- Metals & Minerals

- Alumina Market

Alumina Market Size, Share, and Growth Forecast for 2026 - 2033

Alumina Market by Grade (Smelter Grade, Chemical Grade), Application (Aluminum Production, Alumina Hydrate, Calcined Alumina), and Regional Analysis for 2026 - 2033

Alumina Market Size and Trends

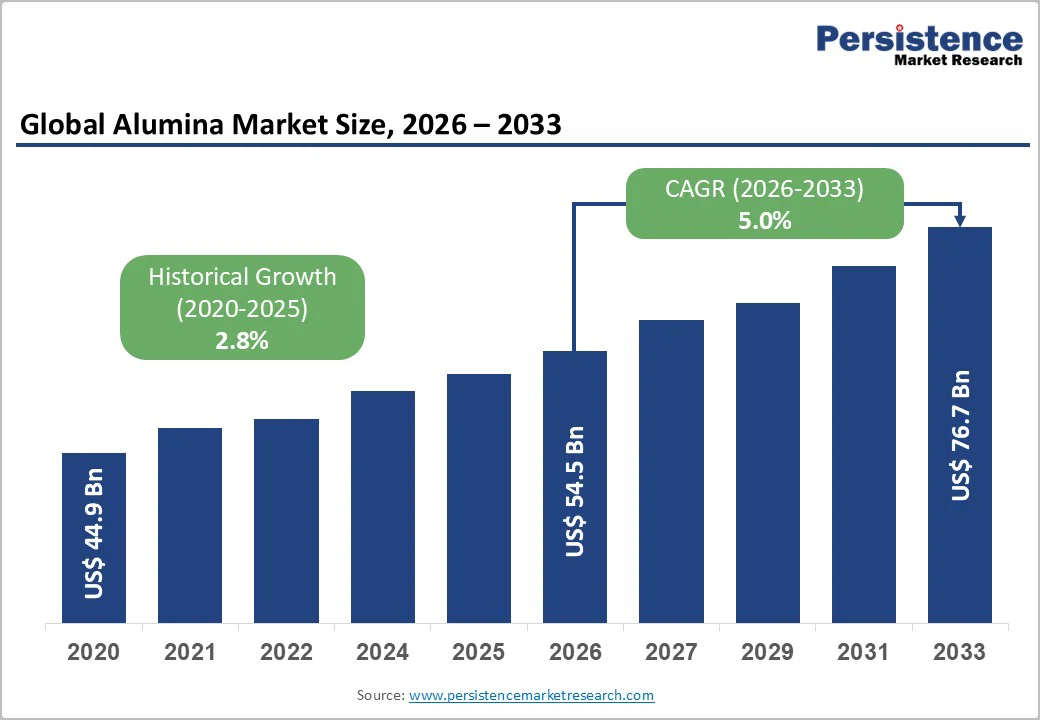

The global alumina market size is expected to be valued at US$54.5 billion in 2026 and is projected to reach US$76.7 billion by 2033, growing with a CAGR of 5% between 2026 and 2033.

The market expansion is driven by three primary factors: accelerating aluminum consumption across lightweight transportation & sustainable packaging applications, strategic capacity expansions in emerging markets, and technological advancements in refining processes that reduce production costs and environmental impact.

Key Industry Highlights

- Dominant Grade: In 2025, smelter-grade alumina represented over 92% of the total demand, growing at a baseline 5.0% CAGR anchored to primary aluminum production demand.

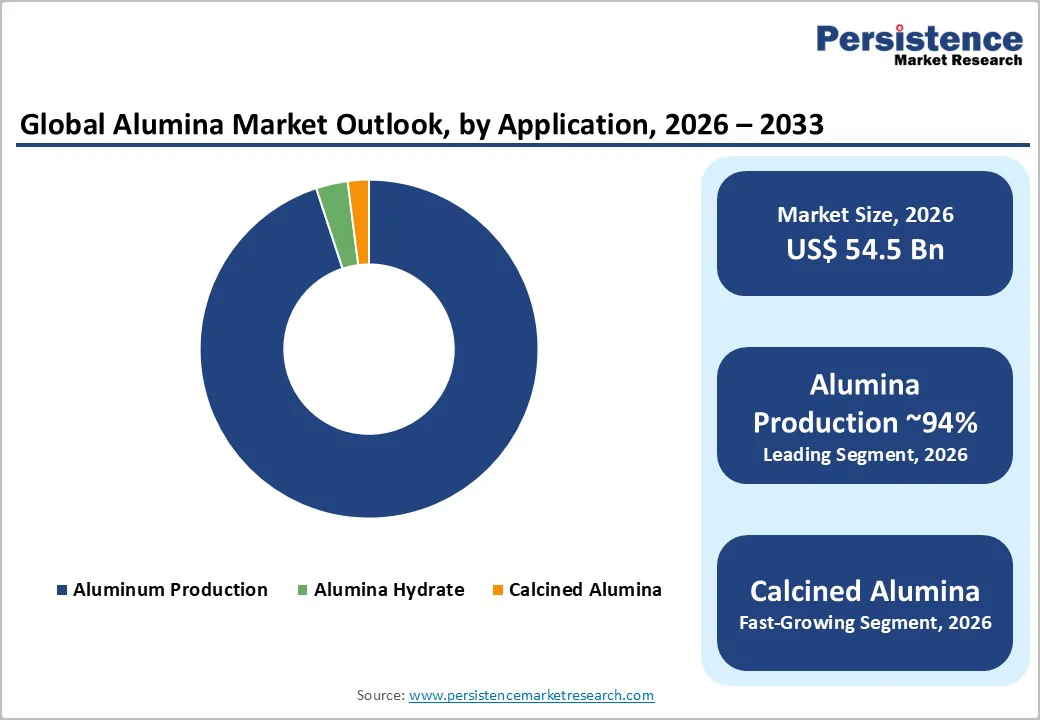

- Leading Application: Aluminum production continues to dominate, holding over 94% share in 2026, with automotive transportation representing the fastest-growing end-use category at 5% CAGR, reflecting EV adoption and lightweighting imperatives.

- Production Scenario: Global alumina production exceeded 144 million tons in 2025, with over 50% originating from China, showcasing its supremacy in the industry.

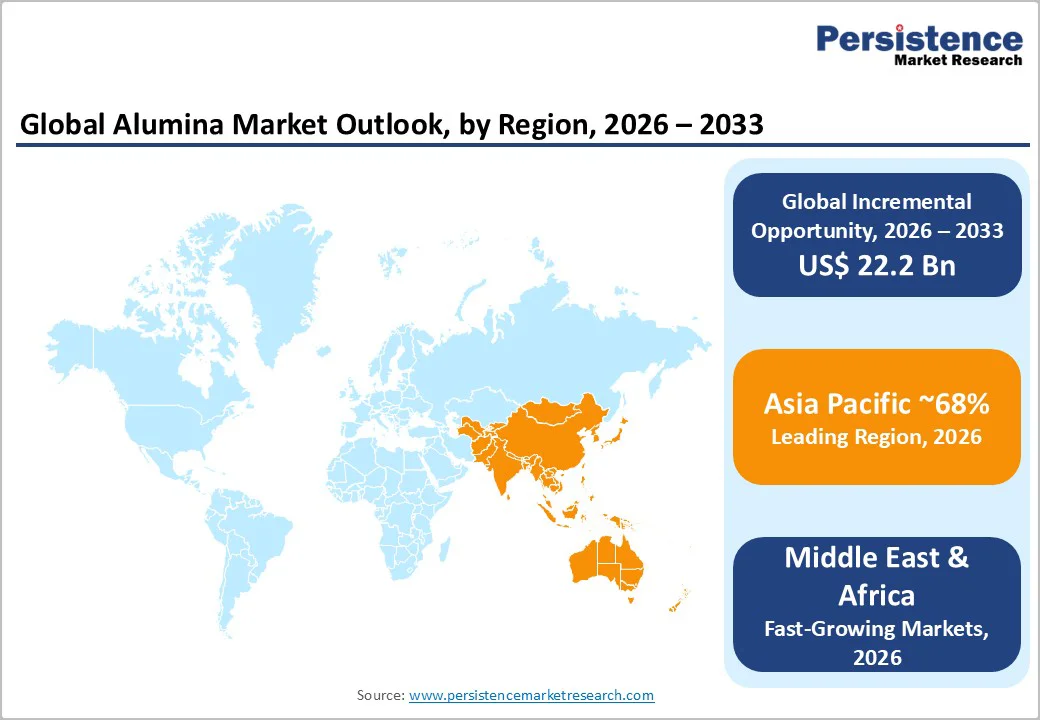

- Regional Dynamics: Asia Pacific commanding over 65% global market share, with China at US$29 billion in 2026, demonstrating baseline maturity, and India emerging as the fast-growing major economy with 8% CAGR

- Capacity Expansion: Emerging market capacity expansion with 23 million tons cumulative new refining capacity (China 13 mnt, India 1.5 mnt, Indonesia 4.5 mnt, Guinea 2 mnt) entering production 2024-2026, fundamentally restructuring global supply chains toward lower-cost regions.

- Price Volatility: The global alumina market has experienced fluctuating prices, reaching an all-time high of US$695 per tonne in Q4 2024 and US$650 in Q1 2025; however, prices have since declined owing to excess supply and muted consumer demand.

| Key Insights | Details |

|---|---|

|

Alumina Market Size (2026E) |

US$54.5 Bn |

|

Market Value Forecast (2033F) |

US$76.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

2.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

Market Dynamics

Drivers - Skyrocketing Demand for Aluminum from the Construction and Automotive Sectors to Boost Sales of Smelter Grade Alumina

Alumina is classified into two primary grades: Smelter Grade Alumina (SGA) and Chemical Grade Alumina (CGA). The smelter-grade alumina is produced only by calcination of aluminum hydroxide in refineries and is mainly accounted for in the market. In 2025, SGA accounted for roughly 92% of total alumina demand and is anticipated to grow at a relatively strong CAGR of 5.0% from 2026 to 2033.

There is currently significant demand in the automotive industry for lightweight, high-performance materials and weight reductions, which are considered necessary to improve fuel efficiency and further augment battery range, especially in electric vehicles. This trend is expected to lead to burgeoning demand for advanced aluminum materials.

Aluminum parts are expected to replace iron and steel components in vehicles as early as the next ten years, greatly enhancing aluminum demand. Various nations are thus directed towards improving their production capacities to meet this demand.

Bauxite is the main raw material for alumina. In an average refining process, 4 to 5 tons of bauxite are processed to yield roughly 1.95 tons of alumina, of which, via the electrolytic process, almost 1 ton of primary aluminum can be produced.

This grade of alumina is the one necessary to produce aluminum for derived value-added products such as flat, extruded, and forged. Aluminum as a construction material is critical for numerous industries, particularly automotive, aerospace, packaging, and consumer goods.

- The global aluminum market is forecast to surpass a whopping US$400 billion by 2033.

Technological Advancement and Energy Efficiency Improvements in Alumina Refining Processes

Continuous innovation in the Bayer process and emerging refining methodologies has substantially reduced production costs and environmental impact, creating competitive advantages for early adopting producers.

Modern refining technologies have improved thermal efficiency by 15-25%, reducing energy consumption per ton of alumina produced. Advancements in catalyst support materials and filtration systems have enabled smaller-scale, modular refinery designs, facilitating capacity expansion in locations previously considered economically non-viable.

China's refinery utilization reached 98.2% in Q1 2025, with energy efficiency improvements enabling profitability amid price volatility. The shift toward renewable energy integration, particularly hydroelectric in Yunnan province and wind/solar in Inner Mongolia, has created structural cost advantages for green alumina production, with market pricing premiums of 5-15% observed for certified low-carbon alumina.

Government support for cleaner production methodologies across developed and developing economies has accelerated technology adoption cycles, creating market pull for innovative suppliers.

Restraint - Supply Chain Vulnerability, Bauxite Availability Constraints, and Fluctuating Price Levels are Poised to Have Big Knocks on Profitability Metrics

Alumina production dependency on bauxite ore creates structural supply chain fragility concentrated in limited geographic regions, with Guinea, Brazil, and Australia collectively controlling 75% of proven reserves. Australia's production disruptions in 2024 (Rio Tinto, South32) led to an alumina price escalation of more than 70% year-over-year, highlighting supply concentration risk.

Export dependency creates geopolitical vulnerability: Indonesia's domestic ore reservation policies, combined with changing trade dynamics, create uncertainty for international refineries. Bauxite ore beneficiation contamination and mineral composition variability require continuous process adaptation, increasing operational complexity and capex requirements.

Reserve depletion trajectories in established mining regions create long-term cost escalation risks, with new mining development requiring 7–10-year lead times and US$2-4 billion capex commitments. These structural constraints limit production flexibility and create cyclical cost pressures independent of refining efficiency improvements.

The average alumina price in Q42024 surged to US$695 per ton, a 50% increase from 2020. Maintaining high alumina prices is dependent on energy cost concerns across the value chain, posing a challenge in the future. This scenario creates an opportunity for market participants to examine solutions to improve market resilience and stability.

Opportunities - High Purity Alumina (HPA) Applications in Semiconductor, Advanced Ceramics, and Display Technologies

The high-purity alumina (HPA) market is poised for distinct growth, with a 21.6% CAGR between 2026 and 2033, compared to 5.0% overall market growth, reflecting premium valuation and specialized application requirements. The global high-purity alumina market is projected to exceed US$13 billion by 2033. Semiconductor manufacturing uses ultra-pure alumina in substrates and packaging materials, with demand expanding directly in line with global semiconductor capacity additions.

Advanced ceramic applications in telecommunications infrastructure, aerospace components, and industrial high-temperature applications represent nascent, high-margin opportunities. Display technology innovation, including micro-LED, flexible displays, and augmented reality applications, requires specialized alumina specifications commanding 3-4x pricing premiums relative to smelter-grade material.

Water filtration and precision polishing applications serve environmental remediation and specialty manufacturing segments. Market sizing for the high-purity segment projects US$22.87 billion by 2033, representing an incremental value-creation opportunity for producers with specialty processing capabilities and quality certifications.

Specialty Alumina Market Expansion Supporting Digital Transformation and Clean Energy Transition

Reactive and calcined alumina grades, representing 4% of the overall market, are experiencing accelerating growth, with 7-8% CAGR driven by catalyst applications, filtration media, and emerging technology adoption.

The global catalyst market's expansion to US$35 billion by 2026 is expected to generate incremental alumina demand for support materials in petrochemical, refining, and environmental remediation applications. Clean energy transition creates demand expansion for specialized alumina grades: lithium-ion battery separator coatings, hydrogen production catalysts, and carbon capture support materials.

The global activated alumina market is forecasted to surpass US$1.5 billion by 2033, reflecting growing adoption in industrial desiccation, air purification, and wastewater treatment applications. These specialty segments command 15-25% price premiums over commodity grades and demonstrate counter-cyclical demand characteristics, providing portfolio diversification and margin stabilization for diversified producers.

Category-wise Insights

Grade Insights

Leading Segment: Smelter Grade Alumina (Over 92% of Global Demand)

Smelter-grade alumina (SGA) remains the dominant segment, accounting for over 92% of global alumina demand, with a market size estimated at US$50.4 billion in 2026 and projected to reach US$70.6 billion by 2033. This segment's dominance reflects its essential role as primary feedstock for primary aluminum production, which constitutes 94% of total alumina consumption.

SGA market growth follows aluminum smelting capacity expansion trajectories, with China's capacity additions and strategic refinery operations in Vietnam, Indonesia, and Bahrain driving incremental volume absorption. The Bayer process remains the standardized production methodology, with continuous technological refinement improving energy efficiency and purity consistency.

Regional production consolidation around low-cost hydroelectric (Yunnan) and wind/solar (Inner Mongolia) resources has created competitive cost structures enabling Chinese producers to maintain global pricing influence.

Fastest Growing Segment: Chemical Grade and Specialty Alumina

Chemical-grade and specialty alumina segments demonstrate substantially elevated growth trajectories compared to commodity smelter-grade material. This acceleration reflects demand expansion from semiconductor manufacturing, advanced ceramics production, lithium-ion battery separator coating, and emerging display technology applications. The high-purity alumina (HPA) segment is specifically exhibiting accelerating adoption in electronics and energy storage applications.

Reactive alumina demand growth reflects the expanding catalyst market, environmental remediation applications, and the adoption of industrial filtration media. Activated alumina segment growth demonstrates emerging adoption in hydrogen production and carbon capture support materials. These specialty grades typically command a price premium over smelter-grade material, creating substantial margin expansion opportunities for producers with specialized processing capabilities and quality certifications required for semiconductor and advanced material applications.

By Application Insights

Dominant Segment: Aluminum Production (Over 94% of Global Demand)

Aluminum production accounts for the overwhelming share of global alumina consumption, reflecting the essential feedstock requirement for primary aluminum smelting. This segment encompasses both conventional aluminum casting alloys for transportation, construction, and packaging applications, and emerging battery-grade aluminum for lithium-ion cell manufacturing.

Aluminum's lightweight properties (one-third the density of steel) and infinite recyclability have driven market share expansion in automotive lightweighting applications, with each vehicle containing 40-60kg of aluminum compared to 20-30kg historical levels. Commercial aircraft construction requires an 80% aluminum content, driving demand for aerospace-grade aluminum.

The packaging segment represents 25% of end-use aluminum consumption, with beverage can and food packaging applications demonstrating resilience across economic cycles. This application segment's growth directly correlates with global manufacturing capacity additions, with China's 43 million tons of aluminum production (2024) requiring a proportionate alumina feedstock supply.

Secondary Segments: Alumina Hydrate and Calcined Alumina

Alumina hydrate applications represent specialized segments serving refractories manufacturing (refractory bricks, gunning materials for high-temperature furnaces), fire-resistant ceramics for aerospace and defense applications, and emerging thermal management applications in electronics.

Alumina hydrate offers hydroxyl bonding advantages in refractory applications, with U.S. defense-sector adoption increasing 2.5x between 2024 and 2025, reflecting heightened military manufacturing demand. Calcined alumina applications include industrial abrasives, polishing media, and emerging precision manufacturing applications that require specific particle size distributions and thermal stability.

Both application segments demonstrate pricing premiums of 50-100% relative to primary aluminum production feedstock, reflecting specialized manufacturing processes and quality certifications required for industrial and defense applications.

Regional Insights

North America Alumina Market: Mature Market Stability with Specialized Application Focus

North America accounted for more than 7% of the global alumina demand in 2025, with very slow growth expected in the coming years. Canada has the major alumina demand in the region, primarily due to its lower carbon footprint production. The existence of hydropower sources empowers Canada to make its products competitive in pricing against other areas. It is also considered the fourth-largest primary aluminum producer in the world after China, India, and Russia.

The U.S. was Canada's largest export destination for aluminum products, accounting for around 90% of total aluminum imports. This trend will likely continue for the next few years, as the country is over-reliant upon imports to fulfill its demands for aluminum and aluminum products.

The U.S. alumina market size is projected to exceed US$4.5 billion by 2033, growing with a CAGR of 2.8% between 2026 and 2033. U.S. automotive lightweighting initiatives and EV battery component manufacturing create specialized alumina demand for high-purity applications, commanding premium pricing relative to commodity smelter-grade material.

Defense sector demand expansion, particularly refractory-grade alumina for military applications, demonstrated 2.5x growth between 2024-2025, reflecting geopolitical supply chain reshoring initiatives. Canada's hydroelectric-powered aluminum production and export orientation to U.S. markets create integrated North American supply chains. A regulatory environment emphasizing carbon footprint reduction in the transportation sector is driving material specification shifts toward aluminum with certified low-carbon processing provenance.

Europe Alumina Market: Demonstrating Mature Market Dynamics and Growth Profile

Europe is the second-largest alumina market globally, projected to surpass US$8.5 billion by 2033, up from a baseline of approximately US$7.2 billion in 2026. This growth trajectory reflects a 2.0% CAGR over the forecast period, substantially below the global average, indicating developed-economy market saturation and manufacturing relocation. Russia accounts for over 40% of the regional demand, followed by Germany, U.K., France, and Spain, with significant geographic concentration around automotive manufacturing hubs (Germany) and aerospace production centers (the UK, France).

European Union environmental regulations, including Extended Producer Responsibility frameworks and carbon border adjustment mechanisms, have created substantial compliance cost structures for alumina producers. Water usage restrictions in Mediterranean regions create capacity constraints for traditional refinery operations. Circular economy directives emphasizing aluminum recycling have reduced primary aluminum demand growth trajectories while driving secondary aluminum production expansion. Premium pricing for certified low-carbon alumina (produced using renewable energy) reaches 10-15% above commodity benchmarks, reflecting sustainability purchasing mandates across automotive and aerospace supply chains.

METLEN's January 2025 investment (US$333.76 million) in bauxite, alumina, and gallium production capacity expansion reflects the European producer's commitment to supply chain integration and margin enhancement. Strategic partnerships with Rio Tinto provide long-term bauxite supply security and alumina offtake agreements. Investment opportunities focus on specialty alumina production supporting semiconductor and advanced material applications, with European research institutions providing technology access and innovation collaboration.

Asia Pacific Alumina Market: Leading Region with Differential Growth Dynamics

The Asia Pacific region dominates the global alumina market, accounting for over 65% market share in 2026. Regional growth trajectories demonstrate significant heterogeneity: China expanding at 4.8% CAGR (2026-2033) versus Japan's mature market 1.5% growth. India represents the fastest-growing major economy with 8% CAGR (2026-2033), while ASEAN nations (Indonesia, Vietnam, Thailand) collectively demonstrate 6.9% average growth.

China's alumina market is projected to reach US$29 billion in 2026, accounting for over 75% of regional consumption. The government-imposed 45.5-million-ton aluminum production cap creates strategic capacity constraints, limiting primary alumina demand expansion despite refining capacity additions.

China's 13 million tons of new alumina refinery capacity added in 2025 positions the nation to export surplus supplies to regional markets, creating pricing pressure dynamics. Production consolidation around renewable energy regions (Yunnan hydroelectric, Inner Mongolia wind/solar) creates competitive cost advantages.

Chinese producers (Chalco, Coalco, regional operators) maintain integrated bauxite mining and alumina refining operations, providing supply chain control. Capacity utilization reached 98.2% in Q1 2025, indicating limited production flexibility and limited maintenance of pricing power despite the emergence of a surplus.

India's alumina market is projected to exceed US$5 billion by 2033, growing at 8% CAGR, reflecting explicit policy objectives toward import substitution and integrated supply chain development. Vedanta's planned US$15 billion integrated complex in Odisha represents an anchor investment with a 1.5 million tonne initial phase expanding toward 2+ million tonnes ultimately. India's alumina imports collapsed 66.27% year-over-year (April 2024-March 2025), reflecting rapidly expanding domestic capacity absorption. However, India imported 2.45 million tonnes of alumina in CY 2024, indicating continued import requirements during the transition period. Price sensitivity in the Indian market reflects developing-economy purchasing patterns, with buyers deferring procurement during elevated pricing periods (2024 alumina price surge to 70% above the prior-year depressed import volumes). Future demand expansion tied to aluminum smelting capacity growth (targeting 6-6.5 mntpa by end-2025 from 4.15 mntpa current production).

Southeast Asia represents a critical production expansion center, with Indonesia emerging as a major new alumina refining location. Three major refinery projects (SGAR, PT Dinamika Sejahtera Mandiri, PT Quality Sukses Sejahtera) collectively add 4.5 million tons annual capacity, with Phase 1 operations commencing in 2024-2025. Indonesia's geographic proximity to bauxite reserves and low-cost energy infrastructure creates structural competitive advantages. Vietnam and Thailand represent secondary emerging refining locations.

ASEAN market growth reflects manufacturing consolidation from higher-cost regions and expanding aluminum consumption in the commercial and construction sectors. Price-sensitivity in Southeast Asian markets creates competition dynamics requiring cost optimization and supply security for producer profitability maintenance.

Middle East & Africa Alumina Market: Guinea's Transition: From a Bauxite Exporter to Value-Added Alumina Production Hub

Guinea represents a critical bauxite supply source with 75% of global proven reserves concentrated across Guinea, Brazil, and Australia. However, Guinea's August 2025 revocation of Emirates Global Aluminium's (EGA) mining concession, reassigning the 690 km² concession (400 million tonnes estimated bauxite reserves) to state-backed Nimba Mining SA, establishes a precedent for aggressive resource nationalism and state control expansion across African bauxite-producing regions.

The GAC license revocation originated in October 2024 when Guinean customs authorities suspended bauxite exports, citing customs duties compliance violations and delayed progress on domestic alumina refinery commitments. By May 2025, formal license revocation proceedings commenced; in August 2025 finalized the concession reassignment was finalized without compensation. This action eliminates EGA's anticipated 2-million-ton annual alumina capacity addition (planned September 2026 commencement), which would have represented strategic production diversification outside established Chinese and Western producer capacity.

Guinea Bauxite Market Dynamics: Despite GAC license revocation, Guinea's bauxite exports surged 36% in H1 2025 to nearly 100 million tonnes, driven by Chinese demand and infrastructure growth. However, state-backed Nimba Mining SA management of the reassigned concession introduces uncertainty regarding export capacity maintenance, refining investment commitments, and operational efficiency compared to EGA's integrated operations.

African market growth remains constrained by limited domestic aluminum consumption, with production oriented toward export markets. However, Guinea's strategic shift toward state control and domestic value-addition reflects broader African policy objectives to maximize mineral resource returns through domestic refining, smelting, and advanced material production, creating long-term structural change in bauxite supply chain management.

Competitive Landscape

Manufacturers are Driving Their Commitment Toward Sustainability and The Circular Economy

Several leading companies such as Aluminium Corporation of China Limited (CHALCO), China Hongqiao Group Ltd, Shandong Xinfa Group, Alcoa, Rio Tinto Alcan, and Rusal have successfully integrated their alumina businesses. These manufacturers are pursuing capacity expansion and resolving bottlenecks present in their facilities that would have positive implications on general performance.

Sustainability and carbon reduction are now top priorities, constituting the technological drivers for advancement within the alumina sector. In a radical rethink, this would set out to address every aspect of the value chain, right from bauxite and alumina to finished aluminum products.

- For example, in 2022, Alcoa executed a pioneering alumina refining technology that substantially lowered energy emissions and, in a sustainable manner, managed bauxite residue, reiterating their commitment.

Recent Developments

- In 2025, METLEN Energy & Metals signed a long-term strategic agreement with Rio Tinto to secure supply chain improvements in both Bauxite and Alumina. The investment will significantly increase the refinery’s (plant in Agios Nikolaos, Viotia, Greece) output from 860,000 Tonnes to 1,265,000 Tonnes annually.

- In 2025, Emirates Global Aluminium completed an expansion at its Al Taweelah alumina refinery. This expansion will unlock up to 50,000 tonnes of additional alumina production per year.

- In 2025, Rusal, a leading aluminum company in Russia, announced plans to acquire a 26% share in an Indian alumina refinery owner for US$243.75 million. The strategic move is expected to aid Rusal in reducing dependency on third-party raw materials, with the company losing almost 40% alumina supply in the past couple of years.

- In 2024, Press Metal Aluminium Holdings Bhd declared that it is expected to spend RM 1.04 Bn in cash for the planned new alumina refinery joint venture in West Kalimantan, Indonesia. Strategic partnership agreements to develop a strong joint venture together with PT Kalimantan Alumina Nusantara (KAN) and its partners, PT Alakasa Alumina Refineri (AAR) and PT Dinamika Sejahtera Mandiri (DSM), have been signed with great anticipation.

Companies Covered in Alumina Market

- Aluminum Corporation of China Limited (Chalco)

- Alcoa Corporation

- China Hongqiao Group Co. Ltd.

- Jinjiang Group

- Rio Tinto Alcan

- Norsk Hydro ASA

- South32 Limited

- United Company Rusal IPJSC

- Alumina Limited

- Vedanta Limited

- Emirates Global Aluminum (EGA)

- Nalco

Frequently Asked Questions

The global alumina market was valued at around US$44.9 billion in 2020 and is projected to reach approximately US$76.7 billion by 2033, driven by aluminum production and specialty applications.

Asia Pacific is the leading region, accounting for more than 65% of global alumina demand, with China as the largest consumer and India as the fastest-growing market during the forecast period.

Alumina is primarily used in aluminum production, which consumes over 94% of global output, while the rest goes into applications such as refractories, ceramics, abrasives, and high-purity grades for electronics and batteries.

Rising adoption of electric vehicles, advanced ceramics, semiconductors, and energy storage systems is boosting demand for high-purity and specialty alumina grades, which are growing faster than smelter-grade material.

Guinea’s large bauxite reserves and recent license actions affecting major producers have increased focus on supply security, prompting alumina producers to reassess sourcing strategies and diversify away from single-country dependence.