- Specialty & Fine Chemicals

- Aluminum Curtain Wall Market

Aluminum Curtain Wall Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Aluminum Curtain Wall Market by Application (Commercial Building, Institutional and Public Building, and Industrial Building), By Product Type (Unitized Curtain Wall, Stick-Built Curtain Wall, and Semi-Unitized Curtain Wall), and Regional Analysis for 2026 - 2033

Aluminum Curtain Wall Market Size and Trends Analysis

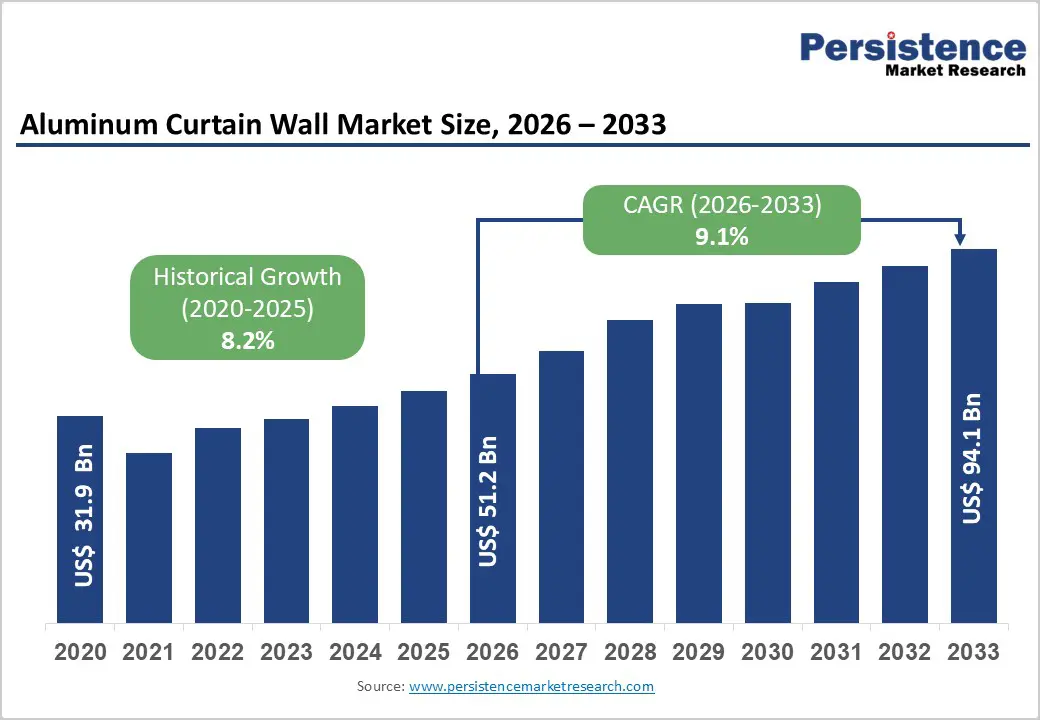

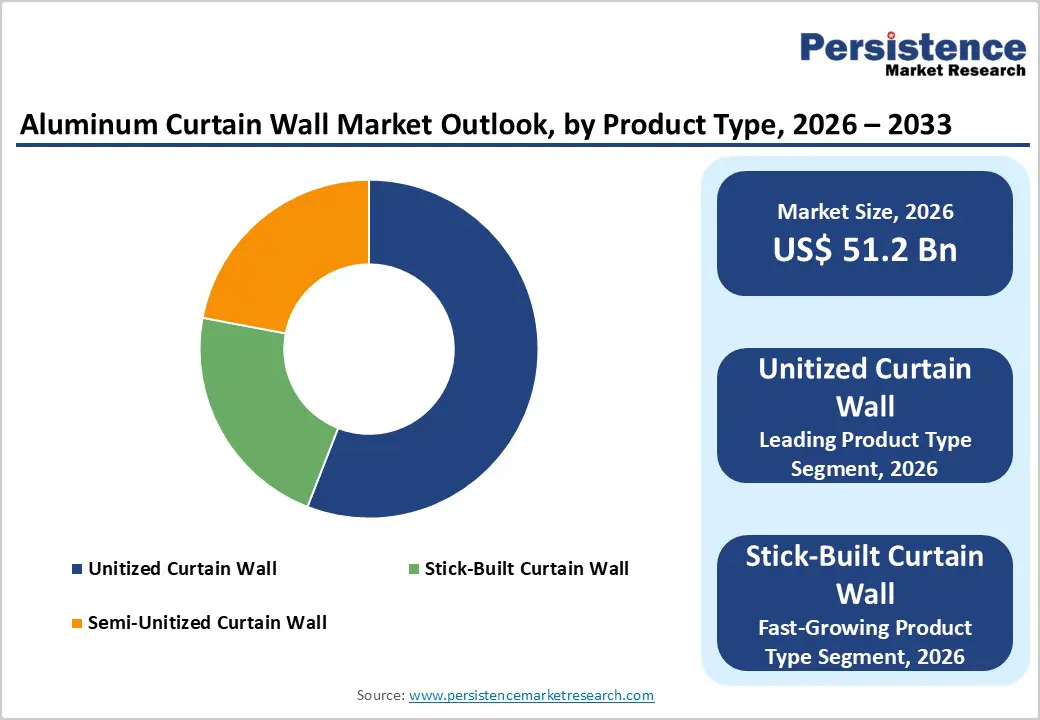

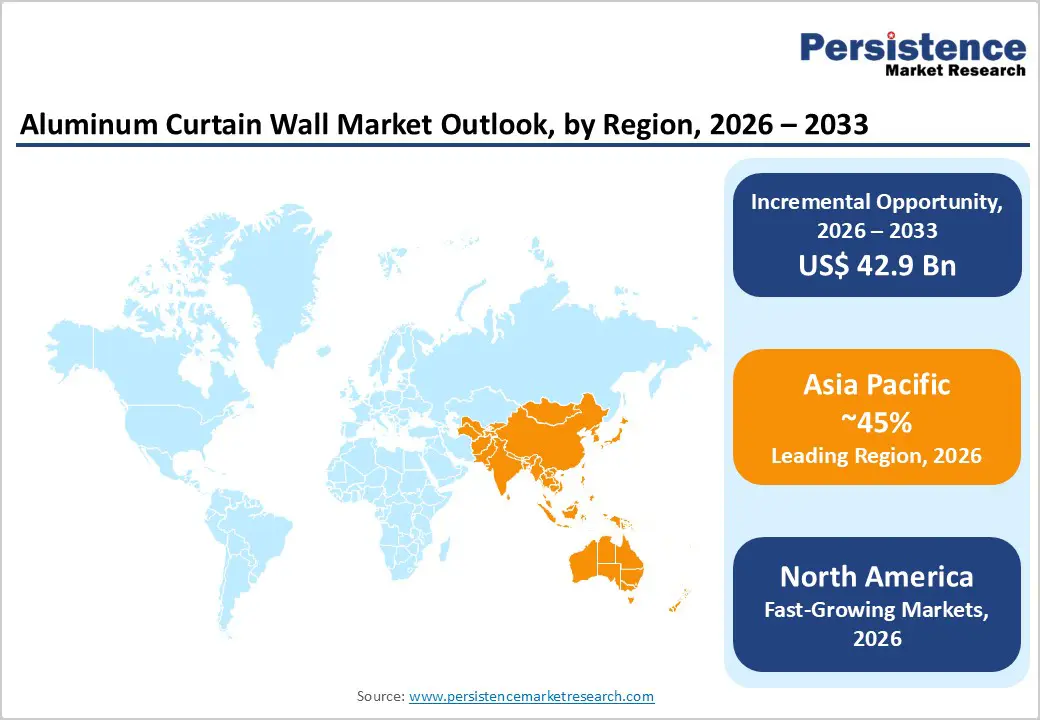

The global aluminum curtain wall market size is likely to be valued at US$ 51.2 billion by 2026, expanding further to US$ 94.1 billion by 2033, demonstrating robust growth potential with a CAGR of 9.1% between 2026 and 2033.

The aluminum curtain wall market exhibits exceptional momentum, driven by three primary catalysts: accelerating urbanization and high-rise commercial construction, stringent energy efficiency regulations mandating advanced building envelope solutions, and technological advancements in lightweight, thermally-broken aluminum systems. The market acceleration reflects increased commercial adoption of sustainable façade solutions and growing preference for prefabricated unitized systems in emerging economies. Commercial buildings, representing over 70% of revenue share, remain the dominant application segment, while Asia Pacific's commanding 45%+ market share underscores the region's construction dominance globally.

Key Industry Highlights:

- Dominant Application Segment: Commercial buildings command above 70% revenue share with high-rise structural applications emerging as the fastest-growing subsegment at 9.5% CAGR, reflecting accelerated vertical urbanization in the Asia Pacific and emerging metropolitan centers.

- Product Type Leadership: Unitized curtain wall systems maintain above 60% revenue dominance through superior factory quality control and installation efficiency, while stick-built systems expand at 9.6% CAGR in retrofit and custom architectural applications.

- Regional Market Concentration: Asia Pacific dominance with 45%+ global revenue share and 9-10% CAGR positioning the region for disproportionate market growth, with China (9.7% CAGR) and India (9.0% CAGR) leading absolute growth increments.

- North American Technology Premium: The U.S. market is expanding at 9.3% CAGR through 2035, above global average, driven by retrofit market expansion, stringent energy codes, and LEED certification adoption requirements.

- Strategic Market Drivers: Energy efficiency regulations and green building mandates creating structural demand for high-performance systems, with approximately 48% of certified green buildings incorporating curtain wall solutions.

| Key Insights | Details |

|---|---|

| Aluminum Curtain Wall Market Size (2026E) | US$ 51.2 Bn |

| Market Value Forecast (2033F) | US$ 94.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.2% |

Market Dynamics

Drivers - Energy Efficiency Regulations and Green Building Mandates

Rise in global energy efficiency regulations and mandatory green building standards directly drive demand for aluminum curtain wall systems as architects and developers seek high-performance building envelope solutions. India's National Building Code mandates 30% energy reduction for new construction, while Maharashtra's Energy Conservation Building Code Rules 2025 establishes binding compliance requirements for commercial buildings exceeding 100 kW electrical load, compelling builders to adopt thermally efficient façade systems. The international LEED certification framework, adopted across 186 countries with 195,000 certified buildings, prioritizes building envelope performance, energy consumption reduction, and environmental impact minimization.

Aluminum curtain walls with thermally broken frames and double-glazed glass assemblies achieve LEED prerequisites for minimum energy performance and reduce operational heating and cooling expenses by up to 25%, directly fulfilling regulatory energy reduction mandates. The Living Building Challenge, requiring 100% zero energy buildings, necessitates high-performance exterior systems, while mandatory renewable energy percentages and smart building technology integration favor aluminum systems with integrated controls and solar-responsive capabilities. Government incentive mechanisms, including tax credits, expedited permitting, and reduced fees for green-certified buildings, accelerate aluminum curtain wall adoption as developers maximize compliance across multiple regulatory frameworks. This regulatory convergence transforms aluminum curtain walls from discretionary architectural elements into essential components for meeting enforceable sustainability standards, positioning the market for sustained expansion through 2035.

Restraint - Regulatory Complexity and Installation Expertise Barriers

Curtain wall system installation requires specialized technical expertise, certified labor, and compliance with evolving building codes across multiple jurisdictions. Geographic fragmentation in building code adoption creates complexity, with only 2 U.S. states (California and Nevada) having adopted ASHRAE 90.1-2016 standards, while 19 states use ASHRAE 90.1-2013 equivalents, and 29 states retain ASHRAE 90.1-2010 or older standards. This regulatory heterogeneity requires system customization across markets, increasing engineering costs and reducing economies of scale.

Fire-resistant requirements, acoustic performance standards, wind load specifications, and seismic considerations necessitate specialized design and installation expertise. Labor shortages in skilled curtain wall installation trades, particularly in developed markets, create project delays and cost escalation. Certification and training requirements for installers add to project overhead. Retrofitting existing building stock with advanced curtain wall systems presents technical complexities around structural compatibility, thermal bridging elimination, and building code compliance verification, limiting the retrofit segment's growth potential despite strong demand signals.

Opportunity - Net-Zero Energy Building Retrofits and Façade Modernization

The existing global building stock represents a massive retrofit opportunity, with approximately 85-90% of buildings expected to remain operational through 2050. Building retrofitting and facade modernization projects are expanding at elevated growth rates as building owners pursue energy efficiency improvements, tenant attraction, and regulatory compliance. Double-glazed, triple-glazed, and ventilated curtain wall systems are experiencing 30% year-over-year adoption growth for retrofit applications across North America and Europe, driven by net-zero energy renovation requirements.

Commercial office building retrofits represent $1.2+ trillion in annual global investment potential across North America, Europe, and Asia Pacific. Aging building stock in developed markets presents immediate retrofit opportunities, with municipal and national governments increasingly mandating energy performance improvements for commercial buildings. The retrofit segment's expansion trajectory suggests a 12-15% CAGR through 2033, outpacing new construction growth. Building owners pursuing ESG objectives and stakeholder pressure for carbon footprint reduction are prioritizing façade modernization as a visible, measurable sustainability commitment, creating sustained market demand beyond traditional new construction cycles.

Category-wise Analysis

Application Insights

The commercial building segment remains the dominant application area in the aluminum curtain wall market, generating over 70% of total revenue and maintaining strong long-term growth momentum. Demand is anchored by large office towers, shopping malls, hotels, corporate campuses, and mixed-use commercial developments, where curtain walls serve as essential elements for architectural distinction, energy-efficient performance, and tenant attraction. Premium commercial projects in major business districts increasingly depend on advanced façade systems to elevate brand identity and justify higher rental values. The rising adoption of smart building technologies such as automated shading, integrated HVAC systems, and intelligent lighting further strengthens demand for technologically compatible curtain wall systems. This segment’s sustained dominance is also supported by recurring investments in new urban commercial construction as well as extensive retrofit programs across global metropolitan centers.

The institutional and public building segment represents the fastest-growing application area, driven by expanding investments in government infrastructure, healthcare facilities, educational institutions, transportation hubs, and cultural establishments. Growing emphasis on sustainable architecture, enhanced daylight utilization, improved energy performance, and modern architectural identities is accelerating curtain wall adoption in these facilities. Additionally, increasing government spending on public infrastructure upgrades, along with the modernization of aging institutional buildings, is creating strong demand for durable, high-performance aluminum façade systems.

Product Type Insights

The aluminum curtain wall market is led by unitized curtain wall systems, which account for over 60% of total revenue due to their strong structural, operational, and economic advantages. These systems are manufactured in controlled factory environments, ensuring higher precision, improved quality control, and reduced risks of on-site installation errors. Their ability to be installed 40-50% faster than stick-built systems significantly shortens project schedules, lowers labor costs, and enhances overall construction efficiency. Unitized systems also deliver superior air-tightness and thermal performance, enabling builders to meet stringent modern energy-efficiency regulations. Their standardized prefabricated modules streamline supply chains, while compatibility with modular and high-rise construction further strengthens their adoption among major commercial and institutional developers seeking predictable performance and cost outcomes.

In contrast, stick-built curtain wall systems represent the fastest-growing segment, expanding at a 9.6% CAGR, driven by their exceptional design flexibility. Since these systems are assembled entirely on-site, they easily accommodate complex geometries, customized façade dimensions, and unique architectural features capabilities often limited in standardized unitized systems. Stick-built solutions are increasingly preferred for small to mid-scale projects, retrofits, and renovations where site-specific adjustments are essential. Their versatility allows regional fabricators to address niche architectural demands, supporting continued market growth despite rising unitized system penetration.

Regional Insights and Trends

Asia Pacific Drives Global Aluminum Curtain Wall Growth with Strong Urbanization and Rising Green Construction Demand

Asia Pacific leads the global aluminum curtain wall market with over 45% revenue share and the fastest growth momentum, expanding at an estimated 9-10% CAGR well above the global average. This dominance is driven by rapid urbanization, a surge in high-rise construction, and growing adoption of energy-efficient façade systems. China accounts for nearly 35-40% of regional demand, supported by large-scale commercial development across Tier-1 and emerging Tier-2/Tier-3 cities. Strong government-backed infrastructure pipelines and rising green building certification rates continue to elevate curtain wall adoption in premium projects.

India is the fastest-growing major market, expanding at around 9% CAGR, fueled by Smart Cities Mission investments, IT-sector campus development, and increasing construction of Grade-A office parks in Bengaluru, Hyderabad, Mumbai, and NCR. Japan maintains steady demand through specialized applications in seismic-resistant architecture, while Southeast Asian markets including Thailand, Vietnam, Indonesia, and Malaysia grow at 8-9% annually, supported by rapid metropolitan expansion.

Growth is further propelled by commercial real estate investment, sustainable building regulations, and supply chain diversification across emerging economies. Strengthening building codes, particularly in China and India, emphasize energy performance, seismic safety, and fire resistance, shaping material specifications. The competitive landscape features dominant Chinese manufacturers alongside global players expanding their presence through technology-driven solutions and regional partnerships.

North America’s Aluminum Curtain Wall Market Accelerates with Energy Efficiency and Retrofit-Driven Growth

North America remains a mature yet fast-evolving aluminum curtain wall market defined by advanced building codes, strong technology adoption, and premium construction standards. The U.S. market leads the region with a projected 9.3% CAGR through 2035, well above the global average, driven by growing demand for energy-efficient building envelopes and a rapidly expanding retrofit sector. Commercial construction activity remains resilient, with high-growth cities such as Austin, Denver, Nashville, and major Sunbelt metros fueling sustained demand for curtain wall installations. Favorable economic conditions, robust capital flows into commercial real estate, and sophisticated financing mechanisms further reinforce regional market expansion.

The United States contributes 75-80% of regional market value, while Canada shows steady growth supported by major development in Toronto, Vancouver, and Montreal, alongside stringent thermal-performance requirements. Mexico is emerging as a developing market, with rising commercial activity in Mexico City, Guadalajara, and Monterrey.

Growth is anchored by strict energy-efficiency regulations such as ASHRAE 90.1-2016, rapid adoption of retrofit solutions, and the rising influence of LEED and Living Building Challenge certifications. Additionally, net-zero mandates, seismic codes, and enhanced fire-safety standards are shaping high-performance system demand. The competitive landscape is defined by strong manufacturer-fabricator partnerships, increasing consolidation, and higher design-phase collaboration. Investment momentum is growing in high-performance glazing, thermal innovation, smart façade technologies, and retrofit-focused services.

Competitive Landscape

The aluminum curtain wall market exhibits moderate consolidation with a combination of global-scale multinational manufacturers, regional leaders, and specialized fabricators maintaining competitive viability. The top 10 manufacturers account for approximately 45-50% of global market value, while the remaining 50-55% is distributed among mid-market regional players and specialized fabricators. This structure reflects the balance between economies of scale in large-project execution and regional/specialized expertise in custom applications.

Geographic market concentration, with Asia Pacific representing 45%+ of global demand, creates advantages for manufacturers with established Asian manufacturing capacity and regional distribution networks. Global leaders (Kawneer, Efco, Schüco) maintain competitive dominance through technological platforms, established customer relationships, and geographic distribution. Chinese manufacturers (Yuanda, Xinyi Glass) are rapidly expanding market share through cost advantages, manufacturing scale, and domestic market dominance. Mid-market regional manufacturers retain competitive positions through specialized expertise, customization capabilities, and relationships with regional architects and developers. The market structure supports competitive dynamism with consolidation opportunities, technology-driven disruption vectors, and emerging competitor threats from alternative façade systems.

Key Industry Developments:

- In August 2024, Alumil introduced LOOP 80, a groundbreaking aluminum recycling initiative that marks a major advancement in sustainable manufacturing. The program focuses on producing an aluminum alloy with a minimum of 80% recycled content, significantly lowering the company's environmental impact. LOOP 80 reflects Alumil’s broader commitment to sustainability and circular economy practices, reinforcing its long-term strategy to integrate high-recycled materials into its product portfolio while promoting more responsible resource use.

Companies Covered in Aluminum Curtain Wall Market

- Alumil

- Aluplex

- ALUTECH

- EFCO, LLC

- Enclos Corp.

- GUTMANN Group

- HansenGroup

- heroal

- HUECK System GmbH & Co. KG

- Josef Gartner GmbH

- Kalwall

- Kawneer Company, Inc.

- National Enclosure Company

- Ponzio

- Purso

- RAICO Bautechnik GmbH

- Reynaers

- SAPA

- Schüco India

- Skansa

- Other Market Players

Frequently Asked Questions

The Aluminum Curtain Wall market is estimated to be valued at US$ 51.2 Bn in 2026.

The key demand driver for the Aluminum Curtain Wall market is the rising global focus on energy-efficient, high-performance building façades driven by strict sustainability regulations and growing commercial construction activity.

In 2026, the Asia Pacific region will dominate the market with an exceeding 45% revenue share in the global Aluminum Curtain Wall market.

Among applications, commercial buildings have the highest preference, capturing beyond 70% of the market revenue share in 2026, surpassing other applications.

Alumil, Kawneer Company, Inc., Schüco International / Schüco India, Reynaers Aluminium, GUTMANN Group, Josef Gartner GmbH (Permasteelisa Group), Enclos Corp. are a few leading players in the Aluminum Curtain Wall market.