- Metals & Minerals

- Ferro Aluminum Market

Ferro Aluminum Market Size, Share, and Growth Forecast, 2026 – 2033

Ferro Aluminum Market by Product Type (Pure Ferro Aluminum Alloy, Ferro Aluminum Alloy Mixture), Application (Automobile Industry, Machinery Manufacturing, Fireworks Industry, Others), and Regional Analysis for 2026 – 2033

Ferro Aluminum Market Size and Trends Analysis

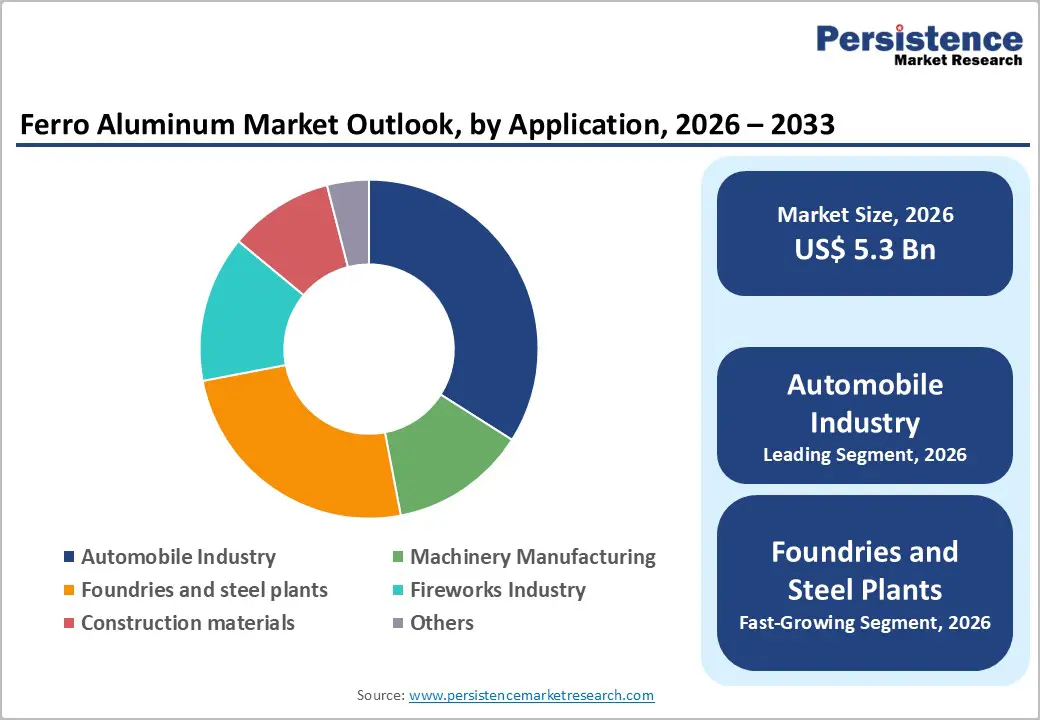

The global ferro aluminum market size is likely to be valued at US$5.3 billion in 2026 and is expected to reach US$7.2 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by its essential role as a deoxidizing, alloying, and grain-refining agent in steelmaking and specialty alloy production.

Rising demand for high-performance steels and lightweight alloys in automotive, aerospace, and construction is driving market growth. The automotive sector is a key consumer, using ferro aluminum to improve strength, reduce weight, and enhance corrosion resistance in vehicle components, including electric and hybrid models. Steel and foundry industries also depend on ferro aluminum to refine metal quality and enhance durability. Ongoing advancements in alloy production, such as improved purity, consistency, and low-carbon processing methods, are further improving manufacturing efficiency and sustainability.

Key Industry Highlights:

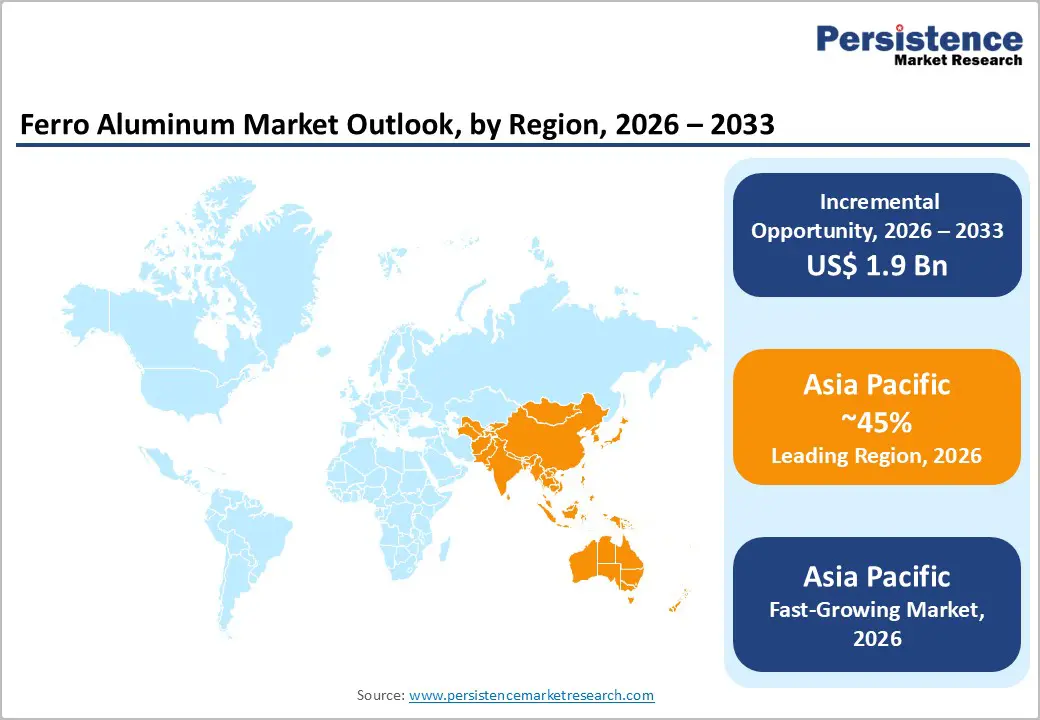

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by strong industrialization, steel production, and automotive expansion.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the ferro aluminum in 2026, supported by infrastructure development, rising domestic vehicle production, and cost-efficient manufacturing advantages.

- Leading Product Type: Pure ferro aluminum alloys are projected to represent the leading product type in 2026, accounting for 61% of the revenue share, driven by their uniform composition and suitability for precision applications.

- Leading Application: The automobile industry is anticipated to be the leading end-user, accounting for over 38% of the revenue share in 2026, supported by demand for lightweight, high-strength steels in vehicles.

| Key Insights | Details |

|---|---|

| Ferro Aluminum Market Size (2026E) | US$5.3 Bn |

| Market Value Forecast (2033F) | US$7.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Demand from the Foundry and Steel Industries for Deoxidation, Alloying, And Grain Refinement

Ferro aluminum is extensively used in the steel and foundry industries due to its ability to act as a potent deoxidizer and alloying agent. Its application improves tensile strength, corrosion resistance, and uniformity in specialty steels and castings. Foundries increasingly rely on ferro aluminum to produce high-quality steel and metal alloys for automotive, construction, and machinery sectors. With steel production growing and demand for high-performance alloys rising, ferro aluminum has become indispensable in refining processes, enhancing material properties, and meeting stringent industrial standards, thereby driving sustained market demand.

Ferro aluminum contributes to grain refinement in steel, ensuring superior mechanical and structural properties in end-use applications. Steel manufacturers prefer it over alternatives for precision alloying, as even minor impurities in the metal can compromise product quality. The growth of infrastructure projects and industrial machinery manufacturing elevates consumption, as high-strength steels are essential for durability and performance. The combination of technical efficacy and industrial necessity cements ferro aluminum’s role as a key market driver, particularly in regions with high steel output and evolving foundry capabilities.

Expansion of Automotive Manufacturing and Lightweighting Initiatives, Particularly in Electric Vehicles

The automotive sector is a major consumer of ferro aluminum, especially with increasing emphasis on lightweighting to improve fuel efficiency and EV performance. Manufacturers use ferro aluminum to produce aluminum-rich alloys that enhance strength while reducing weight in chassis, body panels, and electric vehicle components. With electric vehicle adoption accelerating, demand for high-performance, lightweight alloys has surged, positioning ferro aluminum as a crucial material for next-generation vehicles. Its integration into automotive applications also helps meet regulatory emission standards by enabling lighter, more efficient designs without compromising safety or durability.

The trend toward hybrid and fully electric vehicles has prompted automakers to adopt custom-grade ferro aluminum alloys tailored to specific component requirements. Light-weighting initiatives extend beyond EVs, encompassing conventional vehicles seeking improved efficiency and reduced carbon footprint. The automotive industry's expansion in emerging economies increases regional demand, creating opportunities for producers to scale operations and innovate alloy formulations. This sustained focus on automotive applications reinforces ferro aluminum’s position as a growth driver, linking industrial trends to materials engineering and market expansion.

Barrier Analysis - Environmental Regulations Governing High-Temperature Smelting and Emissions

Ferro aluminum production involves high-temperature smelting, generating significant energy consumption and emissions, which are increasingly regulated worldwide. Stringent environmental laws in major producing regions, including Asia-Pacific and Europe, mandate reduced greenhouse gas emissions and adherence to air quality standards. Compliance often requires substantial investments in emission control technologies and process optimization, increasing production costs. Smaller or fragmented producers may struggle to meet these standards, limiting output or creating supply inconsistencies.

Governments are promoting cleaner production methods, requiring modernization of traditional furnaces and adoption of energy-efficient technologies. Non-compliance can result in fines, license revocation, or operational shutdowns, creating barriers for smaller market participants. The capital-intensive nature of environmental compliance may slow new entrants and delay capacity expansions, particularly in regions with emerging industrial growth. While demand remains strong, regulatory pressure tempers market growth and necessitates ongoing innovation in sustainable and low-emission ferro aluminum production methods.

Market Fragmentation Leading to Quality Inconsistency and Limited Innovation Capacity

This fragmentation leads to inconsistent product quality, particularly in alloy composition, aluminum content, and deoxidation efficiency. Such variability can deter end-users, especially in automotive and aerospace sectors, where precise material properties are critical. Fragmented supply chains also limit investment in research and development, reducing opportunities for innovative formulations and process optimization. The lack of standardization and R&D capability restrains overall market growth and inhibits the development of high-performance, custom-grade alloys demanded by advanced industries.

Fragmented production increases supply chain complexity and operational inefficiencies, including variable lead times and inconsistent pricing. Manufacturers may struggle to scale production or respond to sudden spikes in demand due to limited capacity coordination. End-users, particularly in precision industries, may prefer trusted suppliers or large-scale producers, leaving smaller players at a disadvantage. This competitive disparity and restricted innovation hinder overall market progression, reinforcing the need for consolidation, standardization, and strategic partnerships to enhance product quality.

Opportunity Analysis - Adoption of Sustainable Low-Carbon Production Methods and Secondary Aluminum Recycling

Technologies such as electric arc furnaces, renewable energy integration, and process optimization enable greener manufacturing, aligning with environmental mandates. Secondary aluminum recycling enhances sustainability by reintroducing scrap aluminum into ferro aluminum production, reducing raw material dependency and energy usage. Adoption of these practices can lower costs, improve corporate social responsibility profiles, and attract environmentally conscious customers, positioning companies for long-term competitiveness in an evolving industrial landscape.

Governments and industry bodies are providing incentives for sustainable practices, including tax benefits, subsidies, and technology grants. Recycling helps the environment and makes supply chains more efficient and secure. Companies that integrate green production and recycling into their business models can differentiate themselves in a competitive market, opening opportunities for premium pricing and long-term contracts with automotive and aerospace clients.

Growth of Custom-Grade Alloys for Electric Vehicle and Aerospace Applications

The rising demand for electric vehicles and advanced aerospace components presents a significant opportunity for custom-grade ferro aluminum alloys. Tailored formulations with optimized aluminum content and deoxidation properties allow manufacturers to meet stringent weight, strength, and corrosion resistance requirements. Automotive EV components, such as battery casings, lightweight chassis, and body panels, benefit from alloys engineered for specific mechanical performance, while aerospace structures demand precision alloys for high-stress and temperature-sensitive applications.

Advancements in metallurgical technology allow for rapid prototyping and alloy modification, enabling producers to respond quickly to evolving customer requirements. Partnerships with OEMs and aerospace manufacturers drive demand for specialized ferro aluminum grades, fostering innovation in alloy composition and production processes. As the EV and aerospace industries expand, the opportunity for tailored alloys grows, offering manufacturers the chance to lead in high-performance, value-added segments.

Category-wise Analysis

Product Type Insights

Pure ferro aluminum alloy are expected to lead the ferro aluminum market, accounting for approximately 61% of revenue in 2026, driven by their high aluminum content, uniform composition, and suitability for precision applications, particularly in sectors that demand consistent performance. Automotive manufacturers, for example, rely on pure ferro aluminum in chassis and EV components to ensure optimal deoxidation and grain refinement during steel production, where even minor impurities can compromise structural integrity. Aerospace applications similarly require precise alloy specifications for lightweight, high-strength parts, such as fuselage components, which benefit from the alloy’s consistent properties.

Ferro aluminum alloy mixtures are likely to represent the fastest-growing segment in 2026, supported by their flexibility in formulation and cost-effectiveness for foundry and construction applications. While it holds a smaller market share compared to pure grades, its popularity is rising as steel producers and casting facilities seek alloys tailored to specific reactivity profiles without the full-cost premium of pure ferro aluminum. For example, a construction foundry may use a mixture to adjust aluminum content depending on the type of steel or casting being produced, optimizing strength and weldability while reducing material costs. These mixtures allow manufacturers to customize performance parameters for different industrial applications, including non-critical automotive parts and infrastructure projects, where precision requirements are slightly less stringent.

Application Insights

The automobile industry is projected to lead the market, capturing around 38% of the revenue share in 2026, supported by its production of lightweight, high-strength steels, making it essential for vehicle chassis, EV battery casings, and corrosion-resistant components. For example, major electric vehicle manufacturers incorporate ferro aluminum into chassis alloys to reduce weight while maintaining structural integrity and safety standards. Light-weighting initiatives, driven by fuel efficiency regulations and EV performance requirements, enhance the alloy’s importance. The automotive sector’s substantial contribution to steel consumption ensures continuous demand for high-quality ferro aluminum, particularly pure grades used for critical deoxidation and grain refinement processes.

Foundries and steel plants are likely to be the fastest-growing, driven by rising demand for specialty steels and high-performance castings. These facilities increasingly use ferro aluminum to enhance tensile strength, weldability, and overall material quality in large-scale infrastructure and machinery manufacturing projects. For example, a steel plant producing high-strength alloy steel for industrial machinery incorporates ferro aluminum mixtures to tailor deoxidation and grain refinement properties, improving yield and reducing defects. The segment benefits from ongoing infrastructure expansion and industrialization, particularly in emerging economies, where demand for high-quality metals is accelerating.

Regional Insights

North America Ferro Aluminum Market Trends

North America is likely to be a significant market for ferro aluminum in 2026, driven by a combination of sustained industrial demand and evolving material preferences. The region remains a significant consumer of ferro alloys, including ferro aluminum, because of its mature steel and automotive industries that require consistent alloying and deoxidation performance to meet rigorous production standards. For example, companies such as Novelis Inc., a major aluminum producer and recycler, are investing in sustainable and low carbon aluminum facilities in North America, reflecting a shift toward environmentally compliant and efficient metal production, which indirectly supports ferro aluminum usage in alloying processes.

Despite solid demand, North America’s ferro aluminum landscape faces structural challenges. Domestic production capacity does not fully satisfy regional needs, resulting in significant reliance on imports from suppliers to bridge the supply gap. This import dependency influences pricing and supply chain dynamics, especially when tariff measures or trade shifts affect raw material flows. Growth is moderated by stringent environmental regulations that require cleaner processing technologies and higher recycling rates, pushing producers to innovate and adopt sustainable practices to remain competitive.

Europe Ferro Aluminum Market Trends

Europe is likely to be a significant market for ferro aluminum in 2026, due to a well established industrial base and a strong emphasis on quality steel and alloy production. Driven by demand from automotive, machinery, and specialty steel sectors, ferro aluminum supports high performance steelmaking for structural and corrosion resistant applications across key industries in countries such as Germany, France, and Italy. European producers are increasingly focusing on energy efficient and sustainable alloying practices to meet stringent environmental regulations and support circular economy goals, bolstering demand for recyclable and high performance alloy inputs in metallurgical processes.

Despite robust demand, Europe faces competitive and operational challenges. Domestic ferro alloy producers are balancing import pressures and high energy costs while striving to maintain market share and competitiveness. For example, Outokumpu, a major Finnish stainless steel producer, is investing in advanced alloy technologies and expansion into high value materials to enhance its position and drive growth in Europe’s alloy market. These strategic moves demonstrate how key players are adapting to market dynamics, regulatory pressures, and sustainability imperatives, reinforcing Europe’s nuanced but resilient ferro aluminum landscape.

Asia Pacific Ferro Aluminum Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by rapid industrialization, robust steel production, and expanding manufacturing sectors across major economies such as China, India, Japan, and Southeast Asia. The region’s vast demand for high strength, lightweight alloys in automotive, construction, and infrastructure applications fuels steady growth in ferro aluminum consumption, as manufacturers prioritize materials that enhance durability and corrosion resistance in steel and aluminum alloys.

Amidst this broader growth, regional players are adapting to shifting industrial needs and sustainability priorities. For example, China Hongqiao Group, one of the largest aluminum producers in Asia, has been intensifying its focus on alloy and aluminum product innovation while investing in cleaner energy sources and recycling initiatives to align with environmental goals and reduce carbon intensity. Such strategic moves demonstrate how companies operating in the Asia Pacific ferro aluminum ecosystem are responding to evolving regulatory and market trends.

Competitive Landscape

The global ferro aluminum market exhibits a moderately fragmented structure, driven by the presence of numerous regional producers alongside established multinational alloy manufacturers catering to diverse industrial demand across steelmaking, automotive, aerospace, and foundry sectors. Producers vary from large specialty alloy suppliers to smaller regional manufacturers, each competing on product quality, cost, and service capabilities. The competitive landscape reflects investments in high purity products, low carbon manufacturing processes, and tailored alloy grades to meet specific customer needs.

With key leaders including AMG Advanced Metallurgical Group N.V., FE Mottram Ltd., and Nihon Yakin Kogyo Co., Ltd., the market features a mix of regional players that hold significant share through differentiated offerings and specialized expertise. These players compete through product innovation, strategic partnerships, bespoke alloy solutions, and investments in cleaner production technologies, which help enhance market presence, optimize costs, and meet stringent performance requirements across end user industries.

Key Industry Developments:

- In November 2025, Indian Metals & Ferro Alloys Ltd. completed the acquisition of a ferro-chrome plant from Tata Steel at Kalinganagar, Odisha for INR 610 crore (US$66.5 million). The acquisition adds about 99 MVA of furnace capacity, including both operational and under-construction units, increasing IMFA’s total production capacity to over 0.5 million tonnes annually. This strategic move strengthens IMFA’s position in the global ferro-alloys sector and supports increased supply of alloying materials used in steel and specialty metal manufacturing.

Companies Covered in Ferro Aluminum Market

- Shree Bajrang Sales Pvt. [U1] Ltd.

- Anyang Zhenxin Metallurgical Materials Co., Ltd.

- Ferro Alloys Corporation Ltd. (FACOR)

- Westbrook Resources Ltd.

- Mortex Group

- Bansal Brothers

- REXTAR GROUP

- Shanghai Zhiyue Industrial Co., Ltd.

- Aarti Steels Ltd.

- IMFA (Indian Metals & Ferro Alloys Ltd.)

- Eramet

- Tata Steel

- Ferroglobe PLC

Frequently Asked Questions

The global ferro aluminum market is projected to reach US$5.3 billion in 2026.

Rising demand from steelmakers and automotive manufacturers for high-strength, lightweight, and corrosion-resistant alloys drives the ferro aluminum market.

The ferro aluminum market is expected to grow at a CAGR of 4.5% from 2026 to 2033.

Adoption of sustainable low-carbon production methods and development of custom-grade alloys for electric vehicle and aerospace applications are key market opportunities.

Shree Bajrang Sales Pvt. Ltd., Anyang Zhenxin Metallurgical Materials Co., and Ferro Alloys Corporation Ltd. are the leading players.