- Specialty & Fine Chemicals

- Sodium Aluminum Silicate Market

Sodium Aluminum Silicate Market Size, Share, and Growth Forecast, 2026-2033

Sodium Aluminum Silicate Market by Source (Natural, Synthetic), End-Use (Construction, Electronics, Petrochemical Refineries, Agriculture, Food & Beverages, Automotive & Aerospace, Others), and Regional Analysis for 2026-2033

Sodium Aluminum Silicate Market Share and Trends Analysis

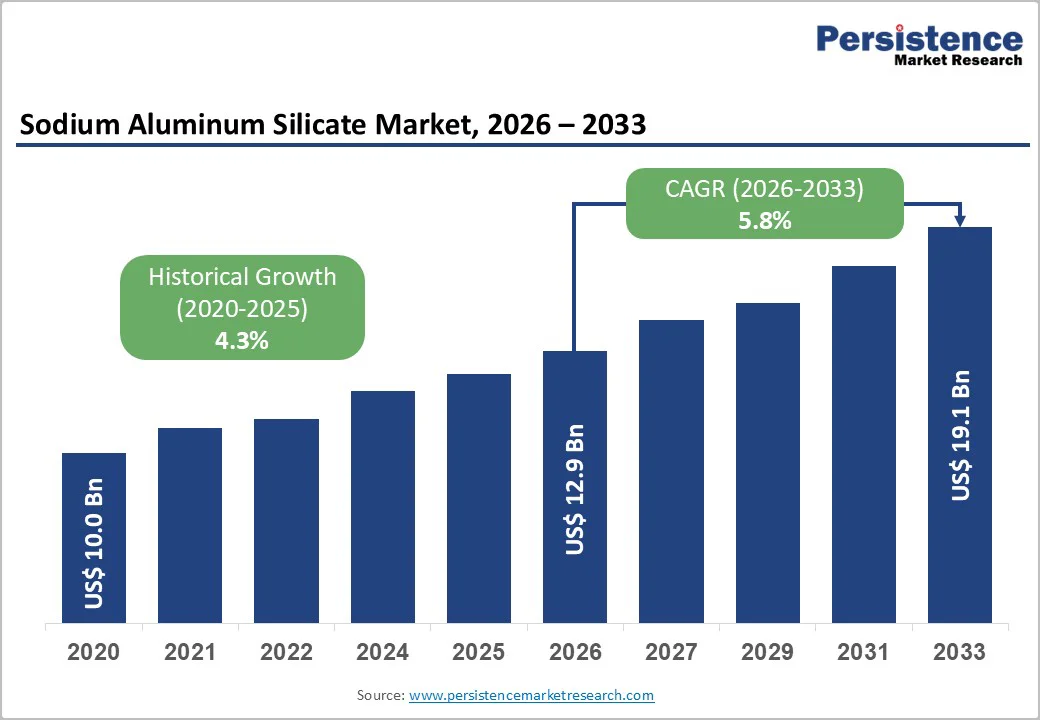

The global sodium aluminum silicate market size is likely to be valued at US$ 12.9 billion in 2026 and is projected to reach US$ 19.1 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026 - 2033. The market is expected to continue to expand due to consistent demand from construction materials, food and beverage additives, and refining catalyst applications, reinforced by well-established regulatory approvals and dependable material performance characteristics. Long-term demand stability, combined with incremental product and process innovation, positions sodium aluminum silicate (SAS) as a critical material across both industrial and consumer-oriented value chains. Clear regulatory frameworks across major economies and stable access to raw material inputs strengthen long-term market predictability, reinforcing sodium aluminum silicate’s role as a structurally resilient component of the broader silicates industry.

Key Industry Highlights

- Source Leadership and Growth Outlook: Synthetic sodium aluminum silicate is expected to dominate with an estimated 65% share in 2026, and is likely to grow the fastest at about 5.8% CAGR through 2033, driven by consistent quality standards.

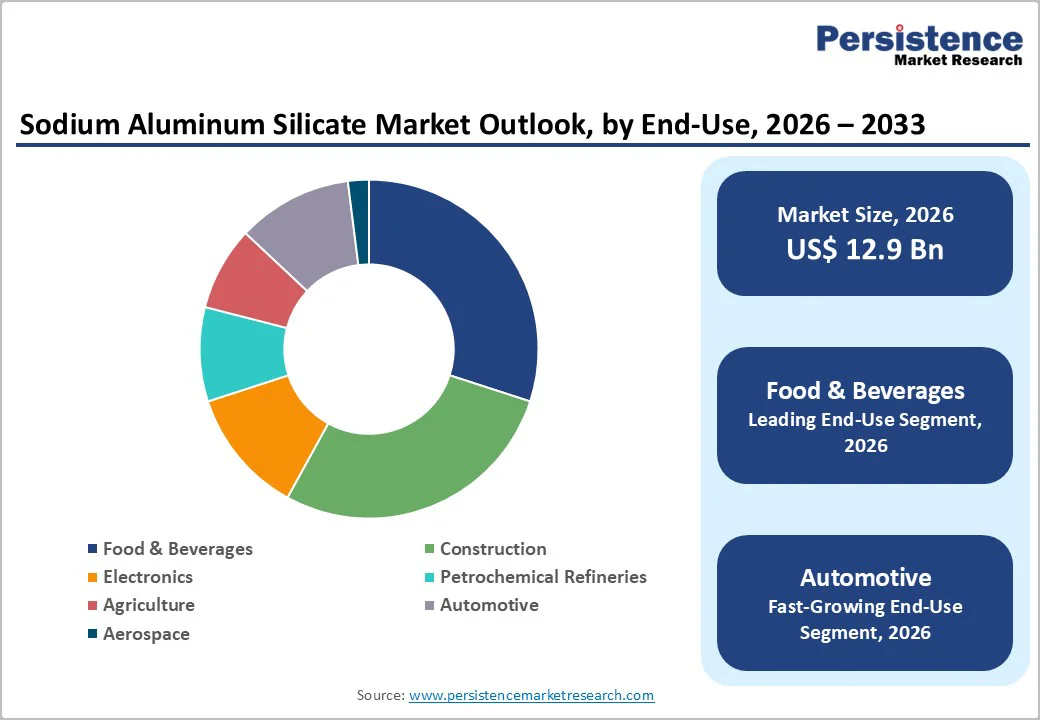

- End-Use Leadership: Food & beverages is expected to remain the leading end-use segment, accounting for approximately 30% of market revenue in 2026, driven by its role in anti-caking and stabilization applications,

- Fastest-growing End-Use: Automotive is forecast to expand at a CAGR of 7% from 2026 to 2033, due to the extensive use of sodium aluminum silicate in performance and durability enhancement.

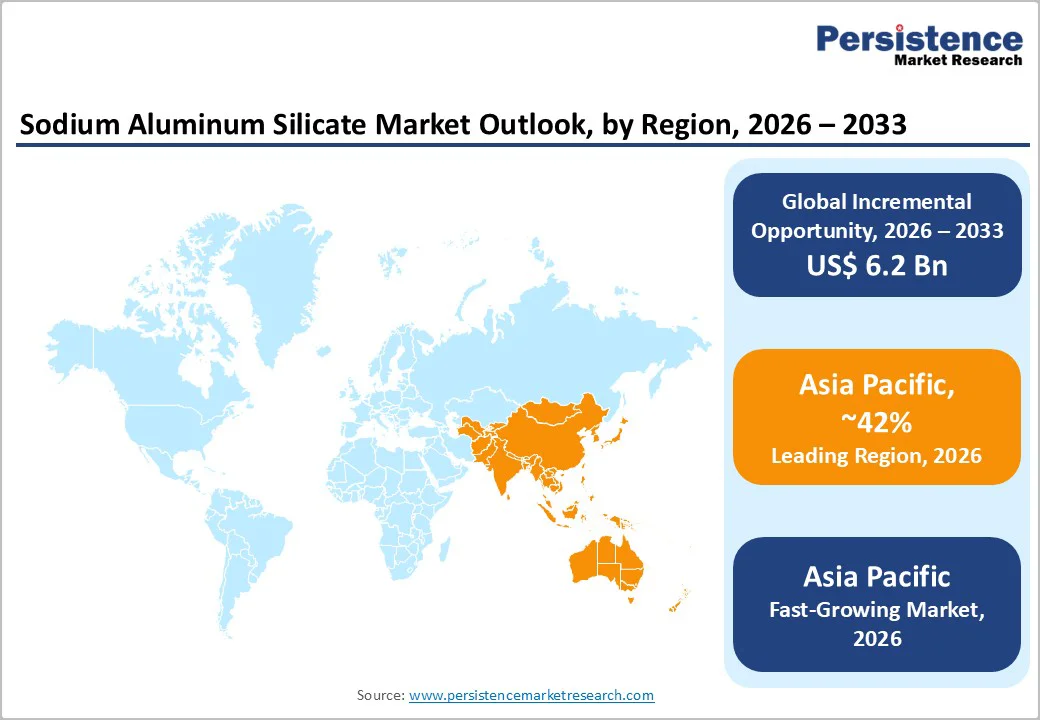

- Regional Leadership: Asia Pacific is anticipated to hold the largest regional share at approximately 42% of the market in 2026, led by manufacturing scale-up and infrastructure investments.

| Report Attribute | Details |

|---|---|

|

Sodium Aluminum Silicate Market Size (2026E) |

US$ 12.9 Bn |

|

Market Value Forecast (2033F) |

US$ 19.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Robust Industrial and Consumer Demand Supporting Market Growth

The sodium aluminum silicate market benefits from strong demand across multiple sectors, including construction, petrochemical refining, and food processing, which collectively underpin market expansion. In construction, it is valued as a functional filler and performance enhancer in cement, coatings, and specialty building materials due to its thermal stability, binding efficiency, and favorable cost-to-performance ratio. Sustained urbanization, infrastructure development, and public housing initiatives create predictable bulk demand, providing stability against short-term economic fluctuations. This demand is supported by industry moves such as PQ Corporation’s expansion of its specialty silica production facility in Pasuruan, Indonesia, which added a state-of-the-art micronizer to meet growing industrial needs, including construction and coatings.

The role of the compound in petrochemical refining as a catalyst component and filtration aid ensures recurring procurement driven by efficiency and throughput optimization. In the food and beverage sector, sodium aluminum silicate is widely approved as an anticaking and processing aid, facilitating safe and consistent application in packaged foods. Regulatory stability supports long-term supply agreements, while increasing consumption of processed foods contributes to expanding volumes. Further reinforcing supply security, PQ’s acquisition of Sibelco’s specialty silicate business in Lödöse, Sweden, in early 2025 strengthens its European network, ensuring consistent availability of high-quality silicates for industrial and consumer applications. These initiatives diversify demand sources, reduce reliance on cyclical markets, and position the compound as a strategically important, high-demand material across multiple value chains.

Energy and Substitution Challenges Constraining Market Growth

The production of sodium aluminum silicate is highly energy intensive, with electricity and fuel costs representing a significant portion of total manufacturing expenses. Volatility in energy prices can compress margins and delay capacity expansions, particularly affecting smaller producers who lack scale or access to low-cost power. These cost pressures reduce short-term supply flexibility and limit the ability to respond to rising demand in construction, refining, and food applications, creating a structural restraint on market growth.

The compound also faces substitution risk from alternative silicates and synthetic additives that offer comparable performance in applications such as anti-caking, coatings, and catalyst supports at lower or more stable costs. Industrial buyers increasingly evaluate alternatives based on formulation economics rather than chemical specificity, constraining pricing power for standard grades. This dynamic emphasizes the need for producers to focus on high-purity, application-specific SAS solutions to maintain competitiveness and protect market share.

Expanding Demand from Industrial, Specialty, Agricultural, and Sustainable Applications

The market is poised to benefit from growing industrialization and manufacturing expansion in emerging markets, where government-led initiatives and localized supply chains are driving higher consumption of functional inorganic materials. Proximity-based production and regional partnerships offer producers scalable growth opportunities, as infrastructure, electronics, and food processing sectors increasingly adopt the compound. Rising industrial output and urbanization ensure incremental volume growth, while investments in sustainable construction materials, such as Brazilian research in aluminosilicate-based geopolymers using fly ash, red mud, and marble waste for low-carbon, circular economy binders, highlight increasing adoption of environmentally conscious building applications and durable, high-performance materials.

Demand is also shifting toward high-purity, application-specific grades for electronics, advanced refining, and food applications, which command higher margins and foster long-term customer relationships. Modern agriculture also supports growth, as Sodium aluminum silicate’s moisture control properties improve fertilizer handling, storage, and post-harvest efficiency. Across industrial, specialty, agricultural, and sustainable construction applications, the compound is positioned as a structurally expanding material, enabling producers to move up the value chain while mitigating commodity price exposure and aligning with global sustainability and circular economy objectives.

Category-wise Analysis

Source Insights

Synthetic SAS is expected to continue leading as a source, accounting for approximately 65% of the sodium aluminum silicate market revenue share in 2026, due to its consistent quality, controlled particle size, and suitability for regulated applications such as food processing, electronics, and refining. Industrial buyers favor synthetic SAS for its reproducibility, compliance with safety standards, and ability to meet precise formulation requirements. Its dominance is reinforced by widespread adoption across high-value, performance-critical applications.

The synthetic segment is likely to be the fastest growing, projected to expand at a CAGR of 6.1% through 2033, driven by the rising demand for high-purity and application-specific SAS grades. Investments in controlled synthesis technologies and quality certification frameworks further support growth. While natural ones remains cost-competitive and relevant for bulk construction and agricultural applications, variability in composition limits its adoption in regulated and high-performance applications, keeping synthetic aluminum silicate at the forefront of both revenue and growth.

End-Use Insights

Food & beverages is expected to dominate the end-use segment in 2026, capturing approximately 30% of the SAS market revenues in 2026, driven by its widespread application as an anti-caking and stabilization agent. Steady demand in packaged foods, combined with regulatory acceptance and a shift toward higher-value, clean-label formulations, ensures consistent revenue generation and positions this segment as the backbone of market growth. Its functional benefits, including moisture control and product stability, reinforce long-term adoption across diverse food processing applications.

Automotive is an emerging high-growth end-use segment, projected to expand at a CAGR of roughly 7% during the 2026-2033 forecast period, driven by the use of sodium aluminum silicate in performance enhancement, durability, and lightweighting applications. Key applications include tires, polymer fillers, and specialty coatings, where this compound improves mechanical strength, thermal stability, and overall material efficiency. Rising demand for lightweight, high-performance components in vehicles, coupled with stricter durability and safety standards, is fueling adoption, positioning automotive as a strategically important growth segment within the market.

Regional Analysis

North America Sodium Aluminum Silicate Market Trends

North America is a key market for sodium aluminum silicate, with the United States likely to be the leading regional demand. The regional market benefits from mature construction activities, advanced food processing industries, and a well-established petrochemical refining base. Regulatory clarity from agencies such as the U.S. Environmental Protection Agency (EPA) and Food and Drug Administration (FDA) provides stable operational frameworks, supporting consistent procurement and long-term supply agreements. High-value applications in food, electronics, and industrial processes reinforce the importance of SAS across multiple end-use sectors.

The competitive dynamics of the regional market are governed by strong supplier-buyer relationships and an emphasis on process efficiency and compliance-driven upgrades. The growth of the North America SAS market is anticipated to be moderate, with a CAGR of around 4.5% through 2033, reflecting incremental adoption of high-purity grades rather than large-scale volume expansion. Investment priorities focus on technological optimization, operational sustainability, and maintaining margins rather than rapid capacity expansion, ensuring predictable and stable market performance.

Europe Sodium Aluminum Silicate Market Trends

Europe is a major market for the compound, with Germany, the United Kingdom, France, and Spain serving as key contributors. Growth is underpinned by ongoing construction renovation projects, strict food safety regulations, and the use of sodium aluminum silicate in specialty industrial applications. Regulatory harmonization across the European Union (EU) fosters standardized production methods and the use of high-purity grades, while sustainability initiatives encourage energy-efficient manufacturing. Stable baseline demand is maintained by Europe's mature industrial infrastructure and consistent requirements in both industrial and consumer sectors.

The competitive landscape in Europe is moderately consolidated, with regional producers prioritizing specialty applications and regulatory compliance rather than competing solely on volume. Market expansion is fueled by the rising adoption of high-performance grades in construction, food processing, and refining industries. Companies focus on operational strategies such as environmental compliance, process optimization, and product differentiation, which reinforce a stable, quality-driven growth path instead of rapid capacity expansion. This approach supports long-term market resilience and enables suppliers to address evolving regulatory and sustainability demands effectively.

Asia Pacific Sodium Aluminum Silicate Market Trends

Asia Pacific is set to be the fastest-growing regional SAS market and is expected to secure about 42% of the sodium aluminium silicate market share in 2026. China, India, and ASEAN economies are driving this upswing through manufacturing scale-up, infrastructure buildout, and rising demand from refining and other industrial end uses. Growing domestic consumption across sectors such as food, construction, electronics, and specialty industrial uses positions the area as both a demand anchor and a production base. Government-led industrialization programs and policy support further accelerate adoption by improving project pipelines and shortening buying cycles. ?

The Asia Pacific market is expected to expand at a 6.5% CAGR through 2033, supported by high-volume applications alongside newer specialty requirements. Companies are increasingly prioritizing local manufacturing, supply chain optimization, and cost-efficient output to improve responsiveness and protect service levels as demand rises. Ready access to raw materials, available skilled labor, and broader industrial ecosystem development reinforce APAC as the primary growth engine for both scale-driven and premium opportunities. For producers pursuing global expansion, the most resilient approach is to combine regional capacity planning with application-specific grade strategies and partnership-led go-to-market execution in priority countries.

Competitive Landscape

The global sodium aluminum silicate market structure is moderately consolidated, with leading players such as BASF, W. R. Grace & Co., Clariant, and AkzoNobel controlling a significant share of total revenue. These companies leverage established industrial relationships, regulatory compliance expertise, and integrated production and quality management capabilities. Investment in advanced synthesis technologies, high-purity grade development, and quality certification frameworks helps them maintain a competitive edge across food, construction, electronics, and refining applications.

Regional and niche producers focus on specialty segments, including application-specific grades for electronics, food-grade SAS, and industrial catalysts. Entry barriers such as energy-intensive production, regulatory approvals, and stringent quality standards limit new competitors, while innovation in high-purity and performance-optimized sodium aluminum silicate creates differentiation opportunities. Market consolidation is expected to continue gradually as leading manufacturers expand production capacity, enter new regional markets, and pursue technology-driven partnerships to enhance product offerings and service capabilities.

Key Industry Developments

- In May 2025, researchers from Brazil developed sustainable alkali-activated binders using iron ore tailings, carbide lime, and sodium silicate, forming N-A-S-H and C-A-S-H gels.

The binders effectively immobilize heavy metals below regulatory thresholds, reducing environmental risks from tailings while cutting Portland cement reliance and emissions in line with circular economy principles. - In April 2025, aluminosilicate prices rose across Europe and Asia, with China experiencing a 1% increase driven by bullish construction sector demand, while Germany saw a 3.8% gain amid supply tightness despite moderate downstream demand from glass, ceramics, and construction.

Europe faced weak residential orders and reduced building permits, prompting trader price hikes. - In February 2025, PQ Corporation partnered with ADDITIVA Produtos Químicos to expand its presence in Brazil. Leveraging ADDITIVA’s technical expertise and logistical infrastructure, PQ aims to enhance the commercialization of its GASIL® silica products across industrial applications, including paints, coatings, and construction, improving market accessibility and customer support in the region.

Companies Covered in Sodium Aluminum Silicate Market

- BASF SE

- Evonik Industries AG

- W.R. Grace & Co.

- PQ Corporation

- Solvay S.A.

- Huber Engineered Materials

- Tokuyama Corporation

- Nippon Chemical Industrial

- IQE Group

- Sibelco

- Omya

- Shandong Xinhecheng

- Henan Province Xixia County Silica

- Madhu Silica

Frequently Asked Questions

The global sodium aluminum silicate market is projected to reach US$ 12.91 billion in 2026.

Widening applicability of SAS in construction, food & beverages, electronics, and refining, supported by regulatory acceptance, consistent material quality, and rising infrastructure and industrialization activities are driving the market.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Opportunities exist in high-purity SAS for electronics, food processing, and refining, along with emerging applications in automotive, aerospace, fertilizers, and specialty coatings.

BASF SE, Evonik Industries AG, W.R. Grace & Co., PQ Corporation, and Solvay S.A. are some of the key companies in the market.