- Aerospace & Defense

- Aerospace Accumulator Market

Aerospace Accumulator Market Size, Share, and Growth Forecast, 2026 – 2033

Aerospace Accumulator Market by Product Type (Piston, Bladder, Diaphragm), Aircraft Type (Narrow-body, Wide-body, Others), Material (Steel, Composites, Others), Application (Landing Gear, Braking Systems, Flight Controls), and Regional Analysis 2026 – 2033

Aerospace Accumulator Market Size and Trends Analysis

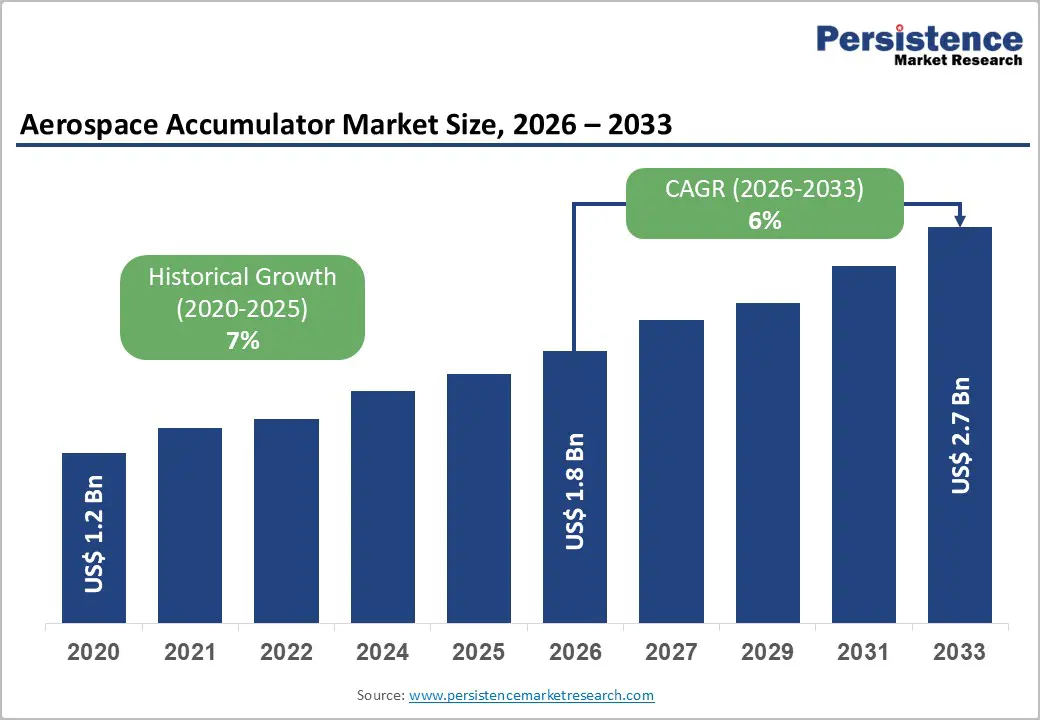

The global aerospace accumulator market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by the resurgence in global commercial aircraft deliveries, particularly for narrow-body platforms, and the increasing adoption of More Electric Aircraft (MEA) technologies which necessitate advanced, high-pressure hydraulic solutions.

Furthermore, the intensified focus on lightweighting strategies to enhance fuel efficiency is driving a structural shift from traditional steel to composite-based accumulator designs.

Key Industry Highlights:

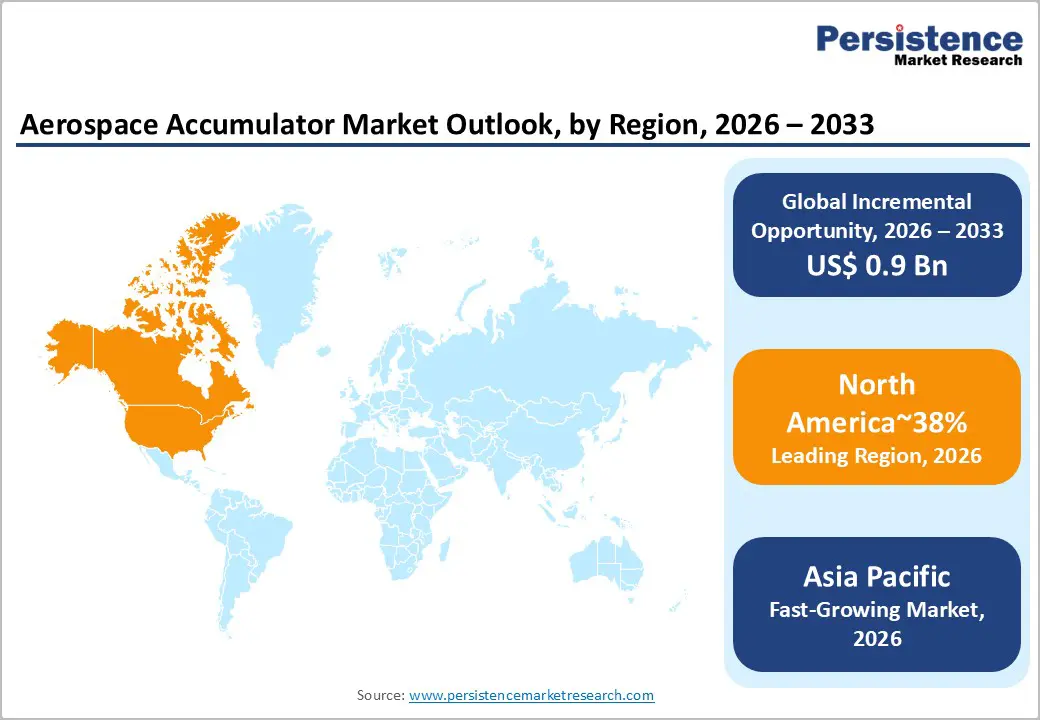

- Leading Region: North America is expected to lead with around 38% share, anchored by the concentration of aircraft OEMs, tier-1 suppliers, and MRO infrastructure.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing, driven by accelerating aircraft deliveries, fleet expansion by regional carriers, and rising indigenous aerospace manufacturing programs.

- Leading Material: Steel is expected to lead with roughly 52% share, supported by its high fatigue strength, pressure tolerance, and certification maturity in aerospace hydraulic systems.

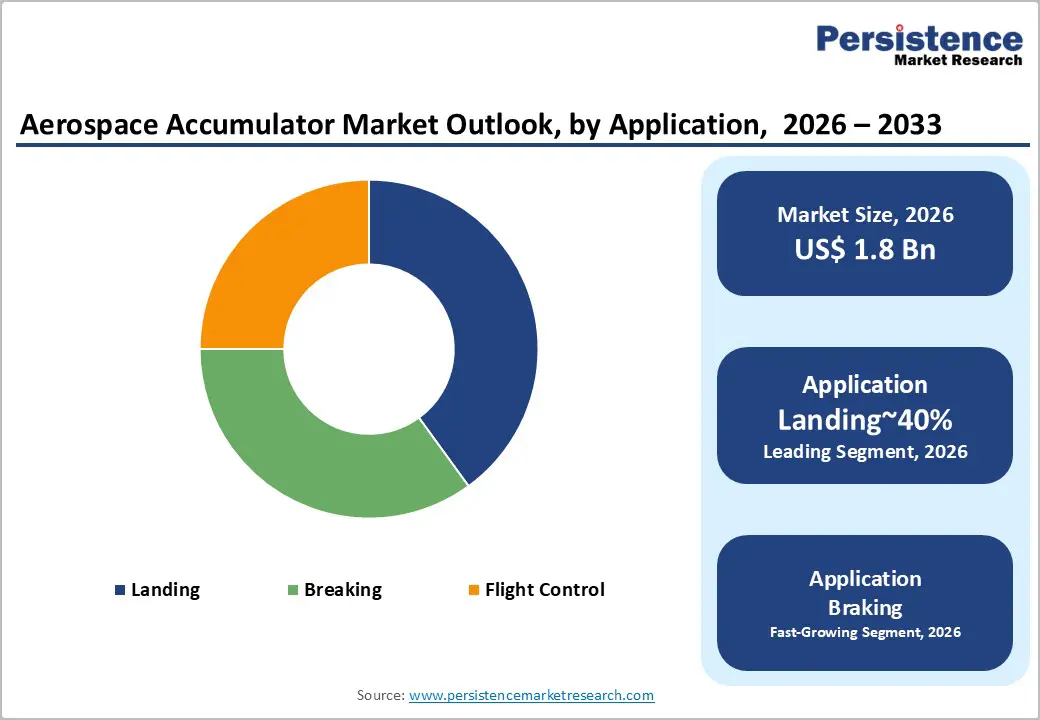

- Leading Application: Landing gear systems are expected to lead with about 40% share, reflecting the critical role of accumulators in shock absorption, emergency extension, and load stabilization.

| Key Insights | Details |

|---|---|

| Aerospace Accumulator Market Size (2026E) | US$1.8 Bn |

| Market Value Forecast (2033F) | US$2.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Adoption of Electro-Hydrostatic Actuators within More Electric Aircraft Architectures

The transition toward More Electric Aircraft is reconfiguring hydraulic system design by decentralizing actuation architectures around electro-hydrostatic actuators rather than centralized hydraulic networks. EHAs concentrate power conversion and fluid control at the point of use, increasing reliance on compact, high-response accumulators to buffer pressure transients, stabilize local energy demand, and support fault-tolerant operation. This architectural shift embeds accumulators within distributed actuation nodes across flight control, braking, and secondary systems, structurally increasing unit intensity per airframe. As aircraft platforms pursue electrical load optimization and hydraulic line reduction, accumulator integration becomes a core enabler of localized hydraulic stability within electrified actuation frameworks.

At the value-chain level, decentralized hydraulics elevate technical requirements for accumulator miniaturization, thermal tolerance, and dynamic response under high-frequency duty cycles. Certification regimes for electrically driven actuation impose stringent reliability and redundancy thresholds, increasing validation burdens for pressure storage components integrated within safety-critical control loops. The pivot toward electrified architectures reallocates development effort toward materials, sealing technologies, and compact form factors compatible with distributed installation constraints. These dynamics structurally expand addressable demand for specialized aerospace accumulators aligned with MEA-driven system architectures across advanced fixed-wing platforms.

Rising Global Aircraft Production and Fleet Renewal

Rising global aircraft production is a primary structural driver for demand across hydraulic subsystems, including accumulators integrated into landing gear, braking, flight-control actuation, and emergency power circuits. The commercial aviation sector continues to expand capacity to support sustained growth in passenger traffic, driving steady OEM build rates for narrow-body and wide-body platforms and accelerating replacement of aging fleets. As airlines prioritize fuel efficiency, dispatch reliability, and lower maintenance burden, newer aircraft architectures embed higher-performance hydraulic architectures that rely on robust, high-pressure accumulator systems to stabilize pressure, dampen pulsations, and provide redundancy for safety-critical functions.

This production upcycle translates directly into higher accumulator content per aircraft through broader system integration, tighter safety certification standards, and increasing system complexity in next-generation platforms. Program-level ramp-ups across high-volume single-aisle families create predictable, multi-year offtake visibility for qualified accumulator suppliers, reinforcing long-cycle OEM supply agreements and platform lock-in effects. In parallel, easing regulatory bottlenecks and normalized certification throughput improve line-rate stability, reducing delivery volatility for tier suppliers. Collectively, these dynamics elevate accumulators from commoditized hydraulic components to safety-critical, specification-driven subsystems with recurring demand across new-build aircraft and long-tail aftermarket support.

Barrier Analysis – Weight Penalties and Design Constraints in Hydraulic Accumulators

Structural weight sensitivity within aerospace platforms is intensifying as fuel efficiency, emissions compliance, and range optimization become central design constraints across new aircraft programs. Hydraulic accumulators, particularly piston-based configurations, introduce mass penalties that directly counter system-level weight reduction targets embedded within airframe and propulsion integration strategies. As aircraft architectures migrate toward electrified subsystems, traditional fluid-power components face increasing scrutiny within trade-off analyses that prioritize lightweight electrical alternatives for actuation and energy buffering. This design tension constrains the design envelope available for accumulator integration, especially within tightly packaged control surfaces and distributed actuation nodes.

At the value-chain level, weight-driven design constraints reallocate development priorities toward advanced materials, compact form factors, and multifunctional components capable of offsetting mass penalties through performance consolidation. Certification and safety requirements limit the extent of lightweighting achievable through material substitution, increasing engineering cost and elongating qualification cycles for redesigned accumulator architectures. As OEMs pursue aggressive mass budgets, procurement preferences increasingly favor electrically driven solutions where feasible, structurally narrowing the addressable market for conventional hydraulic accumulators within next-generation platform architectures.

Opportunity Analysis – Composites in Next-Generation Aircraft Platforms

The increasing use of composites in next-generation aircraft platforms represents a strategic growth opportunity across structural, interior, and subsystem applications as OEMs pursue aggressive weight reduction, durability, and lifecycle-efficiency targets. New aircraft programs and platform upgrades emphasize higher composite content to improve fuel efficiency, extend range, and lower total operating costs, while also enabling greater design freedom for complex geometries and integrated structures. This shift is reinforced by the parallel transition toward more electric aircraft architectures, where lightweight materials directly support higher power density requirements and improved energy efficiency across onboard systems.

Beyond primary structures, composites are gaining traction in secondary components, housings, and functional assemblies that benefit from corrosion resistance, vibration damping, and thermal stability. Emerging electric and hybrid-electric propulsion concepts further amplify demand for lightweight enclosures, structural supports, and energy-related subsystems where mass savings translate into meaningful performance gains. The opportunity is most actionable through early-stage design partnerships with airframers, tier suppliers, and research organizations to co-develop certifiable composite solutions aligned with evolving regulatory and safety frameworks. Suppliers that can demonstrate manufacturability at aerospace quality standards, repeatable performance, and certification readiness are positioned to secure design wins and embed into long-cycle aircraft programs, creating durable, high-value participation in future fleet upgrades and new platform launches.

Urban Air Mobility and eVTOL Platforms

Urban air mobility platforms and electric vertical takeoff and landing architectures introduce a new design envelope for fluid-power subsystems, defined by extreme power-to-weight sensitivity and tightly constrained packaging volumes. Safety-critical functions such as emergency landing gear deployment and braking energy buffering still require localized pressure storage, creating a niche role for miniaturized accumulators within otherwise electrified propulsion and actuation architectures. This application context elevates demand for composite pressure vessels and advanced sealing systems that can meet burst strength, fatigue, and thermal stability requirements while minimizing structural mass. Integration of such components into distributed actuation nodes aligns with the modular system layouts characteristic of eVTOL airframes.

At the value-chain level, entry into UAM platforms reallocates development and qualification effort toward lightweight composite manufacturing, aerospace-grade liner materials, and compact valving assemblies capable of meeting stringent safety certification thresholds. Regulatory pathways for novel aircraft categories impose conservative validation regimes for pressure-containing components, increasing testing scope and compliance cost for lightweight accumulator designs. The convergence of electrified propulsion with residual hydraulic safety functions embeds specialized accumulators within next-generation mobility supply chains, structurally expanding addressable demand for ultra-lightweight, certified pressure storage solutions tailored to emerging aerial mobility ecosystems.

Category-wise Analysis

Material Type Insights

Steel is expected to dominate the aircraft accumulator materials market, accounting for approximately 52% share in 2026, underpinned by its entrenched role in legacy and in-production commercial aircraft programs across landing gear, braking, and primary hydraulic workflows. Adoption remains anchored by proven fatigue resistance, high-pressure tolerance for demanding duty cycles, and comparatively favorable unit economics versus advanced alloys and composites, with OEMs and MRO providers prioritizing qualification continuity, supply chain reliability, and standardized repair processes in high-utilization fleets. Vendors such as Parker Hannifin, Safran Landing Systems, and Eaton Aerospace are expanding certified steel accumulator portfolios with service kits and overhaul programs to lock in fleet workflows and long-term support contracts. This combination of mature qualification pathways, ecosystem lock-in, and predictable aftermarket demand sustains steel’s dominance within structured deployment models.

Composites are anticipated to be the fastest-growing segment, driven by weight-reduction imperatives and performance limitations of metallic housings across wide-body aircraft, next-generation narrowbodies, and emerging eVTOL platforms. Growth is being catalyzed by advances in carbon-fiber reinforced polymer architectures, filament winding, and resin systems qualified for high-pressure cyclic loads, which materially improve mass efficiency and corrosion immunity without compromising burst strength. Accelerating adoption is supported by digital twins for pressure vessel validation, automated fiber placement, and integrated health monitoring, lowering qualification friction for first-time adopters. Companies including Parker Hannifin, Senior Aerospace, and Liebherr-Aerospace are scaling composite accumulator platforms and hybrid material designs to capture early-cycle demand and embed switching costs.

Application Insights

Landing gear is expected to dominate, accounting for approximately 40% share in 2026, underpinned by its entrenched role in safety-critical hydraulic workflows across commercial aviation, regional aircraft, and military platforms. Adoption remains anchored by the non-discretionary requirement for emergency extension, retraction damping, and shock absorption under high load cycles, with OEMs and operators prioritizing qualification continuity, redundancy architectures, and certified reliability in high-utilization fleets. Ongoing platform evolution, including health-monitoring sensors, digitally validated pressure vessels, and improved sealing systems, continues to reinforce replacement cycles and utilization intensity. Vendors such as Safran Landing Systems, Liebherr-Aerospace, and Parker Hannifin are expanding landing-gear-specific accumulator portfolios with integrated actuation modules and lifecycle service programs to lock in enterprise workflows and long-term support contracts.

Braking systems are anticipated to be the fastest-growing segment, driven by rising operational intensity, tighter stopping-distance requirements, and performance constraints of legacy hydraulic buffering across high-cycle commercial fleets and next-generation aircraft architectures. Growth is being catalyzed by brake-by-wire integration, advanced anti-skid control, and higher-energy dissipation requirements, which materially improve braking responsiveness, thermal management, and safety margins. Companies including Honeywell Aerospace, Collins Aerospace, and Parker Hannifin are scaling braking-optimized accumulator platforms and service models to capture early-cycle demand and embed switching costs.

Regional Insights

North America Aerospace Accumulator Market Trends

North America is expected to remain the leading market, accounting for approximately 38% of global demand in 2026, supported by deep enterprise penetration, a dense tier-supplier base, and strong alignment between regulatory frameworks and industrial certification regimes. The region is positioned to retain structural dominance as fleet modernization, compliance-driven retrofits, and platform standardization are set to prioritize high-reliability hydraulic subsystems. Technology adoption is expected to concentrate on digital health monitoring, predictive maintenance interfaces, and lightweight architectures, which are projected to raise replacement value rather than expand unit volumes. Policy coordination and certification practices are set to continue shaping procurement behavior, sustaining a premiumized market structure. The regional industrial ecosystem is anticipated to favor scale, qualification depth, and platform commonality, positioning North America to lead standards diffusion and supplier consolidation across global programs.

The U.S. is expected to serve as the regional anchor, shaping momentum through its regulatory architecture, platform concentration, and procurement signaling. Industry structure is anticipated to favor a small group of platform leaders that integrate materials science, controls, and aftermarket services, with strategies increasingly oriented toward software-enabled diagnostics and modular upgrade paths. Investment flows are likely to prioritize qualification infrastructure and supply-chain resilience, reinforcing a service-led monetization model. Technology adoption is set to accelerate around smart components and condition-based maintenance, while vendor strategies are expected to emphasize long-cycle contracts and ecosystem partnerships.

Asia Pacific Aerospace Accumulator Market Trends

Asia Pacific is expected to register the fastest growth trajectory in demand, as industrial scaling, localized supply-chain development, and rapid fleet expansion accelerate subsystem adoption across commercial and defense platforms. Demand is anticipated to be reinforced by aircraft induction programs and expanding MRO networks, while supply is likely to deepen through joint ventures, technology transfer, and progressive localization of critical components. Technology adoption is projected to prioritize manufacturability, modular designs, and reliability improvements that support high-utilization fleets, with growing emphasis on condition-based maintenance to optimize lifecycle performance. Policy coordination and industrial programs are set to reduce qualification frictions and improve export readiness, positioning the region to capture incremental share through scale-driven economics and platform participation.

China is expected to serve as the regional anchor, shaping momentum through platform localization strategies and state-supported industrial ecosystems. Industry structure is anticipated to evolve toward vertically coordinated clusters that combine materials processing, component fabrication, and system integration, while vendor strategies are likely to emphasize co-development models with global OEMs to accelerate capability maturity. Investment flows are set to prioritize production tooling, testing infrastructure, and workforce specialization, reinforcing throughput and quality assurance. Technology adoption is anticipated to advance around localized manufacturing, digital quality systems, and scalable design architectures, positioning the region to convert volume growth into durable supplier competitiveness and sustained participation in global aircraft programs.

Europe Aerospace Accumulator Market Trends

Europe is expected to remain a structurally mature and strategically influential market, with growth anchored in compliance-driven upgrades, sustainability mandates, and platform-level optimization rather than greenfield capacity expansion. Demand is anticipated to be reinforced by fleet renewal cycles and retrofit programs aligned with decarbonization pathways, while supply is likely to remain distributed across specialized precision engineering clusters serving major airframe programs. Technology adoption is projected to prioritize lightweight architectures, hybridized subsystem designs, and digitally enabled reliability management, reinforcing replacement value and lifecycle monetization. Policy alignment is set to continue steering procurement criteria toward environmental performance and system efficiency.

Germany is expected to function as the regional anchor, shaping industrial momentum through its concentration of advanced manufacturing capabilities and integration within continental airframe supply chains. Investment flows are likely to concentrate on advanced manufacturing processes and certification infrastructure, reinforcing supply-chain resilience and technical depth. Technology adoption is set to advance around composite-intensive designs and hybridized hydraulic architectures, positioning European vendors to compete on efficiency, environmental performance, and compliance credibility within global programs.

Competitive Landscape

The aerospace accumulator market exhibits a moderately consolidated structure, with a concentrated top tier of global incumbents and a fragmented base of specialized suppliers. Market leadership rests with diversified aerospace and motion control groups that embed accumulators within broader hydraulic and actuation system portfolios, enabling them to compete as integrated solution providers rather than component-only vendors.

Competitive positioning centers on technological breadth, certification depth, and the ability to deliver lightweight, high-reliability, and increasingly smart hydraulic solutions that support next-generation aircraft architectures. Niche manufacturers remain active in mission-specific and defense-tailored applications, but their scale limitations and narrower certification coverage constrain participation in large fleet programs and global platform rollouts.

Key Industry Highlights:

- In January 2026, the company sold its Aerostructures business and announced a share buyback program, refocusing its efforts on its core fluid conveyance and high-technology component sectors.

- In November 2025, Senior plc became a member of the HAPSS consortium for hydrogen aircraft propulsion, aiming to advance fluid conveyance and thermal management solutions for zero-emission liquid hydrogen propulsion systems.

Companies Covered in Aerospace Accumulator Market

- Parker Hannifin

- Eaton Corporation

- Triumph Group

- Safran

- Circor Aerospace

- GKN Aerospace

- Liebherr-International AG

- Senior plc

- Crane Aerospace & Electronics

- Hayley Group

- Ametek

- APPH

- Arkwin Industries

- Moog Inc.

- Woodward

- Valcor Engineering Corporation

- Beaver Aerospace & Defense

Frequently Asked Questions

The global aerospace accumulator market is projected to be valued at US$1.8 billion in 2026 and is expected to reach US$2.7 billion by 2033, driven by the recovery in commercial aircraft production and the integration of advanced hydraulic systems in More Electric Aircraft (MEA) architectures.

The shift toward decentralized, point-of-use hydraulic actuation increases the unit intensity of compact, high-response accumulators per airframe to buffer pressure transients and ensure fault tolerance. This architectural evolution elevates accumulators from passive components to critical enablers of electrified flight control and braking systems.

The aerospace accumulator market is forecast to grow at a CAGR of 6.0% from 2026 to 2033, reflecting steady demand from rising narrow-body deliveries and increasing hydraulic system complexity in next-generation platforms.

North America is the leading regional market, accounting for approximately 38% share, anchored by its concentration of major aircraft OEMs, tier-1 suppliers, and mature MRO infrastructure. Asia Pacific is the fastest-growing region, driven by accelerating fleet expansion, indigenous manufacturing programs, and localized supply-chain development.

The aerospace accumulator market is moderately consolidated, with leadership from diversified aerospace suppliers such as Parker Hannifin, Eaton Corporation, and Safran, which embed accumulators within broader hydraulic and actuation system portfolios. Other significant players include Triumph Group, Liebherr-International, and Senior plc, competing through certification depth and lightweight material innovation.