- Technology

- AI Agents Market

AI Agents Market Size, Share, and Growth Forecast, 2025 - 2032

AI Agents Market By Agent System (Single-agent Systems, Multi-agent Systems), Technology (Machine Learning, Computer Vision, Natural Language Processing, Others), Application, End-user Industry, and Regional Analysis for 2025 - 2032

AI Agents Market Size and Trends Analysis

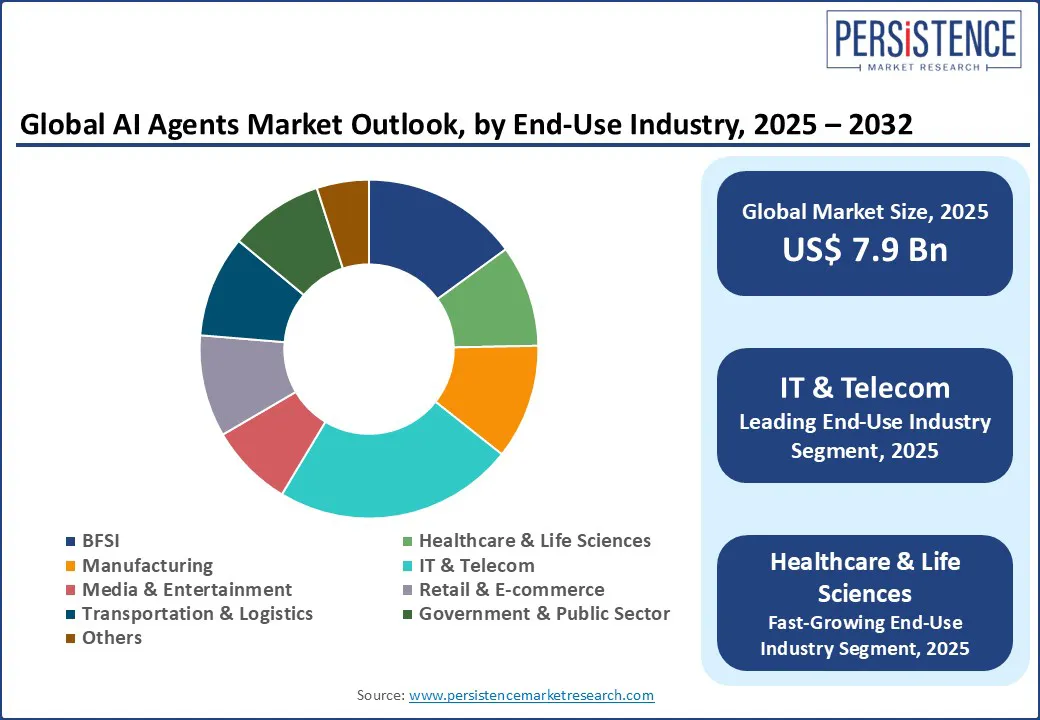

The global AI Agents Market size is projected to rise from US$ 7.9 Bn in 2025 to US$ 98.2 Bn by 2032. It is anticipated to witness a CAGR of 43.7% during the forecast period from 2025 to 2032. AI agents are autonomous or semi-autonomous software systems that leverage various technologies to perform tasks, make decisions, and interact with users or environments. These agents are increasingly adopted across industries to automate repetitive processes, enhance customer experience, reduce operational costs, and improve decision-making, making them crucial in both enterprise and consumer-facing applications.

Key Industry Highlights:

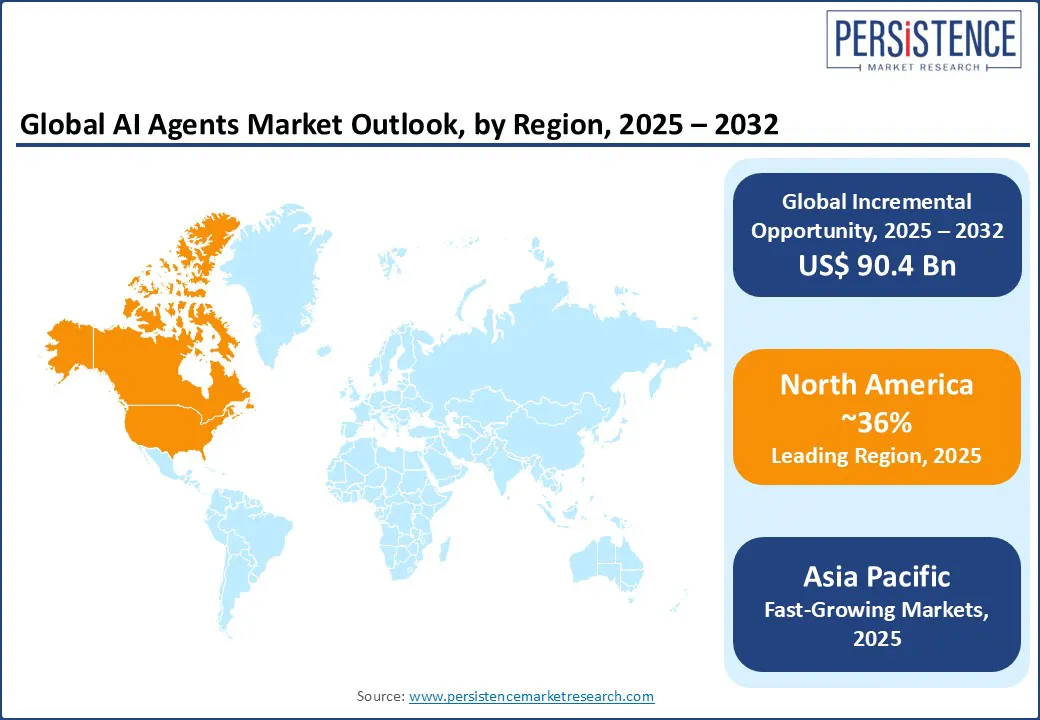

- North America is estimated to hold more than 36% share in 2025, driven by tech infrastructure, high AI adoption across industries, and supportive government initiatives.

- Machine learning is expected to account for more than 34% share in 2025 due to its pivotal role in enabling AI agents to learn, adapt, and make data-driven decisions autonomously.

- IT & telecom is expected to account for more than 23% share in 2025 due to rapid digital transformation, rising automation needs, and 5G-driven real-time analytics.

- Asia Pacific will achieve the highest rate due to rapid digital transformation, government AI initiatives, and expanding tech infrastructure across emerging economies.

- The combination of edge devices and cloud infrastructure empowers real-time decision-making and remote AI agent deployment.

- The explosion of structured and unstructured data fuels AI agents to learn, adapt, and optimize actions across domains.

- Advanced NLP enables AI agents to serve diverse population by understanding and interacting in multiple languages.

| Global Market Attribute | Key Insights |

| AI Agents Market Size (2025E) | US$ 7.9 Bn |

| Market Value Forecast (2032F) | US$ 98.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 43.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 29.5% |

Market Dynamics

Driver - Automation Driving Operational Efficiency and Customer Engagement

AI agents are revolutionizing internal operations by automating routine and rule-based tasks such as invoice processing, scheduling, workflow management, and compliance checks. This enables human employees to focus on strategic and creative responsibilities, especially in sectors such as banking, healthcare, and manufacturing, where efficiency and accuracy are crucial. In the U.S., the Department of Commerce reported in 2024 that AI-driven automation improved operational efficiency in federal agencies by upto 50% in administrative tasks.

Governments are adopting AI agents to streamline administrative services. For example, the UK central government handles 143 million citizen-facing transactions annually, 84% of which are highly automated, potentially saving 1,200 man years (amount of work performed by a person in one year) by automating just one minute per transaction. By mid-2025, more than 75% of global enterprises use AI in at least one function, with ~70% deploying generative AI, such as chatbots. These agents, integrated into platforms like telecom and banking apps, manage queries, resolve issues, and offer personalized upselling, enhancing customer engagement across multiple channels.

Restraint - Compliance Burdens and Bias Risks

Ethical AI development requires transparency, fairness, and accountability principles that are challenging to uphold in autonomous systems. Many AI agents, especially those based on deep learning, operate as black boxes, making it hard to justify decisions such as loan rejections or healthcare service changes. In 2024, the U.S. Department of Commerce issued updated guidelines stressing audits for disparate impact across gender, race, and disability, prompting companies to invest more in fairness testing, raising costs and delaying market entry. The lack of standardized global frameworks further restricts cross-border deployment.

Regulatory complexity also hinders growth, especially as AI agents gain autonomy. The EU AI Act (2024) mandates strict controls on high-risk applications, requiring documentation, logging, and human oversight, which may overwhelm smaller firms. In the U.S., 693 AI-related bills were introduced in 2024, with 31 approved, adding to the fragmented compliance landscape. Independent decision-making also creates accountability gaps, prompting regulators to enforce HITL (human-in-the-loop) systems, enhancing safety but reducing efficiency. According to a study, in healthcare, biased AI systems caused a 30% higher mortality rate for non-Hispanic Black patients as of May 2024, underlining the grave consequences of unchecked bias.

Opportunity - Voice-Enabled and Edge AI Agents

Voice-enabled agents, powered by advancements in speech recognition and natural language understanding are increasingly embedded in smartphones, smart speakers, vehicles, and appliances. Their hands-free operation and intuitive interfaces enhance user experience and drive adoption across consumer and enterprise sectors. Public services are also embracing voice bots to improve accessibility, particularly for digitally low-literate population. This demand is pushing companies to build AI agents that understand diverse languages, accents, and contexts. As per a study, 30% of healthcare organizations now use voice-enabled EMRs, boosting productivity by 40% and raising patient satisfaction by 60%.

Edge AI enhances this shift by enabling real-time processing on local devices, reducing latency, and improving data privacy. In smart factories, AI agents on edge-enabled sensors and robots respond to voice commands, detect anomalies, and assist in complex tasks, even ensuring safety during cloud outages. For instance, Missouri’s public services handled 32,000 monthly inquiries with voice agents, cutting wait times by 70%.

AI Agents Market Key Trends

Rise of LegalTech and RegTech with Multi-Step Reasoning

LegalTech leverages AI to streamline tasks such as contract analysis, legal research, and case management, while RegTech uses AI to ensure compliance with regulatory frameworks in finance, healthcare, and data privacy. In 2024, the U.S. federal government introduced 59 AI-related regulations, more than double the number in 2023, signaling increased regulatory focus. GenAI models, which power modern AI agents, are now embedded in workflows requiring multi-step reasoning, such as legal document review and financial compliance.

The 2025 LegalOn contract survey showed a 75% year-over-year increase in AI use for contract review from 8% in early 2024 to 14% in 2025, with nearly two-thirds of firms actively evaluating AI solutions. Organizational adoption of GenAI doubled globally, with 26% of legal firms actively using it and 95% of professionals expecting it to become central within five years. Autonomous agents with multi-step reasoning are also transforming business process automation into areas such as procurement and finance by enabling end-to-end workflows with minimal human intervention.

Category-wise Analysis

By Technology, Machine Learning Dominates the Market Share, Fueled by Real-Time Decision-Making and Predictive Capabilities

Based on technology, the market is divided into machine learning, computer vision, natural language processing & others. Machine learning is projected to hold the largest share of over 34% in 2025 due to its critical role in enabling autonomous decision-making, predictive analytics, and adaptive behavior in real-time environments. Advancements in supervised and reinforcement learning are also enhancing AI agents' capabilities. The availability of large datasets and improved computational power is fueling widespread adoption.

Natural language processing (NLP) is expected to grow at the highest rate due to rising demand for human-like interactions in customer service, virtual assistants, and chatbots. Businesses across sectors are adopting NLP to automate communication, extract insights from unstructured data, and enhance multilingual support. Advancements in large language models (LLMs) and generative AI are further accelerating NLP integration.

By End-user Industry, IT & Telecom Drive Adoption with Rapid Digitalization and 5G Expansion

By end-user, the segmentation includes BFSI, healthcare & life sciences, manufacturing, IT & telecom, media & entertainment, retail & e-commerce, transportation & logistics, government & public sector, and others. Out of these, IT & telecom are expected to account for more than 23% share in 2025. This dominance is driven by rapid digital transformation and increasing demand for intelligent automation. They are widely adopted to enhance customer service through chatbots, automate network management, and improve cybersecurity. The rollout of 5G and edge computing is further accelerating the deployment of AI-driven tools for real-time analytics and predictive maintenance. Telecom operators are integrating AI agents to optimize bandwidth usage and personalize user experiences.

The healthcare & life sciences industry is projected to grow at a significant rate due to increasing demand for intelligent diagnostics, virtual health assistants, and personalized medicine. AI agents are streamlining clinical workflows, automating administrative tasks, and improving patient engagement. The growing volume of medical data and the need for real-time decision support are accelerating adoption.

Regional Insights

North America AI Agents Market Trends

North America is expected to account for a share of more than 36% in 2025. The increasing reliance on cloud computing, edge devices, and enterprise software has made AI agents vital for streamlining operations across finance, healthcare, retail, and logistics. In the U.S. AI Agents Market, a key demand driver is federal support, as outlined in the updated 2023 National AI R&D Strategic Plan, emphasizing trustworthy AI, workforce readiness, and public-sector innovation. Federal agencies are actively deploying to automate tasks such as administrative form processing and customer service, with initiatives targeting automation of over 300 standardized roles.

Defense applications are also propelling demand, with the Department of Defense backing programs such as Thunderforge involving companies such as Scale AI, Anduril, and Microsoft. Federal AI contracts rose from $355 million in 2022 to $4.6 billion in 2023, a 1,200% surge largely driven by military and public-sector deployments. In Canada, the renewed Pan-Canadian AI Strategy supports institutions such as Vector Institute and Mila, while Responsible AI Agent adoption is expanding in government services such as immigration and pension systems. Industries are leveraging AI agents to counter labor shortages in agriculture, mining, and manufacturing.

Asia Pacific AI Agents Market Trends

In China, the adoption of AI agents is driven by strong state backing through flagship policies like the New Generation AI Development Plan, alongside local subsidies and pilot zones. As of H1 2024, there were 81 public tenders for LLM-based projects, up from just one in H1 2023, spanning sectors such as energy, telecom, and finance. DeepSeek’s R2 model, launched in early 2025, is now deployed across 13 city governments and 10 state-owned enterprises.

In Japan, where over 29% of the population is aged 65 or older (2024), AI agents support eldercare and healthcare operations. Toyota and NTT’s Mobility AI Platform, with a ¥500 billion joint investment aimed at achieving a zero-traffic-accident society, will begin development in 2025 and aims for full adoption by 2030. South Korea focuses on embedding AI agents in smart cities and home devices, while India’s INR10,372 crore IndiaAI Mission (2024-29) supports local agentic innovation, such as Ola’s Kruti, launched in June 2025, with multi-language capabilities and enabling tasks such as cab bookings, payments, and scheduling.

Europe AI Agents Market Trends

Germany’s demand is driven by its robust Industry 4.0 ecosystem, where AI-powered automation, digital twins, and predictive maintenance are becoming standard. In 2024, 19.8% of German firms already used AI, up from 11.6% in 2023, with another 17.5% planning adoption. France is leveraging AI extensively in manufacturing and aerospace, with 45% of firms using AI in 2024; Renault alone has integrated AI into 68% of its European production lines. The French government has also launched initiatives in 2024 promoting responsible AI use in healthcare and legal tech, boosting demand in diagnostics, workflow automation, and compliance.

The United Kingdom is advancing AI adoption through its National AI Strategy, post-Brexit, with regulatory sandboxes and public-private partnerships playing key roles. In 2024, HM Treasury reported that over 70% of London fintech firms were testing AI agents for fraud detection, customer support, and algorithmic trading. The UK’s leadership in AI ethics research further supports wider deployment across sectors. In the Benelux region, adoption is strong across both public and private sectors, with the Netherlands standing out; in 2025, the Dutch Ministry of Infrastructure and Water Management reported a 30% rise in autonomous freight pilots powered by AI.

Competitive Landscape

The global AI Agents market is moderately fragmented, with a mix of established tech giants and emerging AI-focused startups actively competing. Companies are focusing on developing highly specialized or industry-specific AI agents. Players are integrating multi-modal capabilities and advanced generative AI to enhance agent intelligence, user engagement, and decision-making capabilities.

Key Industry Developments

- In July 2025, Airship launched AI Agents to automate and optimize customer experiences across mobile apps and websites. These intelligent, task-specific agents handle everything from personalized messaging and user onboarding to real-time experimentation and actionable recommendations, enabling continuous, goal-driven improvements without code.

- In June 2025, IQVIA unveiled custom-built AI agents powered by NVIDIA technology at GTC Paris, aimed at enhancing workflows and accelerating insights in life sciences. These agentic solutions showcase how IQVIA is leveraging AI and domain expertise to transform business processes and improve patient outcomes.

- In May 2025, Siemens is expanding its industrial AI portfolio by introducing advanced autonomous AI agents within its Industrial Copilot ecosystem. These agents can proactively execute complex industrial tasks through a coordinated orchestrator, boosting productivity by up to 50% while allowing users full control over task delegation.

- In May 2025, NTT DATA launched its enterprise-grade Smart AI Agent Ecosystem, offering industry-specific solutions to accelerate digital transformation. The company also introduced a patented plug-in that converts legacy bots into autonomous agents and expanded its alliance network to deliver tailored solutions.

Companies Covered in AI Agents Market

- Microsoft

- IBM

- AWS

- OpenAI

- Amelia

- NVIDIA

- Leena AI

- Salesforce, Inc.

- Adept AI

- Oracle

- Kinaxis

Frequently Asked Questions

The global AI agents market is projected to be valued at US$7.9 Bn in 2025.

Rising demand for automation and the increasing adoption of AI agents for personalized, real-time decision-making and operational efficiency are key market drivers.

The AI agents market is poised to witness a CAGR of 43.7% from 2025 to 2032.

The increasing adoption of intelligent virtual assistants, combined with growing integration with IoT and edge computing for real-time decision-making, presents significant market opportunities.

Google, Microsoft, IBM, AWS, OpenAI, Amelia, and NVIDIA are among the leading key players.