- Telecommunications

- Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market

Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market Size, Share, and Growth Forecast, 2026 - 2033

Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market by Integration / Solution Type (Network Integration, OSS/BSS Integration, Cloud & Virtualization Integration, Security Integration, Data & API Integration, Misc.), Service Model (Managed Services, Professional Services, Support & Maintenance Services, Misc.), Deployment Mode (On Premise, Hybrid, Cloud), End User (Telecom Operators, Enterprises, Government & Public Sector, Misc.) and Regional Analysis for 2026 - 2033

Asia-Pacific, Latin America, and EMEA System Integration in the Telecommunication Market and Trends Analysis

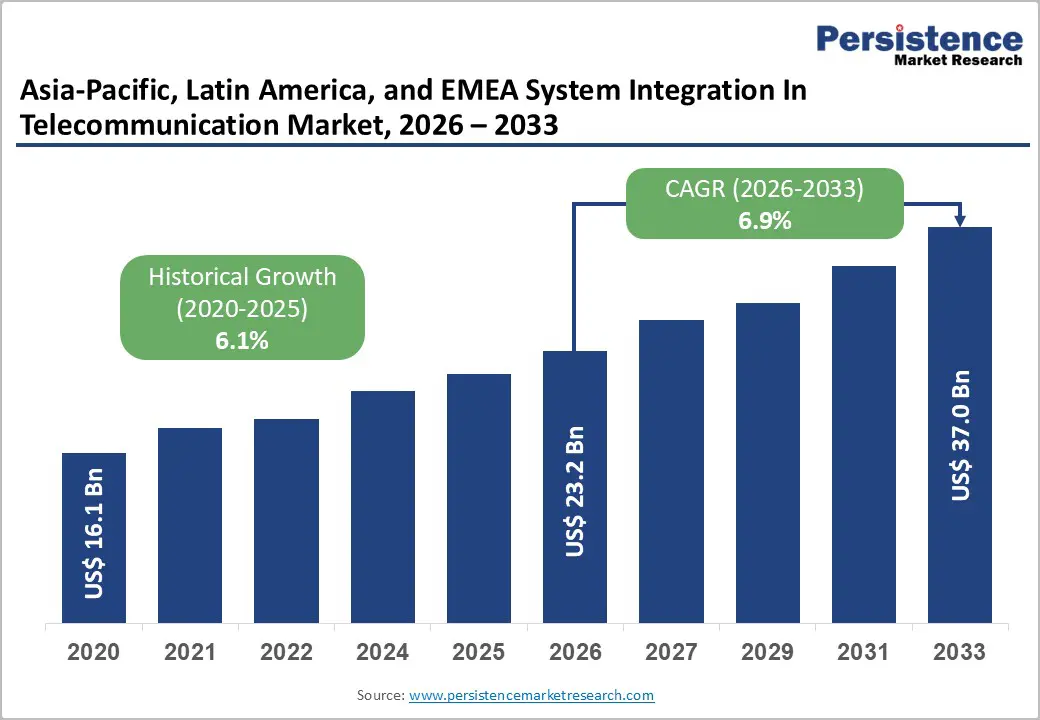

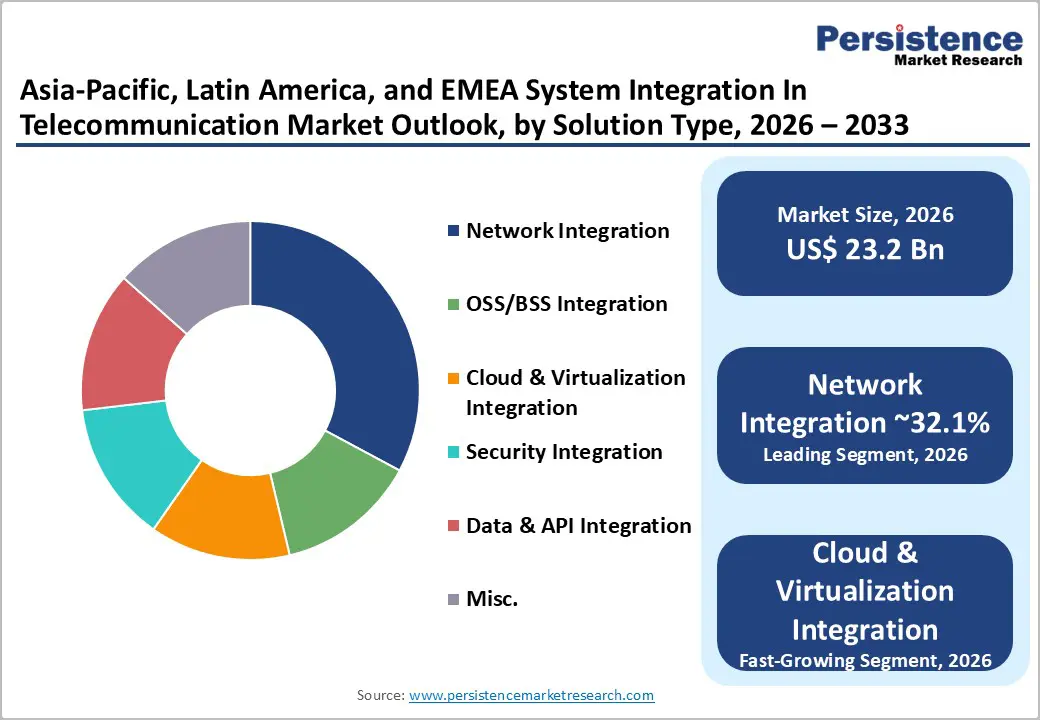

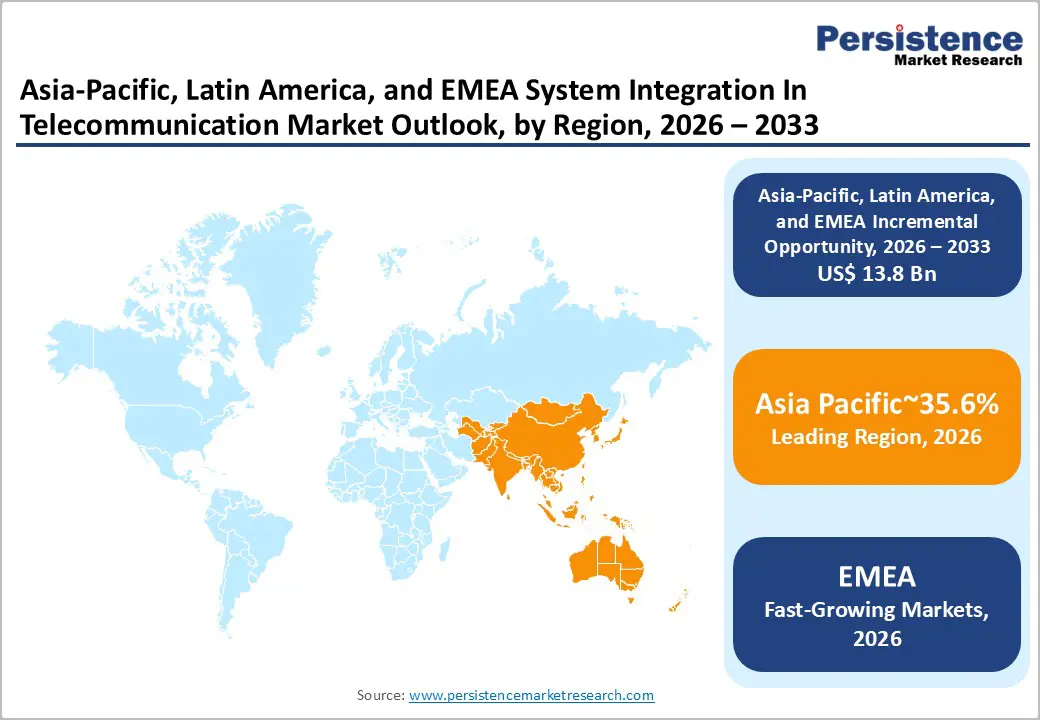

The Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market size was valued at US$ 23.2 billion in 2026 and is projected to reach US$ 37.0 billion by 2033, registering a CAGR of 6.9% between 2026 and 2033. Market expansion is primarily driven by large-scale 5G network deployments, widespread adoption of cloud and virtualisation solutions, and increasing demand for secure, high-performance optical backhaul infrastructure in telecom networks.

Enhanced digital inclusion policies, government-backed broadband projects, and the proliferation of mobile internet users across Asia-Pacific and EMEA underpin the sustained demand for integrated telecommunication services. A comparative analysis of performance from 2020 to 2026 reveals a steady recovery from pre-2020 infrastructure gaps, underscoring the sector's resilience.

Key Industry Highlights:

- Regional Leadership: Asia-Pacific leads the System Integration in Telecommunication Market with 45% share, driven by India’s 1.21B telecom subscribers, 979M internet users, China’s 1.108B internet users, and large-scale 5G and fiberization initiatives.

- Strong EMEA Market: EMEA holds 35% share, supported by 1.4M ICT enterprises generating €667B value added, high labour productivity (~€92,800/employee), and EU policies like GDPR, Digital Services Act, and Digital Decade investments.

- Latin America Presence: Latin America represents 20% of the market, with Brazil, Mexico, and Chile prioritising broadband access, OSS/BSS modernisation, and hybrid cloud integration, reinforced by ANATEL spectrum auctions and rural connectivity programs.

- Dominant Integration Segment: Network Integration leads with 32.1% share, reflecting its critical role in 5G orchestration, multi-vendor management, optical backhaul deployment, and end-to-end network operations.

- Fastest-Growing Integration Segment: Cloud & Virtualisation Integration is the fastest-growing segment, driven by OSS/BSS modernisation, hybrid-cloud adoption, and digital service platform integration across telecom and enterprise networks.

- Leading Service Model: Managed Services commands 44.4% share, reflecting operators’ preference for outcome-based end-to-end network management, while Professional Services expand rapidly, addressing cloud, Open RAN, and AI-enabled automation needs.

| Asia-Pacific, Latin America, and EMEA Market Attributes | Key Insights |

|---|---|

| System Integration in Telecommunication Market (2026E) | US$ 23.2 Bn |

| Market Value Forecast (2033F) | US$ 37.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Dynamics

Growth Drivers

5G Network Deployment Requirements

5G infrastructure rollout creates fundamental demand for system integration services within the Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market. Telecom operators deploy heterogeneous networks combining 4G LTE, 5G NR, and private networks requiring unified management platforms. India's telecom sector recorded 1.21 billion subscribers and 979 million internet users by June 2025, with 5G contributing 25 percent of wireless data usage in FY25 following 308,466 sites deployed by July 2023. China operates 4.6 million 5G base stations supporting 1.108 billion internet users as of December 2024 per CNNIC. Latin America launched 40+ commercial 5G networks across 13 countries by May 2024.

These deployments generate requirements for network orchestration, service assurance, and multi-domain integration across radio access, core, and transport layers. Operators require integration platforms supporting network slicing, edge computing, and real-time analytics to monetise 5G capabilities while maintaining service continuity during technology transitions.

Digital Services Platform Proliferation

Exponential growth in data-intensive digital services necessitates advanced OSS/BSS integration within the System Integration in Telecommunication Market. China's digital economy recorded 1.029 billion online payment users, 1.004 billion e-government users, and 974 million online shopping users by December 2024, alongside 249 million generative AI users. India demonstrates 20.27 GB monthly data consumption per user, up from 0.26 GB in 2014, with average costs declining 97 percent to INR 9.18/GB. EU households achieved 99 percent internet access in the Netherlands/Luxembourg by 2025, with 74 percent e-commerce penetration and 52 percent eID usage.

Telecom operators integrate these platforms with billing systems, customer care applications, and real-time charging engines to support dynamic pricing models and service bundling. Integration requirements span API management, data synchronisation across hybrid cloud environments, and compliance with regional data protection regulations.

Government Connectivity Infrastructure Programs

National broadband initiatives across Asia-Pacific, Latin America, and EMEA drive sustained demand for system integration services in the System Integration in Telecommunication Market. India's BharatNet project connected 2.13 lakh Gram Panchayats with optical fibre by 2024, targeting 42,000 additional under amended programs alongside 1.5 crore rural home connections. Brazil allocates US$1.2 billion through 2026 via Programa Internet Brasil for 22 million rural residents. EU Digital Decade policies mandate universal connectivity, with 94 percent individual internet usage recorded in 2025.

These programs require integration of rural base stations, satellite backhaul, and national fiber networks with urban core infrastructure. Integration services ensure seamless handovers, unified subscriber management, and centralised network monitoring across geographically dispersed deployments.

Market Restraining Factors

Legacy System Modernization Complexity

Monolithic OSS/BSS platforms deployed over 15-20 years create migration barriers within the System Integration in Telecommunication Market. Operators maintain revenue-critical systems managing billions of subscribers, where service interruptions cost millions daily. Technical debt accumulated through proprietary protocols and customised integrations requires 3–5-year replacement cycles averaging US$500M plus per Tier-1 operator. Integration projects face 30-40 percent scope creep from undocumented dependencies, delaying ROI realisation.

Regulatory Fragmentation and Compliance Complexity

The divergent regulatory landscapes across Asia-Pacific, Latin America, and EMEA create substantial operational and compliance barriers for system integration service providers. India's telecommunications regulations, China's state-owned operator dynamics, and the varying licensing frameworks across Southeast Asian nations present distinct integration challenges requiring customized solutions.

Europe's GDPR, Digital Services Act, and data sovereignty requirements impose stringent architectural constraints on system design, necessitating localized infrastructure deployment and enhanced security controls that substantially increase implementation costs. Latin America's fragmented regulatory environment, with varying spectrum allocation policies, infrastructure sharing mandates, and national security requirements across Brazil, Mexico, Colombia, and Peru, forces integration providers to develop region-specific capabilities, limiting scalability and compressing margins across the System Integration in Telecommunication Market.

Key Market Opportunities

Private 5G Networks for Industrial Applications

Private 5G deployments targeting manufacturing, mining, and logistics create integration opportunities within the Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market. Enterprises require dedicated network slices supporting ultra-reliable low-latency communications (URLLC) for robotics and massive machine-type communications (mMTC) for IoT sensor networks.

India's Smart Cities Mission integrates IoT platforms across 100 cities requiring enterprise-grade network integration. China's Made in China 2025 initiative deploys private 5G across 200-plus industrial parks. Operators partner with system integrators to deliver turnkey solutions combining private core networks, multi-tenancy platforms, and industry-specific applications, generating recurring managed services revenue over 7 to 10 year contracts.

Open RAN Architecture Adoption

Open RAN standardisation breaks vendor lock-in, creating system integration opportunities within the Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market. Operators achieve 30-40 percent capex reduction through disaggregated architecture while accessing best-of-breed components across multiple vendors.

Vodafone/NTT Docomo collaborations establish interoperability frameworks for O-RAN compliant deployments. Latin American operators leverage open RAN towers in Peru's Internet Para Todos covering 6,500 villages. Integration services focus on orchestration platforms, zero-touch automation, and multi-vendor service assurance, positioning specialist integrators as essential partners in next-generation network transformations.

Category-wise Analysis

Integration / Solution Type Insights

Network Integration leads with 32.1% share in 2026 due to its foundational role in 5G deployments. Operators require unified management across radio access networks, packet core, and transport layers supporting network slicing and dynamic service orchestration. India's 308,466 5G sites and China's 4.6M base stations generate sustained demand for multi-vendor integration platforms ensuring seamless handovers and quality-of-service guarantees.

Cloud & Virtualization Integration represents the fastest-growing segment driven by OSS/BSS modernization. Operators migrate 62.8 percent of managed services to cloud-native deployments requiring container orchestration, microservices integration, and hybrid-cloud connectivity. EU telecoms leverage €667B ICT value added for virtualization projects supporting 94%percent internet penetration recorded in 2025.

Service Model Insights

Managed Services command 44.4% share in 2026 reflecting operators' preference for outcome-based contracts. Providers assume end-to-end responsibility for network operations, fault management, and performance optimization across 1.21B Indian subscribers and 1.108B Chinese internet users. Standardization enables scale economies across multi-country footprints.

Professional Services exhibit the fastest growth addressing skills gaps in cloud-native architectures and Open RAN deployments. Operators engage specialists for 5G core design, network slicing implementation, and AI-driven automation. India's Digital India schemes create demand for implementation expertise across 246 BPO units.

End User Insights

Telecom Operators dominate with 63.4% share in 2026, representing primary customers for network modernization. Tier-1 operators manage multi-billion subscriber bases requiring integration across hybrid IT environments. India's US$43.42B telecom revenue (FY25) and the EU's €667B ICT value sustain carrier-led investments

Enterprises drive fastest growth through private 5G and IoT integration requirements. Manufacturing sectors deploy dedicated network slices for Industry 4.0 applications. China's 313M rural internet users enable agricultural IoT, while EU generative AI usage fuels enterprise analytics platforms.

Regional Insights and Trends

Asia Pacific Market Trend

Asia-Pacific holds 45% of the System Integration in Telecommunication Market share, propelled by extensive 5G network rollouts, nationwide fiber optic infrastructure deployments, and accelerated mobile broadband network expansions. India and China serve as key engines of regional growth, with India recording 1.21 billion telecom subscribers, 979 million internet users, and gross telecom revenue of US$ 43.42 billion in FY25, while China supports 1.108 billion internet users, reflecting massive digital adoption.

Government initiatives, such as India’s BharatNet program and China’s gigabit fiber infrastructure, are accelerating rural connectivity, urban network densification, and high-capacity optical backhaul deployment, creating significant opportunities for system integrators. Regulatory measures, including TRAI mandates for infrastructure sharing and 100% FDI through the automatic route, have attracted US$ 40.07 billion in cumulative investment, reinforcing long-term capital inflows into network expansion.

The competitive landscape is marked by a mix of telecom operators like Reliance Jio and Bharti Airtel and IT/system integration leaders such as TCS and Infosys, who provide managed and professional services for complex integration projects. Strategic investment activities, including 5G spectrum auctions and continued FDI inflows, ensure sustained infrastructure development and digital transformation across the region through 2033, positioning Asia-Pacific as the dominant and most technologically advanced market for telecommunication system integration.

Latin America Market Trend

The Latin America System Integration in Telecommunication Market, accounting for 20% of the regional market, is shaped by government-led initiatives promoting broadband access, digital inclusion, and rural connectivity. Brazil drives the market with its US$ 1.2 billion Internet Brasil program, connecting 22 million rural users, while Colombia contributes US$ 650 million toward remote connectivity projects. By May 2024, over 40 operational 5G networks across 13 countries demonstrate the region’s commitment to next-generation infrastructure.

Regulatory mechanisms, including ANATEL spectrum auctions and fibre-to-home mandates, accelerate infrastructure deployment and create opportunities for system integrators to implement OSS/BSS modernisation, hybrid cloud adoption, and edge solutions. Major telecom operators and IT collaborations further enhance market capabilities companies such as TIM Brasil invested US$ 1.2 billion in 5G expansion, Telefónica partnered with Microsoft for edge computing, and América Móvil acquired Columbus Networks for US$ 580 million, expanding service coverage and integration potential. Additionally, Open RAN deployments in Peru, covering 6,500 villages, highlight emerging integration opportunities in underserved regions, positioning system integrators to deliver network, cloud, and virtualization services across enterprise and operator segments.

Europe Market Trend

Europe commands 35% share within the Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market, supported by robust digital transformation policies and ICT sector development across the European Union. The EU’s ICT sector comprises 1.4 million enterprises generating €667 billion in value added, with Germany alone contributing 22.8 percent of sectoral value added, reflecting concentrated telecom investment and strong deployment capacity in major economies.

High labor productivity facilitates complex system integration projects, while widespread digital adoption, including 94 percent internet usage in 2025 and 99 percent household access in the Netherlands, ensures sustained demand for infrastructure and services. Regulatory frameworks such as GDPR, the Digital Services Act, and the European Electronic Communications Code (EECC) drive investment in security integration, cloud virtualization, and data services. Major operators, including Vodafone, Deutsche Telekom, and Orange, alongside system integrators like Accenture and Capgemini, are actively participating in large-scale deployments. Strategic initiatives under the Digital Decade and emerging Open RAN programs channel over €200 billion into next-generation telecom infrastructure, creating substantial opportunities for system integrators to deliver comprehensive, compliant, and high-performance solutions across EMEA.

Competitive Landscape

The System Integration in Telecommunication market across Asia-Pacific, Latin America, and EMEA varies from consolidated to moderately fragmented, shaped by technological maturity, regulatory environments, and telecom investment levels. Asia-Pacific is largely consolidated-oligopolistic, dominated by major vendors executing 5G, cloud, and OSS/BSS integration for Tier-1 operators.

Latin America remains moderately fragmented, with cost-sensitive operators relying on both local and global integrators for modernization, cloud migration, and multi-vendor network integration. EMEA skews oligopolistic to consolidated, particularly in Western Europe and the Middle East, where high-value telco cloud, cybersecurity, and automation projects favour top-tier integrators. Across these regions, leading players such as Ericsson, Nokia, Huawei, IBM, Wipro, Capgemini, and Tech Mahindra maintain a strong competitive presence due to telecom domain expertise and strategic operator alliances.

Key Industry Developments

- Oct 15, 2025 – Bharti Airtel & IBM announced a strategic partnership to enhance Airtel Cloud with IBM’s hybrid and AI-ready cloud technologies, enabling interoperability across on-premises, multi-cloud, and edge environments. The collaboration supports integration of mission-critical enterprise workloads such as SAP Cloud ERP on IBM Power, strengthening Airtel’s telecom-cloud ecosystem for regulated industries. This development reflects the growing convergence of telecom and cloud system integration capabilities to serve enterprise digital transformation needs.

- Oct 07, 2025 – Telstra & Ericsson announced a collaboration to accelerate the telecom industry's shift toward autonomous networks, focusing on overcoming integration challenges across multi-vendor environments. The initiative includes developing intent-translation frameworks, trustworthy AI, and a knowledge plane to enhance intelligent network control. The program aims to validate real-world use cases and set industry standards that support large-scale telecom system integration and automation.

Companies Covered in Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market

- Ericsson

- Wipro

- Nokia Networks

- Huawei

- IBM

- Tech Mahindra

- Infosys

- DXC Technology

- Cognizant

- Syntel

- ZTE

- TCS

- Amdocs

- Samsung

- HCL

- Sitixis Technologies

Frequently Asked Questions

The Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market is projected to be valued at US$ 23.2 Bn in 2026.

The Managed Services segment is expected to account for approximately 44.5% of the Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market by Component in 2026.

The Asia-Pacific, Latin America, and EMEA market is expected to witness a CAGR of 6.9% from 2026 to 2033.

The Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market growth is driven by large-scale 5G network deployments, proliferation of data-intensive digital services requiring OSS/BSS integration, and government-led connectivity infrastructure programs across Asia-Pacific, Latin America, and EMEA.

Key market opportunities in the Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication Market include private 5G networks for industrial applications and the adoption of Open RAN architectures, enabling multi-vendor integration and turnkey enterprise solutions.

Key players in the Asia-Pacific, Latin America, and EMEA System Integration in Telecommunication include Ericsson, Wipro, Nokia Networks, Huawei, IBM, and Tech Mahindra.