- Plastics, Polymers & Resins

- Asia Pacific PE Woven Films Market

Asia Pacific PE Woven Films Market Size, Share, and Growth Forecast, 2025 - 2032

Asia Pacific PE Woven Films Market By Product Type (General, UV Stabilized), Material Type (Virgin PE, Reinforced PE), Application (Greenhouse Covers, Low Tunnels, Mulches, Grain and Silage Pile Covers), and Country Analysis for 2025 - 2032

Asia Pacific PE Woven Films Market Size and Trends Analysis

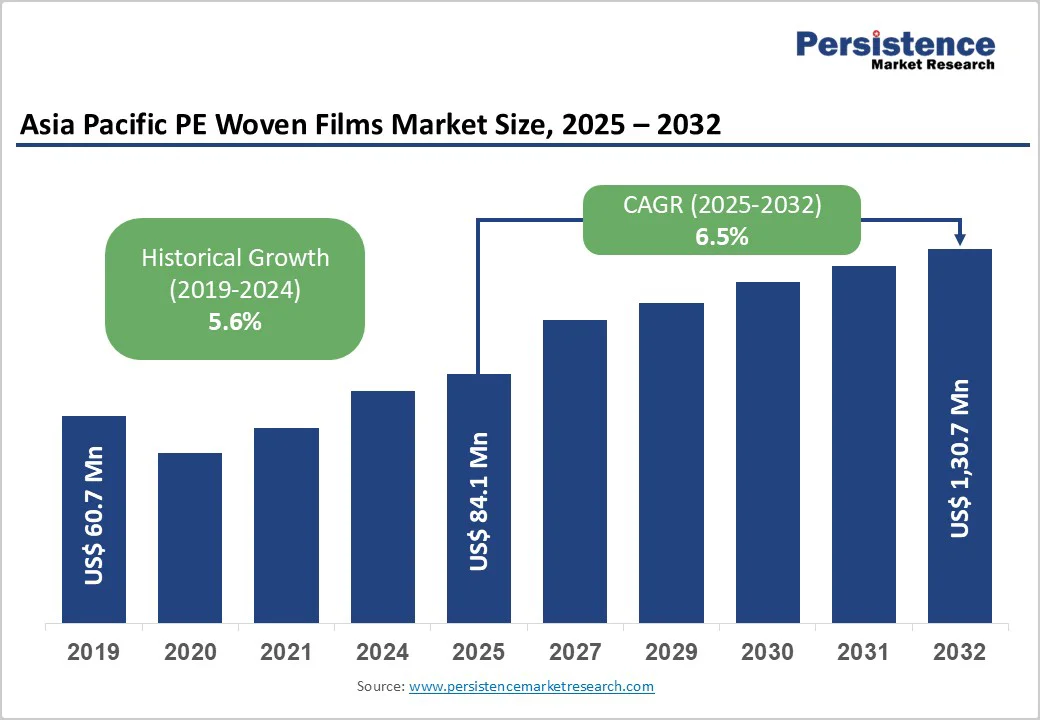

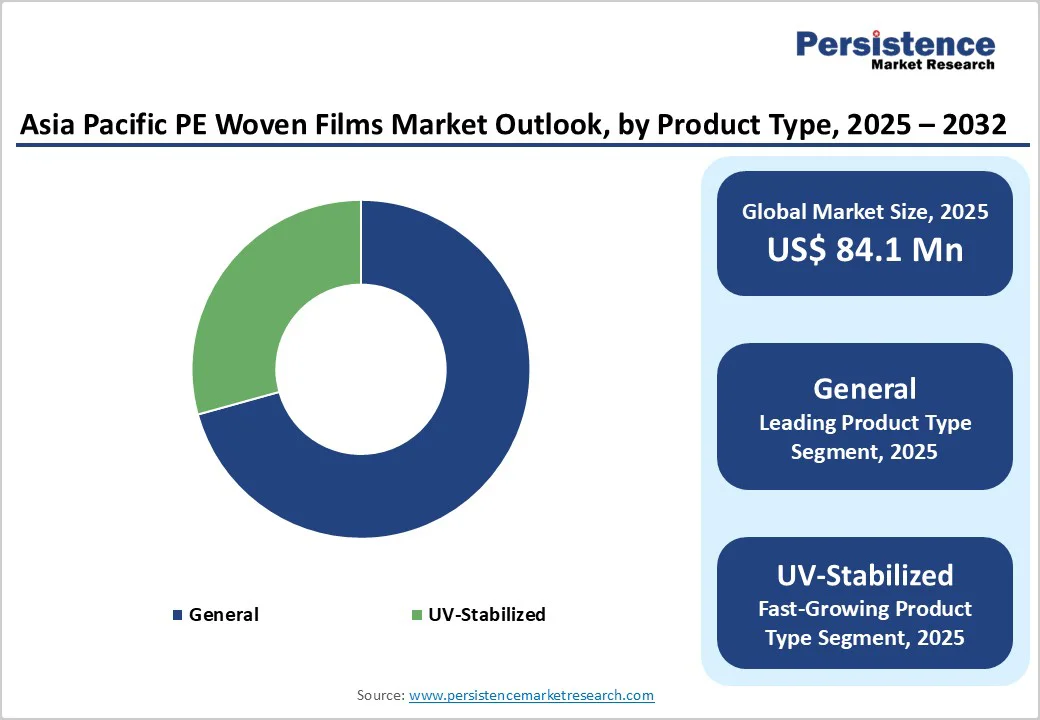

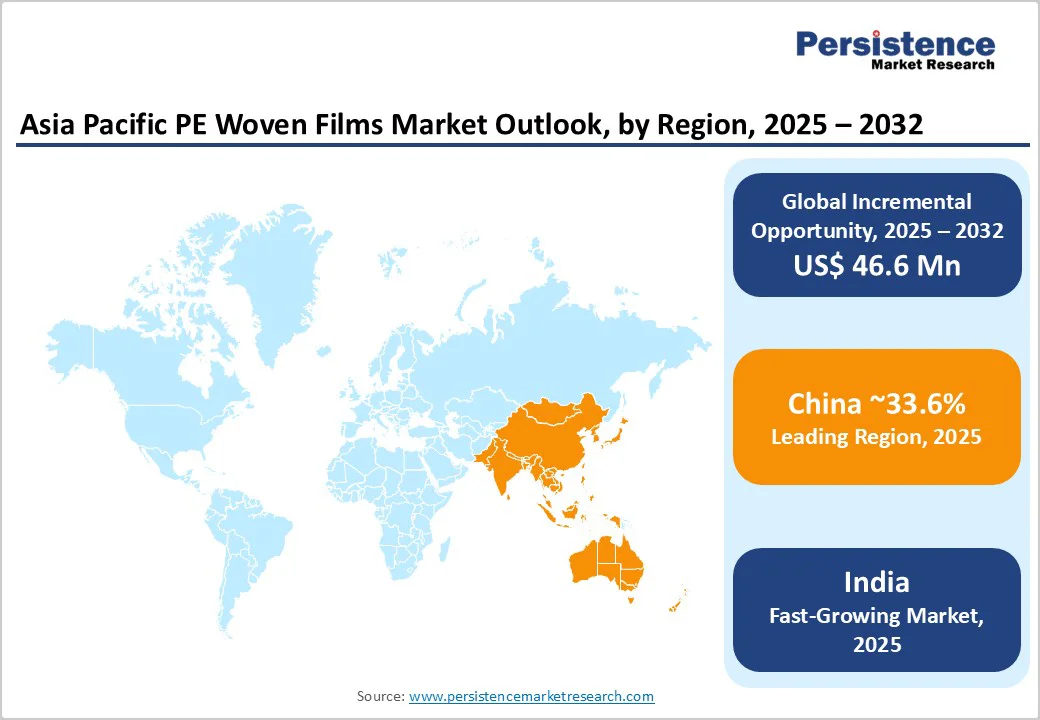

The Asia Pacific PE woven films market size is likely to be valued at US$84.1 Million in 2025 and is estimated to reach US$130.7 Million in 2032, growing at a CAGR of 6.5% during the forecast period 2025-2032, driven by ongoing industrialization, infrastructure expansion, and the rising demand for durable packaging materials.

Key Industry Highlights

- Leading Product Type: General PE woven films hold nearly 70.7% share in 2025, as they provide an excellent balance of strength, flexibility, and water resistance at low cost.

- Dominant Material Type: Virgin PE, approximately 65.8% of the Asia Pacific PE woven films market share in 2025, since it ensures better sealing, lamination, and hygiene standards required in food and medical packaging.

- Key Application: Soil remediation and erosion control recorded around 35.2% share in 2025, as governments in China and India are using PE woven films in large-scale erosion control and riverbank protection programs.

- Leading Country: China, with about a 33.6% share in 2025, backed by its vast polymer production base, low manufacturing costs, and superior export infrastructure.

- Fastest-growing Country: India, fueled by the availability of polymer feedstock from Reliance Industries and Indian Oil, which improves raw material stability.

- Expansion Strategy: Shell-CNOOC’s JV recently announced an expansion of its petrochemical complex in Guangdong, including a new ethylene cracker and associated capacity, which will indirectly feed polymer or polyethylene feedstock supply.

| Key Insights | Details |

|---|---|

|

Asia Pacific PE Woven Films Market Size (2025E) |

US$84.1 Mn |

|

Market Value Forecast (2032F) |

US$130.7 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Construction and Infrastructure Activities

The surge in infrastructure and construction projects across Asia Pacific is propelling the demand for PE woven films in civil and structural applications. These films are being used as vapor barriers, roofing membranes, and geotextile liners due to their high tensile strength and moisture resistance.

In 2024, large-scale projects such as India’s Bharatmala highway program and China’s urban redevelopment plans created greater demand for durable as well as weather-resistant materials. Builders are adopting reinforced and UV-stabilized PE woven films to extend the lifespan of roads, bridges, and building foundations.

Booming E-commerce and Consumer Goods Sectors

The ongoing boom in e-commerce and organized retail is fueling the demand for premium, lightweight, and moisture-proof packaging materials. PE woven films are becoming a preferred choice for wrapping, cushioning, and pallet covering, especially for goods shipped over long distances.

In 2025, packaging manufacturers in Southeast Asia and India have expanded production lines to meet rising orders from online marketplaces and logistics companies. Their superior tear resistance and reusability make them ideal for packaging heavy items such as appliances, fertilizers, and industrial components.

Barrier Analysis - Volatile Polymer Prices Hindering Production Consistency

Frequent fluctuations in polyethylene prices remain a major challenge for producers of PE woven films in Asia Pacific. The region’s dependence on imported polymer feedstock, especially in Southeast Asian countries, exposes manufacturers to global oil price swings and supply chain disruptions.

When crude oil prices rise, the cost of raw materials such as HDPE and LDPE directly impacts production margins and pricing stability. For instance, during early 2024, polymer price spikes in China and India compelled several mid-sized converters to temporarily reduce production or delay exports.

Quality Limitations Restricting High-end Applications

While low-cost PE woven films are popular for bulk packaging, they often suffer from quality issues such as uneven thickness, limited tear resistance, and poor printability. These drawbacks restrict their use in premium sectors, including branded consumer packaging or high-visibility retail bags.

Buyers in export markets mainly demand better finish, consistent lamination, and improved aesthetics, which several low-end producers in the region still struggle to meet. This inability to meet performance and appearance standards continues to limit the market reach of low-grade PE woven films.

Opportunity Analysis - Rising Shift toward Sustainable Polymer Alternatives

The rising emphasis on reducing plastic waste is pushing manufacturers in Asia Pacific to explore biodegradable and bio-based alternatives for PE woven films. Regional producers are experimenting with blends of bio-PE derived from sugarcane or corn starch to lower carbon emissions without compromising strength.

For instance, several China- and Japan-based packaging firms have introduced partially bio-based woven films compatible with existing recycling systems. A few companies are also investing in chemical recycling and unique reprocessing technologies to convert post-consumer PE waste into reusable pellets.

Emergence of Functional Films for Specialized Applications

Manufacturers are extensively designing PE woven films with improved functional attributes to serve niche markets. Microporous woven films are gaining traction in hygiene products, including disposable medical gowns and baby diapers, due to their breathability and liquid resistance.

In the food industry, breathable woven films that prevent condensation are being adopted for fresh produce and bakery packaging. Companies in South Korea and Taiwan are investing in precision extrusion and coating technologies to achieve uniform pore structures and improved air permeability. This move toward specialized films is helping regional producers differentiate themselves from commodity-grade competitors.

Category-wise Analysis

Product Type Insights

General PE woven films are expected to account for approximately 70.7% of the share in 2025, as they combine strength, flexibility, and cost-efficiency, making them suitable for a wide range of applications such as packaging, tarpaulins, and construction covers. Their woven structure provides excellent tensile strength and tear resistance while remaining lightweight, which makes them ideal for heavy-duty packaging of cement, fertilizer, and grains. They also have superior moisture and dust resistance, which is valued in tropical regions of Asia Pacific where humidity levels are high.

UV-stabilized PE woven films are witnessing steady demand due to their important role in agricultural and outdoor applications. These films are treated with UV absorbers or stabilizers that protect them from degradation caused by prolonged sunlight exposure. Farmers in countries such as India, Thailand, and Vietnam are extensively using UV-stabilized films for mulching, pond lining, and greenhouse covers to ensure long lifespan and better crop protection.

Material Type Insights

Virgin PE is speculated to capture around 65.8% of the share in 2025, due to its consistent mechanical strength, uniform texture, and high processability compared to recycled PE. It ensures better film quality, high load-bearing capacity, and smooth lamination- key for applications requiring durability and hygiene, including food packaging, medical wrapping, and industrial liners. Virgin polyethylene also provides superior resistance to puncture, moisture, and chemicals, which is essential in construction and transportation uses.

Reinforced PE woven films are gaining traction due to their improved durability and ability to withstand mechanical stress. These films integrate mesh or scrim layers during extrusion or lamination, resulting in improved tear resistance and dimensional stability. Such films are widely used in heavy-duty tarpaulins, pond liners, and temporary shelters where high tensile strength is essential. The construction sector mainly favors reinforced PE for scaffolding covers and vapor barriers, as it can resist wind load and rough handling at job sites.

Application Insights

The soil remediation and erosion control segment is predicted to hold nearly 35.2% of the share in 2025, owing to the films’ ability to act as superior, water-resistant barriers that stabilize soil and prevent nutrient loss. These films are used for lining contaminated soil, landfills, and embankments, where they prevent leaching of pollutants and erosion caused by rain or wind. Governments in Asia Pacific, especially China and India, have launched large-scale land restoration projects, where PE woven geotextiles are employed to reinforce soil and reduce sediment displacement.

Greenhouse covers represent a key application for PE woven films as they provide optimal protection and a controlled microclimate for crops. The woven structure allows good light diffusion while maintaining thermal insulation, which helps in extending growing seasons and improving yield. Farmers prefer PE woven greenhouse films over traditional glass or rigid plastics due to their lightweight nature, low cost, and easy installation. Modern versions include anti-drip and anti-fog coatings that prevent condensation, promoting healthy plant growth.

Country Insights

China PE Woven Films Market Trends

In 2025, China is estimated to account for approximately 33.6% of the share, owing to high production capacity, intense price competition, and rising emphasis on sustainability and quality improvement. Most of the manufacturing activity is concentrated in provinces such as Shandong, Zhejiang, and Guangdong, where producers benefit from large-scale polymer supply chains and proximity to export ports. However, the market has become saturated, compelling small-scale converters to either upgrade their technology or shut down.

Leading producers are investing in unique extrusion and lamination lines to cater to export demand for BOPP-laminated and recyclable mono-PE woven films. For instance, domestic companies such as Shouguang Jincheng New Material and Shandong Shouguang Packaging have recently modernized facilities to produce high-strength and recyclable PE woven films for food and chemical packaging. The industry is also complying with China’s circular economy goals, with manufacturers experimenting with recycled polyethylene blends.

India PE Woven Films Market Trends

In India, the market is expanding rapidly, pushed by rising demand from the packaging, agriculture, and infrastructure sectors. The country is moving from low-cost manufacturing toward quality-oriented production, backed by increasing investments in BOPP and laminated woven film facilities. Local companies such as Rishi FIBC, Singhal Industries, and TP Polymer are mainly focusing on exports to Europe, the Middle East, and Africa, where recyclable and food-grade packaging films are in high demand.

India’s polymer supply security, supported by giants such as Reliance Industries and Indian Oil Corporation, gives local converters a cost advantage. The government’s ban on single-use plastics and focus on Extended Producer Responsibility (EPR) are also encouraging the development of recyclable mono-material PE woven films. Several producers are now adopting novel circular manufacturing processes, using 20 to 30% recycled resin in woven packaging films to comply with new environmental regulations.

South Korea PE Woven Films Market Trends

South Korea’s market is relatively small but highly specialized, serving high-end applications such as electronics packaging, food protection, and industrial wrapping. The market is guided more by technological sophistication and sustainability goals than by price competition. Under South Korea’s Resource Circulation Act and its 2030 recycling roadmap, companies are shifting toward mono-material PE woven films and recycled-content solutions to reduce environmental impact.

LG Chem and SKC are leading research initiatives in recyclable polymer structures and novel lamination techniques suitable for industrial packaging applications. Korea-based converters are also forming partnerships with global chemical firms to create eco-friendly woven films with improved mechanical strength and recyclability. Domestic manufacturers are carving out a niche by supplying high-quality, compliant, and environmentally sustainable woven films that comply with the country’s strict green manufacturing policies.

Competitive Landscape

The Asia Pacific PE woven films market is dominated by a mix of large-scale manufacturers in China and India and several mid-sized players across Southeast Asia. China remains the production powerhouse owing to its extensive polymer supply chain, low-cost labor, and export-oriented manufacturing hubs in provinces such as Shandong and Zhejiang. India-based producers, including Rishi FIBC and Singhal Industries, are strengthening their position through vertically integrated operations and exports to the Middle East and Europe. Various regional players in Vietnam, Thailand, and Indonesia are focusing on contract manufacturing for global packaging companies.

Business Strategies

In the Asia Pacific PE woven films market, competition is intensifying around product differentiation rather than volume. As plain PE woven films are commoditized, companies are shifting toward high-performance or laminated variants used in food packaging, fertilizers, and construction. For instance, several India- and China-based firms have recently invested in BOPP-laminated woven film lines to meet the rising demand for moisture-resistant and printable packaging solutions.

Key Industry Developments

- In May 2025, JPFL Films approved an INR 700 crore (US$84.3 Million) investment to expand its Nashik facility with new BOPP, PET, and CPP film lines.

- In January 2025, Polyplex Corporation approved a new BOPET film plant in India to add 52,400 MTPA capacity.

Companies Covered in Asia Pacific PE Woven Films Market

- Ginegar Plastic Products Ltd.

- Gale Pacific Commercial

- Hebei Weikete Plastic Products Selling Co., Ltd.

- Shandong Zhengbang Plastic Products Co., Ltd.

- LUGUAN Plastics

- Foshan Haili Plastic Products Co., Ltd.

- Henan Fengcheng Plastic Co., Ltd

- Winco Industries Group Co., Ltd.

- YANTAI BAGEASE PACKAGING PRODUCTS CO., LTD.

- Polyplex Corp. Ltd.

- Supreme Industries

- Specialty Polyfilms Pvt. Ltd.

- J.K. Polyfilm

- Mono Industries

- Essen Multipack Limited

- INABATA & Co., Ltd.

- Puyoung Industrial Co., Ltd.

- ESEN POLYTHENE CO PTE LTD

- GRC Group

Frequently Asked Questions

The Asia Pacific PE woven films market is projected to reach US$84.1 Million in 2025.

Expanding infrastructure projects and increasing focus on sustainability are the key market drivers.

The Asia Pacific PE woven films market is poised to witness a CAGR of 6.5% from 2025 to 2032.

Expansion of advanced recycling facilities and development of bio-based PE woven films are the key market opportunities.

Ginegar Plastic Products Ltd., Gale Pacific Commercial, and Hebei Weikete Plastic Products Selling Co., Ltd. are a few key market players.