- Animal Feed & Additives

- Animal Feed Micronutrients Market

Animal Feed Micronutrients Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Animal Feed Micronutrients Market by Nutrient Type (Trace Minerals, Vitamins, Others), by Livestock (Ruminant, Poultry, Swine, Aquaculture, Equine), by Form (Soild, Liquid) and Regional Analysis from 2025 to 2032

Animal Feed Micronutrients Market Share and Trends Analysis

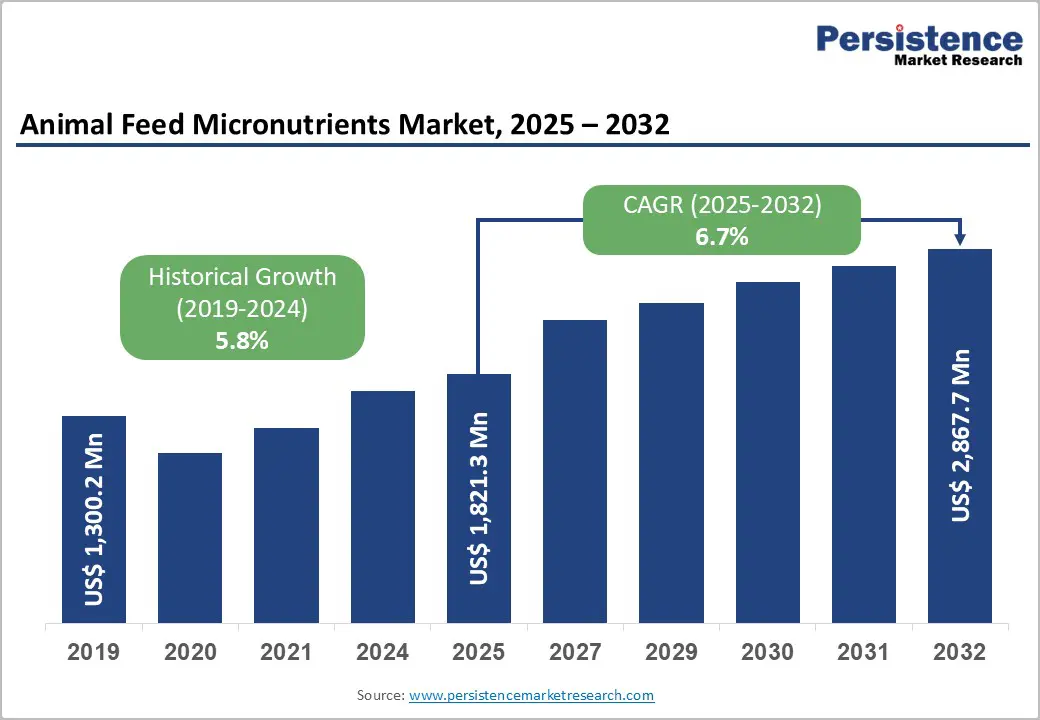

The global animal feed micronutrients market is estimated to grow from US$1,821.3 million in 2025 to US$2,867.7 million by 2032. The market is projected to record a CAGR of 6.7% during the forecast period from 2025 to 2032.

The global Animal Feed Micronutrients market is growing at a significant pace, especially in developing countries, driven by increased awareness among the agricultural community. Most of the agricultural community is opting for advanced methods and nutritional solutions in animal husbandry to maximize output in a shorter timeframe.

Key Industry Highlights

- Leading Nutrient Type: Trace Minerals dominate the market due to their importance in immune function, feed efficiency, reproduction, and overall growth in livestock.

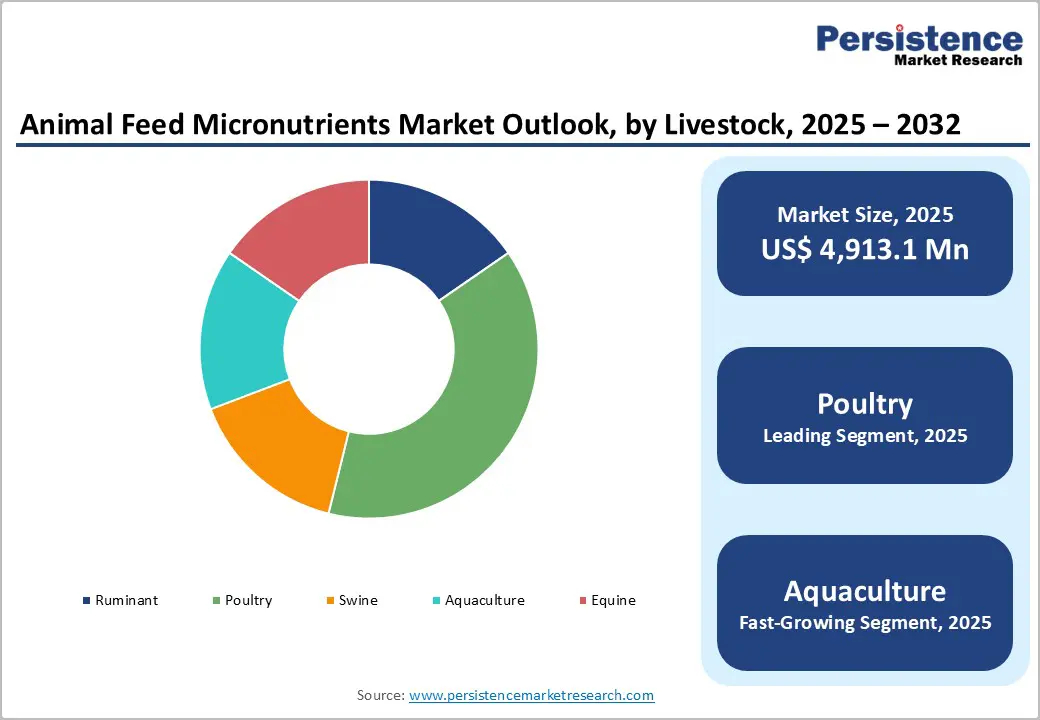

- Dominant Animal Feed Nutrient, by Livestock Type: Poultry, accounting for around 45%, driven by rising global poultry consumption and expansion of commercial poultry farming, and increasing demand for micronutrient-enriched feed formulations.

- Fastest Growing Livestock Type: Aquaculture, as the modern aquaculture systems require nutrient-rich feed to maintain fish health, growth rates, and disease resistance, making micronutrients essential.

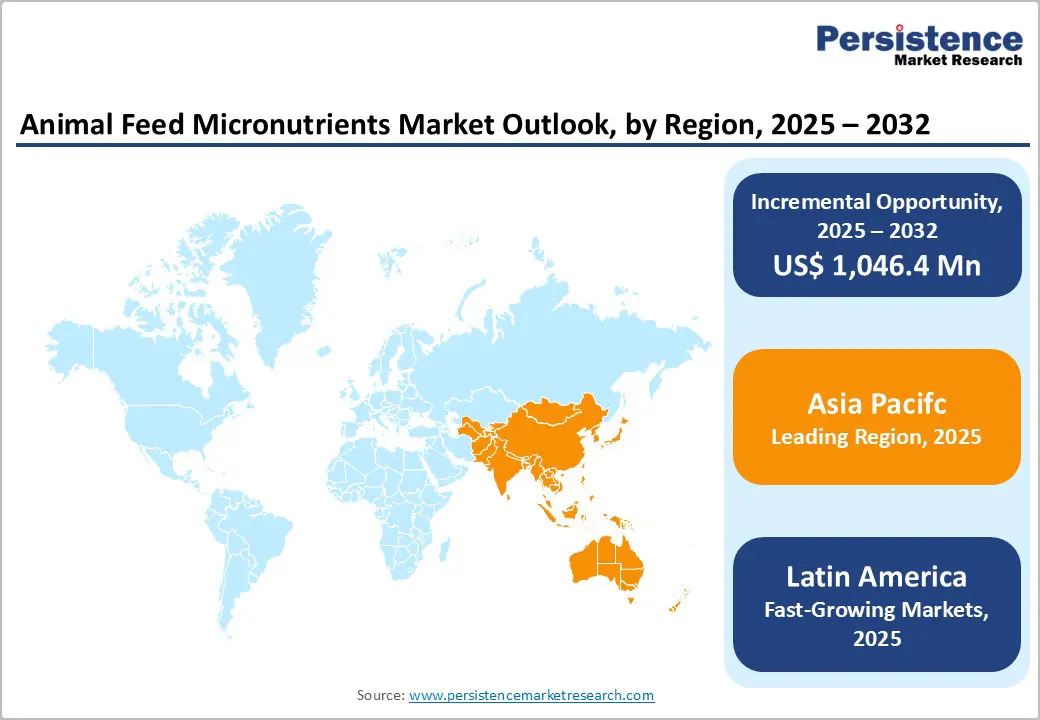

- Leading Region: Asia Pacific, holding approximately 35% market share, due to its large livestock population, strong domestic demand, and supportive government policies. This dominance is driven by rapid urbanization, rising meat consumption, and the expansion of the poultry and aquaculture industries in countries such as China, India, and Southeast Asia.

- Fastest-Growing Region: Latin America, propelled by its large cattle and poultry industry and demand for high-quality animal protein.

- Dominant Animal Feed Micronutrient by Form: Liquid minerals are gaining traction in the animal feed micronutrients market owing to their superior results, reasonable costs and availability of novel delivery systems from manufacturers

- Distinctive Strategies: Market players are developing signature products that are exclusive to their portfolios. Expansion of manufacturing capabilities also appears to be a major differentiator for players in the animal feed micronutrients market. Companies are also providing nutrition solutions to livestock businesses, such as online tools and dose calculators, to establish a loyal consumer base.

| Global Market Attributes | Key Insights |

|---|---|

| Animal Feed Micronutrients Market Size (2025E) | US$ 1,821.3 Mn |

| Market Value Forecast (2032F) | US$ 2,867.7 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

Market Dynamics

Driver - Increasing emphasis on feed efficiency to achieve rapid animal growth and higher output

Rising demand for feed efficiency is transforming the dynamics of the global animal feed micronutrients market as producers aim to achieve faster growth rates and improved output quality. Micronutrients such as zinc, copper, selenium, and manganese are being increasingly incorporated into feed formulations to optimize nutrient absorption, boost immunity, and enhance feed conversion ratios. With pressure mounting to reduce production costs and environmental impact, livestock producers are adopting precision nutrition strategies that deliver maximum weight gain with minimal feed waste. Advances in bioavailability technologies and chelated mineral formulations are improving nutrient uptake efficiency. This growing focus on feed performance and resource optimization is positioning micronutrient-enriched feeds as a cornerstone of modern, sustainable livestock production systems.

Restraints - Fluctuating mineral and vitamin prices are disrupting feed cost stability

Volatile mineral and vitamin prices are increasingly disrupting the stability of feed costs in the global animal feed micronutrients market. Supply chain imbalances, geopolitical tensions, and fluctuating raw material costs for key inputs have led to unpredictable pricing trends. Seasonal variations in crop yields and energy costs further amplify procurement challenges for feed manufacturers. These price swings strain profit margins, forcing producers to reformulate or reduce micronutrient inclusion, which can affect animal health and performance. The heavy reliance on imported feed-grade minerals and vitamins in developing regions compounds the instability, pushing companies to seek local sourcing, recycling, or synthetic alternatives to mitigate exposure to global price shocks.

Opportunity - Capitalizing on the surge in organic livestock and premium feed demand

A strong opportunity is unfolding in the global animal feed micronutrients market as demand accelerates for organic livestock products and premium feed solutions. Consumers increasingly associate animal welfare and clean nutrition with product quality, driving farmers to eliminate synthetic additives and adopt micronutrients sourced from plants, algae, or other natural origins. Feed manufacturers developing certified organic or naturally chelated mineral blends stand to gain from this shift. Premium feed segments for poultry, dairy, and aquaculture are expanding as producers seek nutrient-dense, residue-free formulations that enhance animal immunity and yield. Startups focusing on traceable supply chains, fermentation-based vitamin production, and eco-friendly mineral processing technologies are well-positioned to capture growth in this evolving, sustainability-driven market landscape.

Category-wise Analysis

By Livestock, Poultry dominates the animal feed micronutrients market

Poultry accounts for approximately 46% of the market share as of 2024, driven by the sector’s vital dependence on micronutrients to support rapid growth, egg production, and immunity in layers and broilers. As poultry is among the most intensively farmed livestock categories worldwide, maintaining feed efficiency and flock health remains essential to profitability. The use of trace minerals, vitamins, and amino acid blends improves feed conversion and meat quality. Conversely, ruminants like cattle and sheep require micronutrients to optimize rumen function and milk production.

Swine feed remains the second-largest segment, with micronutrients enhancing reproduction and lean meat yield. Aquaculture applications are expanding as fortified feeds prevent vitamin deficiencies in fish, while the growth of equine feed remains limited due to declining ownership and high feed costs.

By Nutrient Type, vitamins are expected to show promising growth during the forecast period

Vitamins are projected to grow at a CAGR of 7.9% during the forecast period, supported by their expanding role in improving livestock productivity, disease resistance, and fertility. With growing awareness among farmers about the importance of balanced micronutrient intake, vitamin-enriched feeds are becoming essential for maintaining animal health and product quality. The demand for vitamins A, D, E, and the B-complex is surging, as they play key roles in metabolism, bone health, and immune modulation.

Innovations in feed-grade vitamin stabilization and encapsulation technologies are enhancing nutrient bioavailability and shelf life. As antibiotic use in animal farming continues to decline, vitamins are gaining prominence as natural alternatives to boost growth and overall vitality across poultry, swine, and ruminant production systems.

Region-wise Insights

Asia Pacific Animal Feed Micronutrients Market Trends

Asia Pacific holds approximately 35% market share in the global animal feed micronutrients market, driven by rapidly expanding livestock and aquaculture industries across the region. In China, demand for fortified feed is rising to support high pork and poultry production, with micronutrients enhancing growth, immunity, and reproductive performance. India’s dairy and poultry sectors are increasingly adopting vitamin- and mineral-enriched feeds to meet rising milk and meat consumption, while precision feeding practices are gaining traction.

Japan focuses on functional feed solutions for poultry and aquaculture, integrating vitamins and trace minerals to improve health and product quality. Australia emphasizes sustainable and high-quality livestock production, with fortified feed contributing to animal welfare and export-ready meat. Regional manufacturers are investing in bioavailable and encapsulated micronutrients to optimize feed efficiency and livestock performance.

Latin America Animal Feed Micronutrients Market Trends

The Latin America animal feed micronutrients market is expected to grow at a CAGR of 6.9%, driven by the expansion of the processed food, nutraceutical, and beverage industries. Brazil dominates the region, supported by its large cattle and poultry industries and strong feed production infrastructure, followed by Argentina and Mexico, which are enhancing their feed production capabilities. The market in Latin America is further driven by the region’s expanding cattle, poultry, and swine sectors.

Rising meat exports, urbanization, and increased protein consumption are prompting farmers to adopt nutrient-rich feed formulations to improve animal health and productivity. Micronutrients such as zinc, copper, and manganese are increasingly being incorporated to support immunity and growth. Additionally, technological advancements and the rise of commercial farming practices are creating significant opportunities for feed manufacturers across the region.

Europe Animal Feed Micronutrients Market Trends

Rising seafood demand in Europe is creating opportunities for specialized aquafeed formulations, particularly in countries such as Spain and Norway. Use of food industry by-products in feed formulations to reduce waste and improve sustainability aligns with the EU’s circular economy goals, thus boosting the demand for animal feed. Additionally, the shift toward precision nutrition and sustainable feeding practices is fueling demand for advanced micronutrient solutions, including organic and bioavailable mineral sources. The expansion of intensive livestock operations, particularly in the poultry and swine sectors, amplifies the need for optimized feed efficiency to meet growing protein consumption trends.

U.S. Animal Feed Micronutrients Market Trends

U.S. regulations on feed safety and additive compliance encourage the use of scientifically validated micronutrients, reducing reliance on antibiotics and promoting animal welfare. These stringent regulatory standards on feed safety and quality further accelerate market adoption, as producers seek compliance while maintaining efficiency. Adoption of precision nutrition and sensor-enabled dosage systems enables accurate micronutrient supplementation, improving productivity and reducing waste. All these factors are expected to drive market growth, driven by rising demand and consumption of micronutrients as animal feed in the U.S.

Market Competitive Landscape

The animal feed micronutrients market is highly competitive, with several key players focusing on product innovation and geographical expansion. Leading companies such as Cargill, Archer Daniels Midland (ADM), Nutreco, and Zinpro Corporation dominate the market by offering a wide range of micronutrient products, including zinc, copper, and manganese, for enhanced livestock performance.

Companies are increasingly investing in research and development to create more efficient and bioavailable micronutrients, such as chelated minerals, which improve absorption in animals. Regional players in emerging markets are gaining momentum by delivering cost-effective solutions tailored to local requirements. Additionally, strategic mergers, acquisitions, and partnerships are prevalent as firms aim to strengthen their market position and address the growing demand for advanced animal nutrition.

Key Industry Developments:

- In November 2025, Cargill Animal Nutrition & Health completed a major expansion of its Engerwitzdorf, Austria, facility, boosting production capacity by 50%. The expansion strengthens Cargill’s ability to meet surging demand for advanced micronutrition solutions and reinforces its commitment to innovation and customer growth.

- In October 2025, BASF SE launched Lutavit® A/D3 1000/200 NXT, a next-generation microencapsulated vitamin blend combining vitamins A and D3. The innovation enhances nutrient stability and feed efficiency, reinforcing BASF’s focus on sustainable, high-performance animal nutrition solutions.

- In September 2025, ADM and Alltech announced plans to form a North American animal feed joint venture, set to launch in early 2026. The partnership will combine ADM’s 15 U.S. feed mills with Alltech’s 33 U.S. and Canadian facilities, enhancing production scale and regional customer reach.

Companies Covered in Animal Feed Micronutrients Market

- BASF SE

- ADM

- dsm-firmenich

- Balchem Corporation

- Alltech Inc.

- Cargill, Incorporated

- Kemin Industries

- Lallemand Inc.

- Nutreco N.V.

- Novus International, Inc.

- Purina Animal Nutrition LLC

- Zinpro Corporation

- Bluestar Adisseo Company

- AG Solutions

- Others

Frequently Asked Questions

The global Animal Feed Micronutrients market is projected to be valued at US$1,821.3 Mn in 2025.

Increasing emphasis on feed efficiency to achieve rapid animal growth and higher output is fueling the demand for Animal Feed Micronutrients in the global market.

The global Animal Feed Micronutrients market is poised to witness a CAGR of 6.7% between 2025 and 2032.

Capitalizing on the surge in organic livestock and premium feed demand represents a major market opportunity. Precision nutrition and sustainable feeding practices are showcasing promising market potential.

Major players in the global Animal Feed Micronutrients market include BASF SE, ADM, DSM-Firmenich, Balchem Corporation, Alltech Inc., Cargill, Incorporated, Kemin Industries, Lallemand Inc., and others.