supremacy and justifying a continued growth trajectory.

Installation Type Analysis

Point-of-use (POU) filtration systems retain the dominant market position within the Southeast Asia residential water treatment equipment sector, commanding approximately 80% of residential installations through 2024. This overwhelming market preference reflects the accessibility, affordability, and installation simplicity of POU systems, which require minimal or no professional installation while delivering immediate improvements in drinking water quality. Countertop and under-sink POU filter configurations address the prevalent consumer preference for decentralized water treatment solutions in rental accommodations and residential spaces with constrained modification flexibility. The rapid growth of smart POU systems featuring IoT connectivity, exemplified by LG Electronics' March 2025 introduction of ThinQ AI platform-integrated purifiers and Coway's Icon Pro water purifier with full-screen LCD displays, has elevated POU segment attractiveness among digitally aware consumers.

Point-of-entry (POE) whole-house treatment systems are emerging as the fastest-growing installation category, driven by growing consumer interest in protecting household plumbing infrastructure, water-dependent appliances, and ensuring water quality for non-drinking applications. POE systems' capability to address entire-home water quality simultaneously, combined with technological advances enabling compact and cost-effective whole-house solutions, positions this segment for sustained above-market growth rates approaching 10-12% CAGR through 2033.

Country Insights

Indonesia Residential Water Treatment Equipment Trends

Indonesia represents the largest market in Southeast Asia for residential water treatment equipment, driven by its large population, uneven municipal water quality, and rising urbanization. Many households rely on groundwater and decentralized water sources, which increases demand for filtration systems, RO purifiers, and point-of-use treatment solutions. Growing health awareness, middle-class expansion, and concerns over waterborne diseases are accelerating adoption, particularly in urban and peri-urban areas. While bottled water remains prevalent, cost and sustainability concerns are pushing consumers toward in-home purification systems. The market is supported by increasing retail availability and local assembly of affordable systems, positioning Indonesia as the volume-dominant market in the region.

Vietnam Residential Water Treatment Equipment Trends

Vietnam is one of the fastest growing markets for residential water treatment equipment in Southeast Asia, supported by rapid urban development, industrial pollution concerns, and declining surface and groundwater quality. Rising household incomes and heightened awareness of water contamination issues—such as heavy metals and agricultural runoff—are driving strong demand for RO, UV, and multi-stage filtration systems. Urban households increasingly view water purifiers as essential appliances rather than discretionary products. Growth is further supported by expanding modern retail channels and e-commerce penetration, making Vietnam a high-CAGR market within the regional landscape.

Malaysia Residential Water Treatment Equipment Trends

Malaysia represents a moderately developed and stable market, characterized by relatively high household awareness of water quality and established adoption of residential filtration systems. Although municipal water coverage is widespread, concerns around aging infrastructure, water interruptions, and sediment contamination sustain demand for under-sink and countertop filtration units. Malaysian consumers show a preference for branded, mid- to premium-range products, including RO and alkaline water systems. Growth is steady rather than rapid, driven primarily by replacement demand and upgrades, positioning Malaysia as a mature, value-driven market within Southeast Asia.

Singapore Residential Water Treatment Equipment Trends

Singapore is a highly developed but low-growth market for residential water treatment equipment, supported by strong public water infrastructure and stringent national water quality standards. Adoption of residential water treatment systems is largely discretionary, driven by lifestyle preferences rather than necessity. Consumers favor compact, premium filtration systems focused on taste improvement, mineral enhancement, and convenience rather than basic purification. High household incomes and strong brand awareness support premium pricing, but limited population growth and excellent municipal water quality constrain volume expansion. As a result, Singapore remains a niche, premium-focused market within the region.

Competitive Landscape for the Residential Water Treatment Equipment Market

The Southeast Asia residential water treatment equipment market exhibits pronounced fragmentation at the regional level despite significant consolidation at the global manufacturer level. International premium manufacturers including Panasonic, LG Electronics, Koninklijke Philips, and A.O. Smith exercise dominant influence through technologically advanced product portfolios and substantial distribution networks, commanding approximately 35-40% cumulative market share in urban metropolitan segments. Domestically positioned manufacturers including Kent RO Systems and Eureka Forbes maintain substantial market presence through superior distribution channel development, localized product customization addressing regional water quality characteristics, and competitive cost positioning that resonates with middle-income consumers.

The 2024 acquisition of Pureit by A.O. Smith for approximately $120 million represents a strategic consolidation that significantly enhanced A.O. Smith's South Asian market penetration while simultaneously demonstrating continued acquisition activity within the sector. Market entrants from technology-oriented companies, exemplified by Coway's premium market positioning and recent design award accolades, are implementing differentiation strategies emphasizing smart connectivity, aesthetic design integration, and subscription-based service models. Emerging competitive dynamics prioritize research and development investments in membrane technology innovations, such as Philips' partnership with Aquaporin leveraging nature-inspired biomimetic filtration, alongside strategic geographic expansion into rapidly urbanizing Southeast Asian markets characterized by accelerating consumer purchasing power.

Key Market Developments

- In January 2025, Eureka Forbes introduced its advanced Aquaguard water purifier series featuring proprietary Longlife Nanopore Filter technology offering extended operational life of up to two years without requiring filter replacement, significantly reducing maintenance costs and environmental waste from cartridge disposal compared to conventional RO systems requiring quarterly filter changes.

- In March 2025, LG Electronics unveiled a comprehensive portfolio of IoT**-connected smart water purifiers integrated with ThinQ AI platform capabilities, enabling remote monitoring, predictive maintenance scheduling, and energy consumption optimization through smartphone applications and voice command interfaces.

Companies Covered in Southeast Asia Residential Water Treatment Equipment Market

• Eureka Forbes

• Kent RO Systems Limited

• Panasonic Corp ADR

• LG Electronics

• HUL (Pureit)

• Koninklijke Philips N.V.

• Mitsubishi Rayon Cleansui Co. Ltd.

• P.T. Holland (Nazava)

• A.O. Smith

• Mazuma Thailand Co. Ltd.

• Tata Chemicals Limited

• BRITA GmbH

• Pentair PLC

• Coway Co., Ltd.

Frequently Asked Questions

The Southeast Asia residential water treatment equipment market is projected to reach US$ 3.1 billion by 2033, representing an 8.2% CAGR from the 2026 valuation of US$ 1.8 billion, driven by escalating waterborne disease concerns, rapid urbanization, and government clean water access initiatives.

The predominant demand drivers include the widespread prevalence of waterborne pathogens causing an estimated 500,000 annual deaths globally according to WHO data, rapid urbanization affecting 250 million Southeast Asian individuals, contamination of approximately 80% of regional river water according to UNEP assessments, and government initiatives.

Reverse Osmosis technology commands approximately 55% market share across the Southeast Asia residential water treatment equipment sector, attributed to its superior capability in removing dissolved impurities, heavy metals, chemical contaminants, and microbiological pathogens that characterize regional water quality challenges including elevated TDS concentrations and agricultural contamination.

Vietnam, Indonesia, and the Philippines collectively exhibit the fastest regional growth rates, characterized by 8-10% CAGR, driven by accelerating urbanization, rising middle-class purchasing power, expanding e-commerce infrastructure, and increasing consumer awareness of waterborne illness risks combined with government investments in water treatment infrastructure.

Smart Water Treatment System Integration and IoT-Enabled Connected Device Proliferation constitutes the paramount opportunity, as exemplified by Coway's Icon Pro award-winning smart purifier and LG Electronics' ThinQ AI platform integration, enabling manufacturers to differentiate offerings through connectivity features, remote monitoring capabilities, and predictive maintenance functionality while commanding premium pricing.

Leading market participants include Kent RO Systems Limited commanding over 5 million customer base, Eureka Forbes Limited operating as a trusted regional brand, LG Electronics and Panasonic Corporation representing premium international competition, A.O. Smith Corporation (following Pureit acquisition expanding regional presence), Coway Co. Ltd. emphasizing smart connectivity, and Koninklijke Philips N.V. partnering with Aquaporin for advanced membrane technology development.