- Metals & Minerals

- Ammonium Fluoride Market

Ammonium Fluoride Market Size, Share, and Growth Forecast 2026 – 2033

Ammonium Fluoride Market by Product Type (Anhydrous, Wet), Form (Solid, Liquid), Grade (Industrial, Electronic, Reagent), Application (Semiconductor Manufacturing, Others), and Regional Analysis 2026 – 2033

Ammonium Fluoride Market Size and Trends Analysis

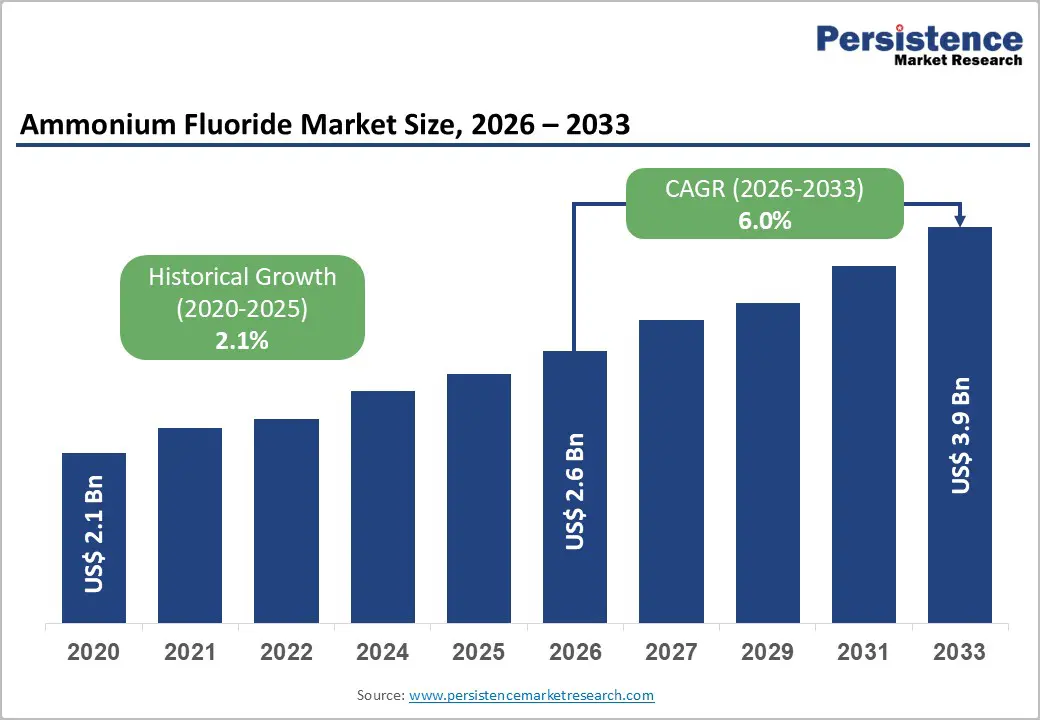

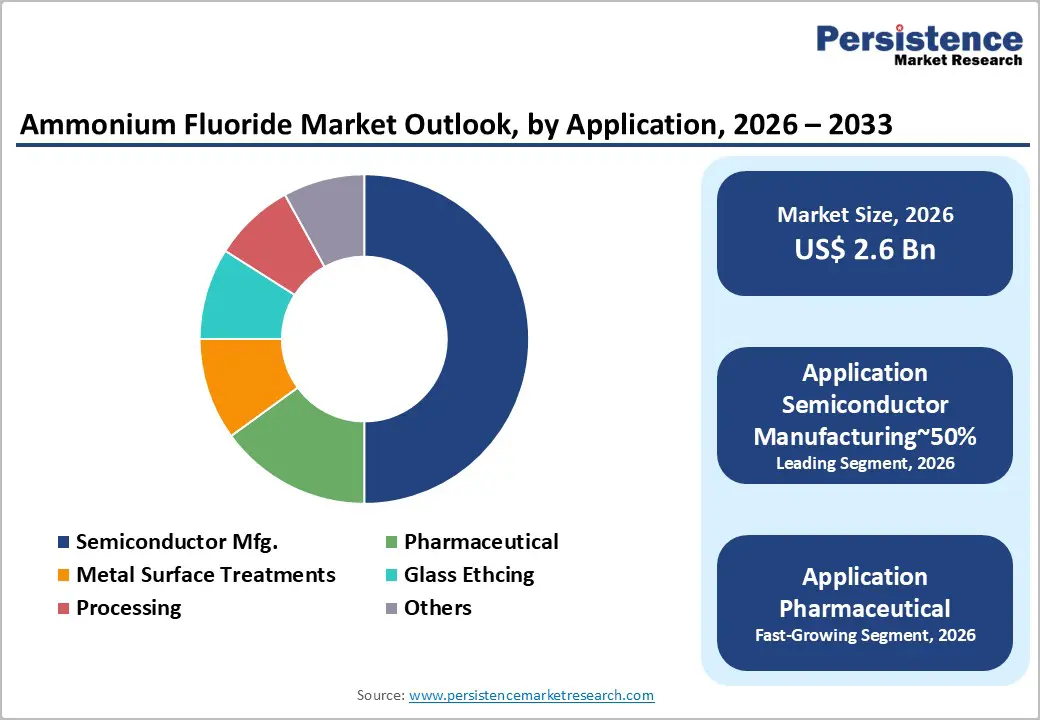

The global ammonium fluoride market size is likely to be valued at US$2.6 billion in 2026 and is expected to reach US$3.9 billion by 2033, growing at a CAGR of 6.0% during the forecast period between 2026 and 2033, driven by the exponential demand for high-purity wet chemicals in the semiconductor manufacturing sector, specifically for etching and cleaning processes essential for 5G and AI chip production. Market momentum is further shaped by global supply chain realignment strategies, particularly the “China Plus One” approach, which is accelerating capacity expansion across Southeast Asia and India.

Key Industry Highlights:

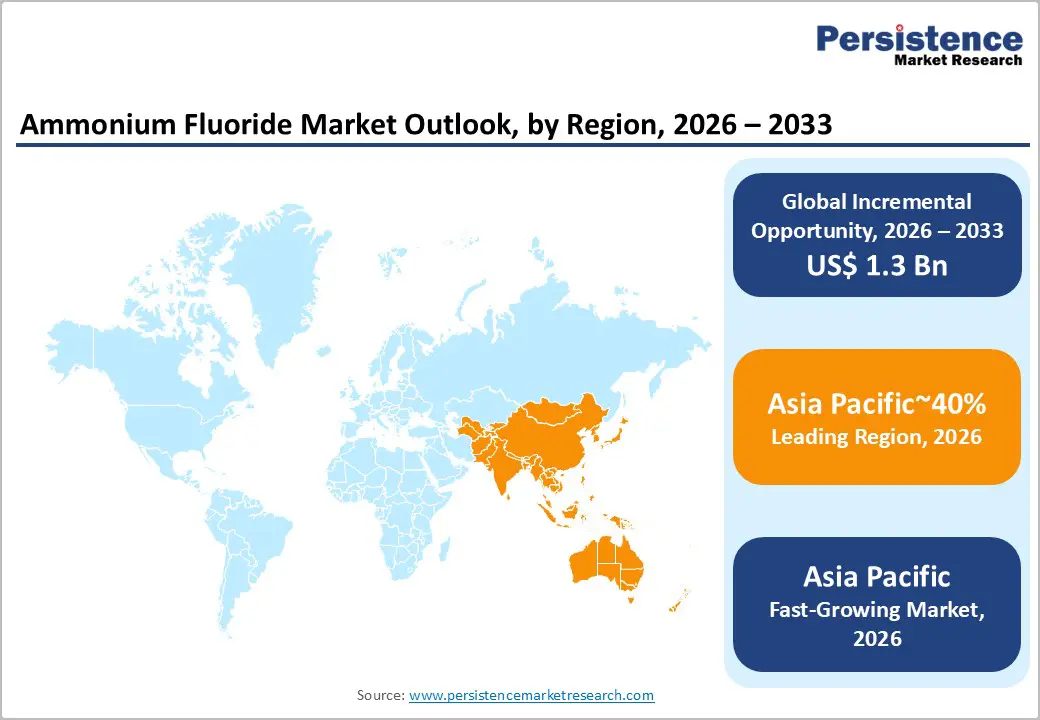

- Leading Market Region: Asia Pacific is expected to lead the ammonium fluoride market with an estimated 40% share in 2026, driven by dominant semiconductor fabrication capacity, high-volume pharmaceutical production, and integrated chemical manufacturing ecosystems.

- Leading Product Type: Wet formulations are projected to remain the leading product type with approximately 70% share, anchored by ultra-high-purity solutions used in semiconductor etching, photovoltaic fabrication, and automated chemical delivery systems.

- Leading Application: The semiconductor segment is anticipated to retain leadership with 52.4% share, driven by precision etching, Buffered Oxide Etch (BOE) solutions, and 3D/3.5D IC packaging in advanced fabs.

- Key Industry Developments: In October 2025, Paradeep Phosphates completed a merger with Mangalore Chemicals & Fertilizers, boosting capacity by 23%. The merger enhanced fertilizer production, including ammonium-based complexes, offering synergies for ammonium fluoride-related agricultural applications.

| Report Attribute | Details |

|---|---|

|

Ammonium Fluoride Market Size (2026E) |

US$2.6 Bn |

|

Market Value Forecast (2033F) |

US$3.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Semiconductor Industry Expansion Driven by AI and Advanced Connectivity

The accelerating expansion of the global semiconductor manufacturing ecosystem remains the dominant driver for ammonium fluoride demand. As chipmakers scale production to support artificial intelligence workloads, advanced connectivity networks, and proliferating connected devices, fabrication facilities are operating at sustained high utilization levels. Ammonium fluoride plays a critical role in buffered oxide etch formulations used during wafer cleaning and precise etching steps, making it an indispensable input across front-end semiconductor processes.

Continued investments in new fabrication plants and capacity expansions directly translate into structurally rising consumption across mature and emerging semiconductor hubs. This demand is further reinforced by the industry’s transition toward increasingly advanced process nodes. As device architectures become more complex and feature sizes shrink, fabrication processes require higher chemical purity and tighter contamination control. This shifts demand toward electronic-grade ammonium fluoride with stringent impurity thresholds, supporting value growth alongside volume expansion.

In June 2025, Mitsubishi Gas Chemical Company entered into a strategic partnership with a leading Taiwanese semiconductor manufacturer to supply high-quality ammonium fluoride solutions. This partnership strengthens supply chains for semiconductor etching, potentially increasing market access in Asia Pacific.

Structural Vulnerability from Raw Material Supply Concentration and Regulatory Friction

The ammonium fluoride market faces a serious structural barrier stemming from its heavy dependence on a narrow and geopolitically sensitive raw material base. Production is critically tied to fluorspar-derived hydrofluoric acid, yet global fluorspar mining is highly concentrated and exposed to export controls, environmental crackdowns, and shifting trade policies. This concentration risk leaves producers with limited sourcing flexibility, weak bargaining power, and heightened exposure to sudden cost spikes or forced production curtailments, undermining long-term supply reliability.

This vulnerability is compounded by increasingly stringent environmental and toxicity regulations governing fluoride handling and disposal. Ammonium fluoride and its intermediates are classified as hazardous, triggering strict compliance obligations under regulatory regimes such as REACH and U.S. environmental statutes. Producers are required to deploy closed-loop systems, advanced effluent treatment, and corrosion-resistant infrastructure to manage fluoride waste safely.

In sensitive regions, regulatory non-compliance risks operational shutdowns, delayed capacity additions, and constrained geographic expansion, making supply-side growth structurally slower than demand growth and amplifying volatility across the value chain.

Ultra-High Purity Grades for Advanced Semiconductor Fabrication

A high-value opportunity is emerging around the development of ultra-high purity ammonium fluoride tailored for next-generation semiconductor fabrication. As leading-edge logic and memory devices transition toward increasingly complex architectures, tolerance for metallic and ionic contaminants has narrowed dramatically. This elevates ammonium fluoride from a commodity etchant component to a yield-critical material, tightly linked to process stability in advanced wafer cleaning and buffered oxide etch steps.

Existing global capacity for such ultra-high purity grades remains limited, creating a structural supply gap as advanced fabs scale production. Manufacturers that invest in advanced purification, contamination control, and analytical verification capabilities are well-positioned to capture this premium segment. Ultra-high purity grades aligned with yield enhancement objectives allow suppliers to integrate deeper into Tier-1 foundry qualification cycles, significantly increasing switching costs and customer stickiness.

As semiconductor leaders prioritize defect reduction and process consistency over raw material cost, ultra-high purity ammonium fluoride represents a defensible pathway for value creation and strategic positioning within the advanced electronics materials ecosystem. In March 2025, the University of Oxford and Colorado State University developed a new method to recycle fluoride from PFAS chemicals. The technique destroys 'forever chemicals' while recovering fluorine for reuse in ammonium fluoride production, promoting circular economy practices amid regulatory scrutiny on fluorides.

Category–wise Analysis

Product Type Insights

Wet formulations are anticipated to remain the leading product type in the ammonium fluoride market, accounting for approximately 70% of total demand in 2026, driven primarily by semiconductor manufacturing requirements. Liquid solutions, particularly the standardized concentrated ammonium fluoride formulation, are most likely to be favored due to precise concentration control, safer automated handling, and compatibility with ultra-clean fabrication environments.

As chip architectures continue to shrink and impurity tolerances tighten, demand is expected to concentrate further around ultra-high-purity wet chemistries integrated into closed, automated chemical delivery systems. Ongoing capacity localization by suppliers such as Honeywell, Solvay, Daikin Industries, Morita Chemical, and Stella Chemifa is likely to reinforce the dominance of wet formulations, especially as advanced logic, memory, 5G, and AI-related semiconductor production expands globally.

Anhydrous ammonium fluoride is expected to emerge as the fastest-growing product category, supported by its increasing relevance in moisture-sensitive and solid-state technologies. Growth is likely to be driven by next-generation semiconductor processes, dry etching techniques, and advanced battery chemistries where water-based solutions are incompatible.

As fabrication nodes become more structurally delicate and energy storage technologies evolve toward solid-state and fluoride-ion systems, anhydrous forms are anticipated to see accelerating adoption in high-value niche applications. Investments in dry processing, closed-loop recovery systems, and application-specific formulations by players such as Honeywell, Solvay, Merck KGaA, Gujarat Fluorochemicals, and Sunlit Arizona are expected to underpin sustained momentum for this segment.

Application Insights

The semiconductor segment is anticipated to remain the leading application in the ammonium fluoride market, commanding an estimated 52.4% share in 2026. This dominance is driven by ultra-high-purity wet formulations used in Buffered Oxide Etch (BOE) solutions for advanced chip fabrication, including 3D and 3.5D IC packaging.

Demand is likely to expand as fabs adopt 12-inch wafers, AI/GPU-optimized etching, and photovoltaic applications, requiring precision etching cycles and in-line purity monitoring. Supply chain near-shoring and on-site chemical generation by key players such as Stella Chemifa, Honeywell, Kanto Chemical, Sunlit Group, and Mitsubishi Chemical further reinforce this segment’s sustained lead, especially under geopolitical pressures and PFAS-related wastewater regulations.

The pharmaceutical segment is projected to be the fastest-growing application, fueled by the increasing complexity of drug molecules and reliance on fluorine-mediated synthesis. Ammonium fluoride is used as a fluorinating agent, catalyst for silylation, and in protecting/deprotecting functional groups, with relevance in high-potency APIs, peptide synthesis, and radiopharmaceutical production.

Growth is likely to accelerate due to continuous flow chemistry adoption, solvent-free fluorination, and the development of custom reagent blends. Leading suppliers such as Merck KGaA, Thermo Fisher Scientific, Evonik Industries, Honeywell, and TCI Chemicals are expanding high-purity, anhydrous, and analytical-grade NH F offerings, aligning with cGMP and pharmacopeia compliance requirements to meet pharmaceutical-scale demand.

Regional Insights

Asia Pacific Ammonium Fluoride Market Trends

Asia Pacific is expected to lead the global market, holding approximately 40% share in 2026, while also emerging as the fastest-growing region due to its dominant semiconductor manufacturing infrastructure and high-volume production capabilities. The market is driven by the expansion of semiconductor fabrication, pharmaceutical manufacturing, and chemical production capacity.

The region is likely to benefit from China’s integrated supply chains, which provide competitive pricing advantages, and the rapid scaling of production in Southeast Asian countries such as Vietnam and Malaysia. Demand is anticipated to grow across electronics, metallurgy, and construction sectors, with semiconductor fabs in Taiwan and South Korea driving the uptake of ultra-high-purity ammonium fluoride for precise etching and surface cleaning. India and China’s pharmaceutical industries are also expected to sustain strong growth for ammonium fluoride in drug synthesis and analytical testing.

Industrial trends in APAC are anticipated to focus on AI-driven quality control, automated chemical handling systems, and customized chemical formulations for high-growth verticals like EV batteries and microelectronics. Sustainability initiatives, including closed-loop recycling and environmentally friendly production methods, are likely to accelerate, alongside stricter safety and environmental regulations that are reshaping operational strategies.

Leading players such as Stella Chemifa, Fujian Kings Fluoride, Honeywell, Zhejiang Sanmei Chemical, and Solvay are expected to consolidate their positions through innovation, compliance, and regional manufacturing expansion, reinforcing APAC’s dominant and fastest-growing market status. These structural, policy-driven, and logistical factors are expected to sustain Asia Pacific’s dual position as both the leading and fastest-growing market. Leading APAC manufacturers are adopting AI-driven quality control and automated chemical handling systems to meet the "zero-defect" standards required by modern 2nm and 3nm chip fabs.

North America Ammonium Fluoride Market Trends

North America is expected to hold approximately 35% of the global market in 2026, reflecting a mature and stable regional position supported by a strong semiconductor and electronics manufacturing ecosystem. The U.S. anchors regional activity through concentrated R&D and high-value manufacturing, while federal incentives under the CHIPS and Science Act encourage domestic fabrication facility expansion, generating consistent demand for electronic wet chemicals. Strict EPA regulations on fluoride effluent maintain compliance barriers, reinforcing adoption among established players with capable infrastructure.

The region is likely to remain steady as localized investments continue to re-shore chemical supply chains, mitigating geopolitical risk and ensuring supply reliability. High standards for environmental compliance and manufacturing integration support ongoing adoption across semiconductor and electronics applications. Concentrated industrial infrastructure, regulatory oversight, and policy-driven incentives are expected to sustain North America’s mature market profile, enabling incremental growth through operational efficiency rather than expansion-led acceleration.

Europe Ammonium Fluoride Market Trends

Market growth in Europe is supported by established automotive electronics and specialty pharmaceutical manufacturing. Germany, France, and the U.K. anchor regional activity, with Germany leading due to its strong automotive and chemical production capabilities, including firms such as Infineon and Bosch. The European Chips Act reinforces demand for high-purity etchants by promoting semiconductor manufacturing expansion, while stringent REACH regulations guide product formulation, handling, and packaging standards.

The region is likely to maintain stability as manufacturers continue aligning production processes with compliance requirements and efficiency mandates. Germany’s industrial base ensures consistent capacity for automotive and chemical applications, while regulatory oversight supports safe, standardized operations. Investments in high-purity materials and adherence to environmental directives reinforce operational reliability. These structural, policy-driven, and industrial factors are expected to preserve Europe’s mature market profile, supporting incremental growth without significant acceleration.

Competitive Landscape

The global ammonium fluoride market shows moderate consolidation, with the top five players, including Merck, Honeywell, Solvay, Dongyue, and Stella Chemifa, accounting for roughly 45% of the overall market share. Concentration is significantly higher in the electronic grade segment, where the top five suppliers control close to 60% of demand, reflecting strong entry barriers linked to purification technology, quality assurance, and customer qualification cycles. Market leaders compete primarily on purity levels, process consistency, and long-term supply reliability, which are critical for semiconductor and advanced electronics applications.

In contrast, the industrial and technical grade segments remain highly fragmented, with numerous Chinese and Indian producers competing on cost and volume. Competitive intensity in this segment remains high, although several mid-tier Asian manufacturers are investing in purification upgrades to move toward higher-value electronic and specialty grades, gradually narrowing the gap with established leaders.

Key Industry Highlights:

- In May 2025, China Kings Resources Group expanded its fluorspar beneficiation capacity and integrated downstream fluorochemical production. The expansion targets growing demand from lithium-ion batteries and specialty chemicals, enhancing ammonium fluoride feedstock availability and potentially reducing global prices by improving efficiency.

- In April 2025, Minersa Group advanced development activities at its fluorspar mining operations in Southern Africa. This initiative aims to secure long-term supply for European fluorochemical manufacturers, offering opportunities for ammonium fluoride producers to diversify away from Chinese dominance amid export controls.

- In March 2025, Fluorsid invested in process optimization and environmental efficiency upgrades across its fluorspar processing and fluorochemical facilities. Upgrades focus on sustainable production to meet EU regulations, potentially reducing costs for ammonium fluoride derivatives while improving eco-friendly credentials for global exports.

Companies Covered in Ammonium Fluoride Market

- Stella Chemifa Corporation

- Honeywell International Inc.

- Solvay S.A. (Syensqo)

- Morita Chemical Industries Co., Ltd.

- Merck KGaA

- Dongyue Group Limited

- Fubao Group

- Zhejiang Sanmei Chemical Industry Co., Ltd.

- Fujian Kings Fluoride Industry Co., Ltd.

- Shaowu Huaxin Chemical Industry Co., Ltd.

- Mitsubishi Gas Chemical Company, Inc.

- Daikin Industries, Ltd.

- BASF SE

- Linde plc

- Avantor, Inc.

- Do-Fluoride New Materials Co., Ltd.

- Arkema S.A.

Frequently Asked Questions

The global ammonium fluoride market is projected to be valued at US$2.6 billion in 2026 and is forecast to reach US$3.9 billion by 2033, driven by rising demand from semiconductor manufacturing and high-purity chemical applications.

Demand is increasing due to expanding semiconductor fabrication driven by AI and advanced connectivity, rising wafer etching and cleaning requirements, and higher purity standards associated with advanced process nodes, which elevate ammonium fluoride from a commodity input to a yield-critical material.

The ammonium fluoride market is expected to grow at a CAGR of 6.0% between 2026 and 2033, supported by capacity expansion in Asia Pacific and sustained investments in advanced semiconductor manufacturing.

Anhydrous ammonium fluoride is the fastest-growing product type, driven by rising purity requirements in pharmaceuticals, reagents, and specialty chemical applications, along with advantages in storage efficiency and controlled on-site preparation.

Key players include Merck KGaA, Honeywell International Inc., Solvay S.A. (Syensqo), Stella Chemifa Corporation, Dongyue Group Limited, Morita Chemical Industries, Mitsubishi Gas Chemical Company, Daikin Industries, BASF SE, Arkema S.A., and Avantor Inc.