- Metals & Minerals

- Aluminum Market

Aluminum Market Size, Share, and Growth Forecast 2026 - 2033

Aluminum Market by Source (Primary Aluminum, Secondary Aluminum), Industry (Automotive, Transport, Packaging, Construction, Consumer Durables, Machinery & Equipment, Electricals, Misc.), Product (Rolled, Extruded, Forged, Casting, Wires & Cables, Misc.), by Regional Analysis, 2026 - 2033

Aluminum Market Size and Trend Analysis

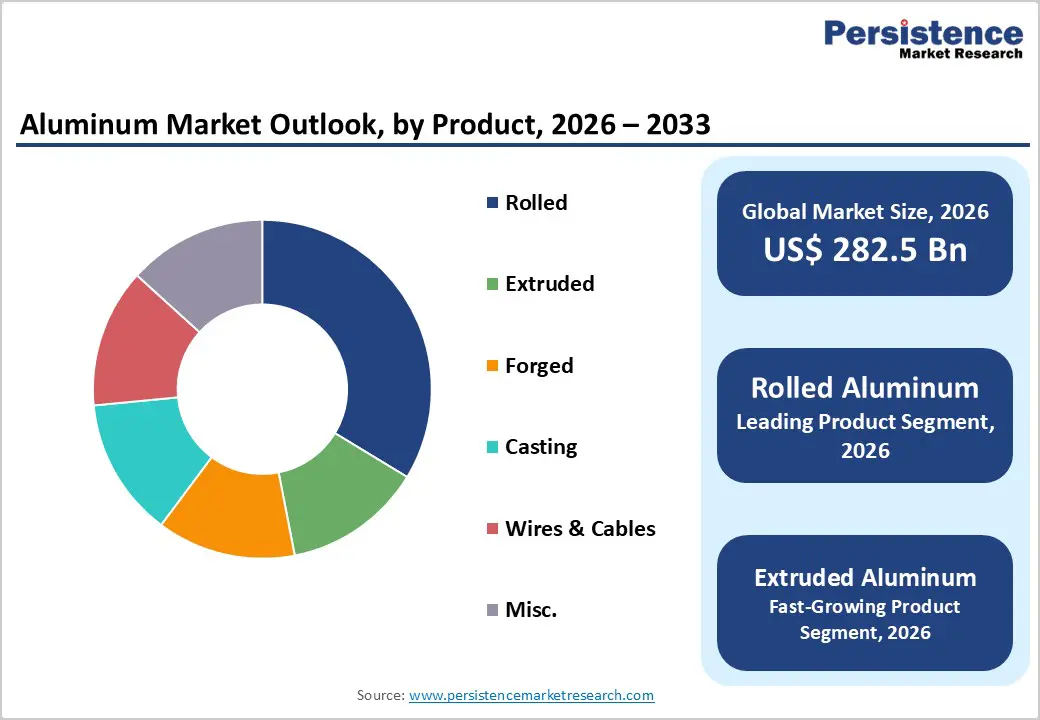

The global Aluminum market size is expected to be valued at US$ 282.5 billion in 2026 and projected to reach US$ 493.6 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033.

This sustained growth is supported by aluminum’s unique combination of low density, high corrosion resistance, infinite recyclability, and superior electrical conductivity, making it essential across the world’s most dynamic industries. The global shift to electric vehicles is a major structural driver, with the International Energy Agency reporting that global EV sales exceeded 17 million units in 2024, a 25% year-on-year increase, boosting demand for lightweight aluminum body structures and battery enclosures. At the same time, large-scale infrastructure programmes in Asia Pacific, the Middle East, and Africa are increasing demand for construction-grade aluminum, while circular economy initiatives are accelerating the adoption of energy-efficient secondary aluminum production worldwide.

Key Industry Highlights

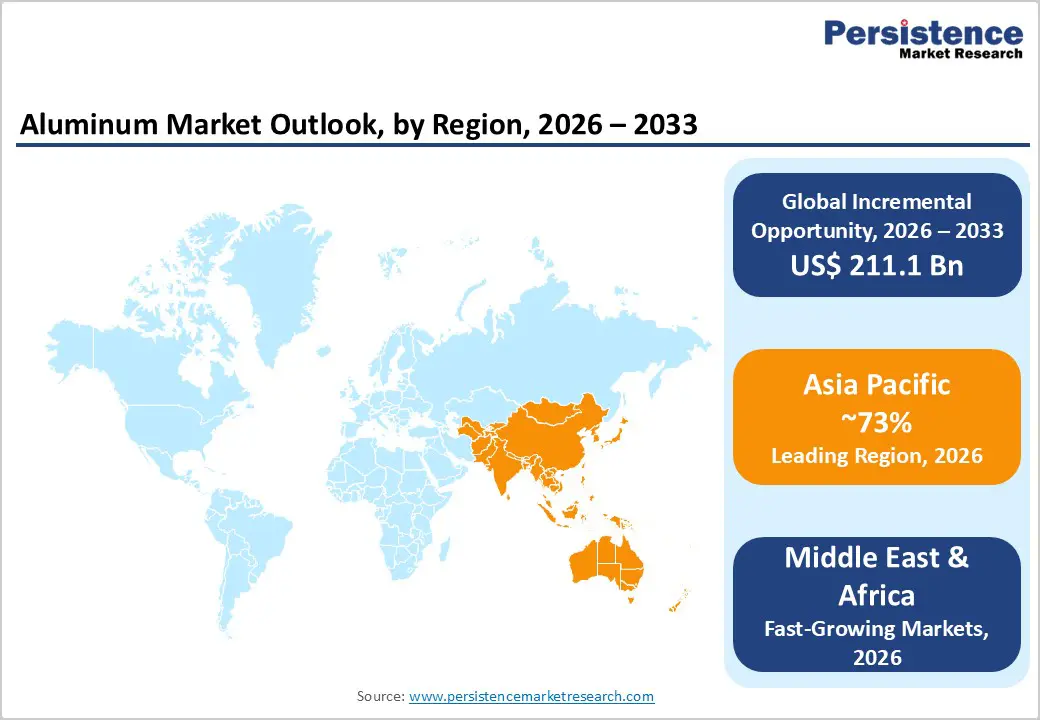

- Leading Region: Asia Pacific commands approximately 73% of the global aluminum market value in 2025, anchored by China’s primary output of approximately 43 million metric tons, robust growth in India, and vast downstream demand from the region’s automotive, construction, and packaging sectors that continue to outpace all other regions.

- Fastest-Growing Region: The Middle East & Africa region is projected to register the highest growth CAGR over 2026–2033, driven by flagship infrastructure programmes such as Saudi Vision 2030, UAE mega-projects, and rapidly expanding construction, consumer durables, and packaging industries across Gulf Cooperation Council and sub-Saharan economies.

- Dominant Product Segment: Rolled aluminum leads all product categories with approximately 35% market share in 2025, owing to its pervasive deployment across automotive body panels, aerospace sheet, beverage can stock, and architectural cladding, markets that collectively span the broadest range of industries consuming aluminum globally.

- Fastest-Growing Segment: Extruded aluminum is the fastest-growing product segment, propelled by surging demand from EV battery frame structures, solar racking systems, and architectural facades across Asia Pacific and North America, with the extrusion sector holding ~31.5% of product revenues in 2025 and projected to record the highest forecast CAGR through 2033.

- Key Market Opportunity: Secondary aluminum, consuming less than 5% of primary smelting energy, presents the single largest structural opportunity. OEM Scope 3 mandates, EU CBAM, and PPWR policies are driving certified low-carbon aluminum demand, with secondary production forecast to reach 40.6 million metric tons by 2030 at a CAGR of 5.3%.

| Key Insights | Details |

|---|---|

|

Aluminum Market Size (2026E) |

US$ 282.5 Billion |

|

Market Value Forecast (2033F) |

US$ 493.6 Billion |

|

Projected Growth CAGR (2026–2033) |

8.3% |

|

Historical Market Growth (2020–2025) |

7.8% CAGR |

Market Dynamics

Drivers - Accelerating Adoption of Aluminum in Electric and Conventional Automotive Manufacturing

The automotive sector remains the most influential demand driver for aluminum, contributing about 30% of total global aluminum consumption in 2025. A key principle in vehicle engineering shows that reducing vehicle weight by 10% improves fuel efficiency by 6%–8%, making aluminum’s 60% weight advantage over steel highly attractive for automakers facing stricter emission regulations worldwide. In the United States, Corporate Average Fuel Economy (CAFE) standards require fleet-wide fuel efficiency targets, while the European Union limits CO? emissions to 95 grams per kilometre for new passenger cars.

The growth of electric vehicles has intensified this trend, as lightweight aluminum components in battery enclosures, chassis frames, and body-in-white structures help offset the weight of high-voltage batteries and increase driving range. According to the IEA, global EV sales surpassed 17 million units in 2024, marking a 25% year-on-year rise and creating a strong long-term demand base for aluminum across both primary and fabricated products.

Rapid Urbanisation and Infrastructure Investment in Emerging Economies

Urbanisation at an unprecedented pace across Asia Pacific, Latin America, Middle East, and Africa is generating structural demand for aluminum in construction, electrical transmission, and consumer durables. Aluminum’s corrosion resistance, formability, and aesthetic versatility make it the preferred material for window frames, curtain walls, structural facades, roofing panels, and power distribution infrastructure in rapidly developing urban environments. In India, the government’s Union Budget for 2024–25 allocated US$ 32 billion specifically toward rural development and infrastructure enhancement, creating direct downstream demand for construction-grade aluminum.

China’s sustained urbanisation programme, alongside its position as the world’s largest aluminum producer at approximately 43 million metric tons in 2024 (US Geological Survey), ensures a deeply integrated supply-demand ecosystem. In the Middle East, flagship initiatives such as Saudi Vision 2030 and the UAE National Infrastructure Plan are channelling hundreds of billions of dollars into aluminum-intensive mega-projects, including smart cities, transportation networks, and renewable energy installations, adding significant new growth frontiers beyond historically dominant markets in North America and Europe.

Restraints - High Energy Intensity and Volatile Input Cost Structure

Primary aluminum smelting is one of the most energy-intensive industrial processes globally, consuming approximately 14–15 megawatt-hours of electricity per metric ton of metal produced. Energy costs alone represent 30%–40% of total production expenditures, making aluminum producers acutely vulnerable to electricity price volatility and energy supply disruptions. The Russia–Ukraine conflict triggered record energy price spikes across Europe, rendering numerous EU primary smelters economically unviable and accelerating capacity curtailments.

According to Eurostat, the European Union recorded an aluminium trade deficit of EUR 11.1 billion in 2024, as domestic primary output declined sharply and import dependence deepened. Concurrently, volatile bauxite and alumina prices further compress smelter margins, deterring greenfield capacity investment in energy-expensive regions and concentrating new capacity in low-energy-cost jurisdictions such as Middle East and Asia.

Escalating Trade Policy Barriers and Geopolitical Supply Chain Disruptions

Escalating trade policy barriers and geopolitical supply chain disruptions are increasingly shaping the global aluminum market, affecting both pricing and investment confidence. The Trump administration’s 50% import tariffs on steel and aluminum entering the United States in 2025 disrupted long-established trade routes, with U.S. aluminum imports valued at approximately US$ 28.3 billion in 2024, sourced mainly from Canada (52%), UAE (8%), and Bahrain (4%). These tariffs drove the Platts U.S. Midwest Transaction premium from 18.8 to 23.8 cents per pound by mid-January 2025, significantly raising downstream manufacturing costs and constraining domestic investment in aluminum production and fabrication.

Adding to market volatility, the ongoing U.S., Israel – Iran conflict has caused supply-side disruptions, including strikes on Gulf smelters and shipping delays through the Strait of Hormuz. This geopolitical tension has pushed aluminum prices toward multi-year highs of around $3,500 per tonne and created heightened uncertainty for automotive, construction, and packaging industries that rely heavily on imported and lightweight aluminum materials.

Opportunities - Secondary Aluminum Expansion and the Circular Economy Transition

The global momentum toward a circular economy presents one of the most financially compelling opportunities in the aluminum industry. Recycling aluminum consumes less than 5% of the energy required to produce primary metal, delivering dramatic cost savings and greenhouse gas (GHG) emission reductions that align with the Paris Agreement net-zero commitments of governments and corporations alike. Globally, 75% of all aluminum ever produced is estimated to remain in active use, a testament to the metal’s infinite recyclability without quality degradation. Global secondary aluminum production stood at 28.3 million metric tons in 2023 and is projected to reach 40.6 million metric tons by 2030 at a CAGR of 5.3%. Companies that invest early in advanced scrap-sorting, secondary alloy development, and closed-loop collection systems are positioned to command significant pricing premiums, especially as the EU’s Carbon Border Adjustment Mechanism (CBAM) and similar policies increasingly penalise carbon-intensive primary production. Emirates Global Aluminium (EGA) completed the expansion of its Spectro Alloys recycling subsidiary in the U.S. in January 2025, while Novelis has committed to achieving a 90% recycling rate across all its products by 2030, illustrating how leading producers are already commercializing this structural shift.

Green and Low-Carbon Aluminum Demand from OEMs and Packaging Converters

Stringent Scope 3 emission reduction commitments by global automotive OEMs and fast-moving consumer goods companies are driving a structurally growing premium market for certified low-carbon aluminum. In November 2024, Kobe Steel launched Kobenable Aluminum to help customers cut Scope 3 emissions across supply chains. The packaging industry is also shifting, as BlueTriton Brands introduced aluminum bottle packaging for five flagship brands in April 2024, reflecting a move from plastic to infinitely recyclable aluminum. The EU Packaging and Packaging Waste Regulation, adopted in December 2024 and effective August 2026, requires packaging redesign for better recyclability, favoring aluminum over multi-layer plastics. The International Aluminium Institute and industry associations emphasize aluminum’s recyclability as a key advantage. Producers with clean-energy-backed, certified low-carbon supply chains, particularly in Norway, Canada, and the Middle East, using hydroelectric or solar power, are well-positioned to secure long-term premium supply contracts in this growing green-materials market.

Category-wise Analysis

Source Insights

Primary aluminum holds the dominant position in the global aluminum market by source, commanding an estimated 72% revenue share in 2025. This commanding lead reflects the continued scaling of greenfield smelter capacity across China, India, the Middle East, and Southeast Asia, regions that collectively account for the majority of global capacity additions in recent years. The International Aluminium Institute (IAI) recorded world primary aluminium production of 36.459 million metric tons in the first half of 2025, up from 35.960 million metric tons in the corresponding period of 2024. China’s annualised primary production reached approximately 44 million metric tons in Q1 2025, approaching the government-mandated 45-million-tonne cap established in 2017.

Secondary aluminum is the fastest-growing source segment within this category, benefiting from rapid expansion of recycling infrastructure driven by circular economy mandates, energy cost advantages, and growing end-user preference for low-carbon certified metal. Global secondary production is on a trajectory to reach 40.6 million metric tons by 2030 (CAGR of 5.3%), compared to a CAGR of approximately 2.0% for primary production over the same forecast horizon, signalling a gradual but structural shift in the source mix of global aluminum supply toward secondary metal.

Industry Insights

The automotive industry leads all end-use segments in the global aluminum market, capturing approximately 30% of total revenue in 2025. This leadership position is anchored in the industry’s relentless focus on vehicle lightweighting to comply with increasingly stringent emission and fuel economy regulations across major markets. Aluminum’s unique combination of a 60% weight reduction versus conventional steel, while maintaining high tensile strength and excellent crash-energy absorption, makes it the material of choice for body-in-white structures, powertrain housings, suspension components, heat exchangers, and battery enclosures in both internal combustion engine and electric vehicle platforms.

The electric vehicle sub-segment is the fastest-growing industry application, propelled by EV sales of 17 million units globally in 2024 and accelerating battery platform aluminium-intensity per vehicle. The construction, packaging, and electrical end-use segments collectively account for the majority of remaining demand, driven respectively by infrastructure spending in developing nations, the global shift away from single-use plastics, and the expansion of renewable energy transmission grids demanding high-conductivity aluminum cable.

Product Analysis

Rolled aluminum is the leading product segment in the global aluminum market, accounting for approximately 35% of total product revenue in 2025. Flat-rolled products, encompassing sheet, plate, and foil, serve the broadest and most diverse array of end markets, including automotive body panels, aerospace fuselage skins, marine structures, beverage can stock, and architectural cladding, a breadth of application that underpins their structural market leadership. Novelis Inc., a subsidiary of Hindalco Industries, is recognised as the world’s largest aluminium rolling company, supplying automotive-grade sheet and beverage-can body stock across operations in North America, Europe, Asia, and South America.

Extruded aluminum is the fastest-growing product segment, driven by structural demand tailwinds in EV battery frames, solar racking systems, architectural facades, and heat exchanger components. The extrusion segment held approximately 31.5% share in 2025 and is forecast to register the highest growth CAGR through 2033. Casting, forging, and wires & cables round out the product landscape, with wire and cable products benefiting from expanding high-voltage transmission infrastructure linked to global renewable energy programmes that increasingly rely on aluminum’s superior conductivity-to-weight ratio versus copper.

Regional Insights

North America Aluminum Market Trends and Insights

The United States anchors the North American aluminum market, commanding the region’s largest share driven by robust demand from its automotive, aerospace, packaging, and construction industries. CAFE fuel efficiency mandates and EPA emission standards are compelling automakers to systematically increase aluminum content per vehicle, while the accelerating domestic EV market, led by Tesla, General Motors, and Ford, is amplifying demand for lightweight structural aluminum. The U.S. Census Bureau reported total domestic construction spending at approximately US$ 486 billion, a strong pipeline indicator for architectural aluminum demand. The University of Michigan and Norsk Hydro ASA committed to a USD 2.5 million research initiative in 2025 focused on advancing aluminium recycling processes and alloy development.

However, the region faces material headwinds from aggressive trade policy. The 50% import tariff on all aluminium imports into the U.S. introduced in 2025 drove the Platts Midwest Transaction premium sharply higher, inflating downstream input costs for manufacturers. Domestic primary smelter capacity has contracted significantly, declining to 1.36 million tons per year from 1.64 million tons per year in 2022 per USGS data, as high energy costs render several smelters uncompetitive. In Canada, a 432,000-tonne-per-year smelter in British Columbia returned to full production in October 2023, providing a partial supply offset for the regional market. Aluminium imports from Canada continue to supply 52% of U.S. import requirements, reinforcing the bilateral trade dependency.

Europe Aluminum Market Trends and Insights

Europe’s aluminum market is defined by the tension between structurally robust downstream demand from its world-class automotive and packaging industries and acute challenges in primary production competitiveness. Germany, France, U.K., and Spain are the leading consuming nations, collectively accounting for the majority of the region’s aluminum demand through their automotive manufacturing clusters, aerospace supply chains, and premium food and pharmaceutical packaging sectors. Eurostat confirmed that the EU imported EUR 29.5 billion worth of aluminium and related articles in 2024, against exports of only EUR 18.4 billion, resulting in a trade deficit of EUR 11.1 billion, a structural imbalance that reflects the erosion of European primary smelter competitiveness under elevated energy costs.

Policy is increasingly reshaping the European aluminum procurement landscape. The EU Carbon Border Adjustment Mechanism (CBAM), now in its transitional implementation phase, incentivises the use of low-carbon certified aluminum from clean-energy producing nations. The EU Packaging and Packaging Waste Regulation (PPWR), adopted in December 2024 and effective from August 2026, mandates packaging redesign for improved recyclability, further favouring aluminum over multi-layer plastics. In Spain, the 228,000-tonne-per-year San Ciprian smelter approved a restart plan targeting 75% capacity by 2026. In January 2025, Rio Tinto Group and Norsk Hydro ASA jointly committed USD 45 million over five years to develop carbon capture technologies for European and Norwegian smelters, reflecting the industry’s strategic commitment to long-term decarbonisation.

Asia Pacific Aluminum Market Trends and Insights

Asia Pacific dominates the global aluminum market with overwhelming scale, commanding approximately 73% of the market value in 2025. China is the undisputed global hub, producing approximately 43 million metric tons of primary aluminum in 2024 and accounting for ~57% of global primary output per US Geological Survey and IndexBox data. China’s primary aluminium production grew by 2.6% year-on-year in Q1 2025, reaching 10.852 million metric tons according to the International Aluminium Institute (IAI). The Chinese government’s New Energy Vehicle Industry Development Plan (2021–2035) targets 20% EV market penetration by 2025, reinforcing structural aluminium intensity in automotive manufacturing.

India is the region’s fastest-growing aluminum market, with domestic primary production expanding at a CAGR of 8.3% over 2013–2024 (IndexBox). India’s 2024–25 Union Budget earmarked US$ 32 billion for rural infrastructure, channelling demand for construction and electrical-grade aluminum. Vedanta Aluminium, India’s largest primary producer, launched Vedanta Metal Bazaar in February 2024, a digital aluminum trading platform that is transforming domestic procurement. In Japan, demand is driven by high-value aerospace components and automotive body sheet. ASEAN economies including Vietnam, Indonesia, and Thailand are attracting downstream aluminum fabrication investment in electronics, packaging, and automotive supply chains, positioning the broader Asia Pacific region as the single most important growth engine for the global aluminum market through 2033.

Competitive Landscape

The global aluminum market is moderately consolidated at the primary production level, with a few large players controlling a significant share of capacity and influencing global pricing, alloy standards, and decarbonisation trends. Key competitive advantages include renewable-energy-backed low-carbon credentials, proprietary high-strength alloys, vertical integration from raw material to finished products, and access to fast-growing EV and packaging markets. Downstream fabrication is more fragmented, with regional converters and extruders competing through product specialisation, delivery efficiency, and value-added services. Industry strategies increasingly focus on certified green aluminum, expanding recycling capabilities, investing in carbon capture technologies, and securing long-term supply agreements linked to customer decarbonisation goals. This combination of concentrated upstream control and diversified downstream competition, along with a strong emphasis on sustainability, is shaping the market structure and driving strategic alignment across the global aluminum value chain.

Key Developments:

- January 2025: Rio Tinto Group and Norsk Hydro ASA signed a five-year partnership and committed a combined USD 45 million to identify, evaluate, and develop carbon capture technologies for aluminium electrolysis smelters across Europe and Norway, targeting net-zero production by 2050.

- November 2024: Kobe Steel Ltd. launched Kobenable Aluminum, a certified low-CO? aluminum product engineered to help automotive and industrial customers reduce Scope 3 emissions, marking a significant step toward commercialising green aluminum in supply chains.

- February 2024: Vedanta Aluminium, India’s largest primary aluminum producer, introduced Vedanta Metal Bazaar, a first-of-its-kind e-superstore digitising India’s primary aluminum procurement and trading ecosystem, improving price transparency and market access for downstream buyers.

Companies Covered in Aluminum Market

- Aluminum Corporation of China Limited (Chalco)

- China Hongqiao Group Co. Ltd.

- United Company RUSAL IPJSC

- Shandong Xinfa Aluminium Group

- Rio Tinto Group

- Emirates Global Aluminium (EGA)

- State Power Investment Corporation Limited

- Norsk Hydro ASA

- Vedanta Limited

- Alcoa Corporation

- Novelis Inc. (Hindalco Industries)

- Constellium SE

- Century Aluminum Company

- Kobe Steel Ltd.

- Jindal Aluminium Limited

- Kaiser Aluminum Corporation

Frequently Asked Questions

The global aluminum market is estimated at US$ 282.5 billion in 2026 and projected to reach US$ 493.6 billion by 2033, growing at a CAGR of 8.3%.

Key drivers include EV adoption, urbanization-driven construction demand, government infrastructure spending, and circular economy policies promoting secondary aluminum.

Asia Pacific leads, accounting for ~73% of global market value, driven mainly by China and fast-growing markets such as India.

The green and recycled aluminum segment offers major growth due to lower energy use, cost savings, and demand for low-carbon certified metal.

Major producers include China Hongqiao Group, Chalco, RUSAL, Rio Tinto, Norsk Hydro, EGA, Vedanta, Shandong Xinfa, and global downstream leaders like Alcoa, Novelis, and Constellium.