- Hardware & Software IT Services

- Asia Pacific IT Services Market

Asia Pacific IT Services Market Size, Share, and Growth Forecast 2026 - 2033

Asia Pacific IT Services Market by Approach (Reactive Services, Proactive Services), Services (IT Consulting & Implementation, IT Outsourcing, Business Process Outsourcing, Managed Cloud and XaaS Services, Others), Application, Technology, End-user Industry, and Regional Analysis for 2026 - 2033

Asia Pacific IT Services Market Size and Trend Analysis

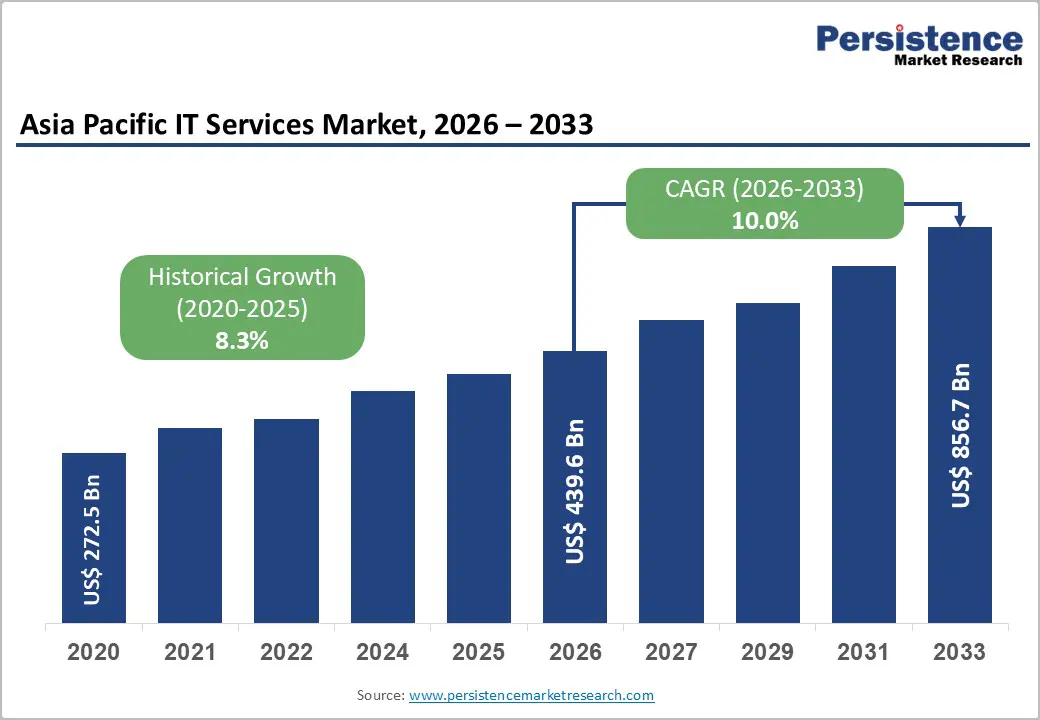

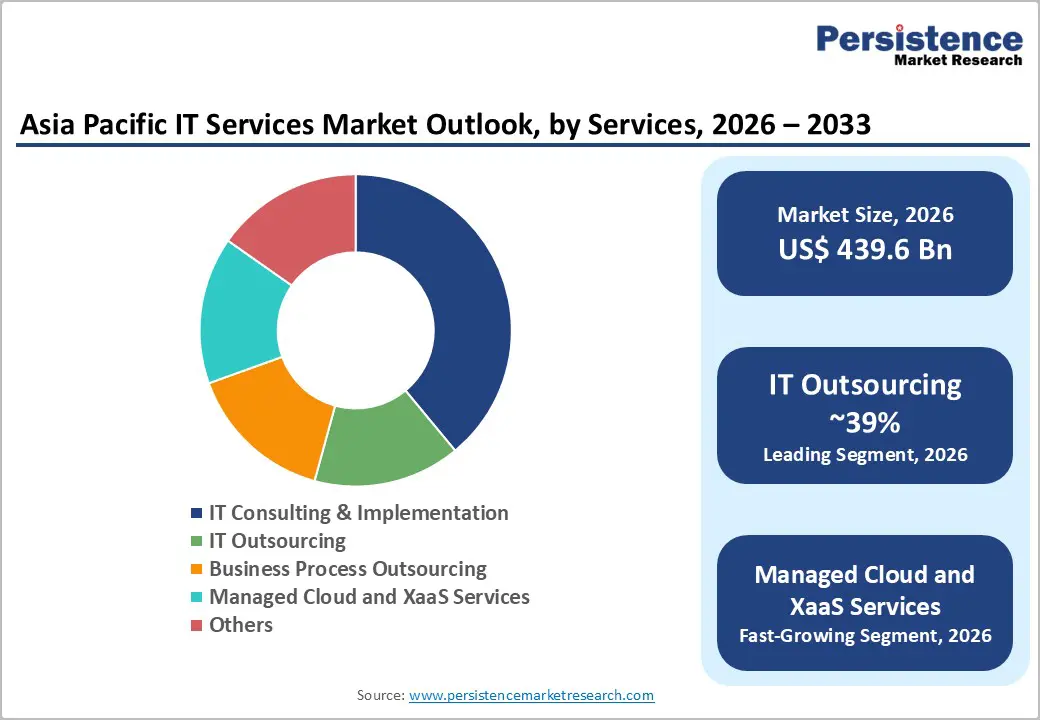

The Asia Pacific it services market is estimated to be valued at US$ 439.6 Bn in 2026 and is projected to reach US$ 856.7 Bn by 2033, growing at a CAGR of 10.0% between 2026 and 2033.

The sustained expansion of the market is primarily driven by accelerating digital transformation initiatives across both mature and emerging economies in the region. Governments and enterprises in China, India, Japan, and Southeast Asia are rapidly scaling investments in cloud infrastructure, artificial intelligence, and cybersecurity to modernize operations, enhance resilience, and maintain competitive advantage. According to IDC, public cloud services spending in the Asia/Pacific region is projected to grow at a CAGR of 19.8% from 2025 to 2029, reflecting the region’s deeply entrenched commitment to technology-led growth.

Key Market Highlights

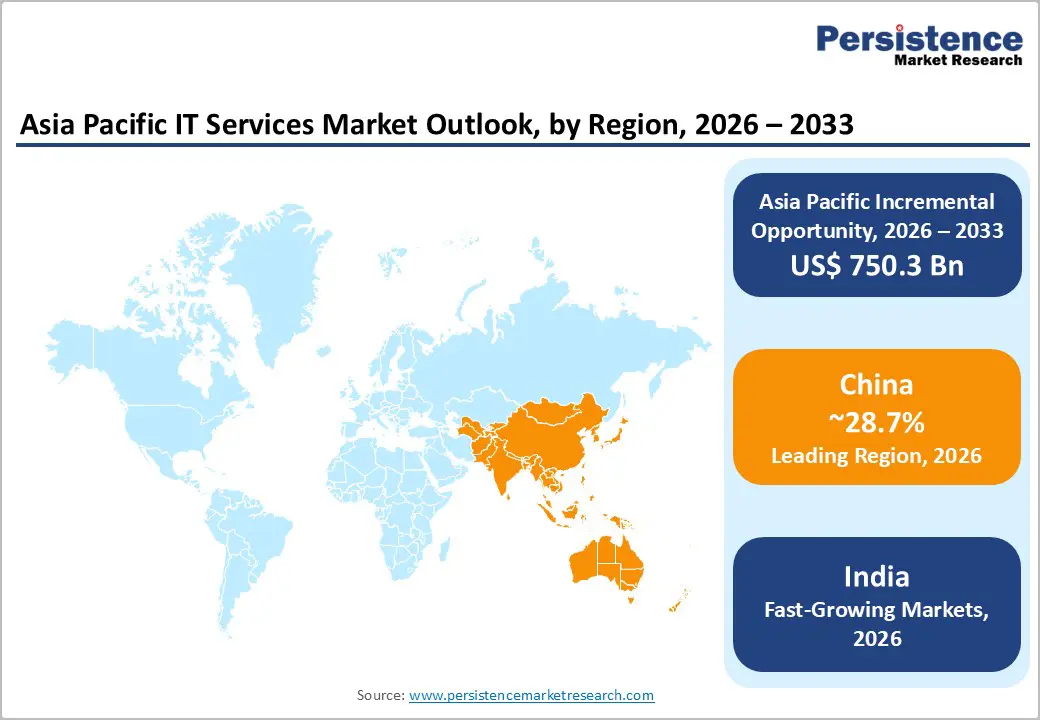

- Leading Country: China dominates the Asia Pacific IT Services market with approximately 28.7% regional share in 2026, propelled by state-directed digitalization, domestic hyperscaler expansion, and large-scale industrial technology modernization programs across manufacturing and financial services.

- Fastest Growing Country: India is the fastest-growing country in the Asia Pacific IT Services market, poised for a CAGR of 10.43% through 2031, driven by IT export leadership surpassing USD 199 billion in FY2024 and an accelerating domestic digital transformation agenda.

- Dominant Segment: IT Outsourcing is the dominant service segment, commanding approximately 39% of the Asia Pacific IT Services market, underpinned by the region’s globally recognized delivery infrastructure and cost-competitive, highly skilled talent base in India, the Philippines, and Vietnam.

- Fastest Growing Segment: Artificial Intelligence & Machine Learning is the fastest-growing technology segment as generative AI and intelligent automation become central to enterprise IT service delivery models.

- Key Market Opportunity: The convergence of AI/ML with Managed Cloud and XaaS models, particularly in Healthcare & Life Sciences and BFSI, represents the most significant growth opportunity, projected to grow at a CAGR exceeding 10%, driven by government digital health mandates and rising demand for compliant, AI-powered managed services.

| Key Insights | Details |

|---|---|

| Asia Pacific IT Services Market Size (2026E) | US$ 439.6 Bn |

| Market Value Forecast (2033F) | US$ 856.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 10.0% |

| Historical Market Growth (2020 - 2025) | 8.3% |

Market Dynamics and Market Growth Drivers

Accelerating Enterprise Cloud Adoption and Digital Transformation Across Asia Pacific

Enterprise cloud adoption has emerged as the most influential driver of growth within the Asia Pacific IT Services market. According to IDC’s Worldwide Software and Public Cloud Services Spending Guide, the region’s public cloud market is expected to reach USD 250 billion by 2025, supported by a 14.2% CAGR through 2028 as generative AI adoption accelerates and enterprises modernize their IT environments.

Organizations across the region are shifting from reactive, on-premises infrastructures to proactive, cloud-native architectures that deliver greater scalability, cost efficiency, and operational resilience. This large-scale migration continues to drive strong demand for IT consulting, cloud migration services, managed services, and cloud-native application development.

Government-Backed Digitalization Programs and Smart Infrastructure Investment

Strategic government investment in digital infrastructure across the region is a structural growth driver for the Asia Pacific IT Services market. National initiatives such as India’s Digital India campaign, China’s Made in China 2025, and Japan’s Digital Agency, which are orchestrating interoperability reforms, are channeling billions of dollars into technology modernization. Australia’s Digital Economy Strategy similarly mandates significant investment in cybersecurity hardening and modernizing data governance, according to the Australian Department of Industry.

Furthermore, government-led smart city projects, 5G network buildouts, and Industrial IoT (IIoT) deployments across manufacturing hubs are generating multi-year IT services contracts. The Southeast Asia Digital Economy, as tracked by SEADS data from February 2025, is expanding at an extraordinary pace, further reinforcing the government-as-catalyst dynamic that continues to fuel demand for IT infrastructure, cybersecurity, and managed services across the region.

Market Restraints

Escalating Cybersecurity Threats and Rising Regulatory Compliance Costs

Escalating cybersecurity incidents are generating substantial financial and operational pressures on enterprises across the Asia Pacific region, slowing the progress of broader digital transformation efforts. IBM Security’s Cost of a Data Breach Report 2024 indicates that the average cost of a data breach in Asia-Pacific rose to USD 3.05 million in 2024, with Singapore recording an average of USD 4.87 million, among the highest globally.

Concurrently, stringent compliance obligations under China’s Cybersecurity Law and India’s Digital Personal Data Protection Act are increasing operational overheads, particularly for mid-market organizations, thereby diverting critical investment away from strategic, growth-focused transformation initiatives.

Acute Shortage of Skilled IT Talent Constraining Service Delivery

A persistent and expanding shortage of skilled IT professionals continues to serve as a significant structural constraint on the Asia Pacific IT Services market. Despite rising demand for cloud architects, AI/ML engineers, cybersecurity specialists, and data scientists, the regional talent pool remains insufficient to meet the accelerating demand.

Industry surveys show that over 51% of IT service providers globally identify skill shortages as a primary operational challenge, with the issue particularly pronounced in Southeast and South Asia. This talent deficit escalates delivery costs, prolongs project timelines, and restricts the ability of service providers to scale effectively, thereby limiting near-term revenue growth.

Market Opportunities

Surging Demand for AI-Powered Managed Services and XaaS in Healthcare and BFSI

The accelerating convergence of Artificial Intelligence and Machine Learning (AI/ML) with managed cloud services is creating a significant and transformative revenue opportunity for IT services providers across the Asia Pacific region. The healthcare and life sciences sector is emerging as the fastest-growing end-user market, driven by government programs such as India’s Ayushman Bharat Digital Mission and Singapore’s National Electronic Health Record initiative, which mandate interoperable and security-enhanced digital platforms.

Concurrently, the Banking, Financial Services, and Insurance (BFSI) sector is advancing large, multi-year managed services engagements as institutions adopt AI-enabled fraud detection, modernize core-banking systems, and strengthen digital-first customer experiences. Managed cloud and XaaS models are projected to expand at a CAGR exceeding 10%, positioning vendors with expertise in HL7 FHIR integration, identity assurance, and privacy-preserving analytics to capture substantial growth.

Emergence of Southeast Asia and India as High-Growth IT Services Hubs

The rapid economic expansion of India and key Southeast Asian markets, including Vietnam, Indonesia, and the Philippines, presents a significant dual opportunity, both as high-value delivery hubs and as rapidly growing consumption markets for IT services. India’s IT and business-process export revenue surpassed USD 199 billion in fiscal 2024, while domestic enterprises across banking, retail, and healthcare continue to accelerate investments in cloud and AI-driven modernization.

The country is further projected to sustain a 10.43% CAGR through 2031, balancing its global outsourcing leadership with a fast-maturing digital economy. In Southeast Asia, rising public-sector cloud adoption and rapid SME digitization, supported by youthful, digitally native populations, are reshaping regional demand. Providers that establish early delivery capabilities and strategic partnerships stand to benefit disproportionately from these structural growth drivers.

Category-wise Insights

Approach Analysis

Within the Approach category, Reactive IT Services maintain a dominant position, representing approximately 55% of the Asia Pacific IT Services market. This segment comprises break-fix support, incident response, and corrective maintenance, functions that organizations adopt as essential operational measures to minimize system downtime and mitigate productivity or revenue losses. The continued reliance on reactive services is largely attributable to the substantial presence of legacy infrastructure across the region, particularly within manufacturing, government, and traditional financial institutions, where modernization timelines often lag operational needs.

Across China, Japan, and South Korea, major industrial conglomerates and state-owned enterprises depend heavily on reactive support for managing complex, aging systems. In contrast, Proactive IT Services, which include managed monitoring, predictive analytics, and continuous optimization, constitute the fastest-growing segment as enterprises increasingly appreciate the long-term cost efficiencies and resilience benefits of anticipatory maintenance strategies.

Services Analysis

Within the Services category, IT Outsourcing (ITO) remains the dominant segment in the Asia Pacific IT Services market, supported by the region’s mature and globally established outsourcing ecosystem. ITO is projected to reach a market volume of US$126.9 billion in 2026, representing approximately 39% of the total services mix. This leadership is driven by enterprises’ strategic need to reduce operational costs, access specialized technical talent, and enhance organizational agility without expanding internal workforce capacity.

India, the Philippines, and Vietnam continue to serve as leading global outsourcing destinations, leveraging extensive pools of English-proficient, technically skilled professionals and highly cost-competitive delivery models. Meanwhile, Managed Cloud and XaaS Services have emerged as the fastest-growing sub-segment, reflecting the region’s accelerated transition from ownership-based IT consumption to scalable, subscription-oriented service models.

Application Analysis

The Application Management segment leads the market, accounting for 32%. This dominance reflects the growing enterprise emphasis on ensuring the continuous performance, reliability, and security of mission-critical applications in an increasingly digital-first operating environment. As organizations transition from legacy monolithic systems to cloud-native, microservices-based architectures, the scope and complexity of application management expand significantly, encompassing performance monitoring, patch management, API orchestration, and incident resolution.

Demand is further accelerated by the rapid growth of mobile applications, e-commerce ecosystems, and digital banking platforms. Meanwhile, Security and Compliance Management is emerging as the fastest-growing segment, driven by rising cyber threats and stringent regulatory frameworks such as China’s Cybersecurity Law and India’s DPDPA.

Technology Analysis

The Artificial Intelligence and Machine Learning (AI/ML) segment remains the dominant technology category in the Asia Pacific IT Services market, contributing roughly 60% of technology-segment revenue. Its leadership stems from AI/ML’s broad applicability across IT service delivery, including automated service-desk operations, predictive infrastructure management, fraud detection in BFSI, and advanced diagnostic imaging in healthcare.

According to the 2025 ISG Provider Lens® report, enterprises are increasingly adopting AI-driven ADM services to modernize legacy systems, enhance operational efficiency, and improve software reliability. Leading providers, such as Accenture, TCS, Infosys, and HCLTech, were recognized as market leaders across multiple ADM quadrants. Cloud Computing remains the second-largest technology segment, while Cybersecurity Solutions continues to be the fastest-growing.

End-User Industry Analysis

The Banking, Financial Services, and Insurance (BFSI) sector remains the leading end-user industry in the Asia Pacific IT Services market, accounting for nearly 25% of total revenue. This leadership is supported by the sector’s sustained focus on digital-first banking models, modernization of core banking systems, deployment of AI-driven fraud-prevention platforms, and expanding regulatory compliance requirements.

The rapid growth of mobile banking, digital payments, and neobanks across China, India, Singapore, and Southeast Asia continues to drive large-scale IT services demand. IT & Telecom holds the second-largest share, propelled by extensive 5G rollouts and OSS/BSS transformation. Meanwhile, Healthcare & Life Sciences is the fastest-growing segment, boosted by government-led digital health initiatives, with Retail & E-commerce also expanding due to omni-channel adoption and AI-enabled personalization.

Country-wise Insights

China Asia Pacific IT Services Market Trends

China holds the largest share of the Asia Pacific IT Services market, accounting for approximately 28.7% of regional revenue in 2026, supported by its extensive enterprise base and state-driven digitalization agenda. Domestic hyperscalers, Alibaba Cloud, Tencent Cloud, and Huawei Cloud, continue to expand in-country cloud regions to reinforce data sovereignty while extending their presence across Southeast Asia.

Government mandates, including the Cybersecurity Law and the Data Security Law, are driving significant investment in compliance-oriented IT services, cybersecurity frameworks, and localized data management platforms. However, growth is gradually moderating as digital infrastructure approaches saturation and regulatory constraints limit foreign provider participation. Despite this, cloud-based solutions and Industry 4.0 initiatives in manufacturing continue to generate sustained demand for specialized IT services.

India Asia Pacific IT Services Market Trends

India is the fastest-growing major market in the Asia Pacific IT Services sector, projected to achieve a CAGR of 10.4% through 2033. The country benefits from dual growth drivers: its globally dominant IT export industry and a rapidly expanding domestic digital economy. India’s IT and business-process services exports surpassed USD 199 billion in FY2024, reinforcing its position as the world’s leading outsourcing hub.

Government-driven initiatives, including Digital India, UPI, and the Ayushman Bharat Digital Mission, are driving substantial domestic demand for cloud, AI, and health IT services. India’s regulatory evolution, particularly the DPDPA, is accelerating investments in data governance and cybersecurity, while state-level incentives such as Andhra Pradesh’s LIFT Policy 4.0 further strengthen India’s role as a premier IT services delivery and consumption market.

Japan Asia Pacific IT Services Market Trends

Japan is the second-largest market within the Asia Pacific IT Services sector, supported by its strong institutional commitment to technology modernization and a highly capitalized enterprise ecosystem. The Japanese Digital Agency, established in 2021, is driving extensive interoperability reforms to eliminate legacy administrative silos, advance government digitalization, and strengthen national cybersecurity posture. According to METI, software adoption among Japanese enterprises exceeds 70%, with the automotive and electronics industries leading the way in digital integration.

Despite this momentum, growth is moderated by challenges such as an aging workforce, reliance on legacy mainframes, and conservative outsourcing models. Domestic leaders, Fujitsu, NTT DATA, NEC, and Hitachi Vantara, are increasingly repositioning around AI-enabled managed services to maintain competitiveness and expand regional presence.

Competitive Landscape

The Asia Pacific IT Services market exhibits a moderately fragmented competitive landscape, with the top ten providers jointly contributing over 40% of regional revenue. Indian industry leaders, Tata Consultancy Services, Infosys, Wipro, HCL Technologies, and Tech Mahindra, continue to command significant outsourcing and transformation engagements through their scale and specialized domain capabilities. Global firms such as Accenture and Capgemini compete by advancing innovation velocity, with Accenture alone reporting more than 1,200 AI and cloud-related patents in 2024. The market is undergoing a marked transition toward AI-embedded service delivery, strategic acquisitions, and ecosystem-centric co-innovation.

Key Market Developments

- October 2025: TCS acquired US-based ListEngage to strengthen its Salesforce practice and accelerate agentic AI capabilities, reinforcing its commitment to AI-led enterprise transformation across Asia Pacific and global markets.

- April 2025: Infosys acquired leading cybersecurity services provider The Missing Link, strengthening its cybersecurity and cloud capabilities across Australia and India, and deepening its managed security services portfolio in the Asia Pacific region.

- August 2025: Accenture announced an agreement to acquire CyberCX, one of the largest cybersecurity service providers in the Asia Pacific region. The acquisition represents Accenture’s largest cybersecurity deal to date and aims to expand its cybersecurity service offerings across the Asia Pacific, particularly in Australia and New Zealand.

Top Companies in the Asia Pacific IT Services Market

- Accenture Plc (Dublin, Ireland) is the foremost digital transformation and IT services integrator in the Asia Pacific, holding approximately 12% of the global IT services consulting share. The company’s AI Navigator platform and over 1,200 AI and cloud patents disclosed in 2024 position it at the forefront of generative AI-driven enterprise transformation. Accenture’s broad vertical coverage, from BFSI and healthcare to manufacturing and public services, combined with its hyperscaler alliance ecosystem, makes it the go-to partner for complex, large-scale transformation mandates across the region.

- Tata Consultancy Services Ltd. (Mumbai, India) is the largest Asia Pacific-origin IT services provider globally, holding a brand value of USD 19.2 billion in 2024. Its Co-Innovation Network (COIN) and Quantum Computing Lab, which enabled 22% of financial and scientific sector clients to pilot quantum use cases, demonstrate its commitment to next-generation capabilities. TCS commands a significant share across outsourcing, application management, and enterprise cloud transformation in Japan, Australia, Singapore, and Southeast Asia.

- Infosys Limited (Bengaluru, India) is distinguished by its AI-first Infosys Topaz platform and the Infosys Cobalt cloud ecosystem, which collectively serve as the backbone of its enterprise transformation offering. The company’s acquisition of The Missing Link in April 2025 significantly deepens its cybersecurity and cloud managed services capabilities in Australia and the broader Asia Pacific region. Infosys serves marquee clients across BFSI, retail, healthcare, and manufacturing, and is a leader in AI-driven ADM services, as recognized by ISG’s 2025 Provider Lens®.

Companies Covered in Asia Pacific IT Services Market

- Accenture

- TCS

- Infosys

- Wipro

- Cognizant

- IBM

- HCL Technologies

- Capgemini

- Deloitte

- Tech Mahindra

- Fujitsu Ltd.

Frequently Asked Questions

The Asia Pacific IT Services market is estimated to be valued at US$ 439.6 Bn in 2026 and is projected to reach US$ 856.7 Bn by 2033, growing at a CAGR of 10.0% during the forecast period of 2026-2033. The historical CAGR between 2020 and 2025 was 8.3%, reflecting consistent market expansion underpinned by rapid digitalization across the region.

The primary demand drivers include the accelerating adoption of cloud computing and enterprise digital transformation initiatives, with IDC projecting the Asia/Pacific public cloud market to reach USD 250 Bn by 2026, along with government-backed digitalization programs such as India's Digital India, China's Made in China 2025, and Japan's Digital Agency reforms that collectively mandate multi-year IT services investments.

IT Outsourcing (ITO) is the dominant segment in the Services category, accounting for approximately 39% of the Asia Pacific IT Services market, driven by the region's globally recognized outsourcing delivery ecosystems in India, the Philippines, and Vietnam. Statista forecasts IT Outsourcing to represent a market volume of US$ 126.9 Bn within the Asia IT services landscape in 2026.

China is the leading country in the Asia Pacific IT Services market, commanding approximately 28.74% of regional revenue in 2026. China's leadership is supported by massive state-directed enterprise digitalization, the dominance of domestic hyperscalers including Alibaba Cloud, Tencent Cloud, and Huawei Cloud, and government policies such as the Cybersecurity Law and Data Security Law mandating compliance-driven IT investments.

The most significant opportunity lies in the convergence of AI/ML with Managed Cloud and XaaS services, particularly within Healthcare & Life Sciences and BFSI. Government-mandated digital health infrastructure programs, such as India's Ayushman Bharat Digital Mission and Singapore's National Electronic Health Record, alongside BFSI's AI-driven modernization, are expected to generate substantial, multi-year managed services contracts at a CAGR exceeding 10%.

The key market players operating in the Asia Pacific IT Services market include Accenture Plc, Tata Consultancy Services Ltd. (TCS), Infosys Limited, Wipro Limited, Cognizant Technology Solutions Corp., IBM Corporation, HCL Technologies Ltd., Capgemini SE, Deloitte Touche Tohmatsu Ltd., Tech Mahindra Ltd., and Fujitsu Ltd.