- Processed Food

- Asian Food Market

Asian Food Market Size, Share, and Growth Forecast, 2026 – 2033

Asian Food Market by Product Type (Instant Noodles, Prepared Meals, Snacks, Sauces & Condiments, Others), Nature (Vegetarian, Non-vegetarian), and Regional Analysis for 2026 – 2033

Asian Food Market Size and Trends Analysis

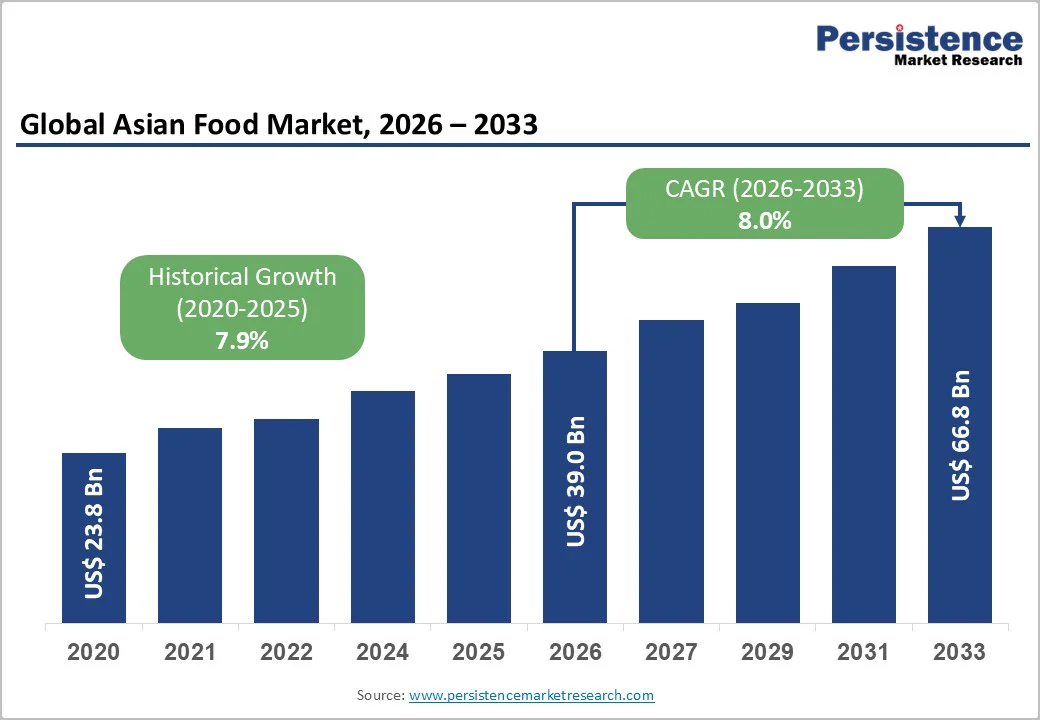

The global Asian food market size is likely to be valued at US$39.0 billion in 2026 and is expected to reach US$66.8 billion by 2033, growing at a CAGR of 8.0% during the forecast period from 2026 to 2033, driven by rising urbanization and fast-paced lifestyles, which are increasing demand for convenience foods such as instant noodles, prepared meals, and ready-to-eat snacks. Growing health awareness is boosting the vegetarian and health-focused product segment, while e-commerce and online grocery channels are improving product accessibility across urban and semi-urban regions. Efficient supply chains and cold storage infrastructure are supporting export growth to North America, Europe, and other emerging markets, expanding the market reach.

Key Industry Highlights:

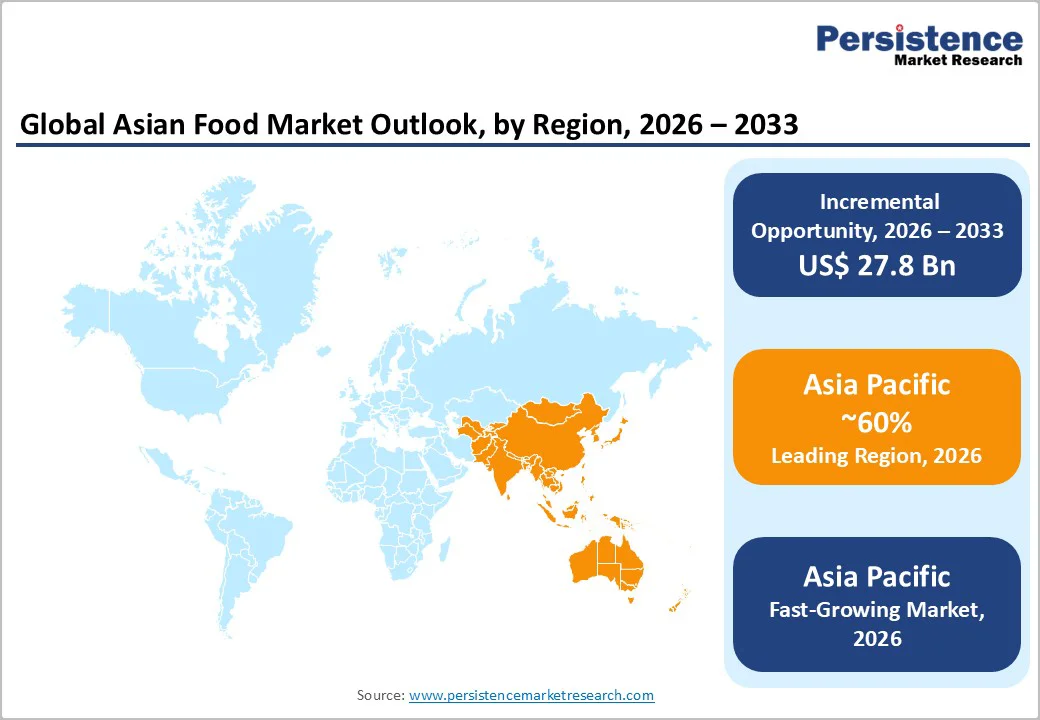

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 60% in 2026, driven by urbanization, middle-class expansion, supportive regulations, and rising e-commerce and cold chain investments.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by supportive regulations and increasing e-commerce and cold chain investments.

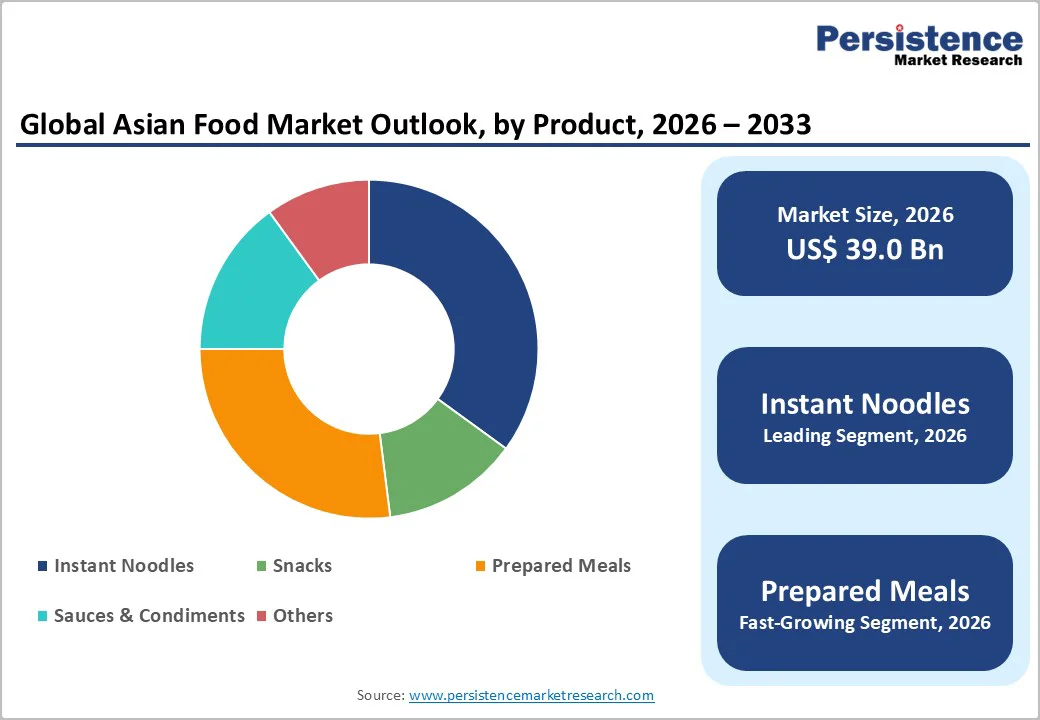

- Leading Product Type: Instant noodles are projected to represent the leading product type in 2026, accounting for 35% of the market share, driven by urbanization, online delivery, and changing lifestyles.

- Leading Nature: Non-vegetarian is anticipated to be the leading food type, accounting for over 50% of the revenue share in 2026, driven by rising protein demand, consumer preference for chicken and pork products, and essential nutrient intake.

| Key Insights | Details |

|---|---|

|

Asian Food Market Size (2026E) |

US$39.0 Bn |

|

Market Value Forecast (2033F) |

US$66.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Convenience-Driven Consumption Rising with Urban Growth

Rapid urbanization across Asia is significantly shaping the demand for convenient and ready-to-eat food products. As more people migrate to urban centers for work and education, lifestyles become busier, reducing the time available for traditional cooking. This shift fuels demand for products such as instant noodles, prepared meals, and packaged snacks, which are easy to prepare and widely available. Urban areas also have better infrastructure for retail and distribution, enabling these products to reach consumers efficiently. Rising disposable incomes in cities allow consumers to spend more on convenience foods without compromising quality, further supporting market growth.

The increasing preference for convenience is closely linked to the proliferation of online food delivery, e-commerce platforms, and modern retail outlets. Consumers are now able to purchase Asian food products quickly and have them delivered directly to their homes, making convenient options even more attractive. Manufacturers are innovating with ready-to-eat meals, single-serve packaging, and flavor variations to meet diverse consumer tastes. This combination of lifestyle changes, retail expansion, and product innovation positions convenience demand as a major growth driver.

Supply Chain Disruptions

The production of convenience foods, snacks, sauces, and ready-to-eat meals relies heavily on the continuous availability of raw materials such as grains, spices, vegetables, and protein sources. Interruptions caused by natural disasters, geopolitical tensions, or transportation bottlenecks can delay manufacturing schedules, increase production costs, and limit product availability in both domestic and international markets. For example, the import of specialty ingredients from countries, including China, Japan, or Thailand, can be impacted by port congestion or regulatory restrictions, affecting the overall supply chain efficiency.

Disruptions in cold chain logistics and warehousing can compromise the quality and shelf life of perishable products such as prepared meals and frozen foods, making it harder for manufacturers and retailers to meet consumer demand. Such inefficiencies also affect online and offline distribution channels, including hypermarkets, convenience stores, and e-commerce platforms. As a result, companies must invest in robust supply chain management, diversified sourcing strategies, and advanced inventory systems to mitigate risks. Without these measures, supply chain disruptions could slow the market’s expansion.

Fusion Products for Western Markets

The growing popularity of Asian cuisine presents a major opportunity for market players to develop fusion food products for Western markets. By blending traditional Asian flavors, ingredients, and cooking styles with Western food preferences, companies can create unique offerings that appeal to a wider consumer base. Products such as ramen-inspired pasta, teriyaki-flavored snacks, or curry-infused ready meals cater to adventurous taste seekers while maintaining the convenience that modern consumers demand. Example snacks infused with teriyaki or curry flavors, ramen-inspired pasta, and ready-to-eat meals blending Asian spices with Western staples. These products cater to the growing demand for convenient, flavorful, and exotic food options while differentiating brands in competitive markets.

Western regions, particularly North America and Europe, are increasingly receptive to ethnic and fusion foods due to globalization, travel exposure, and evolving taste preferences. The expansion of modern retail, hypermarkets, and online grocery platforms facilitates accessibility and distribution. By investing in product innovation, marketing, and localization strategies, companies can strengthen their international footprint and increase revenue. The expansion of modern retail formats, large supermarket chains, and digitally driven grocery platforms enhances product visibility and accelerates penetration for Asian brands.

Category-wise Analysis

Product Type Insights

Instant noodles are expected to lead the Asian food market, accounting for approximately 35% of total revenue in 2026, driven by their affordability, long shelf life, and strong presence of urban retail outlets. Consumers prefer instant noodles for their quick preparation and wide flavor range, making them a staple for students, working professionals, and busy households. Continuous product innovation, such as spicy Korean noodles, fortified variants, and premium cup noodles, helps maintain consumer interest. An example includes Nissin’s Cup Noodles and Indomie’s Mi Goreng, both of which enjoy significant popularity across Asia due to consistent quality, low cost, and easy availability. Manufacturers continuously innovate through new flavors, fortified variants, and premium options, strengthening category loyalty.

Prepared meals are likely to represent the fastest-growing product types in 2026, driven by rising urbanization, time constraints, and the expansion of e-commerce and food delivery platforms. Consumers increasingly prefer ready-to-eat dishes, frozen meals, and meal kits that offer convenience without compromising taste or nutrition. Flavor diversification and microwave-ready packaging further enhance demand. Example ITC’s “Kitchens of India” ready meals or CJ CheilJedang’s Bibigo frozen meals, which have gained traction due to authentic flavors and convenience, appealing to modern consumers seeking quick meal solutions. The rise of meal kits, frozen Asian entrées, and fusion-style meals accelerates growth.

Nature Insights

Non-vegetarian food is projected to lead the Asian food market, capturing around 50% of the total revenue share in 2026, driven by high demand for protein-rich options such as chicken, pork, seafood, and eggs. These foods are deeply rooted in Asian cuisines, ensuring strong household consumption. The segment includes frozen meats, meat-based snacks, broths, and ready-to-eat curries. Rising awareness of nutritional benefits further drives preference for non-veg products. A valid example is Ajinomoto’s chicken gyoza or Korean spicy chicken ramen, which remain popular due to their taste, convenience, and protein-rich profile, reinforcing dominance in the category. Growing awareness of protein intake and essential nutrients also reinforces loyalty toward non-vegetarian products. Retailers and food manufacturers continue expanding offerings through marinated meats, instant broths, and prepared non-veg meals.

The vegetarian segment is likely to be the fastest-growing segment in 2026, driven by rising health consciousness, plant-based dietary trends, and clean-label preferences. Urban consumers increasingly choose vegetable-based snacks, tofu meals, soy products, and plant-protein alternatives. Innovations such as plant-based dumplings, vegetarian noodles, and meat-free curries are widening the consumer base. A suitable example is Nestlé’s plant-based “Harvest Gourmet” range or VegeMeat dumplings, which offer healthier meal solutions while mimicking traditional flavors, appealing to both vegetarians and flexitarian consumers. The segment also benefits from interest in Asian vegetarian cuisine, which is known for its diversity and flavor depth. With supportive regulatory environments and increased retail visibility.

Regional Insights

North America Asian Food Market Trends

The North America region is likely to be a significant market for Asian Food in 2026, driven by increasing demand for authentic, flavorful, and convenient Asian food products. Rising multicultural exposure, expansion of Asian restaurants, and popularity of K-pop, anime, and Asian travel content have increased interest in cuisines such as Japanese, Korean, Thai, Vietnamese, and Chinese. Consumers are shifting toward ready-to-eat and ready-to-cook Asian meals, noodles, dumplings, and sauces that offer restaurant-style flavors at home. For example, the rapid rise of Bibigo dumplings by CJ Foods, which have become a staple in the U.S. freezer aisles, and Nissin’s Cup Noodles, which continue to see a high demand due to convenience and diverse flavor innovations. This preference for quick, global flavors is shaping retail shelves and influencing product launches across supermarkets.

Another notable trend is the growing acceptance of Asian fusion products that blend traditional ingredients with American food formats. Items such as teriyaki-flavored snacks, sriracha-infused sauces, and Korean BBQ meal kits are becoming mainstream. Consumers also show increasing interest in healthier Asian foods, including plant-based dumplings, low-sodium soy sauces, and gluten-free noodles. Example Kikkoman’s low-sodium soy sauce and Annie Chun’s vegan noodle bowls, which cater to health-conscious shoppers while preserving authentic taste. The rise of Asian brands on Amazon, Target, Walmart, and Costco further accelerates availability.

Europe Asian Food Market Trends

Europe is likely to be a significant market for Asian Food in 2026, due to cultural exposure, travel, and the expansion of Asian restaurant chains. The demand for convenience foods such as instant noodles, dumplings, spring rolls, and ready-to-cook Asian meal kits has surged, especially among young urban populations seeking quick meal solutions. European supermarkets such as Tesco, Carrefour, and Aldi are expanding their Asian product shelves to meet this rising interest. For example, Itsu partnered with Bakkavor to roll out a six-item range of chilled ready meals, including dishes such as Katsu Chicken Brown Rice, Chicken Pad Thai Noodles, and Teriyaki Veg Gyoza into Tesco stores nationwide.

The European market’s growing focus on quality, transparency, and product standards is evident. For example, Itsu issued a recall for its frozen “Sizzling Pork Gyoza” in the U.K. after the Food Standards Agency (FSA) found the products could contain small pieces of plastic, prompting removal of those items from major retailers. The recall highlights the challenges brands encounter when scaling Asian food products for wider European markets, including stringent food safety regulations, complex supply-chain oversight, and heightened consumer scrutiny. Manufacturers must balance innovation and convenience with rigorous quality control to maintain consumer trust. Brands are responding through innovative products such as Yutaka’s vegan ramen kits and Thai Kitchen’s gluten-free coconut milk and curry pastes, which cater to diet-conscious shoppers.

Asia Pacific Asian Food Market Trends

The Asia Pacific region is anticipated to be the leading region in the Asian food market in 2026, driven by urban lifestyles, rising incomes, and consumers’ growing preference for convenient, high-quality packaged meals. Asia Pacific is also likely to be the fastest-growing region. Countries such as China, Japan, South Korea, India, and Southeast Asia continue to lead innovation in noodles, frozen meals, snacks, and sauces, supported by dense retail networks and aggressive product rollouts. For example, Nissin expanded its premium “Raoh” noodle line in Japan and Southeast Asia to meet demand for restaurant-style ramen at home, and South Korea’s CJ CheilJedang scaled its Bibigo dumplings across APAC after achieving record sales. These advancements highlight a shift toward elevated flavors, better ingredients, and hybrid Asian-fusion.

Digital penetration and food-delivery growth are reshaping consumption. Platforms like Meituan (China), Zomato (India), and GrabFood (Southeast Asia) have accelerated demand for ready-to-cook and ready-meal formats by promoting value bundles and regional flavors. For example, India's ITC Foods expanded its Master Chef frozen meals and Asian-inspired bowls to cater to the growing home-dining trend across metros. Health-conscious variants low-sodium noodles, plant-based dumplings, and gluten-free sauces, are also rising, driven by younger consumers. This blend of innovation, digital influence, and regional flavor adaptation is solidifying Asia Pacific as the fastest-evolving hub of the Asian food market.

Competitive Landscape

The global Asian food market is moderately fragmented, characterized by a mix of major multinational brands, strong regional specialists, and a growing base of agile local players targeting niche flavors and convenience-driven formats. Leading companies maintain their positions through extensive distribution networks, innovation-focused R&D, and economies of scale, while regional players strengthen consumer loyalty by offering authentic local tastes and rapid product turnover. Key players include Ajinomoto, Nissin, Nestlé, and Calbee. The competitive landscape spans categories such as instant noodles, frozen and prepared meals, snacks, and sauces, each experiencing continuous product innovation and market expansion.

These players compete through accelerated product innovation, strategic retail partnerships, and digital distribution, using e-commerce, D2C channels, and global supermarket listings to widen reach. Recent moves such as Ajinomoto’s focus on ready-to-eat and frozen lines, Conagra’s large frozen-foods rollout, Calbee’s local production strategy in China, and Bibigo’s European expansion illustrate how brands balance global scale with local adaptation. Quality control, supply-chain resilience, and clean-label formulation have become key battlegrounds as regulatory scrutiny and health trends rise; successful firms pair disruptive products with rigorous safety and localization strategies to win shelf and consumer trust.

Key Industry Developments:

- In February 2025, CJ Foods expanded its global footprint by launching new squeezable versions of its bibigo Gochujang and Ssamjang sauces in major European markets, including Germany, the U.K., France, and the Netherlands. The products are reformulated into thinner, versatile textures to suit Western eating habits, making them ideal for dipping and drizzling on everyday foods like fries, salads, and tacos.

- In October 2024, Nestlé expanded its frozen-meals portfolio by launching new Asian-inspired dishes under the Mings brand in the U.S. market. The company also partnered with Tapatío to co-develop fusion frozen meals featuring the brand’s signature flavors. This move reflects Nestlé’s strategy to tap into the rising demand for convenient, globally inspired Asian cuisine across North America.

Companies Covered in Asian Food Market

- Ajinomoto Co. Inc.

- Nissin Food Holdings

- Nestlé S.A

- Toyo Suisan Kaisha Ltd.

- Calbee Group

- ITC Limited

- Unilever PLC

- Kikkoman Corporation

- Asians Food Products

- ConAgra Brands

Frequently Asked Questions

The global Asian food market is projected to reach US$39.0 billion in 2026.

Key growth drivers include increasing global demand for convenient, authentic, and culturally diverse cuisines, further supported by rapid urbanization and the expansion of retail and e-commerce channels.

The Asian food market is expected to grow at a CAGR of 8.0% from 2026 to 2033.

Expansion of fusion Asian products in Western markets, growth in plant-based and clean-label Asian foods, and increasing penetration through online retail and ready-to-eat meal innovations.

Ajinomoto Co. Inc., Nissin Food Holdings, Nestlé SA, Toyo Suisan Kaisha Ltd., Calbee Group, ITC Limited, and Unilever PLC are the leading players.