- Bulk Chemicals

- Aluminum Sulfate Market

Aluminum Sulfate Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Aluminum Sulfate Market by Product Type (Ferric, Non-ferric), Grade (Food, Pharmaceutical, Industrial), Application (Water Treatment, Paper & Pulp, Food & Beverages, Textile, Personal Care, Other), Regional Analysis for 2025 - 2032

Aluminum Sulfate Market Size and Trend Analysis

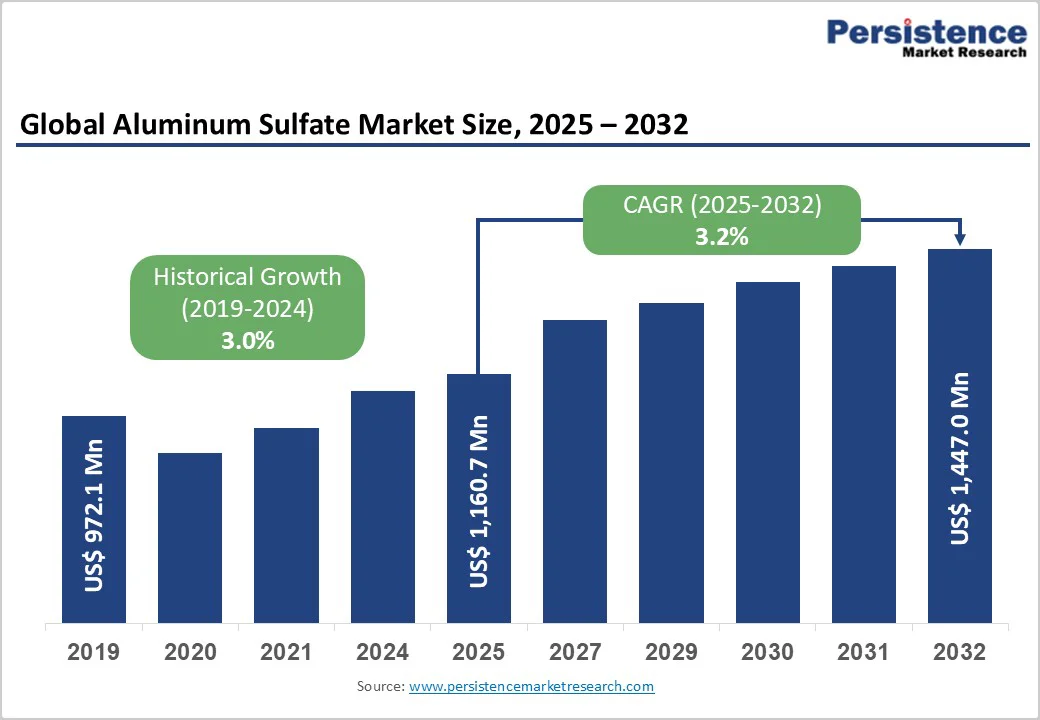

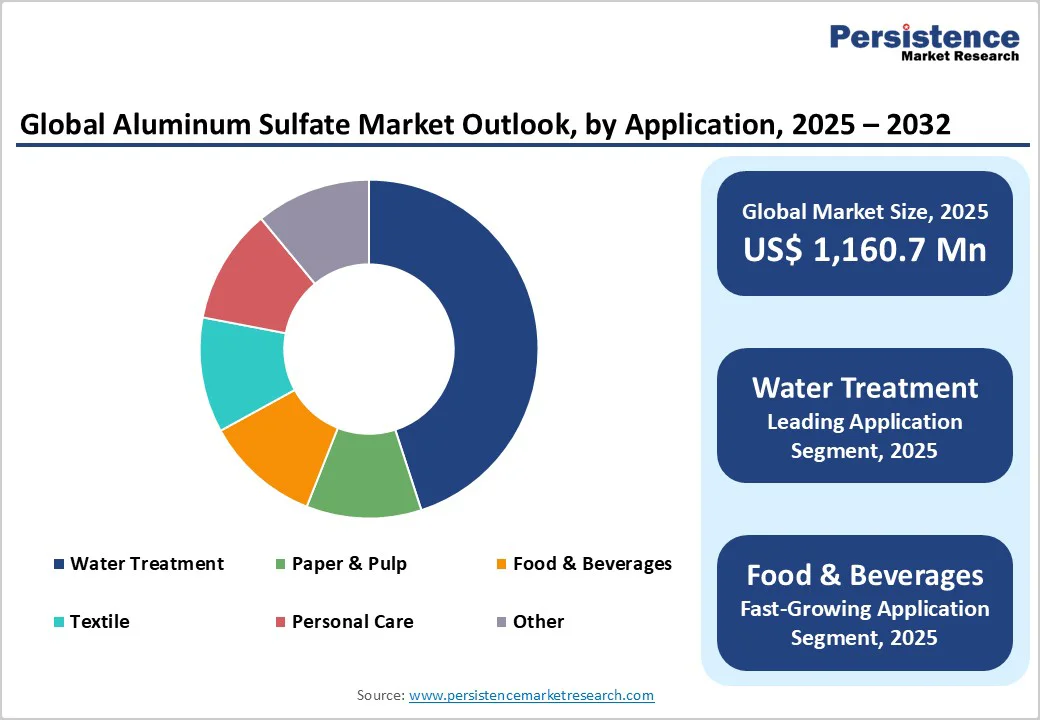

The global aluminum sulfate market size is supposed to be valued at US$1,160.7 million in 2025 and is projected to reach US$1,447.0 million by 2032, growing at a CAGR of 3.2% between 2025 and 2032.

Rise in global water scarcity issues and stringent environmental regulations mandating advanced purification processes. Urbanization and industrial expansion have intensified the need for effective coagulants such as aluminum sulfate, particularly in municipal and industrial water treatment facilities worldwide.

Supporting this, the United Nations reports that over 2 billion people lack access to safely managed drinking water services, fueling demand for reliable treatment chemicals.

Key Industry Highlights:

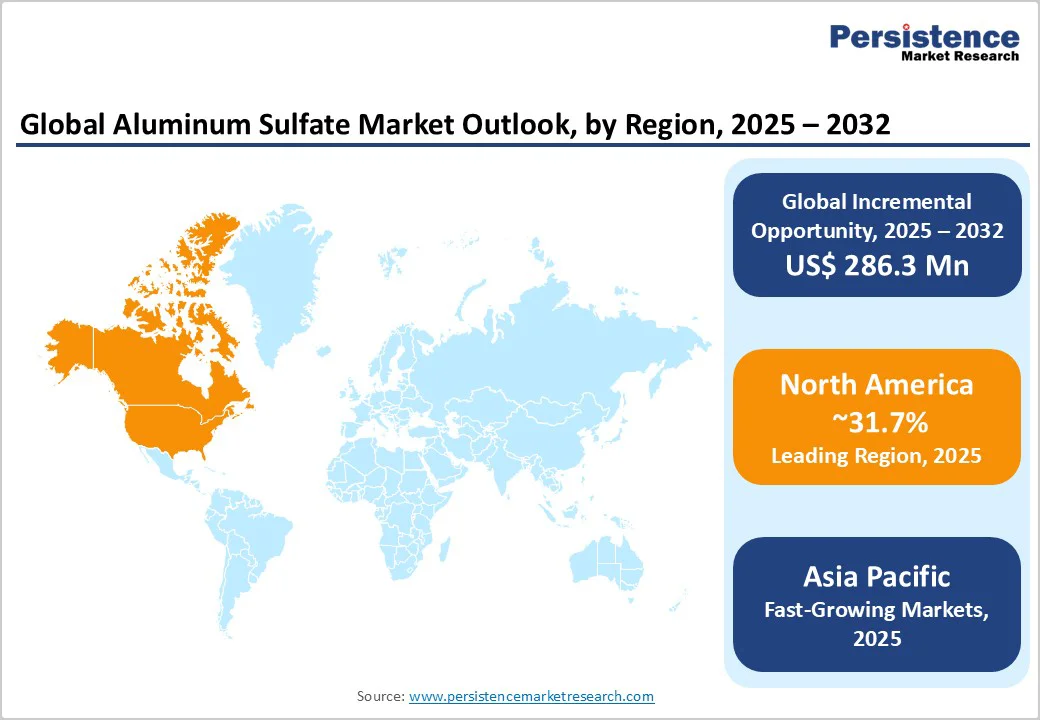

- Regional Leader: North America leads the aluminum sulfate market, with 31.7% of the market share, due to robust EPA-driven water treatment infrastructure and industrial adoption, ensuring steady demand for coagulants in purification processes.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, propelled by urbanization in China and India, where manufacturing expansions heighten the need for affordable water and pulp applications.

- Leading Segment: Water Treatment dominates as the leading application segment, capturing 45% share through essential coagulation roles in global utilities and compliance with water quality standards.

- Fastest Growing Segment: Industrial grade represents the fastest-growing segment, fueled by cost efficiencies in heavy industries like textiles and chemicals amid rising production volumes.

- Growth Opportunities: Key market opportunity lies in sustainable technologies for emerging economies, integrating aluminum sulfate with green water initiatives to meet UN clean water goals.

| Key Insights | Details |

|---|---|

| Aluminum Sulfate Market Size (2025E) | US$ 1,160.7 Mn |

| Market Value Forecast (2032F) | US$ 1,447.0 Mn |

| Projected Growth CAGR (2025 - 2032) | 3.2% |

| Historical Market Growth (2019 - 2024) | 3.0% |

Market Dynamics

Driver - Increasing Demand from the Water Treatment Sector

The surge in global water treatment requirements is a major growth driver for the aluminum sulfate market, as it serves as an essential coagulant for removing impurities and suspended solids in both potable and wastewater processes.

With rapid urbanization and industrialization, particularly in developing regions, the demand for clean water has escalated, prompting governments to invest heavily in infrastructure. For instance, the World Health Organization estimates that waterborne diseases affect over 485,000 people daily, underscoring the urgency for effective treatments.

Aluminum sulfate's cost-effectiveness and efficiency in floc formation make it indispensable, enhancing sedimentation and filtration outcomes. This driver is projected to sustain market momentum, supported by ongoing expansions in the Water & Wastewater Treatment Chemicals Market, where coagulants like aluminum sulfate play a pivotal role in compliance with international standards such as those from the EPA.

Expansion in Paper and Pulp Industry Applications

The robust growth of the paper and pulp industry globally is propelling the aluminum sulfate market, as it is widely used for pitch control, sizing, and retention aids during manufacturing processes. Rising demand for paper products, driven by e-commerce packaging and printing needs, has led to increased production capacities, especially in Asia.

According to the International Council of Forest and Paper Associations, global paper production reached 420 million tons in 2023, a 2% year-over-year increase, highlighting the sector's vitality.

Aluminum sulfate improves paper quality by neutralizing charges and enhancing fiber bonding, reducing waste and improving efficiency. This application not only boosts market volumes but also aligns with sustainable practices in pulp processing, where it aids in reducing chemical usage overall, fostering long-term industry growth.

Restraint - Environmental and Health Regulatory Concerns

A key restraint in the aluminum sulfate market is the growing environmental and health concerns associated with its residual aluminum content in treated water, leading to stricter regulations on usage and disposal. Aluminum sulfate can contribute to elevated aluminum levels in ecosystems, potentially affecting aquatic life and human health through bioaccumulation.

The European Environment Agency notes that aluminum discharges from treatment plants have raised water quality issues in several rivers, prompting tighter effluent limits. These regulations increase compliance costs for manufacturers and end-users, potentially shifting demand toward alternative coagulants like polymers.

Public awareness campaigns have further amplified scrutiny, with studies from the WHO linking chronic aluminum exposure to neurological risks, thus dampening adoption rates in sensitive applications like food processing.

Volatility in Raw Material Prices

Fluctuations in aluminum and sulfuric acid prices pose a major barrier to the aluminum sulfate market. Bauxite, the primary source, saw prices rise 15% in 2024 due to supply chain disruptions from mining regulations in Australia and Guinea, as reported by the International Aluminium Institute.

This volatility increases production costs by up to 25%, squeezing margins for manufacturers. Additionally, sulfuric acid dependency on petroleum byproducts ties it to oil price swings, with OPEC data showing 10-20% annual variations, making budgeting challenging and deterring small-scale producers.

Opportunity - Opportunities in Emerging Sustainable Technologies

Market participants have substantial opportunities in developing eco-friendly aluminum sulfate variants and advanced application technologies, particularly for sustainable water treatment in fast-growing regions like the Asia Pacific. Innovations such as low-residue formulations and integrated dosing systems can address environmental concerns while meeting rising demand from urbanization.

The United Nations Sustainable Development Goals emphasize clean water access, with investments in green infrastructure projected to reach $1.7 trillion annually by 2030. Companies can capitalize by partnering with governments on pilot projects, as seen in recent ASEAN initiatives for wastewater management.

This segment's potential is enhanced by synergies with the Flocculants and Coagulants Market, where aluminum sulfate-based hybrids offer superior performance in phosphorus removal, driving adoption in agricultural runoff treatment.

Expansion into Pharmaceutical and Personal Care Segments

Another promising opportunity lies in the burgeoning pharmaceutical and personal care industries, where high-purity aluminum sulfate grades are increasingly used for formulation stability and as astringents in cosmetics.

With global personal care spending expected to grow at 5.3% CAGR through 2030, demand for non-toxic, regulated variants is surging. Policy shifts, such as the FDA's emphasis on sustainable sourcing, create avenues for certified suppliers to gain market share.

Recent developments in bio-based production methods further reduce environmental footprints, appealing to eco-conscious brands. This end-user focus promises significant revenue pockets, especially as regulatory approvals facilitate entry into high-margin applications like vaccine adjuvants and skincare products.

Category-wise Insights

Product Type Analysis

The non-ferric segment leads the product type category in the aluminum sulfate market, holding approximately 55% market share due to its superior purity and versatility in sensitive applications. Non-ferric aluminum sulfate, free from iron impurities, is preferred in water treatment and food processing to avoid discoloration and contamination risks.

According to EPA guidelines, non-ferric variants ensure compliance with potable water standards, where iron-free coagulants prevent residual staining in distribution systems.

This dominance is supported by industry data indicating higher adoption rates in municipal facilities, with over 70% of U.S. water treatment plants opting for non-ferric grades for optimal clarity and safety. Its chemical stability also enhances efficacy in pH-sensitive environments, solidifying its position as the preferred choice for high-volume users.

Grade Analysis

The industrial grade dominates the grade category in the aluminum sulfate market, commanding about 65% share owing to its cost-effectiveness and broad applicability in heavy-duty processes. Industrial-grade aluminum sulfate is optimized for large-scale uses like wastewater treatment and pulp processing, where high reactivity and bulk availability are crucial.

Data from the American Water Works Association highlights that industrial variants meet AWWA B403 standards for coagulation efficiency, supporting their widespread use in utilities handling millions of gallons daily. This leadership stems from economical production scales and minimal purity requirements compared to specialized grades, enabling seamless integration into manufacturing lines while maintaining performance in turbidity removal and sludge dewatering.

Application Analysis

The water treatment segment leads the application category in the aluminum sulfate market, with roughly 45% market share attributed to its critical role in coagulation and flocculation for impurity removal. As a primary coagulant, aluminum sulfate effectively binds suspended particles, facilitating sedimentation in both municipal and industrial settings.

EPA estimates indicate that 45% of domestic aluminum sulfate consumption is dedicated to water and wastewater treatment, driven by regulatory mandates for pathogen reduction and clarity. This segment's prominence is reinforced by global water quality initiatives, where aluminum sulfate's proven track record in handling diverse contaminants like organics and metals ensures sustained demand across utilities.

Regional Insights

North America Aluminum Sulfate Trends

North America maintains leadership in the aluminum sulfate market, propelled by advanced water infrastructure and rigorous EPA regulations enforcing coagulant use in public supplies. The U.S. dominates regionally, with over 80% of consumption tied to municipal treatment plants addressing aging systems and population growth.

Innovations in optimized dosing technologies further enhance efficiency, reducing chemical footprints while meeting Safe Drinking Water Act standards. Recent developments, such as USALCO's expansions in high-purity production, underscore the region's focus on sustainable solutions amid increasing industrial wastewater volumes.

Europe Aluminum Sulfate Trends

Europe exhibits strong performance in the aluminum sulfate market, harmonized under the EU Water Framework Directive that mandates stringent effluent controls, boosting coagulant adoption across Germany, the U.K., France, and Spain. These nations lead in integrated water management, with Germany's advanced facilities utilizing aluminum sulfate for phosphorus removal in over 60% of plants.

Regulatory alignment promotes cross-border standards, fostering innovation in low-dose formulations. Recent policy updates emphasize circular economy principles, encouraging recycling of treatment byproducts and enhancing market resilience.

Asia Pacific Aluminum Sulfate Trends

Asia Pacific exhibits dynamic growth in the aluminum sulfate market, led by manufacturing advantages in China, Japan, India, and ASEAN countries, where cost efficiencies and abundant bauxite resources enable large-scale production for water treatment and industrial applications.

India generates approximately 72 billion liters of sewage daily, but treats only 28%, creating substantial demand for coagulants such as aluminum sulfate. India's wastewater treatment market is driven by government initiatives, including the Namami Gange Programme, which has sanctioned 203 sewerage infrastructure projects targeting 6,255 million liters per day sewage treatment capacity in the Ganga Basin.

The World Bank Water Security Financing Report 2024 highlights US$ 19.6 billion in multilateral development bank investments for global water infrastructure in 2024, with approximately 14.4 billion directed to low- and middle-income countries in the Asia Pacific catalyzing significant aluminum sulfate demand for coagulation and treatment applications.

Competitive Landscape

The global aluminum sulfate market features a moderately consolidated structure, through integrated supply chains and regional dominance, while fragmented, smaller players serve niche local demands. Key strategies include capacity expansions and R&D investments in sustainable variants, as seen in recent acquisitions enhancing production footprints.

Market leaders differentiate via certifications such as NSF/ANSI 60 for purity, ensuring compliance in water applications. Emerging trends involve digital monitoring for dosing optimization and partnerships for bio-based alternatives, aiming to mitigate environmental critiques while capturing growth in emerging economies.

Key Market Developments

- January 2025: Chemtrade acquired aluminum sulfate water treatment businesses in Florida, New York, and California for USD $30.0 million, bolstering its North American production capacity.

- July 2025: Kemira announced investments in its Tarragona site to expand drinking water treatment portfolio with a new ACH production line, focusing on higher efficiency and reduced emissions.

- March 2024: USALCO enhanced its acidified aluminum sulfate offerings, improving sludge reduction in wastewater applications through advanced manufacturing upgrades.

Top Companies in the Aluminum Sulfate Market

- Chemtrade (Canada) stands as a North American powerhouse, producing over 40% of regional aluminum sulfate via multiple facilities, emphasizing water treatment solutions. Its 2025 acquisitions have strengthened supply chains, generating robust revenues from coagulant sales while prioritizing sustainability certifications.

- USALCO (United States) excels in high-purity and acidified grades, serving municipal and industrial clients with NSF-approved products. Renowned for innovation in low-sludge formulations, it maintains a strong portfolio in phosphorus removal, driving growth through U.S.-focused expansions.

- Kemira (Finland) leads in Europe with diversified inorganic coagulants, investing in eco-friendly production like the 2025 Tarragona project. Its global reach and R&D emphasis on sustainable water tech position it as a key player in regulatory-compliant markets.

Companies Covered in Aluminum Sulfate Market

- Chemtrade

- GEO Specialty Chemicals

- Nippon Light Metal

- C&S Chemical

- USALCO

- Feralco AB

- Affinity Chemicals

- Kemira

- Henan Fengbai Industries Co., Ltd.

- Nankai Chemical Co., Ltd.

- GAC Chemical Corporation

Frequently Asked Questions

The global aluminum sulfate market is valued at US$ 1,160.7 Mn in 2025 and expected to reach US$ 1,447.0 Mn by 2032, reflecting steady expansion driven by water treatment demands.

Key drivers include rising water treatment needs due to urbanization and regulations, alongside growth in the paper and pulp sector for sizing applications, boosting global consumption.

Water treatment leads the application category with 45% share, essential for coagulation in municipal and industrial purification processes worldwide.

North America leads due to advanced EPA regulations and extensive water infrastructure, commanding significant share through high adoption in utilities.

Opportunities arise in sustainable water technologies for emerging markets, aligning with UN goals for clean water access and green coagulant innovations.

Prominent players include Chemtrade, USALCO, and Kemira, focusing on expansions and high-purity products for water and industrial applications.