- Food Packaging

- Aluminum Foam Market

Aluminum Foam Market Size, Share, and Growth Forecast, 2026 - 2033

Aluminum Foam Market by Structure (Closed-cell, Open-cell, Others), Application (Energy Absorber, Sound Insulation, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Aluminum Foam Market Size and Trends Analysis

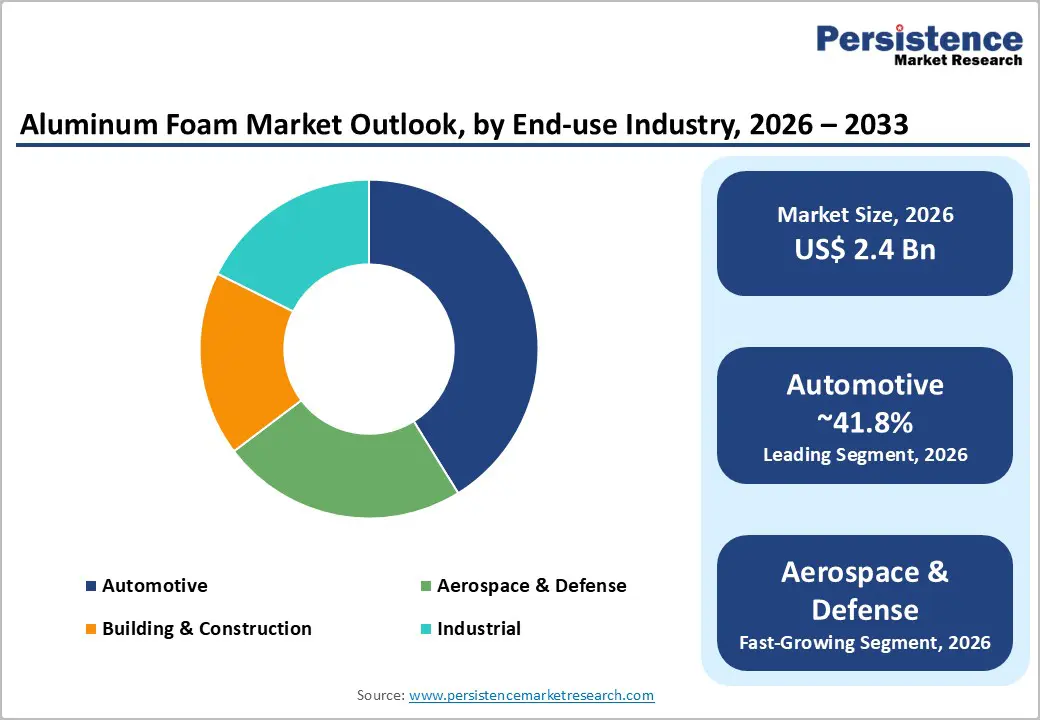

The global aluminum foam market size is likely to be valued at US$2.4 billion in 2026 and is expected to reach US$4.2 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033, driven by the increasing adoption of lightweight, energy-absorbing materials across automotive, aerospace, and industrial sectors. Rising use of aluminum foam in thermal-management systems, filtration modules, and acoustic construction panels further strengthens demand.

Key growth enablers include transportation lightweighting mandates, continuous advances in foam manufacturing technologies such as stabilized and metal infiltration processes, and accelerating industrialization in Asia Pacific. Key risks include aluminum price volatility and challenges in scaling high-quality foam production while maintaining structural consistency.

Key Industry Highlights

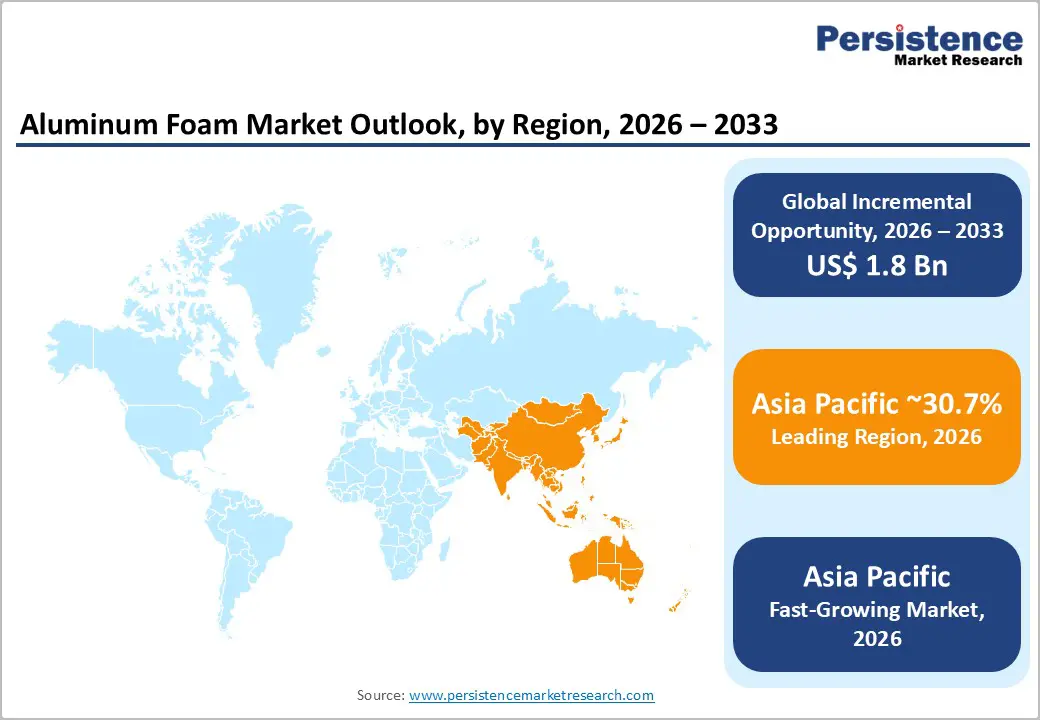

- Leading Region: Asia Pacific, is projected to account for approximately 30.7% of market share, supported by large-scale automotive production, expanding domestic aluminum foam manufacturing in China.

- Fastest-growing Region: Asia Pacific, driven by rapid EV adoption, infrastructure expansion in India and ASEAN countries, and government-backed industrial incentives accelerating pilot-to-volume production.

- Investment Plans: Capital allocation is focused on capacity expansion, localization, and application-specific R&D, with increased investments in EV safety components, thermal-management systems, and defense-grade materials, particularly in China, the U.S., and Germany.

- Dominant Structure: Closed-cell aluminum foam, anticipated to hold approximately 60.4% revenue share, owing to its superior compressive strength, predictable deformation behavior, and widespread use in automotive crash structures and safety-critical applications.

- Leading End-use Industry: Automotive end-use industry, to account for around 41.8% of revenue share, supported by lightweighting initiatives, EV platform development, and growing adoption in crash management and battery protection systems.

| Key Insights | Details |

|---|---|

| Aluminum Foam Market Size (2026E) | US$2.4 Bn |

| Market Value Forecast (2033F) | US$4.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automotive & Transport Lightweighting

Automotive and transportation manufacturers are under sustained pressure to reduce vehicle curb weight by 5-15% per redesign cycle to meet fuel-efficiency, emissions, and electric-vehicle range targets. Lightweight materials, including aluminum foams, have become priority substitutes for conventional steel and polymer structures. Aluminum foam adoption has accelerated in foam-filled crash management systems, anti-intrusion bars, and interior acoustic panels, particularly within electric vehicles, where every kilogram of weight reduction directly improves battery range. Market impact: Aluminum foam’s combination of high energy absorption, low density, corrosion resistance, and recyclability supports its substitution into safety-critical and NVH components, reinforcing strong demand growth within the automotive end-use segment.

Thermal Management and Filtration in Industrial and Defense Applications

Open-cell aluminum foams offer exceptionally high surface area and controlled porosity, enabling compact and high-efficiency heat exchangers and filtration systems. These properties are increasingly valuable in electronics cooling, HVAC systems, aerospace platforms, and defense equipment, where space constraints and thermal loads are intensifying. Growth in electrification, data-dense electronics, and defense modernization has translated into tangible procurement activity for aluminum-foam-based thermal solutions. Market impact: As system-level efficiency becomes a key purchasing criterion, aluminum foam transitions from a structural material to a functional subsystem component, supporting premium pricing and expanding the addressable market beyond traditional crash and construction applications.

Production Scale and Quality Consistency

High-quality aluminum foam production requires precise control of pore size, distribution, alloy composition, and post-processing conditions. Manufacturing variability can increase rejection rates and elevate unit costs compared with conventional metal products. In pilot and early commercial production lines, scrap and yield losses can add 10-30% to effective manufacturing costs, reducing competitiveness in price-sensitive applications. In addition, scaling production while maintaining mechanical consistency often extends commercialization timelines by 12-24 months, particularly for automotive and aerospace programs requiring extensive validation.

Barrier Analysis - Feedstock Price Volatility and Downstream Processing Costs

Aluminum foam production remains highly sensitive to fluctuations in aluminum commodity prices, which can vary by ±10-25% across multi-year cycles. Closed-cell foams, in particular, contain a high proportion of aluminum by weight, amplifying raw-material cost exposure. Downstream processing requirements-including machining, joining, and surface treatments- can add 15-40% to finished-component costs. Together, these factors constrain near-term margin expansion and can delay OEM adoption when total cost of ownership comparisons favor established alternatives.

Opportunity Analysis - OEM Partnerships for Crash-Worthy EV Platforms

A significant opportunity exists for aluminum foam suppliers to secure multi-year supply agreements with electric-vehicle platforms requiring integrated crash-energy management and acoustic solutions. Assuming 1-2 kilograms of aluminum foam per vehicle across a conservative subset of 5 million EVs by 2030, incremental annual material demand could reach tens to low-hundreds of millions of U.S. dollars by the mid-2030s. Early OEM partnerships that validate manufacturability and performance create high switching costs and long-term revenue visibility for qualified suppliers.

Modular Heat-Exchanger and Filtration Retrofit Market

Retrofitting industrial HVAC systems, high-performance cooling equipment, and military electronics with compact aluminum-foam-based heat exchangers and filters represents a near-term scale opportunity. Even 1% penetration of global high-value thermal-management retrofit spending would generate a multi-million-dollar niche market. Suppliers capable of delivering standardized, certified modules rather than custom designs can shorten sales cycles, reduce integration complexity, and command higher margins than bulk structural foam applications.

Category-Wise Analysis

Structure Insights

Closed-cell aluminum foam is likely to be the dominant structural configuration, accounting for approximately 60.4% of the total revenue share in 2026, supported by its sealed pore morphology and high mechanical stability. The closed-cell structure delivers superior compressive strength, predictable stress-strain behavior, and consistent energy absorption, which are essential for safety-critical applications. These characteristics underpin its widespread use in automotive crash management systems, anti-intrusion door beams, underbody protection panels, and blast-resistant architectural elements.

Commercial adoption is concentrated among specialized manufacturers with advanced foaming control technologies capable of producing uniform cell size and density at an industrial scale. Leading automotive OEMs integrate closed-cell aluminum foam into EV battery enclosures and side-impact protection modules to enhance occupant safety without increasing vehicle mass. Due to stringent performance validation requirements and limited supplier availability, closed-cell foams continue to command premium pricing, reinforcing their strong revenue contribution despite moderate volume growth.

Open-cell aluminum foam is likely to be the fastest-growing structural segment, driven by its interconnected porosity that enables fluid permeability, high surface area, and efficient thermal dissipation. This structural format is increasingly adopted in heat exchangers, filtration systems, catalyst substrates, acoustic dampers, and aerospace electronics cooling assemblies. Demand growth is particularly strong in industrial cooling systems, defense avionics, and electric power electronics, where thermal performance and weight reduction directly impact system efficiency and reliability.

Technological advances in reticulation processes, powder metallurgy, and additive manufacturing-assisted foam architectures are improving consistency and functional integration. Surface treatments and ceramic or graphene-based coatings further enhance corrosion resistance and heat transfer efficiency. As end-use demand shifts toward multifunctional, performance-driven components rather than purely load-bearing structures, open-cell aluminum foam is projected to outpace closed-cell formats in CAGR terms over the forecast period.

End-user Industry Insights

Automotive applications are anticipated to represent approximately 41.8% of revenue share in 2026, reflecting sustained demand for lightweight materials that enhance crash safety, noise-vibration-harshness (NVH) control, and energy efficiency. Aluminum foam adoption is strongest in electric vehicles and premium passenger cars, where OEMs prioritize structural safety while compensating for battery-related weight increases.

Closed-cell aluminum foams are increasingly incorporated into front and rear crash boxes, door impact beams, roof reinforcements, and battery protection casings, offering controlled deformation during collisions. Leading automakers in Europe and Asia have begun pilot integration into modular EV platforms, signaling gradual penetration beyond niche models. As regulatory pressure on vehicle emissions and safety standards intensifies, automotive applications will continue to anchor market revenues, even as growth rates stabilize.

The aerospace and defense segment is likely to be the fastest-growing end-use segment, driven by the sector’s exceptional emphasis on weight reduction, thermal stability, acoustic damping, and impact resistance. Aluminum foam is increasingly specified in aircraft interior panels, satellite thermal management systems, radar housings, blast-mitigation structures, and lightweight heat exchangers. Although procurement cycles are long and certification requirements are rigorous, unit values and operating margins are significantly higher than in automotive applications.

Growth is reinforced by defense modernization programs, rising military electronics density, and increased investment in space and unmanned aerial systems. Open-cell foams are gaining traction in avionics cooling and acoustic liners, while closed-cell variants are deployed in ballistic and shock-absorbing applications. As aerospace platforms evolve toward higher electrical loads and compact system integration, aluminum foam adoption is expected to accelerate at a robust CAGR through 2033.

Regional Insights

North America Aluminum Foam Market Trends - Defense-Driven Lightweighting and EV Integration

North America is expected to be a strategically important aluminum foam market, underpinned by advanced manufacturing capabilities, a strong concentration of automotive, aerospace, and defense OEMs, and consistently high defense expenditure. The U.S. leads regional demand, accounting for the majority of consumption due to its mature R&D ecosystem and early adoption of aluminum foam in high-value, performance-critical applications. Canada contributes through the use of stabilized aluminum foam panels in architectural façades, transportation infrastructure, and noise-mitigation barriers, while Mexico plays a growing role as an automotive manufacturing and assembly hub supporting U.S.-based OEM supply chains.

Key growth drivers include U.S. defense modernization programs, accelerated electric vehicle (EV) platform development, and a deep ecosystem for material qualification and testing. Aluminum foam adoption is supported by ongoing investments from aerospace and defense contractors such as Lockheed Martin, Raytheon Technologies, and Northrop Grumman, which increasingly evaluate lightweight energy-absorbing and thermal-management materials for radar systems, avionics housings, and impact-mitigation structures. In the automotive sector, OEMs, including General Motors and Ford, have expanded lightweighting initiatives across EV and hybrid platforms, indirectly supporting aluminum foam demand through Tier-1 suppliers focused on crash structures and battery protection modules.

The regional regulatory environment strongly influences supplier selection. Frameworks governed by ASTM, SAE, and U.S. Department of Defense (DoD) specifications favor manufacturers with long performance histories, traceable production processes, and validated mechanical data. As a result, investment activity increasingly centers on co-development partnerships between foam producers and OEMs, vertical integration to ensure supply reliability, and the development of modular thermal-management solutions for defense electronics and EV systems.

Europe Aluminum Foam Market Trends - Automotive Safety Engineering and Aerospace Qualification

Europe combines automotive engineering leadership, aerospace manufacturing clusters, and a steadily expanding construction retrofit market, making it a structurally balanced aluminum foam region. Germany leads automotive adoption, supported by its premium vehicle manufacturing base and strong emphasis on safety engineering and lightweight design. OEMs such as BMW Group, Volkswagen, and Mercedes-Benz Group actively pursue material substitution strategies to offset electrification-related weight increases, sustaining demand for closed-cell aluminum foams in crash management and NVH applications.

France and the U.K. drive regional growth in aerospace and defense, benefiting from established aircraft manufacturing and defense procurement programs. Companies such as Airbus, Safran, and BAE Systems are increasingly evaluating aluminum foam for use in acoustic liners, lightweight interior panels, and thermal-management components, particularly as aircraft electrification and avionics density continue to rise. Spain contributes to the specialty manufacturing and architectural materials sectors, with aluminum foam panels gaining traction in façade systems and noise-reduction installations for public infrastructure projects.

Regulatory alignment across the European Union acts as a structural growth enabler. EU emissions reduction targets, aerospace modernization initiatives, and green-building directives collectively favor lightweight, recyclable, and fire-resistant materials such as aluminum foam. At the same time, compliance with EN standards and EASA certification requirements raises entry barriers, reinforcing the market position of established suppliers with proven qualification capabilities. Strategic growth across the region is characterized by collaborative R&D programs, university-industry partnerships, and selective acquisitions aimed at expanding production capacity or application-specific expertise.

Asia Pacific Aluminum Foam Market Trends - High-Volume EV Manufacturing and Cost-Scaled Adoption

Asia Pacific is projected to account for approximately 30.7% of the market share and represents the fastest-growing regional market, driven by scale, cost competitiveness, and rapid industrialization. China dominates regional demand, supported by the world’s largest automotive production base and expanding domestic aluminum foam manufacturing capabilities. Chinese automakers and Tier-1 suppliers increasingly incorporate aluminum foam into EV battery enclosures, crash absorbers, and structural reinforcements, aligning with national policies promoting lightweighting and energy efficiency. State-supported industrial clusters further accelerate the transition from pilot production to commercial-scale deployment.

Japan leads in high-precision and functional applications, particularly in thermal-management systems, electronics cooling, and acoustic control. Japanese manufacturers leverage advanced metallurgy and process control to supply aluminum foam components for automotive electronics, industrial machinery, and aerospace subsystems, reinforcing the region’s reputation for quality and reliability. India and ASEAN countries represent emerging growth markets, driven by expanding automotive assembly, infrastructure investments, and urban construction activity. Aluminum foam adoption in these markets remains application-specific but is increasing as local manufacturers seek differentiated materials to meet evolving safety and sustainability standards.

Asia Pacific’s growth trajectory is reinforced by manufacturing scale, cost advantages, and aggressive localization strategies pursued by both regional and global players. Government-backed industrial incentives, particularly in China and India, support capacity expansion and technology transfer. Public-private partnerships accelerate pilot-to-volume transitions, positioning the region as both a major production hub and a rapidly expanding consumption market.

Competitive Landscape

The global aluminum foam market is moderately concentrated, with competition between specialized foam producers, aerospace materials suppliers, and regional construction-focused manufacturers. High-value segments such as aerospace thermal systems and certified automotive crash components show increasing consolidation, while low-value architectural panels remain fragmented.

Recent developments include expanded aerospace product portfolios, strategic partnerships with automotive Tier-1 suppliers, and selective acquisitions aimed at strengthening advanced materials capabilities. These initiatives reflect a clear shift toward OEM integration, system-level solutions, and supply-chain consolidation.

Leading companies prioritize co-development partnerships, technology licensing, vertical integration, and modular product design. Competitive differentiation increasingly depends on certification readiness, supply reliability, and validated performance data.

Key Industry Developments

- In November 2025, ERG Aerospace secured a contract to supply aluminum foam-based heat exchangers for a U.S. fighter jet program, providing superior thermal management performance while reducing overall system weight.

- In March 2025, Dingjian announced the launch of a new open-cell aluminum foam product specifically engineered for EV battery thermal management and lightweighting, aligning with rising electric vehicle material requirements.

Companies Covered in Aluminum Foam Market

- Howmet Aerospace

- ERG Aerospace Corporation

- Cymat Technologies Ltd.

- Alantum Europe GmbH

- Aluinvent Zrt.

- Alusion GmbH

- Shanxi Putai Aluminum Foam Manufacturing Co., Ltd.

- Shanghai Foamfly New Materials Technology Co., Ltd.

- Beijing Zhongjin Aluminum Foam Technology Co., Ltd.

- Liuzhou Tiyang New Building Materials Co., Ltd.

- Aluminum Foam Technologies LLC

- Versarien plc

- Mepura Metallpulver GmbH

- Havel Metal Foam GmbH

- Hollomet GmbH

- Fraunhofer IFAM

- Pohltec Metalfoam GmbH

- ERG Duocel

Frequently Asked Questions

The global aluminum foam market is valued at approximately US$2.4 billion in 2026.

By 2033, the aluminum foam market is expected to reach US$4.2 billion.

Key trends include growing demand for lightweight crash-absorbing materials in electric vehicles, increased use of open-cell aluminum foams in heat exchangers and filtration systems, rising adoption in aerospace and defense thermal-management applications, and ongoing localization of manufacturing capacity in Asia Pacific to reduce costs and improve supply-chain resilience.

The closed-cell aluminum foam segment is the leading structural category, accounting for approximately 60.4% of the total market share, due to its superior mechanical strength, predictable deformation behavior, and widespread use in automotive crash management and safety-critical applications.

The aluminum foam market is projected to grow at a CAGR of 8.4% between 2026 and 2033.

Major companies include Cymat Technologies Ltd., ERG Aerospace Corporation, Alantum Europe GmbH, Shanxi Putai Aluminum Foam Manufacturing Co., Ltd., and Mepura Metallpulver GmbH.