- Advanced Materials

- Asia Pacific Metallic Stearate Market

Asia Pacific Metallic Stearate Market Size, Share, and Growth Forecast 2026 - 2033

Asia Pacific Metallic Stearate Market by Product Type (Zinc Stearate, Calcium Stearate, Aluminum Stearate, Sodium Stearate, Others), End-use Industry (Plastic & Rubber, Pharmaceutical, Cosmetics, Construction, Others), and Regional Analysis for 2026 - 2033

Asia Pacific Metallic Stearate Market Size and Trend Analysis

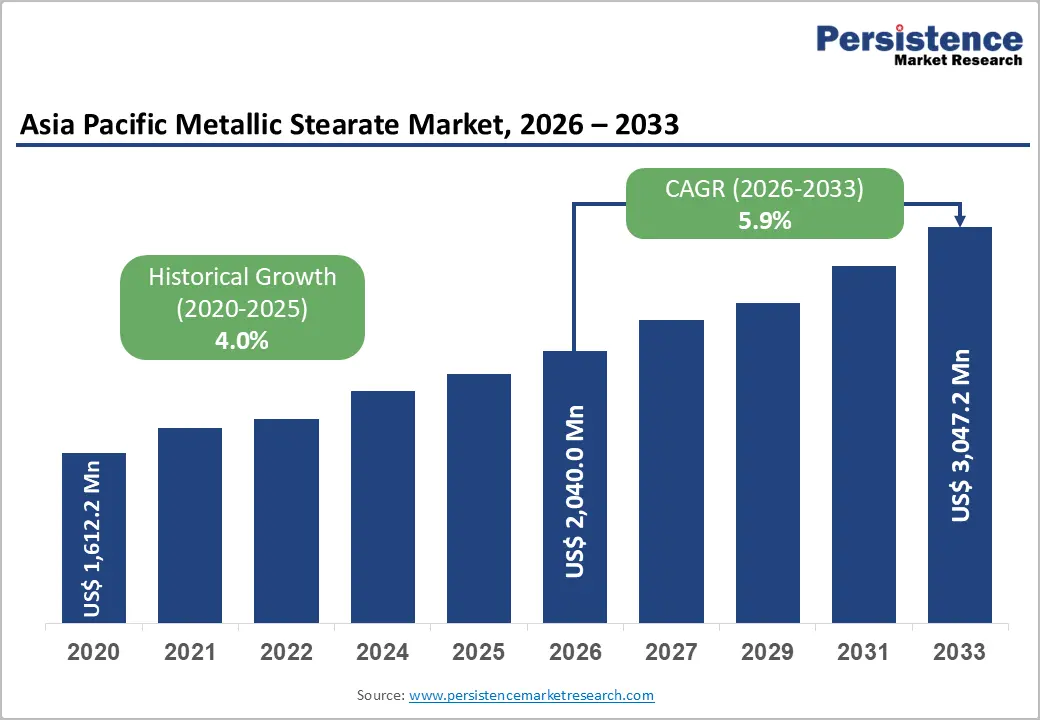

The Asia Pacific metallic stearate market is valued at US$ 2,040.0 Mn in 2026 and is projected to reach US$ 3,047.2 Mn by 2033, growing at a CAGR of 5.9% between 2026 and 2033. The sustained expansion of the plastics, rubber, pharmaceutical, and personal care industries across the region is the primary driver of market growth.

Asia Pacific's position as the world's largest plastics production hub, with China alone accounting for approximately one-third of global primary plastic output, creates substantial and consistent demand for metallic stearates as lubricants, release agents, and stabilizers. Simultaneously, the rapid expansion of generic pharmaceutical manufacturing, particularly in India and South Korea, is escalating the consumption of high-purity calcium and zinc stearates as tablet excipients. Robust urbanization, government-backed infrastructure programs, and rising consumer spending on personal care products further reinforce demand over the forecast period.

Key Industry Highlights:

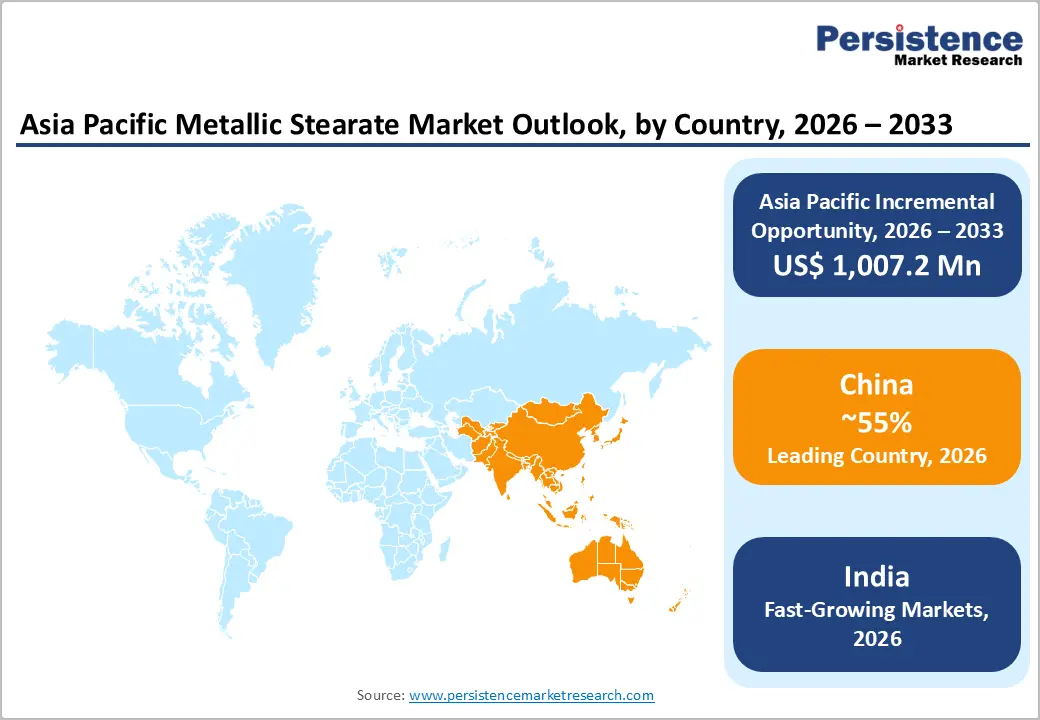

- Leading Country: China leads the Asia Pacific metallic stearate market, with 55% market share of the region, supported by the world's largest plastics production base and extensive rubber, cosmetics, and construction manufacturing activity.

- Fastest Growing Country: India is the fastest-growing country market, propelled by rapid pharmaceutical sector expansion and government-backed manufacturing investment programs, including the PLI Scheme and Bulk Drug Parks.

- Dominant Segment: Zinc Stearate dominates the product type category with approximately 32% revenue share, attributed to its superior mold-release properties, thermal stability, and non-toxic nature, making it the preferred additive in PVC, polyolefin, rubber, and cosmetics manufacturing.

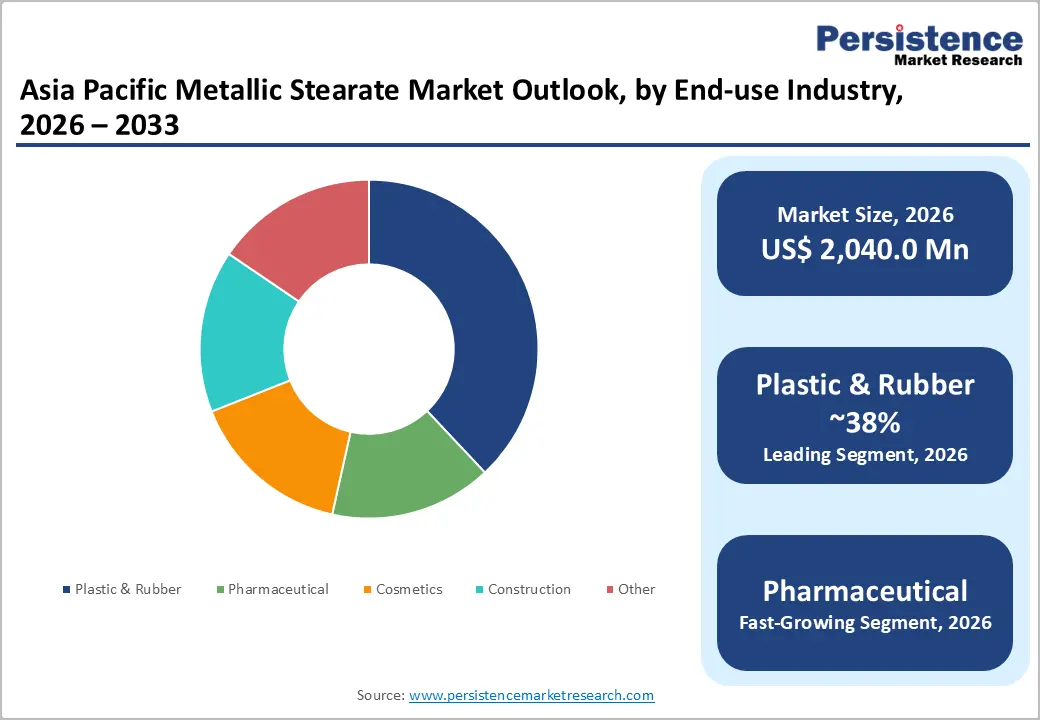

- Fastest Growing Segment: Pharmaceutical is the fastest growing end-use segment, driven by the exponential growth of generic drug manufacturing in India and China and rising demand for pharmacopeia-compliant excipients, including calcium and magnesium stearate in tablet formulations.

- Key Market Opportunity: Bio-based and eco-friendly metallic stearates represent a high-value growth opportunity as multinational buyers increasingly mandate sustainable supply chains, with vegetable-derived calcium stearate lines and low-dust dispersion formats gaining commercial traction across the Asia Pacific.

| Key Insights | Details |

|---|---|

| Asia Pacific Metallic Stearate Market Size (2026E) | US$ 2,040.0 Mn |

| Market Value Forecast (2033F) | US$ 3,047.2 Mn |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 4.0% |

DRO Analysis

Drivers - Expanding Plastics and Polymer Processing Industry Across the Asia Pacific

The extensive scale of plastics manufacturing across the Asia Pacific region represents the primary driver of demand for metallic stearates. China has maintained an average annual growth rate in primary plastics production of over 5.14% between 2020 and 2024, sustaining a global production share of approximately 33%, while output growth in 2025 exceeded 11%, outpacing prior projections. Metallic stearates, particularly zinc and calcium stearates, are essential processing additives used in polyvinyl chloride (PVC), polyethylene (PE), polypropylene (PP), and other thermoplastics to enhance thermal stability, surface finish, and mold-release efficiency.

Growing production of new-energy vehicle components, consumer electronics enclosures, and smart home appliances is further strengthening demand for advanced polymer additives. Moreover, the ongoing relocation of manufacturing capacity to Southeast Asia, including Vietnam, Thailand, and Indonesia, is broadening the regional footprint of plastics processing and expanding market opportunities for metallic stearate suppliers.

Rapid Growth of the Pharmaceutical Sector and Rising Demand for Excipients

The pharmaceutical industries of India, China, and South Korea are generating substantial incremental demand for pharmaceutical-grade metallic stearates, particularly magnesium and calcium stearates used as essential excipients and lubricants in tablet manufacturing. India’s pharmaceutical sector achieved a market value of US$ 55 billion in 2025, with exports rising to US$ 30.47 billion in FY 2024-25, underscoring the country’s growing global manufacturing prominence.

Furthermore, India’s Production Linked Incentive (PLI) Scheme for bulk drugs, with an investment outlay of Rs. 15,000 crore, is significantly enhancing API and formulation manufacturing capacity, thereby accelerating excipient consumption and providing sustained growth momentum for the metallic stearate market.

Restraints - Volatility in Raw Material Prices

Metallic stearates are manufactured primarily from stearic acid, derived from palm kernel oil and animal fats, and metal oxides of zinc, calcium, and aluminum. Palm kernel oil prices are subject to significant volatility driven by weather disruptions, export policy shifts in key producing nations such as Indonesia and Malaysia, and global commodity cycles.

Simultaneous fluctuations in metal commodity prices further compound manufacturers' input cost unpredictability. This double exposure to price swings directly compresses profit margins, particularly for small and medium-sized enterprises, reduces competitive pricing flexibility, and hampers procurement planning for downstream users in pharmaceuticals, plastics, and rubber sectors.

Regulatory Complexity and Shift Away from Lead-Based Stabilizer Systems

Tightening environmental regulations across the Asia Pacific region, particularly prohibitions on lead-based PVC stabilizers in China, South Korea, and Japan, are requiring manufacturers to transition toward calcium-zinc stabilizer systems. Although this regulatory shift ultimately expands long-term demand for metallic stearates, it introduces interim challenges for industry participants.

Manufacturers face formulation disruptions, elevated compliance costs, and increased capital investment as they are compelled to redesign, test, and validate alternative stabilizer technologies. In addition, the adoption of REACH-equivalent chemical control frameworks across several Asia Pacific economies is intensifying regulatory complexity.

Opportunities - Rising Demand for Bio-Based and Eco-Friendly Metallic Stearates

As sustainability increasingly shapes procurement priorities across industries in the Asia Pacific region, the development and commercialization of bio-based metallic stearates represent a significant revenue opportunity for market participants. Conventional palm-oil-derived stearates are facing growing scrutiny due to concerns over deforestation, prompting interest in alternatives produced from non-food vegetable oils and biosynthetic stearic acid. These bio-based solutions are gaining traction across plastics, rubber, and personal care applications.

In November 2024, Peter Greven GmbH & Co. KG introduced a new range of vegetable-based, food-grade calcium stearates designed to meet more stringent regulatory requirements for food-contact packaging. This shift toward green chemistry is further reinforced by corporate sustainability commitments aligned with the United Nations Sustainable Development Goals and increasingly rigorous ESG reporting standards.

Expansion into High-Growth Southeast Asian Markets

Emerging economies within the Association of Southeast Asian Nations (ASEAN), notably Indonesia, Vietnam, Thailand, and the Philippines, are evolving into high-growth demand centers for metallic stearates. This growth is driven by the expanding scale of plastics compounding, rubber manufacturing for automotive components, and the gradual development of domestic capabilities in cosmetics and personal care production. Indonesia has historically been the largest metallic stearate market in Southeast Asia, supported by strong growth in construction materials and a well-established cosmetics industry.

In parallel, the relocation of global supply chains from China to Southeast Asia, accelerated by geopolitical factors and tariff realignments, is attracting sustained investment in polymer processing and rubber manufacturing. These structural shifts are directly increasing regional consumption of metallic stearates. Additionally, capacity expansions by global suppliers underscore the strategic importance of the broader Asia Pacific market in supporting long-term industry growth.

Category-wise Analysis

Product Type Insights

Among the various product types, zinc stearate holds a leading position in the Asia Pacific metallic stearate market, accounting for approximately 32% of total revenue. Its dominance is primarily attributable to its versatility and effectiveness as a mold release agent, internal lubricant, and stabilizer across the plastics and rubber industries, which are the region's largest consumption sectors. Zinc stearate exhibits superior functional characteristics, including a well-defined melting point that enables rapid liquefaction, hydrophobic and lipophilic properties, and a non-toxic profile, making it widely preferred in the processing of PVC, polyolefins, and rubber compounds.

Furthermore, it is extensively used in cosmetics and personal care applications as an emulsifier and thickening agent. Broad applicability across multiple industries, combined with large-scale manufacturing activity in China, India, and Vietnam, continues to support its market leadership. In contrast, calcium stearate is emerging as the fastest-growing segment due to regulatory-driven adoption of calcium-zinc stabilizer systems in place of lead-based alternatives.

Industry Insights

The plastic & rubber segment represents the largest end-use category in the Asia Pacific metallic stearate market, accounting for an estimated 38% of total demand. In this segment, metallic stearates, particularly zinc and calcium stearates, perform essential functions as internal and external lubricants, acid scavengers, anti-blocking agents, and mold-release additives during polymer processing. China’s position as the world’s largest plastics producer, with primary plastics output expanding at an annual rate exceeding 5.14% between 2020 and 2024, significantly reinforces consumption within this segment.

Continued growth in engineered plastics usage for lightweight automotive components, coupled with sustained demand from the packaging industry, further supports market expansion. In contrast, the pharmaceutical segment is emerging as the fastest-growing end-use industry, driven by the rapid scale-up of generic drug manufacturing in India, widely recognized as the “Pharmacy of the World”, along with expanding pharmaceutical production across South Korea, Japan, and China, resulting in rising demand for excipients.

Country-wise Insights

China Metallic Stearate Market Trends

China is the dominant country in the Asia Pacific metallic stearate market, with 55% of the regional market share, underpinned by its position as the world's largest producer and consumer of plastics, rubber, and related polymer materials. China's plastics sector recorded export revenues of approximately US$ 78 billion in the first three quarters of 2024 alone, reflecting the scale of domestic polymer manufacturing. The country's thriving cosmetics, construction, and coatings industries further diversify demand across product types, including zinc, calcium, and aluminum stearates.

China's emphasis on quality control, import substitution, and domestic chemical self-sufficiency, embedded in strategic plans such as "Made in China 2025", is driving investments in higher-purity metallic stearate production aligned with international standards. The trade environment shaped by ongoing U.S.-China tensions has had a mixed impact: while tariffs on specialty chemicals create cost pressures for imported raw materials, they also incentivize domestic production expansion.

India Metallic Stearate Market Trends

India represents the fastest-growing country market for metallic stearates in the Asia Pacific region, driven by concurrent expansion in pharmaceuticals, plastics compounding, personal care manufacturing, and construction. The Indian pharmaceutical sector constitutes the primary demand catalyst, given the essential use of calcium and magnesium stearates as excipients in generic tablet production.

Government initiatives such as the Production Linked Incentive (PLI) Scheme and the Bulk Drug Park Program, with a combined investment exceeding Rs. 15,000 crore, are strengthening domestic API and formulation capacity. In parallel, multinational investments, including Baerlocher GmbH’s capacity expansion in 2025, underscore India’s strategic importance as a global manufacturing and export hub for pharmaceutical-grade metallic stearates.

Japan Metallic Stearate Market Trends

Japan is the second-largest market for metallic stearates in Asia Pacific, supported by a highly advanced industrial ecosystem encompassing high-performance plastics, precision rubber components, pharmaceuticals, and premium cosmetics. The country’s globally recognized automotive industry, led by manufacturers such as Toyota Motor Corporation, Honda Motor Co., Ltd., and Nissan Motor Co., Ltd., generates consistent demand for metallic stearates in engineering plastics and rubber sealing applications.

Furthermore, Japan’s cosmetics and personal care sector, characterized by exceptionally stringent quality requirements, relies heavily on high-purity zinc and sodium stearates as rheology modifiers and thickeners. The regulatory framework, governed by the Pharmaceutical and Medical Device Act and the Chemical Substances Control Law, enforces rigorous safety and quality standards, creating a premium market environment. Japan’s early adoption of bio-based and low-dust dispersion metallic stearate technologies further reflects its strong commitment to sustainability, occupational health, and continuous manufacturing excellence.

Competitive Landscape

Asia Pacific metallic stearate market is moderately consolidated, with a small number of global specialty chemical leaders, including Baerlocher GmbH, Dover Chemical Corporation, Valtris Specialty Chemicals, and Peter Greven GmbH & Co. KG, commanding significant market shares alongside a fragmented tier of regional and local producers. Key differentiators among market leaders include breadth of product portfolio, regulatory compliance credentials, advanced manufacturing technologies such as low-dust pastille and aqueous dispersion formats, and proximity to key manufacturing clusters in China and India. Strategic priorities include capacity expansion in South and Southeast Asia, development of bio-based stearate lines, and growing pharmaceutical-grade product offerings.

Key Developments:

- May 2025: Baerlocher GmbH announced plans for a new MYR 220 million metallic stearate plant in Malaysia, targeting 30,000 TPA of Ca-Zn stearates. The plant is expected to be in operating condition by 2027.

- April 2025: Peter Greven GmbH & Co. KG launched a new bio-based magnesium stearate product range (LIGAMED® grades) derived from RSPO-certified palm oil for pharmaceutical tablet formulations.

- March 2023: Baerlocher GmbH increased production of calcium-based PVC stabilizers and metallic stearates by over 50% at its Bury (UK) facility to address recycled plastics demand.

Top Companies in Asia Pacific Metallic Stearate Market

- Baerlocher GmbH (Munich, Germany) is widely recognized as the global market leader in metallic stearates, estimated to hold approximately 10.5% of the global market share. The company operates a state-of-the-art manufacturing facility in Dewas, Madhya Pradesh, India, serving as the primary production hub for the APAC region. Its product portfolio spans the full range of metallic stearates across PVC stabilization, polymer processing, and specialty chemical segments, with a growing focus on dust-free pastille formats and bio-based innovations.

- Dover Chemical Corporation (Ohio, U.S.) is one of the most established producers of metallic stearates in the global market, with a comprehensive portfolio spanning zinc, calcium, aluminum, and sodium stearates. The company serves multiple end-use sectors, including plastics, rubber, pharmaceuticals, and personal care, offering products that comply with major global regulatory frameworks. Its strong technical service capabilities and long-standing presence in APAC distribution channels sustain its competitive positioning in the region.

- Valtris Specialty Chemicals (Ohio, U.S.) has emerged as a key supplier for pharmaceutical-grade stearates and PVC additive systems, capitalizing on the rapid growth of the generic drug market across the Asia Pacific. The company's focus on high-purity metallic stearate grades that meet USP and NF pharmacopeia standards positions it favorably among pharmaceutical manufacturers in India, China, and South Korea. Strategic research partnerships are reinforcing their innovation pipeline in next-generation stabilizer systems.

Companies Covered in Asia Pacific Metallic Stearate Market

- Dover Chemical Corporation

- Baerlocher GmbH

- Faci S.p.A.

- Valtris Specialty Chemicals

- Norac Additives LLC

- PMC Biogenix Inc.

- BASF SE

- Dow Inc.

- Solvay S.A.

- Peter Greven GmbH & Co. KG

- Nitika Pharmaceutical Pvt Ltd.

- Akrochem Corporation

Frequently Asked Questions

The Asia Pacific metallic stearate market is estimated to be valued at US$ 2,040.0 Mn in 2026, and is projected to reach US$ 3,047.2 Mn by 2033, reflecting a forecast CAGR of 5.9% during the period 2026-2033.

The primary demand drivers include the rapid expansion of the plastics and polymer processing industry, with China maintaining over 33% of global primary plastic production, and the surge in pharmaceutical manufacturing across India and South Korea, where metallic stearates are critical excipients in generic tablet formulation. Urbanization, infrastructure development, and rising personal care consumption across Southeast Asia further amplify market demand.

Zinc Stearate is the leading product type segment, accounting for approximately 32% of market revenue. Its dominance is supported by its superior mold-release and lubricating properties, non-toxic nature, and wide applicability across PVC, polyolefin, rubber, and cosmetics manufacturing, particularly in China, Vietnam, and Thailand, where plastics production is concentrated.

China is the leading country market with 55% market share, driven by its status as the world's largest plastics producer, and the strong presence of rubber, cosmetics, and construction manufacturing sectors. China's emphasis on quality control and domestic chemical capacity expansion further reinforces its market dominance.

Key opportunities include the development and commercialization of bio-based and eco-friendly metallic stearates in response to mounting sustainability mandates from multinational buyers, and strategic market expansion into fast-growing ASEAN economies such as Indonesia, Vietnam, and Thailand, where manufacturing relocation from China is catalyzing new demand for polymer additives, rubber processing aids, and specialty excipients.

The leading companies operating in the Asia Pacific metallic stearate market include Baerlocher GmbH, Dover Chemical Corporation, Valtris Specialty Chemicals, Peter Greven GmbH & Co. KG, Faci S.p.A., PMC Biogenix, Inc., Norac Additives LLC, BASF SE, Dow Inc., Solvay S.A., Seoul Fine Chemical Ind. Co., Ltd., Nitika Pharmaceutical Pvt Ltd., and Akrochem Corporation, among others.