- Animal Health

- Animal Health Active Pharmaceutical Ingredients Market

Animal Health Active Pharmaceutical Ingredients Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Animal Health Active Pharmaceutical Ingredients Market by Animal Type (Companion Animals, Production Animals), by API Type (Antiparasitics, Anti-infectives, NSAIDs & Anesthetics, Others), by Regional Analysis, from 2026 - 2033

Animal Health Active Pharmaceutical Ingredients Market Share and Trends Analysis

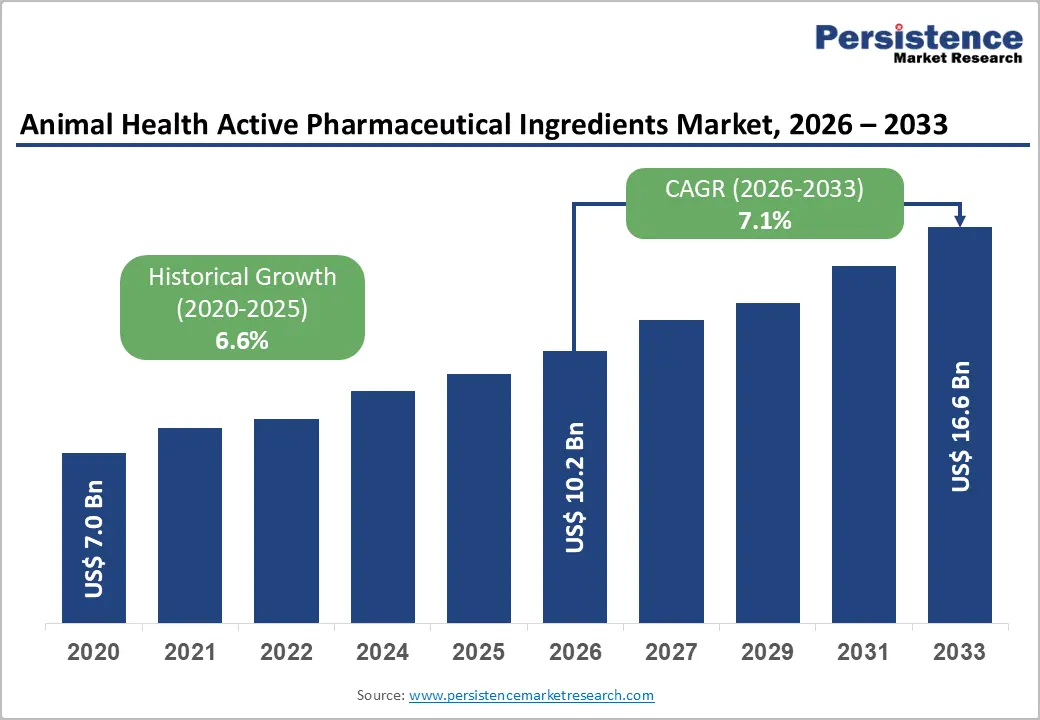

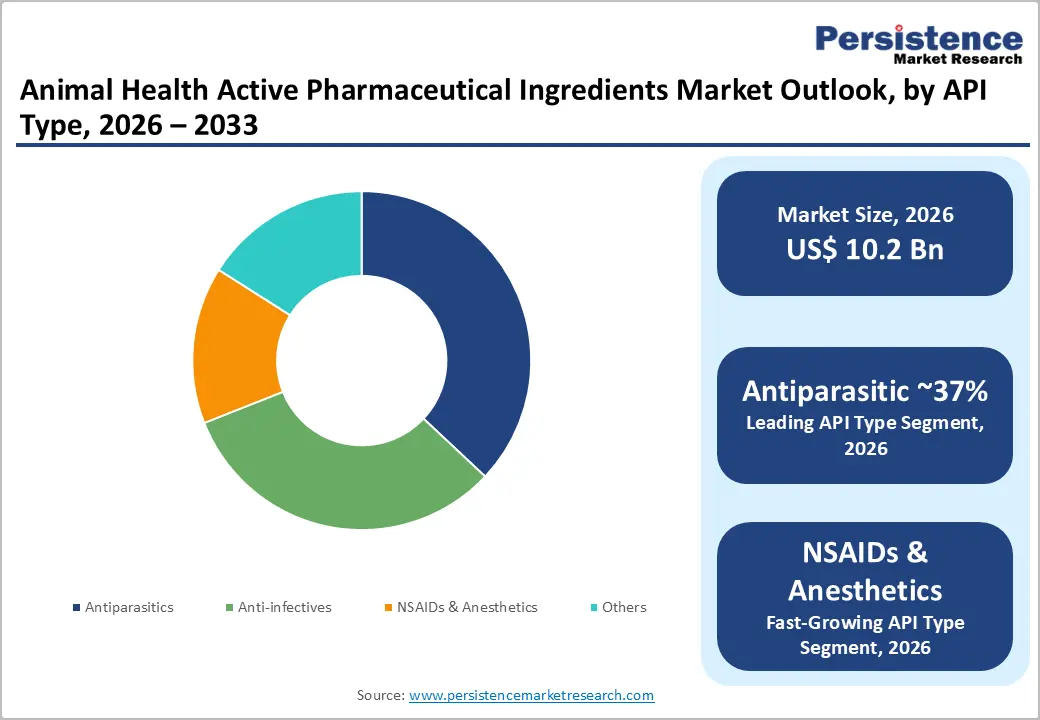

The global animal health active pharmaceutical ingredients market size is estimated to grow from US$ 10.2 billion in 2026 to US$ 16.6 billion by 2033, at a CAGR of 7.1% from 2026 to 2033. The rapidly growing animal health market is a primary driver of growth for animal health active pharmaceutical ingredient (API) market.

Factors such as growing focus on animal well-being, a surge in the number of animal healthcare NGOs, and unmet medical needs act as other major growth drivers in the market. There has been significant growth in the antiparasitic API landscape owing to the abundance of pharmaceutical companies in the Asia Pacific region that are involved in the development of antiparasitic APIs. Anti-infectives are the other segment in the market that is growing rapidly, contributing to significant market revenue.

Key Industry Highlights:

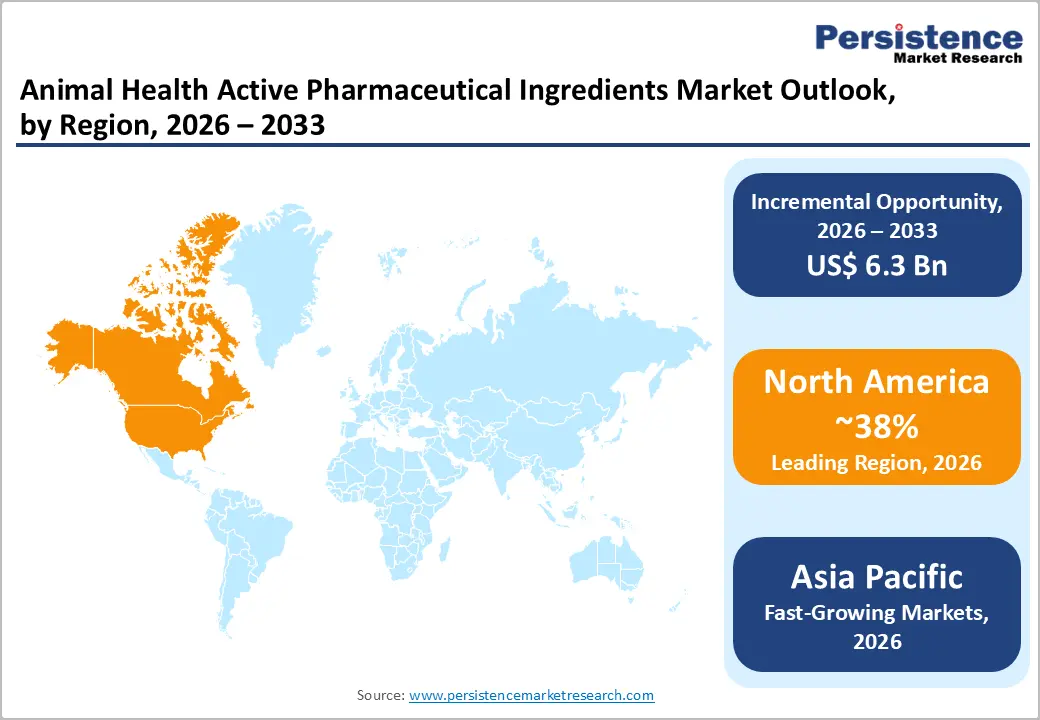

- Leading Region: North America remains the largest market, supported by strong veterinary drug manufacturing capabilities, advanced R&D, and increasing spending on animal healthcare.

- Fastest Growing Region: Asia Pacific is projected to grow at the fastest pace, driven by a large livestock population, increasing pet ownership, and expansion of veterinary API production facilities.

- Dominant Segment: Antiparasitics hold the largest market share due to widespread need for parasite control in livestock and companion animals, along with routine preventive treatments.

- Key Distribution Channel: NSAIDs & anesthetics are the fastest-growing API category driven by chronic pain treatment, surgical procedures, and improved safety-focused veterinary formulations.

| Key Insights | Details |

|---|---|

|

Animal Health Active Pharmaceutical Ingredients Market Size (2026E) |

US$ 10.2 Bn |

|

Market Value Forecast (2033F) |

US$ 16.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.6% |

Market Dynamics

Driver - Expanding Pet Ownership and Premiumization of Animal Care

The steady increase in companion animal ownership across both developed and emerging markets has materially changed spending patterns in veterinary healthcare. Today, families treat their pets like close family members and readily spend money on immediate treatments, check-ups, preventive medicines, and health-related services that keep their pets well for a longer time. This shift directly elevates demand for specialised APIs used in chronic conditions, supportive therapies, and post-surgical care such as NSAIDs, pain-modulating agents, dermatology-specific actives, and endocrine-related APIs. Clinics are prescribing higher-quality formulations that demonstrate better tolerability, smoother pharmacokinetics, and improved compliance, especially in aging animal populations.

Parallel to changing consumer attitudes, structured health financing mechanisms for pets are steadily gaining traction, especially in markets where insurance penetration is rising. Insurance coverage for consultations, diagnostics, and branded formulations has reduced immediate cost barriers, encouraging veterinarians to choose more sophisticated therapies. Additionally, premiumisation has influenced purchasing channels, with specialized clinics, branded pharmacies, and subscription-based veterinary plans becoming common. As a result, manufacturers are allocating greater R&D budgets toward differentiated APIs those suitable for species-specific dosing, modified-release formats, and improved bioavailability which collectively strengthen overall demand in the veterinary active pharmaceutical ingredient space.

Restraints - Stringent Regulatory Requirements and Compliance Costs

Veterinary API development operates within a highly controlled regulatory environment, where authorities closely monitor manufacturing quality, product purity, residue limits, and antimicrobial stewardship standards. Meeting expectations for GMP certification, analytical validation, stability testing, residue depletion studies, and environmental impact assessments involve significant upfront investment. This financial burden often becomes difficult for small-scale manufacturers, forcing them either to limit geographic expansion or reduce product breadth. Additionally, compliance timelines can stretch product launch cycles, especially for APIs that fall into antimicrobial or endocrine-modulating classes, where review standards are stricter. These barriers can delay commercialization, increase operational overheads, and discourage entry of new suppliers, especially in markets demanding sterile infrastructure or specialized containment facilities.

Opportunity - Innovation in Biologics, Targeted Therapies, and Sustainable Manufacturing

An emerging growth avenue in veterinary APIs lies in the shift from conventional small molecules toward biologically derived actives, including recombinant proteins, monoclonal antibodies, and immune modulators. Companion animals increasingly receive therapies that mirror human pharmaceutical advancements, including targeted drugs for inflammatory disorders, cancer, metabolic dysfunction, and chronic skin conditions. Producing these advanced APIs requires specialized manufacturing environments, advanced purification systems, and proprietary cell lines, enabling higher margins and differentiation for manufacturers willing to invest. This evolution also expands long-term exclusivity potential, as biologics often face fewer generic threats.

Simultaneously, sustainability initiatives are reshaping procurement preferences. Regulatory bodies and veterinary pharmaceutical companies are beginning to evaluate suppliers based not only on cost and availability but also on waste handling, solvent reduction, carbon footprint, and overall environmental safety. Manufacturers adopting greener synthesis routes, single-use bioprocessing, solvent recycling, or low-emission manufacturing systems can strengthen their appeal in global sourcing networks. These developments also align with livestock producers’ sustainability goals and companion animal brands that market “clean label” therapeutic products. Collectively, innovation-driven platforms and sustainability-aligned supply models offer a significant competitive runway for API manufacturers looking to differentiate in the animal health ecosystem.

Category-wise Analysis

By Animal Type Insights

The production animals segment dominates the animal health active pharmaceutical ingredients market, accounting for approximately 63% of the market in 2025, as per the given scope. Demand for veterinary drugs for cattle, poultry, and swine continues to rise as producers work to improve productivity, prevent infectious diseases, and comply with strict health and safety regulations. Growing global consumption of meat, eggs, and dairy products has increased the need for effective pharmaceutical ingredients to safeguard herd health. Several companies target this segment by offering drugs for parasite control, respiratory infections, metabolic disorders, and other conditions affecting livestock.

The companion animal segment is projected to record the fastest growth during the forecast period. Higher spending on pet healthcare, increased pet ownership, and greater acceptance of veterinary insurance are encouraging the use of advanced medicines. Veterinary practices now prescribe specialized treatments for chronic pain, skin disorders, and endocrine conditions. This is prompting manufacturers to develop improved APIs, new delivery forms, and species-specific formulations to meet evolving expectations in the companion animal space.

By API Type

Within the API type, antiparasitics hold the largest revenue share in 2025, supported by constant demand for parasite control in livestock and pets. Livestock producers routinely administer products for internal worms, external mites, and protozoal infections due to their direct impact on feed conversion, milk yield, and animal weight gain. Regular deworming programs and herd-level preventive dosing make antiparasitic ingredients essential in commercial farming.

Demand is equally strong in the companion animal segment, where veterinarians widely recommend preventive treatments for fleas, ticks, and heartworm. Pet owners increasingly follow monthly or seasonal preventive schedules, sustaining consistent API use. Another growth driver is the introduction of advanced multi-ingredient formulations that combine endectocides with ectoparasite control. These products reduce dosing frequency, improve treatment compliance, and support premium pricing. Together, these factors reinforce the dominant position of antiparasitics within the animal health API market across both therapeutic and commercial applications.

Region-wise Insights

North America Animal Health Active Pharmaceutical Ingredients Market Trends

In North America, the U.S. leads the veterinary API manufacturing landscape, backed by strong R&D infrastructure, advanced manufacturing capabilities, and higher adoption of innovative veterinary therapies. The country continues to invest in biotechnology platforms, fermentation systems, and integrated supply chains that support large-scale API production. A notable development includes the October 2023 collaboration between SUANFARMA and Willow Biosciences, where strain optimization technologies were applied to produce anti-infective APIs more efficiently, improving economic viability and sustainability.

Increasing pet ownership and a high prevalence of chronic diseases in companion animals are further influencing market growth, encouraging the development of improved active ingredients.

Canada is positioned for significant expansion due to public funding initiatives, university-led biological research, and domestic collaborations between contract manufacturers and veterinary drug companies. These factors are enabling advancements in sustainable production methods and biologically derived APIs. Growing regulatory clarity, attention to livestock disease prevention, and rising animal health investments are expected to support consistent demand in the region.

Asia Pacific Animal Health Active Pharmaceutical Ingredients Market Trends

The Asia Pacific region is anticipated to witness rapid growth, supported by increasing animal health awareness, expanding livestock numbers, and improving veterinary access across key markets. The region is also becoming a strong manufacturing base as companies invest in cost-efficient facilities, contract production capacity, and technology upgrades. China holds the highest share due to its sizeable livestock sector, growth of commercial poultry and swine farms, and rising companion animal ownership in urban areas. Strong demand for veterinary drugs and feed additives is prompting regulators to tighten GMP compliance from 2026 onward, which may encourage consolidation and prioritize high-quality producers.

India is emerging as an attractive export-oriented manufacturing hub, strengthened by an established pharmaceutical ecosystem, cost-effective production, and expansion by leading players. Sai Life Sciences' dedicated veterinary API facility, commissioned in September 2025, reflects this shift toward high-value therapeutic segments. Increasing outsourcing by multinational veterinary companies and domestic consumption growth are expected to reinforce Asia Pacific as a preferred supply destination.

Competitive Landscape

The market shows moderate concentration but is gaining momentum due to the presence of major pharmaceutical companies, CMOs, and smaller specialist firms. Large multinational players hold substantial share because of strong capabilities, varied portfolios, and wider global reach, shaping competition and product direction. Some companies specialise in API manufacturing, focusing on certain therapies or animal types. Growth is further driven by advancements in technology, continued R&D spending, and regulatory alignment. Rising innovation, improved formulations, and expanding manufacturing capacities are enabling faster development and greater availability of veterinary APIs.

Key Industry Developments:

- In September 2025, Sai Life Sciences launched Unit VI in Bidar as a specialized veterinary API facility, expanding manufacturing capacity, improving regulatory alignment, and strengthening sustainable operations to address rising global demand for premium animal health APIs.

- In November 2024, Elanco Animal Health took over the Speke, UK, contract manufacturing site from the bankrupt TriRx Speke Ltd., ensuring the continued supply of key farm animal products and reinforcing its global supply network.

Companies Covered in Animal Health Active Pharmaceutical Ingredients Market

- Zoetis

- Alivira Animal Health Ltd.

- Ofichem Group

- Chempro Pharma Pvt. Ltd.

- Siflon Drugs

- Qilu Animal Health Products Co., Ltd.

- Vetpharma

- SUANFARMA

- MENADIONA

- Excel Industries Ltd.

- Others

Frequently Asked Questions

The global animal health active pharmaceutical ingredients market is projected to be valued at US$ 10.2 Bn in 2026.

Rising livestock diseases, pet ownership, antibiotic-free demand, biologics adoption, and outsourcing to compliant API manufacturers drive market expansion globally.

The global animal health API market is poised to witness a CAGR of 7.1% between 2026 and 2033.

Biologics-based veterinary APIs, HPAPI capacity, sterile injectables, pet-specific formulations, and Asia Pacific contract manufacturing present strong multi-year commercialization opportunities.

Major players include Zoetis, Alivira Animal Health Ltd., Ofichem Group, and Chempro Pharma Pvt. Ltd.